Charles Sturt University ACC568 Case Study: Auditing of API

VerifiedAdded on 2023/03/17

|20

|4344

|57

Case Study

AI Summary

This case study analyzes the audit of Always Precise Instruments Private Limited (API). It begins by identifying potential audit risks associated with various financial ratios, such as current ratio, quick assets ratio, return on equity, and others, providing corresponding audit procedures to mitigate these risks. The analysis further explores weaknesses in API's internal control system, detailing specific vulnerabilities and recommending audit procedures to address them. Furthermore, the study evaluates the selection of samples for testing purposes, aligning these methods with the audit assertions. The case study also examines the memorandum from the audit manager to address specific audit situations and provides detailed audit procedures. The study also assesses the sampling method which aligns with the audit assertions.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

Identifying potential audit risks and audit procedures for overcoming those risks:..................2

Weaknesses in internal control and audit procedures:.............................................................10

Selection of samples for testing purpose:.................................................................................13

References:...............................................................................................................................17

Table of Contents

Identifying potential audit risks and audit procedures for overcoming those risks:..................2

Weaknesses in internal control and audit procedures:.............................................................10

Selection of samples for testing purpose:.................................................................................13

References:...............................................................................................................................17

2AUDITING

Memorandum

To: Wayne Wiadrowski

From: The Audit Manager of Always Precise Instruments Private Limited (API)

Date: 10/05/2019

Subject: Addressing Particular Audit Situations

Different issues could be observed in the financial ratios of Samway Baker Fitzgerald

(SBF) accompanied by certain loopholes in the internal control system of the organisation.

The provided case has certain number of ratios, which are deemed to be at risk. This

mandates the need for the auditor to conduct thorough investigation of the different line items

in the financial statements of Always Precise Instruments Private Limited (API). This would

assist the auditors in finding out whether there is any misstatement associated with the

financial reports of the organisation and accordingly, appropriate audit procedures would be

developed for minimising misstatement risk. Therefore, discussion would be made in terms

of identification of ratios having the potential of audit risk and accordingly, appropriate audit

procedures would be suggested for overcoming them. Moreover, the memorandum

emphasises on the weaknesses in internal control, which could contribute towards audit risk

along with the audit procedures for dealing with such risk. Finally, evaluation would be made

of the sampling method, which aligns with the audit assertions.

Identifying potential audit risks and audit procedures for overcoming those risks:

Ratio Analysis Audit Risk Audit Procedures to

reduce risk

Current ratio The ratio is seen to

increase from 2017

The rise in this ratio

of API denotes the

The ratio needs to be

reviewed over

Memorandum

To: Wayne Wiadrowski

From: The Audit Manager of Always Precise Instruments Private Limited (API)

Date: 10/05/2019

Subject: Addressing Particular Audit Situations

Different issues could be observed in the financial ratios of Samway Baker Fitzgerald

(SBF) accompanied by certain loopholes in the internal control system of the organisation.

The provided case has certain number of ratios, which are deemed to be at risk. This

mandates the need for the auditor to conduct thorough investigation of the different line items

in the financial statements of Always Precise Instruments Private Limited (API). This would

assist the auditors in finding out whether there is any misstatement associated with the

financial reports of the organisation and accordingly, appropriate audit procedures would be

developed for minimising misstatement risk. Therefore, discussion would be made in terms

of identification of ratios having the potential of audit risk and accordingly, appropriate audit

procedures would be suggested for overcoming them. Moreover, the memorandum

emphasises on the weaknesses in internal control, which could contribute towards audit risk

along with the audit procedures for dealing with such risk. Finally, evaluation would be made

of the sampling method, which aligns with the audit assertions.

Identifying potential audit risks and audit procedures for overcoming those risks:

Ratio Analysis Audit Risk Audit Procedures to

reduce risk

Current ratio The ratio is seen to

increase from 2017

The rise in this ratio

of API denotes the

The ratio needs to be

reviewed over

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

to 2018; however, it

fails to match the

market benchmark.

Hence, it denotes

there is increase in

short-term assets in

opposition to short-

term liabilities. The

strategy of API might

be to disclose

increased working

capital available in

the business. Such

depiction would

assist the

organisation in

raising its credit

terms and better

liquidity position in

the market in the

eyes of its suppliers.

fall in short-term

debt of the

organisations, which

is the target of the

organisation in order

to remain profitable

and competitive in

the market. This

denotes towards the

potential audit risk,

in which the

management of API

might inflate their

current assets in

order to show decline

in debt position

(Abbott et al., 2016).

different reporting

period. More

precisely, it is needed

to check current

assets as well as

current liabilities

accompanied by

details of the

transactions in order

to find any type of

misstatements.

Quick assets ratio There is rise in this

ratio in 2018

denoting that API is

converting its

This could be a

management strategy

to minimise

receivables by

The auditor has to

verify the cash

balance collection

from receivables in

to 2018; however, it

fails to match the

market benchmark.

Hence, it denotes

there is increase in

short-term assets in

opposition to short-

term liabilities. The

strategy of API might

be to disclose

increased working

capital available in

the business. Such

depiction would

assist the

organisation in

raising its credit

terms and better

liquidity position in

the market in the

eyes of its suppliers.

fall in short-term

debt of the

organisations, which

is the target of the

organisation in order

to remain profitable

and competitive in

the market. This

denotes towards the

potential audit risk,

in which the

management of API

might inflate their

current assets in

order to show decline

in debt position

(Abbott et al., 2016).

different reporting

period. More

precisely, it is needed

to check current

assets as well as

current liabilities

accompanied by

details of the

transactions in order

to find any type of

misstatements.

Quick assets ratio There is rise in this

ratio in 2018

denoting that API is

converting its

This could be a

management strategy

to minimise

receivables by

The auditor has to

verify the cash

balance collection

from receivables in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

receivables into cash

quickly so that the

current business

obligations could be

covered effectively.

However, this ratio

does not match the

market benchmark

owing to lack of

quick assets in

settling their business

dues.

converting them into

liquid assets and this

situation could create

audit risk. Moreover,

the quick asset ratio

as lower than the

market benchmark

imposes the going

concern position of

the company at risk

(Alzeban &

Gwilliam, 2014).

order to identify

overstatements in

quick assets.

Moreover, the

auditor has to review

quick assets for

verifying whether the

company has

considerable quick

assets in order to

maintain the position

of going concern

(Alzeban & Sawan,

2015).

Return on equity The decline in return

on equity could be

observed in the year

2018 in contrast to

2017 that supports

the strategy of API in

reducing debts for

remaining

competitive.

This aspect results in

likely audit risk

where API’s

management might

have overstated the

equity capital balance

in order to reduce

debts in the

accounting books.

The necessary audit

procedure would be

to analyse the

register used to issue

equity shares along

with invigilating the

resolution of the

API’s board to assure

whether equity share

capital is overstated

or not (Ball, Tyler &

receivables into cash

quickly so that the

current business

obligations could be

covered effectively.

However, this ratio

does not match the

market benchmark

owing to lack of

quick assets in

settling their business

dues.

converting them into

liquid assets and this

situation could create

audit risk. Moreover,

the quick asset ratio

as lower than the

market benchmark

imposes the going

concern position of

the company at risk

(Alzeban &

Gwilliam, 2014).

order to identify

overstatements in

quick assets.

Moreover, the

auditor has to review

quick assets for

verifying whether the

company has

considerable quick

assets in order to

maintain the position

of going concern

(Alzeban & Sawan,

2015).

Return on equity The decline in return

on equity could be

observed in the year

2018 in contrast to

2017 that supports

the strategy of API in

reducing debts for

remaining

competitive.

This aspect results in

likely audit risk

where API’s

management might

have overstated the

equity capital balance

in order to reduce

debts in the

accounting books.

The necessary audit

procedure would be

to analyse the

register used to issue

equity shares along

with invigilating the

resolution of the

API’s board to assure

whether equity share

capital is overstated

or not (Ball, Tyler &

5AUDITING

Wells, 2015).

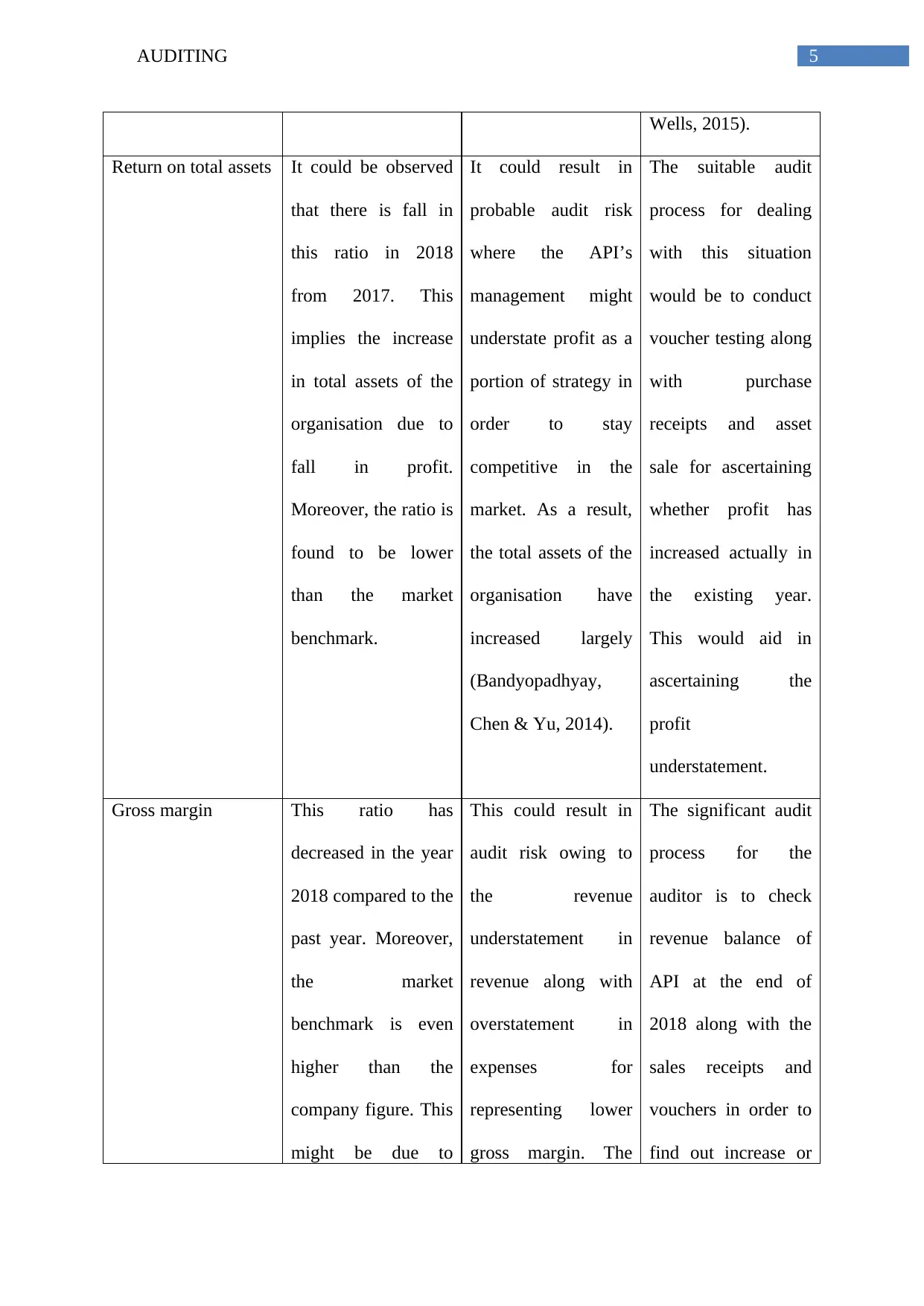

Return on total assets It could be observed

that there is fall in

this ratio in 2018

from 2017. This

implies the increase

in total assets of the

organisation due to

fall in profit.

Moreover, the ratio is

found to be lower

than the market

benchmark.

It could result in

probable audit risk

where the API’s

management might

understate profit as a

portion of strategy in

order to stay

competitive in the

market. As a result,

the total assets of the

organisation have

increased largely

(Bandyopadhyay,

Chen & Yu, 2014).

The suitable audit

process for dealing

with this situation

would be to conduct

voucher testing along

with purchase

receipts and asset

sale for ascertaining

whether profit has

increased actually in

the existing year.

This would aid in

ascertaining the

profit

understatement.

Gross margin This ratio has

decreased in the year

2018 compared to the

past year. Moreover,

the market

benchmark is even

higher than the

company figure. This

might be due to

This could result in

audit risk owing to

the revenue

understatement in

revenue along with

overstatement in

expenses for

representing lower

gross margin. The

The significant audit

process for the

auditor is to check

revenue balance of

API at the end of

2018 along with the

sales receipts and

vouchers in order to

find out increase or

Wells, 2015).

Return on total assets It could be observed

that there is fall in

this ratio in 2018

from 2017. This

implies the increase

in total assets of the

organisation due to

fall in profit.

Moreover, the ratio is

found to be lower

than the market

benchmark.

It could result in

probable audit risk

where the API’s

management might

understate profit as a

portion of strategy in

order to stay

competitive in the

market. As a result,

the total assets of the

organisation have

increased largely

(Bandyopadhyay,

Chen & Yu, 2014).

The suitable audit

process for dealing

with this situation

would be to conduct

voucher testing along

with purchase

receipts and asset

sale for ascertaining

whether profit has

increased actually in

the existing year.

This would aid in

ascertaining the

profit

understatement.

Gross margin This ratio has

decreased in the year

2018 compared to the

past year. Moreover,

the market

benchmark is even

higher than the

company figure. This

might be due to

This could result in

audit risk owing to

the revenue

understatement in

revenue along with

overstatement in

expenses for

representing lower

gross margin. The

The significant audit

process for the

auditor is to check

revenue balance of

API at the end of

2018 along with the

sales receipts and

vouchers in order to

find out increase or

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

decline in revenue or

there might be

increase in cost of

sales with no change

in revenue.

objective of API

could be to show

minimised gross

margin.

decrease in revenue.

Moreover, the

auditor has to review

the expenses of the

organisation to detect

if the expenses are

overstated or not

(Bolton, 2014).

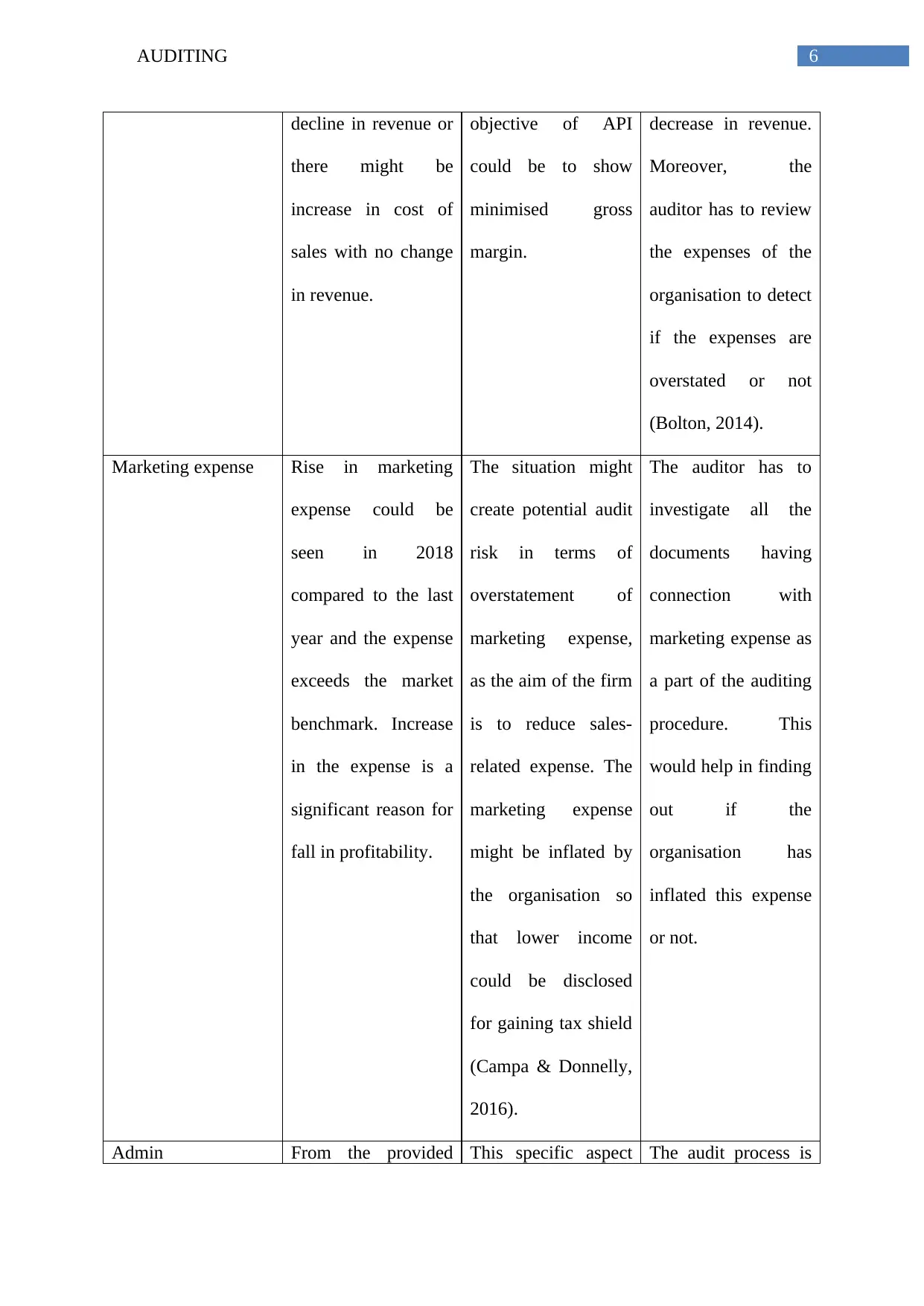

Marketing expense Rise in marketing

expense could be

seen in 2018

compared to the last

year and the expense

exceeds the market

benchmark. Increase

in the expense is a

significant reason for

fall in profitability.

The situation might

create potential audit

risk in terms of

overstatement of

marketing expense,

as the aim of the firm

is to reduce sales-

related expense. The

marketing expense

might be inflated by

the organisation so

that lower income

could be disclosed

for gaining tax shield

(Campa & Donnelly,

2016).

The auditor has to

investigate all the

documents having

connection with

marketing expense as

a part of the auditing

procedure. This

would help in finding

out if the

organisation has

inflated this expense

or not.

Admin From the provided This specific aspect The audit process is

decline in revenue or

there might be

increase in cost of

sales with no change

in revenue.

objective of API

could be to show

minimised gross

margin.

decrease in revenue.

Moreover, the

auditor has to review

the expenses of the

organisation to detect

if the expenses are

overstated or not

(Bolton, 2014).

Marketing expense Rise in marketing

expense could be

seen in 2018

compared to the last

year and the expense

exceeds the market

benchmark. Increase

in the expense is a

significant reason for

fall in profitability.

The situation might

create potential audit

risk in terms of

overstatement of

marketing expense,

as the aim of the firm

is to reduce sales-

related expense. The

marketing expense

might be inflated by

the organisation so

that lower income

could be disclosed

for gaining tax shield

(Campa & Donnelly,

2016).

The auditor has to

investigate all the

documents having

connection with

marketing expense as

a part of the auditing

procedure. This

would help in finding

out if the

organisation has

inflated this expense

or not.

Admin From the provided This specific aspect The audit process is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

expenses/sales information, it could

be witnessed that this

ratio has declined for

API in the year 2018;

however, the

budgeted figure has

been accomplished.

This aligns with the

cost reduction

strategy of API.

could create potential

audit risk associated

with understatement

of admin expenses

owing to the cost

reduction strategy of

the firm.

to check and review

different documents

like receipts and

vouchers associated

with admin expenses.

This would ascertain

whether API has

understated these

expenses or not, as

its role is deemed to

be critical in terms of

profitability

(Chambers & Odar,

2015).

Times interest earned The ratio is seen to

fall from 2017 to

2018 and it is lower

than the market

benchmark as well.

The primary reason

could be decline in

earnings leading to

inability of the

organisation in

settling interest

The decline in this

ratio could cause

potential audit risk of

misstatement of the

earnings of the

organisation in its

accounting books.

This could lead to

fall in the interest

payment of the

company (Choi, Han

In order to respond

this risk, the auditor

is liable to analyse

the alternations in

earnings of the firm

along with

modifications in the

level of debt. The

firm would obtain the

idea of finding out

any errors in its

expenses/sales information, it could

be witnessed that this

ratio has declined for

API in the year 2018;

however, the

budgeted figure has

been accomplished.

This aligns with the

cost reduction

strategy of API.

could create potential

audit risk associated

with understatement

of admin expenses

owing to the cost

reduction strategy of

the firm.

to check and review

different documents

like receipts and

vouchers associated

with admin expenses.

This would ascertain

whether API has

understated these

expenses or not, as

its role is deemed to

be critical in terms of

profitability

(Chambers & Odar,

2015).

Times interest earned The ratio is seen to

fall from 2017 to

2018 and it is lower

than the market

benchmark as well.

The primary reason

could be decline in

earnings leading to

inability of the

organisation in

settling interest

The decline in this

ratio could cause

potential audit risk of

misstatement of the

earnings of the

organisation in its

accounting books.

This could lead to

fall in the interest

payment of the

company (Choi, Han

In order to respond

this risk, the auditor

is liable to analyse

the alternations in

earnings of the firm

along with

modifications in the

level of debt. The

firm would obtain the

idea of finding out

any errors in its

8AUDITING

payment. & Lee, 2014). earnings and level of

debt.

Days in inventory As per the provided

information,

inventory turnover of

API is observed to

increase in 2018 in

contrast to 2017 and

this value seems to

be higher than the

market benchmark.

This situation is

capable of creating

audit risk, in which

the management of

API might have

inflated the ending

inventory so that the

overall inventory

level is reduced.

For dealing with this

risk, inventory count

is deemed to be vital

along with thorough

observation and

review of the same.

In this method, it

would become easy

for the auditor to

identify if there is

any closing inventory

overstatement

(Dogui, Boiral &

Heras‐Saizarbitoria,

2014).

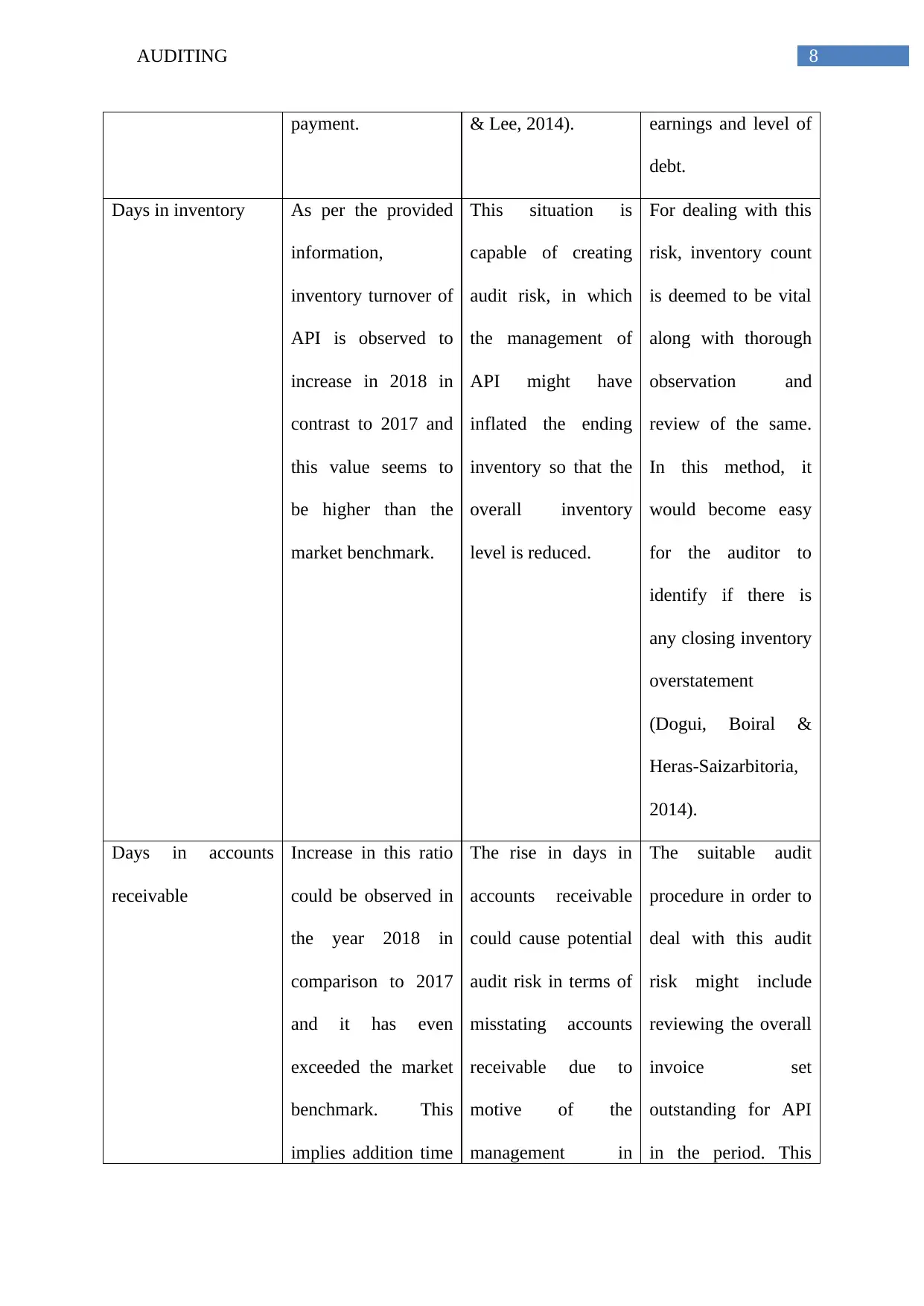

Days in accounts

receivable

Increase in this ratio

could be observed in

the year 2018 in

comparison to 2017

and it has even

exceeded the market

benchmark. This

implies addition time

The rise in days in

accounts receivable

could cause potential

audit risk in terms of

misstating accounts

receivable due to

motive of the

management in

The suitable audit

procedure in order to

deal with this audit

risk might include

reviewing the overall

invoice set

outstanding for API

in the period. This

payment. & Lee, 2014). earnings and level of

debt.

Days in inventory As per the provided

information,

inventory turnover of

API is observed to

increase in 2018 in

contrast to 2017 and

this value seems to

be higher than the

market benchmark.

This situation is

capable of creating

audit risk, in which

the management of

API might have

inflated the ending

inventory so that the

overall inventory

level is reduced.

For dealing with this

risk, inventory count

is deemed to be vital

along with thorough

observation and

review of the same.

In this method, it

would become easy

for the auditor to

identify if there is

any closing inventory

overstatement

(Dogui, Boiral &

Heras‐Saizarbitoria,

2014).

Days in accounts

receivable

Increase in this ratio

could be observed in

the year 2018 in

comparison to 2017

and it has even

exceeded the market

benchmark. This

implies addition time

The rise in days in

accounts receivable

could cause potential

audit risk in terms of

misstating accounts

receivable due to

motive of the

management in

The suitable audit

procedure in order to

deal with this audit

risk might include

reviewing the overall

invoice set

outstanding for API

in the period. This

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

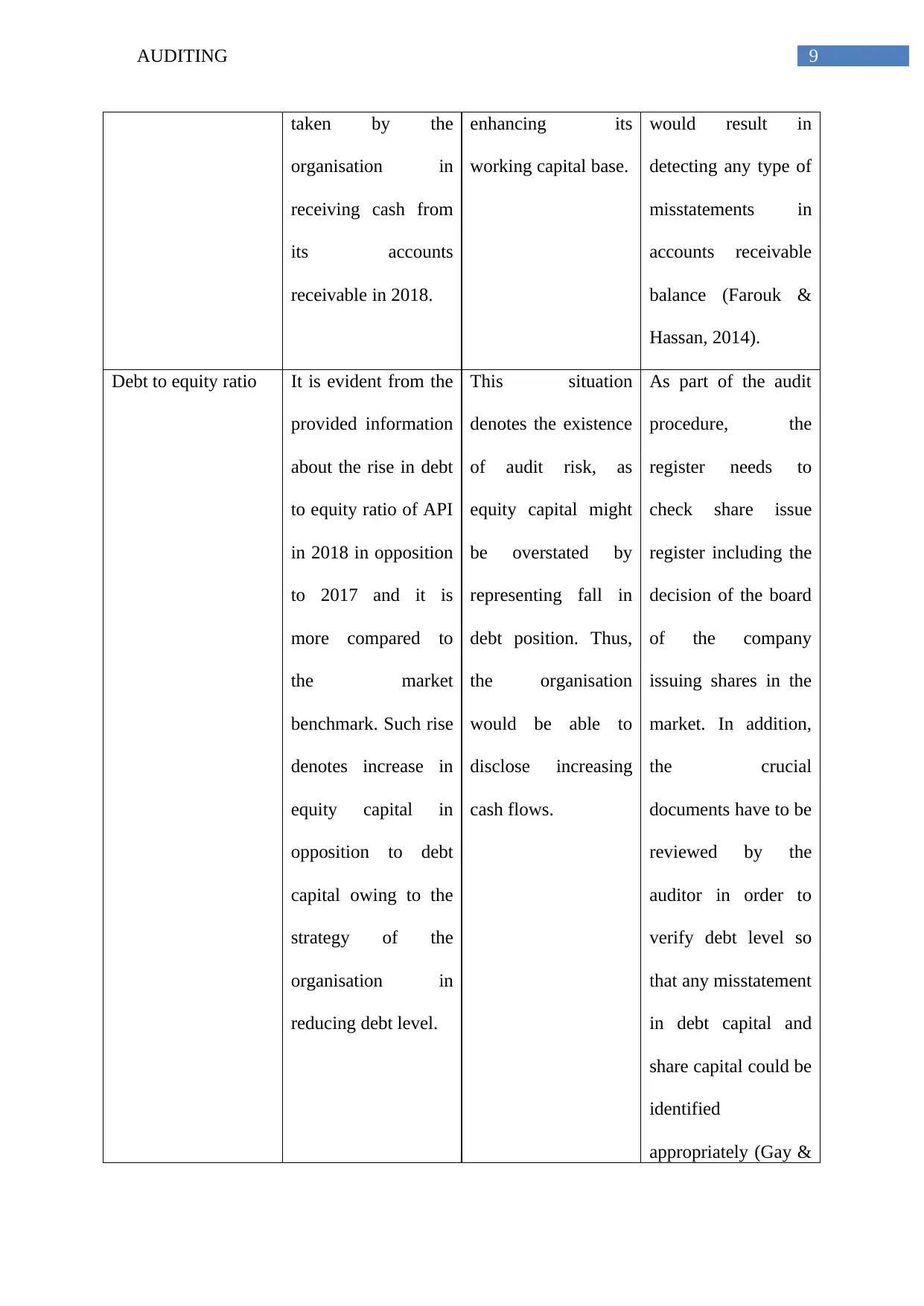

taken by the

organisation in

receiving cash from

its accounts

receivable in 2018.

enhancing its

working capital base.

would result in

detecting any type of

misstatements in

accounts receivable

balance (Farouk &

Hassan, 2014).

Debt to equity ratio It is evident from the

provided information

about the rise in debt

to equity ratio of API

in 2018 in opposition

to 2017 and it is

more compared to

the market

benchmark. Such rise

denotes increase in

equity capital in

opposition to debt

capital owing to the

strategy of the

organisation in

reducing debt level.

This situation

denotes the existence

of audit risk, as

equity capital might

be overstated by

representing fall in

debt position. Thus,

the organisation

would be able to

disclose increasing

cash flows.

As part of the audit

procedure, the

register needs to

check share issue

register including the

decision of the board

of the company

issuing shares in the

market. In addition,

the crucial

documents have to be

reviewed by the

auditor in order to

verify debt level so

that any misstatement

in debt capital and

share capital could be

identified

appropriately (Gay &

taken by the

organisation in

receiving cash from

its accounts

receivable in 2018.

enhancing its

working capital base.

would result in

detecting any type of

misstatements in

accounts receivable

balance (Farouk &

Hassan, 2014).

Debt to equity ratio It is evident from the

provided information

about the rise in debt

to equity ratio of API

in 2018 in opposition

to 2017 and it is

more compared to

the market

benchmark. Such rise

denotes increase in

equity capital in

opposition to debt

capital owing to the

strategy of the

organisation in

reducing debt level.

This situation

denotes the existence

of audit risk, as

equity capital might

be overstated by

representing fall in

debt position. Thus,

the organisation

would be able to

disclose increasing

cash flows.

As part of the audit

procedure, the

register needs to

check share issue

register including the

decision of the board

of the company

issuing shares in the

market. In addition,

the crucial

documents have to be

reviewed by the

auditor in order to

verify debt level so

that any misstatement

in debt capital and

share capital could be

identified

appropriately (Gay &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

Simnett, 2017).

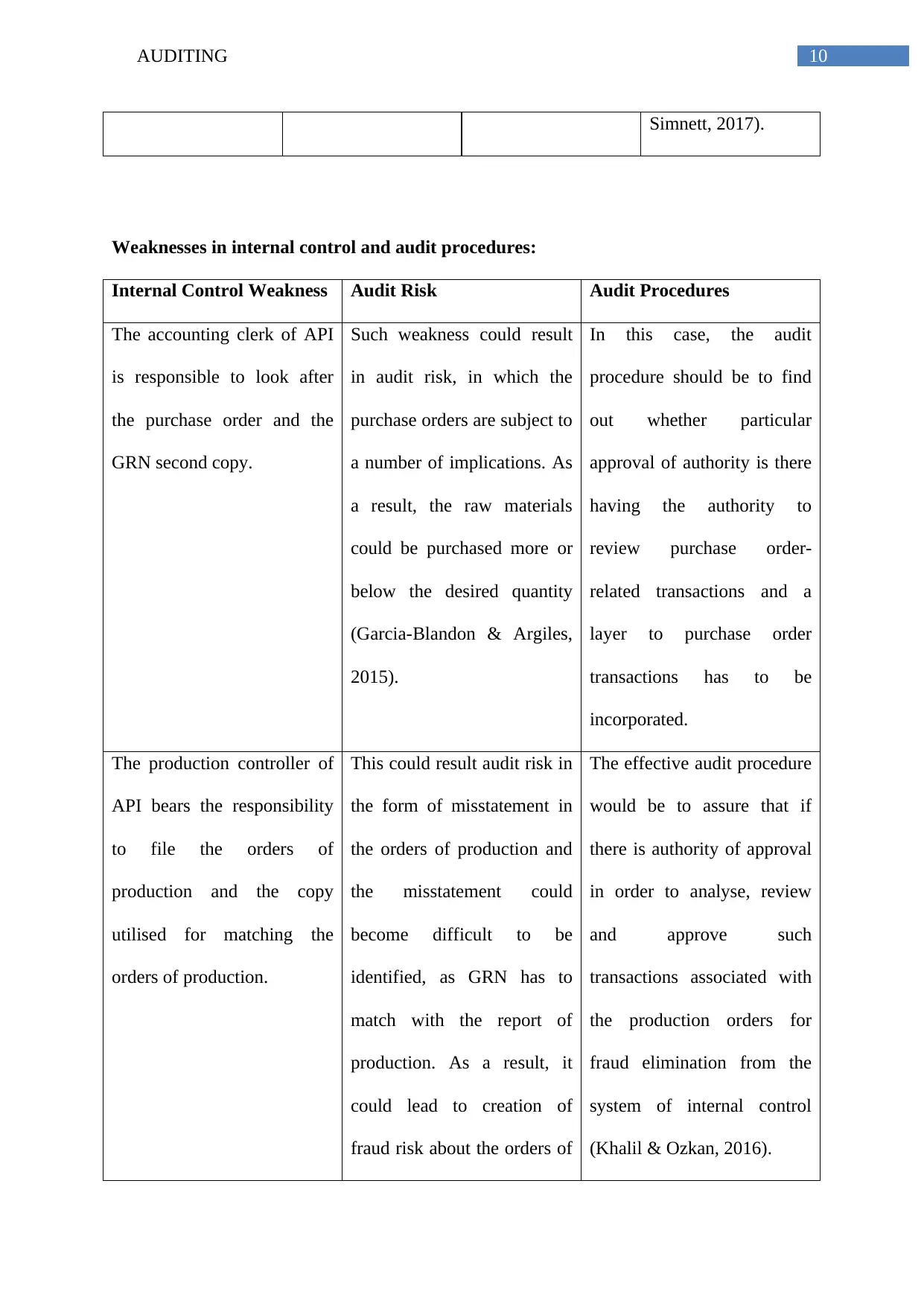

Weaknesses in internal control and audit procedures:

Internal Control Weakness Audit Risk Audit Procedures

The accounting clerk of API

is responsible to look after

the purchase order and the

GRN second copy.

Such weakness could result

in audit risk, in which the

purchase orders are subject to

a number of implications. As

a result, the raw materials

could be purchased more or

below the desired quantity

(Garcia-Blandon & Argiles,

2015).

In this case, the audit

procedure should be to find

out whether particular

approval of authority is there

having the authority to

review purchase order-

related transactions and a

layer to purchase order

transactions has to be

incorporated.

The production controller of

API bears the responsibility

to file the orders of

production and the copy

utilised for matching the

orders of production.

This could result audit risk in

the form of misstatement in

the orders of production and

the misstatement could

become difficult to be

identified, as GRN has to

match with the report of

production. As a result, it

could lead to creation of

fraud risk about the orders of

The effective audit procedure

would be to assure that if

there is authority of approval

in order to analyse, review

and approve such

transactions associated with

the production orders for

fraud elimination from the

system of internal control

(Khalil & Ozkan, 2016).

Simnett, 2017).

Weaknesses in internal control and audit procedures:

Internal Control Weakness Audit Risk Audit Procedures

The accounting clerk of API

is responsible to look after

the purchase order and the

GRN second copy.

Such weakness could result

in audit risk, in which the

purchase orders are subject to

a number of implications. As

a result, the raw materials

could be purchased more or

below the desired quantity

(Garcia-Blandon & Argiles,

2015).

In this case, the audit

procedure should be to find

out whether particular

approval of authority is there

having the authority to

review purchase order-

related transactions and a

layer to purchase order

transactions has to be

incorporated.

The production controller of

API bears the responsibility

to file the orders of

production and the copy

utilised for matching the

orders of production.

This could result audit risk in

the form of misstatement in

the orders of production and

the misstatement could

become difficult to be

identified, as GRN has to

match with the report of

production. As a result, it

could lead to creation of

fraud risk about the orders of

The effective audit procedure

would be to assure that if

there is authority of approval

in order to analyse, review

and approve such

transactions associated with

the production orders for

fraud elimination from the

system of internal control

(Khalil & Ozkan, 2016).

11AUDITING

production.

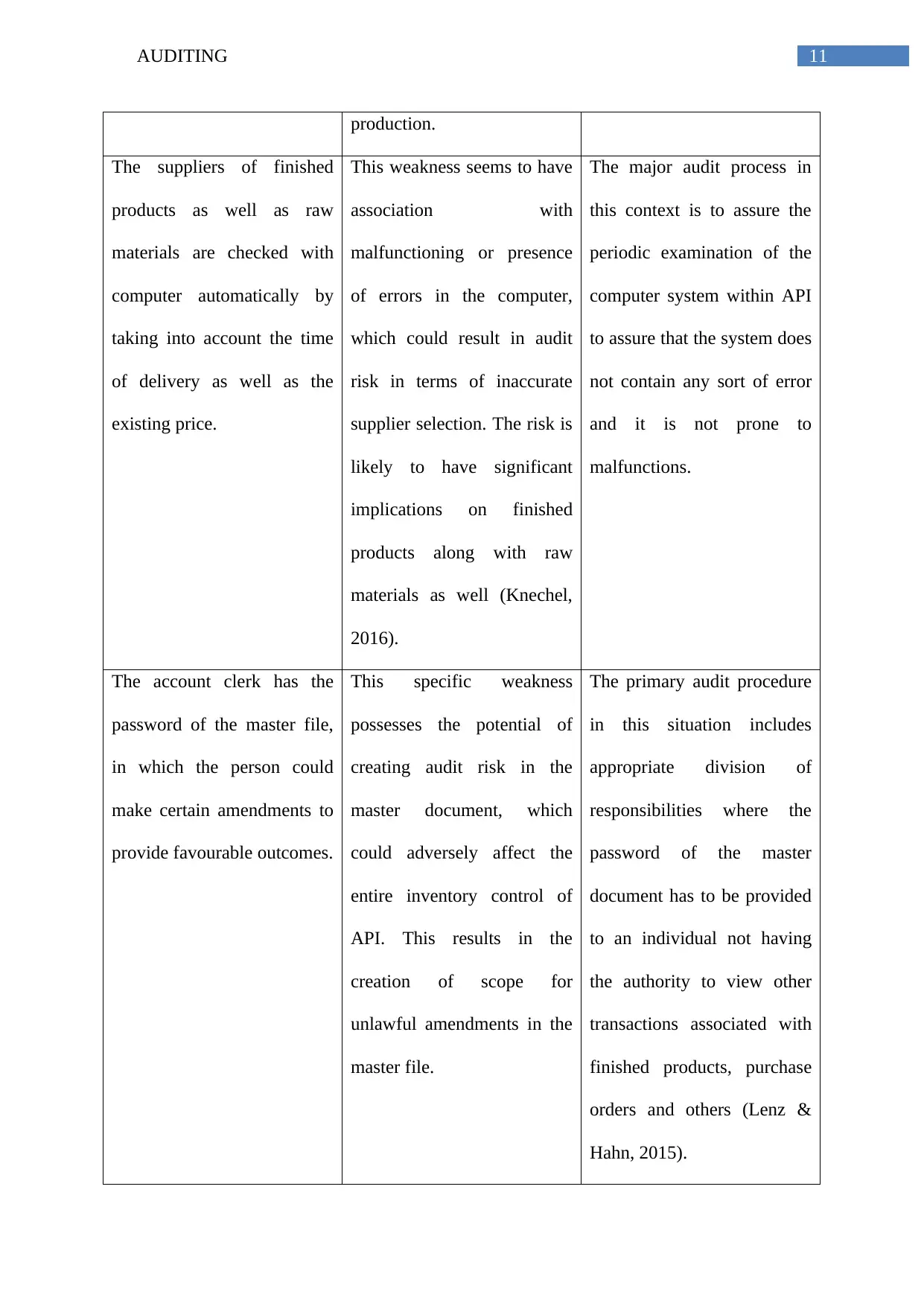

The suppliers of finished

products as well as raw

materials are checked with

computer automatically by

taking into account the time

of delivery as well as the

existing price.

This weakness seems to have

association with

malfunctioning or presence

of errors in the computer,

which could result in audit

risk in terms of inaccurate

supplier selection. The risk is

likely to have significant

implications on finished

products along with raw

materials as well (Knechel,

2016).

The major audit process in

this context is to assure the

periodic examination of the

computer system within API

to assure that the system does

not contain any sort of error

and it is not prone to

malfunctions.

The account clerk has the

password of the master file,

in which the person could

make certain amendments to

provide favourable outcomes.

This specific weakness

possesses the potential of

creating audit risk in the

master document, which

could adversely affect the

entire inventory control of

API. This results in the

creation of scope for

unlawful amendments in the

master file.

The primary audit procedure

in this situation includes

appropriate division of

responsibilities where the

password of the master

document has to be provided

to an individual not having

the authority to view other

transactions associated with

finished products, purchase

orders and others (Lenz &

Hahn, 2015).

production.

The suppliers of finished

products as well as raw

materials are checked with

computer automatically by

taking into account the time

of delivery as well as the

existing price.

This weakness seems to have

association with

malfunctioning or presence

of errors in the computer,

which could result in audit

risk in terms of inaccurate

supplier selection. The risk is

likely to have significant

implications on finished

products along with raw

materials as well (Knechel,

2016).

The major audit process in

this context is to assure the

periodic examination of the

computer system within API

to assure that the system does

not contain any sort of error

and it is not prone to

malfunctions.

The account clerk has the

password of the master file,

in which the person could

make certain amendments to

provide favourable outcomes.

This specific weakness

possesses the potential of

creating audit risk in the

master document, which

could adversely affect the

entire inventory control of

API. This results in the

creation of scope for

unlawful amendments in the

master file.

The primary audit procedure

in this situation includes

appropriate division of

responsibilities where the

password of the master

document has to be provided

to an individual not having

the authority to view other

transactions associated with

finished products, purchase

orders and others (Lenz &

Hahn, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.