ACC621 Auditing: Financial Statement Analysis and Audit Procedures

VerifiedAdded on 2023/06/07

|14

|2666

|174

Report

AI Summary

This report provides a comprehensive analysis of auditing practices, focusing on the preliminary assessment of materiality, analytical review of income statements, and trend analysis of key accounts. It begins with an overview of the audit process, emphasizing the importance of client involvement and sound planning. The preliminary materiality assessment is based on a percentage of sales, and the report discusses the impact of changes in sales on the audit budget. An analytical review of the income statement identifies accounts with significant volatility, including depreciation, repairs and maintenance, superannuation, and interest income. Specific audit procedures are recommended for each identified account to gather relevant evidence and address potential misstatements. The report also evaluates the appropriateness of excluding fraud risk assessment, concluding that a thorough audit and corporate governance review are necessary. The analysis uses data from Cobalt Enterprise's financial statements to illustrate these concepts. Desklib provides resources like this to aid students in their studies.

Running head: ISSUE IN AUDITING PRACTICE

Issues in Auditing Practice

Name of the Student:

Name of the University:

Author’s Note:

Issues in Auditing Practice

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ISSUES IN AUDITING PROJECT

Executive Summary

The aim of the project is to study about the various concept involved in auditing. The

preliminary assessment of materiality for the financial reporting is analyzed. The preliminary

assessment of the audit budget and the effect on changing the same is discussed. An analytical

review of the income statement is performed from the trial balance. Trend Analysis was

performed based on four account where the change in the value showed dispersion and volatility.

The identified account was discussed with relevant audit procedures.

Executive Summary

The aim of the project is to study about the various concept involved in auditing. The

preliminary assessment of materiality for the financial reporting is analyzed. The preliminary

assessment of the audit budget and the effect on changing the same is discussed. An analytical

review of the income statement is performed from the trial balance. Trend Analysis was

performed based on four account where the change in the value showed dispersion and volatility.

The identified account was discussed with relevant audit procedures.

2ISSUES IN AUDITING PROJECT

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

1) Preliminary Assessment of Materiality of the Financial Report..........................................3

2) Analytical Review of the Income Statement........................................................................4

3) Trend Analysis of Income Statement Accounts...................................................................5

4) Audit Procedures..................................................................................................................8

5) Overview Evaluation of the Company.................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Appendix........................................................................................................................................13

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................3

1) Preliminary Assessment of Materiality of the Financial Report..........................................3

2) Analytical Review of the Income Statement........................................................................4

3) Trend Analysis of Income Statement Accounts...................................................................5

4) Audit Procedures..................................................................................................................8

5) Overview Evaluation of the Company.................................................................................9

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Appendix........................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ISSUES IN AUDITING PROJECT

Introduction

The Audit process involves sound planning and construction of creating an

communication and involvement between the auditor and the client. The Audit process consists

of four stages like the Planning stage, Fieldwork task, for reporting of audit work performed and

for follow up report. There should be involvement of client at every stage of the audit process

(DeFon and Zhang 2014). The preliminary assessment of the audit process was done keeping in

context with sales or revenue of the company. The analytical review of the income statement was

performed in order to get a trend analysis of the same. The trend analysis and the accounts

identified in the income statement of the company was further taken into screening, which

showed a greater degree of volatility and dispersion. The audit procedure for each of the

identified account was performed in order to get a relevant evidence for the volatility of the same

(Louwers et al. 2015).

Discussion

1) Preliminary Assessment of Materiality of the Financial Report

The preliminary assessment of Materiality of the financial report was carried on by talking

the percentage breakdown of sales. The audit report preliminary assessment was taken to be

around 5% of the Total Sales/ Revenue of the company. In our example, the following

preliminary assessment budget was set at $ 15,000. The sales of the company was around

131,967. The 5% preliminary assessment calculated would be around (131967*5%), which is

equal to $6598. The 5% breakdown of preliminary assessment was taken as an assumption in

our example. The budget set up by the auditors are in well estimate with the preliminary

budget decided.

Introduction

The Audit process involves sound planning and construction of creating an

communication and involvement between the auditor and the client. The Audit process consists

of four stages like the Planning stage, Fieldwork task, for reporting of audit work performed and

for follow up report. There should be involvement of client at every stage of the audit process

(DeFon and Zhang 2014). The preliminary assessment of the audit process was done keeping in

context with sales or revenue of the company. The analytical review of the income statement was

performed in order to get a trend analysis of the same. The trend analysis and the accounts

identified in the income statement of the company was further taken into screening, which

showed a greater degree of volatility and dispersion. The audit procedure for each of the

identified account was performed in order to get a relevant evidence for the volatility of the same

(Louwers et al. 2015).

Discussion

1) Preliminary Assessment of Materiality of the Financial Report

The preliminary assessment of Materiality of the financial report was carried on by talking

the percentage breakdown of sales. The audit report preliminary assessment was taken to be

around 5% of the Total Sales/ Revenue of the company. In our example, the following

preliminary assessment budget was set at $ 15,000. The sales of the company was around

131,967. The 5% preliminary assessment calculated would be around (131967*5%), which is

equal to $6598. The 5% breakdown of preliminary assessment was taken as an assumption in

our example. The budget set up by the auditors are in well estimate with the preliminary

budget decided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ISSUES IN AUDITING PROJECT

The effect on the preliminary assessment would be such that the change in sales or if

there will be change in the base figure approached for the assessment budget then the whole

of the budgetary process and the preliminary assessment would be affected.

2) Analytical Review of the Income Statement

Analytical Review in the form of trend analysis of the income statement from the trial

balance is given below:

Figure 1: Income Statement of Cobalt Enterprise

Source: Appendix 1

Sales

Cost of Sales

Gross Profit

Expenses

Bank Charges

Depreciation

Interest expense

Printing

Repairs and Maintenance

Wages

Superannuation

Income

Consultancy Fees

Interest Income

Net Profit

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Incom e Statement

2016-17 2015-16

The effect on the preliminary assessment would be such that the change in sales or if

there will be change in the base figure approached for the assessment budget then the whole

of the budgetary process and the preliminary assessment would be affected.

2) Analytical Review of the Income Statement

Analytical Review in the form of trend analysis of the income statement from the trial

balance is given below:

Figure 1: Income Statement of Cobalt Enterprise

Source: Appendix 1

Sales

Cost of Sales

Gross Profit

Expenses

Bank Charges

Depreciation

Interest expense

Printing

Repairs and Maintenance

Wages

Superannuation

Income

Consultancy Fees

Interest Income

Net Profit

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Incom e Statement

2016-17 2015-16

5ISSUES IN AUDITING PROJECT

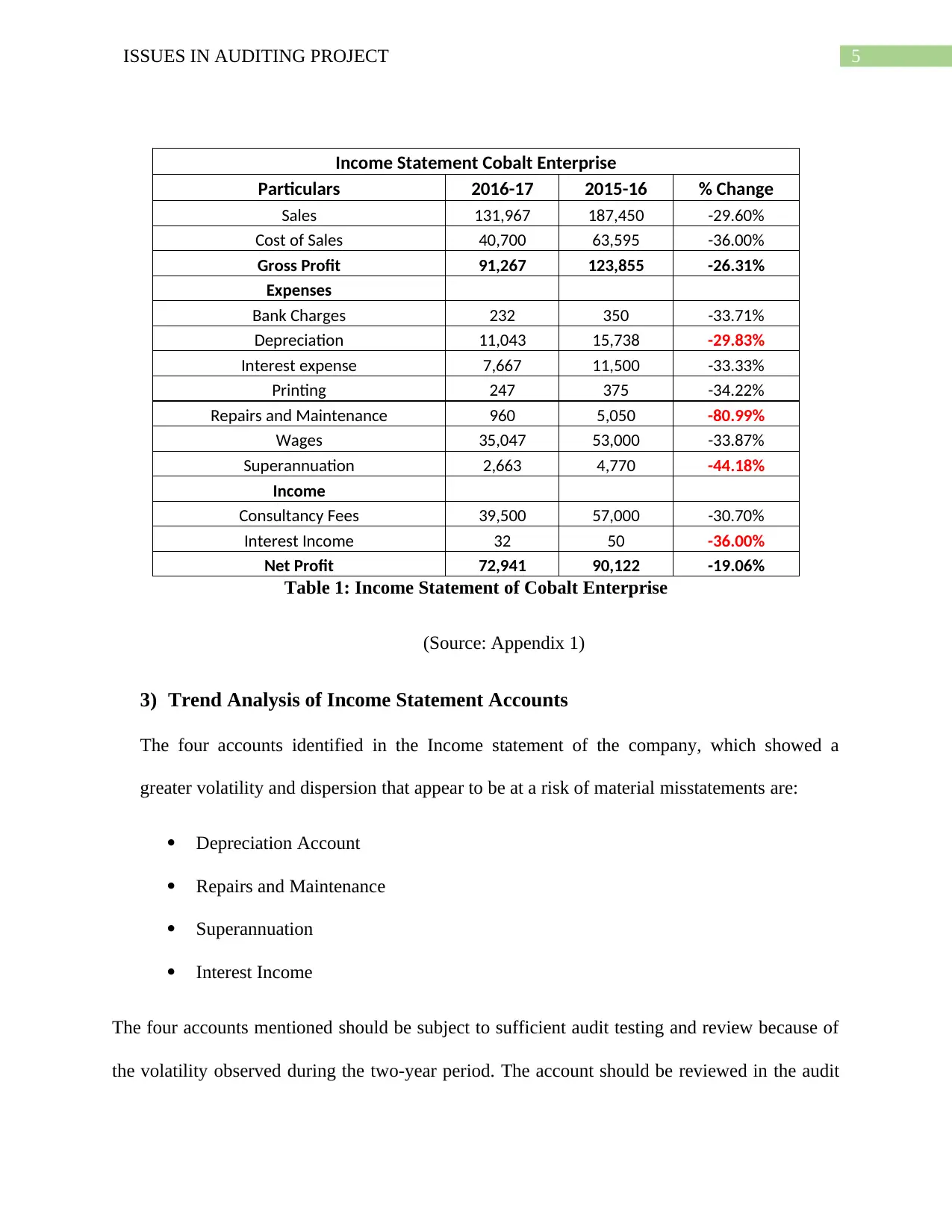

Income Statement Cobalt Enterprise

Particulars 2016-17 2015-16 % Change

Sales 131,967 187,450 -29.60%

Cost of Sales 40,700 63,595 -36.00%

Gross Profit 91,267 123,855 -26.31%

Expenses

Bank Charges 232 350 -33.71%

Depreciation 11,043 15,738 -29.83%

Interest expense 7,667 11,500 -33.33%

Printing 247 375 -34.22%

Repairs and Maintenance 960 5,050 -80.99%

Wages 35,047 53,000 -33.87%

Superannuation 2,663 4,770 -44.18%

Income

Consultancy Fees 39,500 57,000 -30.70%

Interest Income 32 50 -36.00%

Net Profit 72,941 90,122 -19.06%

Table 1: Income Statement of Cobalt Enterprise

(Source: Appendix 1)

3) Trend Analysis of Income Statement Accounts

The four accounts identified in the Income statement of the company, which showed a

greater volatility and dispersion that appear to be at a risk of material misstatements are:

Depreciation Account

Repairs and Maintenance

Superannuation

Interest Income

The four accounts mentioned should be subject to sufficient audit testing and review because of

the volatility observed during the two-year period. The account should be reviewed in the audit

Income Statement Cobalt Enterprise

Particulars 2016-17 2015-16 % Change

Sales 131,967 187,450 -29.60%

Cost of Sales 40,700 63,595 -36.00%

Gross Profit 91,267 123,855 -26.31%

Expenses

Bank Charges 232 350 -33.71%

Depreciation 11,043 15,738 -29.83%

Interest expense 7,667 11,500 -33.33%

Printing 247 375 -34.22%

Repairs and Maintenance 960 5,050 -80.99%

Wages 35,047 53,000 -33.87%

Superannuation 2,663 4,770 -44.18%

Income

Consultancy Fees 39,500 57,000 -30.70%

Interest Income 32 50 -36.00%

Net Profit 72,941 90,122 -19.06%

Table 1: Income Statement of Cobalt Enterprise

(Source: Appendix 1)

3) Trend Analysis of Income Statement Accounts

The four accounts identified in the Income statement of the company, which showed a

greater volatility and dispersion that appear to be at a risk of material misstatements are:

Depreciation Account

Repairs and Maintenance

Superannuation

Interest Income

The four accounts mentioned should be subject to sufficient audit testing and review because of

the volatility observed during the two-year period. The account should be reviewed in the audit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ISSUES IN AUDITING PROJECT

process to get know how about such greater volatility and dispersion in the account (Knechel and

Salterio 2016). The account to be studied should give a brief analysis of the different components

linked to the same and reasons and the trend for the same.

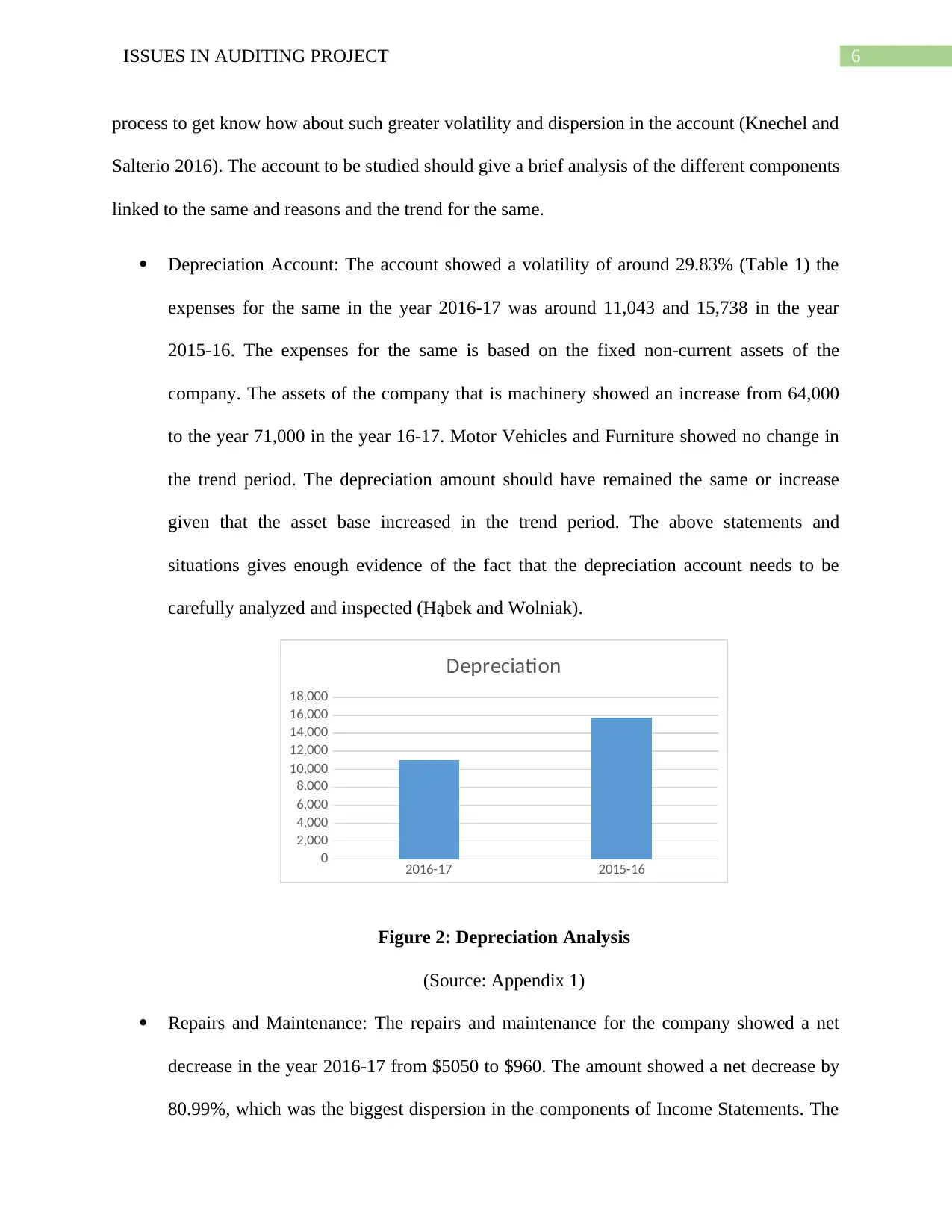

Depreciation Account: The account showed a volatility of around 29.83% (Table 1) the

expenses for the same in the year 2016-17 was around 11,043 and 15,738 in the year

2015-16. The expenses for the same is based on the fixed non-current assets of the

company. The assets of the company that is machinery showed an increase from 64,000

to the year 71,000 in the year 16-17. Motor Vehicles and Furniture showed no change in

the trend period. The depreciation amount should have remained the same or increase

given that the asset base increased in the trend period. The above statements and

situations gives enough evidence of the fact that the depreciation account needs to be

carefully analyzed and inspected (Hąbek and Wolniak).

Figure 2: Depreciation Analysis

(Source: Appendix 1)

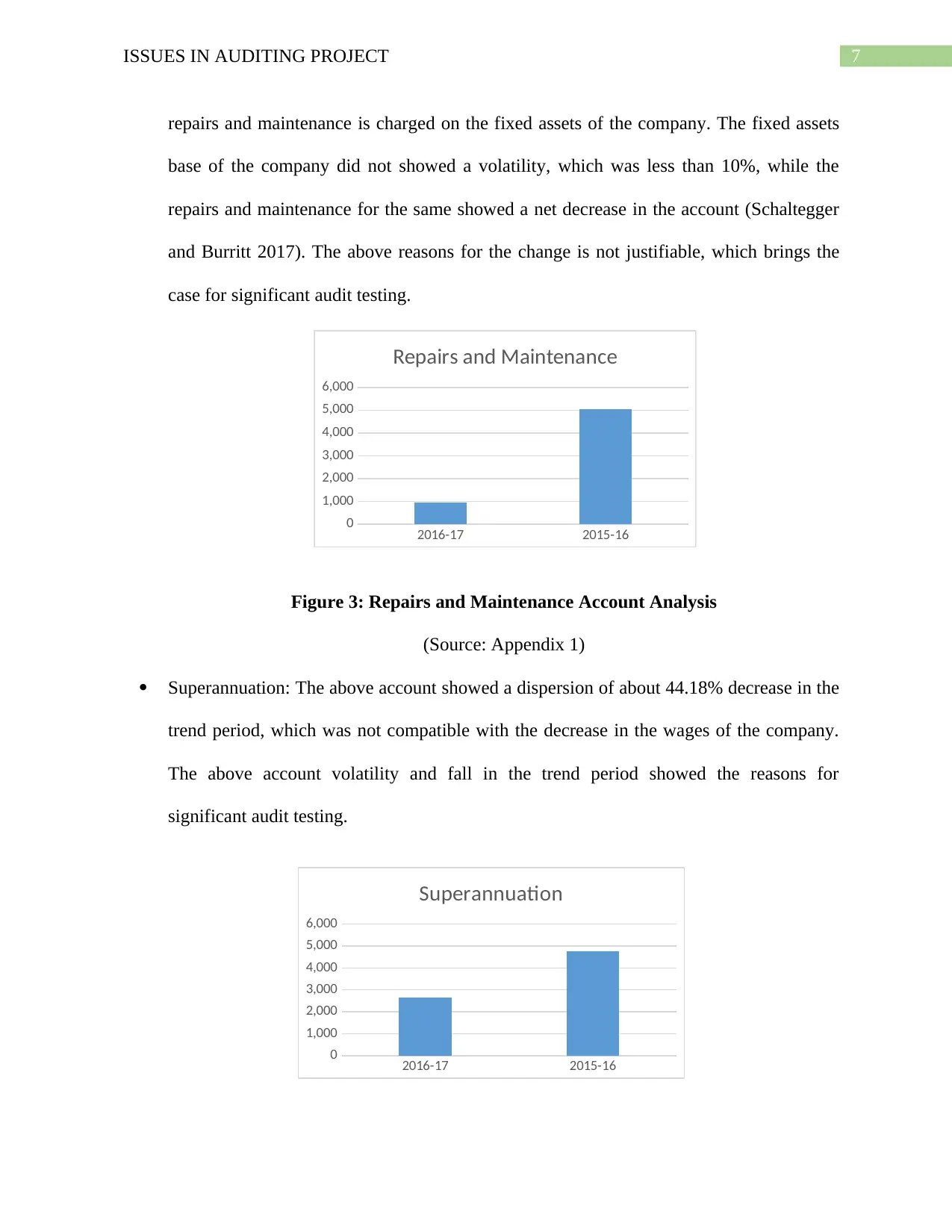

Repairs and Maintenance: The repairs and maintenance for the company showed a net

decrease in the year 2016-17 from $5050 to $960. The amount showed a net decrease by

80.99%, which was the biggest dispersion in the components of Income Statements. The

2016-17 2015-16

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Depreciation

process to get know how about such greater volatility and dispersion in the account (Knechel and

Salterio 2016). The account to be studied should give a brief analysis of the different components

linked to the same and reasons and the trend for the same.

Depreciation Account: The account showed a volatility of around 29.83% (Table 1) the

expenses for the same in the year 2016-17 was around 11,043 and 15,738 in the year

2015-16. The expenses for the same is based on the fixed non-current assets of the

company. The assets of the company that is machinery showed an increase from 64,000

to the year 71,000 in the year 16-17. Motor Vehicles and Furniture showed no change in

the trend period. The depreciation amount should have remained the same or increase

given that the asset base increased in the trend period. The above statements and

situations gives enough evidence of the fact that the depreciation account needs to be

carefully analyzed and inspected (Hąbek and Wolniak).

Figure 2: Depreciation Analysis

(Source: Appendix 1)

Repairs and Maintenance: The repairs and maintenance for the company showed a net

decrease in the year 2016-17 from $5050 to $960. The amount showed a net decrease by

80.99%, which was the biggest dispersion in the components of Income Statements. The

2016-17 2015-16

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Depreciation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ISSUES IN AUDITING PROJECT

repairs and maintenance is charged on the fixed assets of the company. The fixed assets

base of the company did not showed a volatility, which was less than 10%, while the

repairs and maintenance for the same showed a net decrease in the account (Schaltegger

and Burritt 2017). The above reasons for the change is not justifiable, which brings the

case for significant audit testing.

Figure 3: Repairs and Maintenance Account Analysis

(Source: Appendix 1)

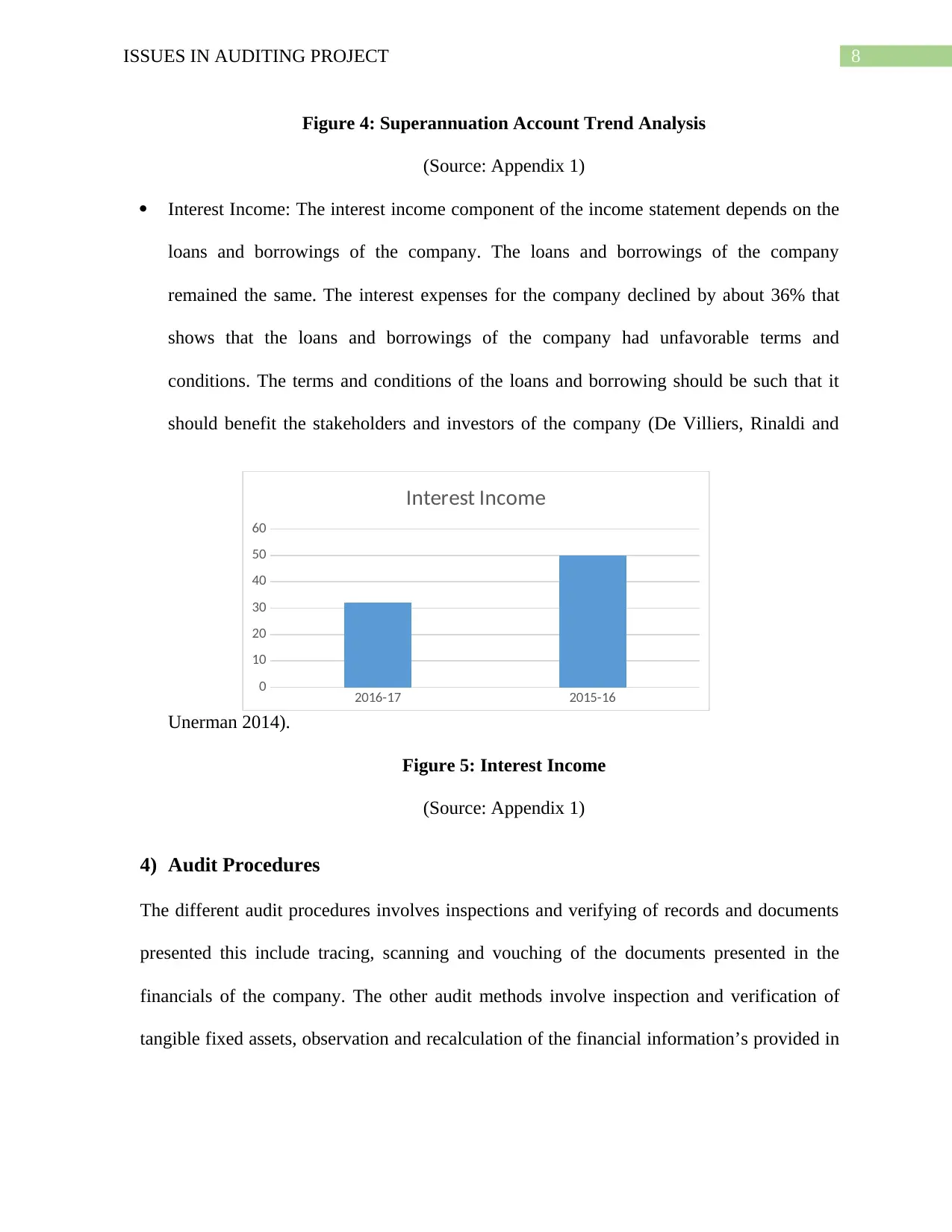

Superannuation: The above account showed a dispersion of about 44.18% decrease in the

trend period, which was not compatible with the decrease in the wages of the company.

The above account volatility and fall in the trend period showed the reasons for

significant audit testing.

2016-17 2015-16

0

1,000

2,000

3,000

4,000

5,000

6,000

Repairs and Maintenance

2016-17 2015-16

0

1,000

2,000

3,000

4,000

5,000

6,000

Superannuation

repairs and maintenance is charged on the fixed assets of the company. The fixed assets

base of the company did not showed a volatility, which was less than 10%, while the

repairs and maintenance for the same showed a net decrease in the account (Schaltegger

and Burritt 2017). The above reasons for the change is not justifiable, which brings the

case for significant audit testing.

Figure 3: Repairs and Maintenance Account Analysis

(Source: Appendix 1)

Superannuation: The above account showed a dispersion of about 44.18% decrease in the

trend period, which was not compatible with the decrease in the wages of the company.

The above account volatility and fall in the trend period showed the reasons for

significant audit testing.

2016-17 2015-16

0

1,000

2,000

3,000

4,000

5,000

6,000

Repairs and Maintenance

2016-17 2015-16

0

1,000

2,000

3,000

4,000

5,000

6,000

Superannuation

8ISSUES IN AUDITING PROJECT

Figure 4: Superannuation Account Trend Analysis

(Source: Appendix 1)

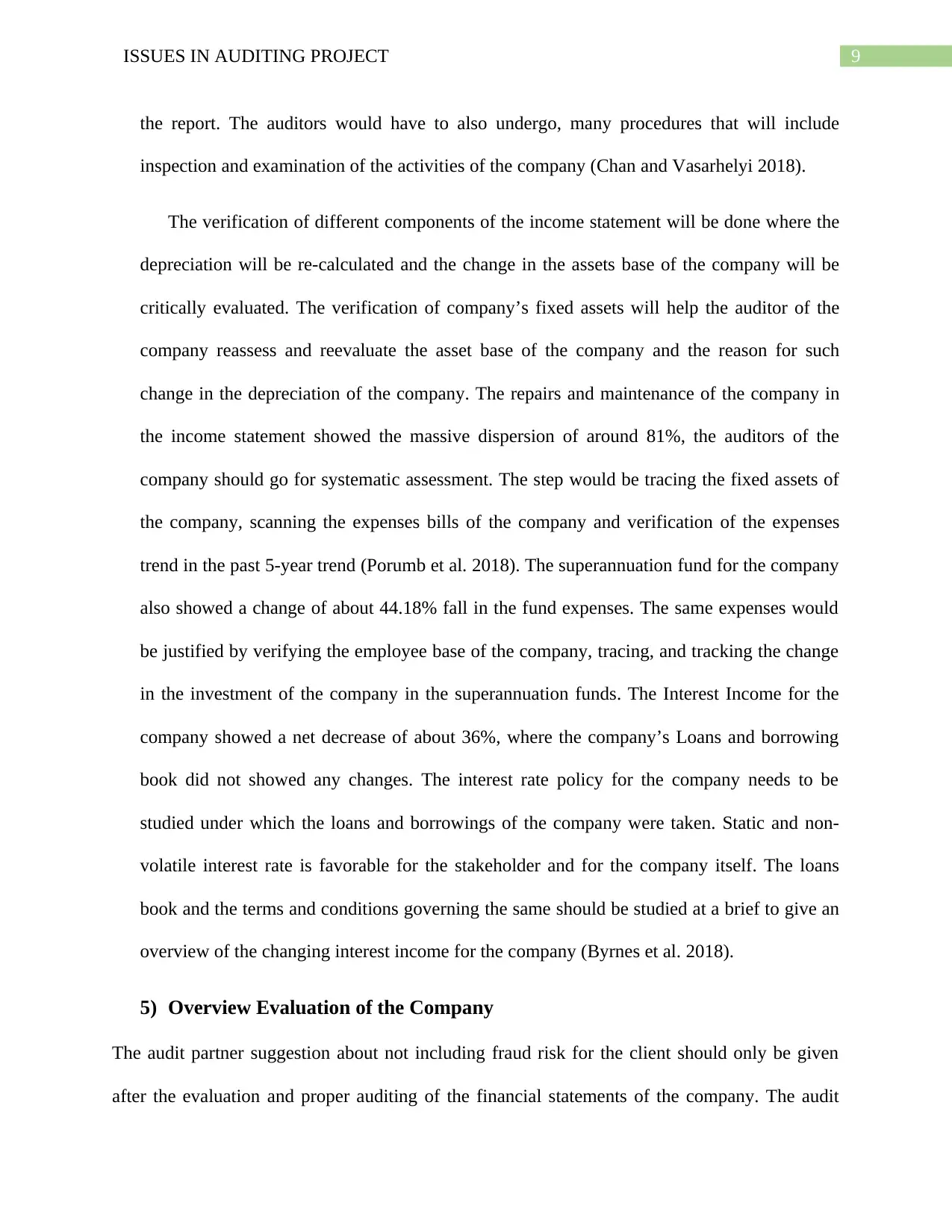

Interest Income: The interest income component of the income statement depends on the

loans and borrowings of the company. The loans and borrowings of the company

remained the same. The interest expenses for the company declined by about 36% that

shows that the loans and borrowings of the company had unfavorable terms and

conditions. The terms and conditions of the loans and borrowing should be such that it

should benefit the stakeholders and investors of the company (De Villiers, Rinaldi and

Unerman 2014).

Figure 5: Interest Income

(Source: Appendix 1)

4) Audit Procedures

The different audit procedures involves inspections and verifying of records and documents

presented this include tracing, scanning and vouching of the documents presented in the

financials of the company. The other audit methods involve inspection and verification of

tangible fixed assets, observation and recalculation of the financial information’s provided in

2016-17 2015-16

0

10

20

30

40

50

60

Interest Income

Figure 4: Superannuation Account Trend Analysis

(Source: Appendix 1)

Interest Income: The interest income component of the income statement depends on the

loans and borrowings of the company. The loans and borrowings of the company

remained the same. The interest expenses for the company declined by about 36% that

shows that the loans and borrowings of the company had unfavorable terms and

conditions. The terms and conditions of the loans and borrowing should be such that it

should benefit the stakeholders and investors of the company (De Villiers, Rinaldi and

Unerman 2014).

Figure 5: Interest Income

(Source: Appendix 1)

4) Audit Procedures

The different audit procedures involves inspections and verifying of records and documents

presented this include tracing, scanning and vouching of the documents presented in the

financials of the company. The other audit methods involve inspection and verification of

tangible fixed assets, observation and recalculation of the financial information’s provided in

2016-17 2015-16

0

10

20

30

40

50

60

Interest Income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ISSUES IN AUDITING PROJECT

the report. The auditors would have to also undergo, many procedures that will include

inspection and examination of the activities of the company (Chan and Vasarhelyi 2018).

The verification of different components of the income statement will be done where the

depreciation will be re-calculated and the change in the assets base of the company will be

critically evaluated. The verification of company’s fixed assets will help the auditor of the

company reassess and reevaluate the asset base of the company and the reason for such

change in the depreciation of the company. The repairs and maintenance of the company in

the income statement showed the massive dispersion of around 81%, the auditors of the

company should go for systematic assessment. The step would be tracing the fixed assets of

the company, scanning the expenses bills of the company and verification of the expenses

trend in the past 5-year trend (Porumb et al. 2018). The superannuation fund for the company

also showed a change of about 44.18% fall in the fund expenses. The same expenses would

be justified by verifying the employee base of the company, tracing, and tracking the change

in the investment of the company in the superannuation funds. The Interest Income for the

company showed a net decrease of about 36%, where the company’s Loans and borrowing

book did not showed any changes. The interest rate policy for the company needs to be

studied under which the loans and borrowings of the company were taken. Static and non-

volatile interest rate is favorable for the stakeholder and for the company itself. The loans

book and the terms and conditions governing the same should be studied at a brief to give an

overview of the changing interest income for the company (Byrnes et al. 2018).

5) Overview Evaluation of the Company

The audit partner suggestion about not including fraud risk for the client should only be given

after the evaluation and proper auditing of the financial statements of the company. The audit

the report. The auditors would have to also undergo, many procedures that will include

inspection and examination of the activities of the company (Chan and Vasarhelyi 2018).

The verification of different components of the income statement will be done where the

depreciation will be re-calculated and the change in the assets base of the company will be

critically evaluated. The verification of company’s fixed assets will help the auditor of the

company reassess and reevaluate the asset base of the company and the reason for such

change in the depreciation of the company. The repairs and maintenance of the company in

the income statement showed the massive dispersion of around 81%, the auditors of the

company should go for systematic assessment. The step would be tracing the fixed assets of

the company, scanning the expenses bills of the company and verification of the expenses

trend in the past 5-year trend (Porumb et al. 2018). The superannuation fund for the company

also showed a change of about 44.18% fall in the fund expenses. The same expenses would

be justified by verifying the employee base of the company, tracing, and tracking the change

in the investment of the company in the superannuation funds. The Interest Income for the

company showed a net decrease of about 36%, where the company’s Loans and borrowing

book did not showed any changes. The interest rate policy for the company needs to be

studied under which the loans and borrowings of the company were taken. Static and non-

volatile interest rate is favorable for the stakeholder and for the company itself. The loans

book and the terms and conditions governing the same should be studied at a brief to give an

overview of the changing interest income for the company (Byrnes et al. 2018).

5) Overview Evaluation of the Company

The audit partner suggestion about not including fraud risk for the client should only be given

after the evaluation and proper auditing of the financial statements of the company. The audit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ISSUES IN AUDITING PROJECT

process should be brief in nature, where proper assessment of the financial position and

analytical review of company’s trend should be performed (Buckless, Krawczyk and Showalter

2014). The audit partner’s suggestion could not be considered as appropriate unless the

company’s corporate governance and proper auditing is conducted. The indications of fraudulent

behavior was found in the components of income statements relating to the fixed non-current

assets of the company and the different expenses related to it. Components such as depreciation

and repairs and maintenance showed greater amount of volatility, which is not justifiable where

the fixed assets of the company remained static (Hossain 2018).

Conclusion

The different procedure and process of auditing is discussed in the project. Preliminary

assessment of the income statement of the company was performed to get a trend analysis of

different components of the income statements. There were four accounts identified in the

income statement of the company which were subject to significant audit testing and there were

different procedures involved for performing the same. The audit procedure and the risk of the

company reporting fraudulent reports depends on the corporate governance and the ethical

guidelines and principles laid down by the company, which should be well assessed by the

auditor of the company.

process should be brief in nature, where proper assessment of the financial position and

analytical review of company’s trend should be performed (Buckless, Krawczyk and Showalter

2014). The audit partner’s suggestion could not be considered as appropriate unless the

company’s corporate governance and proper auditing is conducted. The indications of fraudulent

behavior was found in the components of income statements relating to the fixed non-current

assets of the company and the different expenses related to it. Components such as depreciation

and repairs and maintenance showed greater amount of volatility, which is not justifiable where

the fixed assets of the company remained static (Hossain 2018).

Conclusion

The different procedure and process of auditing is discussed in the project. Preliminary

assessment of the income statement of the company was performed to get a trend analysis of

different components of the income statements. There were four accounts identified in the

income statement of the company which were subject to significant audit testing and there were

different procedures involved for performing the same. The audit procedure and the risk of the

company reporting fraudulent reports depends on the corporate governance and the ethical

guidelines and principles laid down by the company, which should be well assessed by the

auditor of the company.

11ISSUES IN AUDITING PROJECT

References

Buckless, F.A., Krawczyk, K. and Showalter, D.S., 2014. Using virtual worlds to simulate real-

world audit procedures. Issues in Accounting Education, 29(3), pp.389-417.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future Audit

1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing Limited.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement audits.

Accounting Horizons, 29(2), pp.423-429.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2-3), pp.275-326.

Hąbek, P. and Wolniak, R., 2016. Assessing the quality of corporate social responsibility reports:

the case of reporting practices in selected European Union member states. Quality & quantity,

50(1), pp.399-420.

Hossain, M., 2018. Internship Report On “Audit Planning & Procedures of Green Tiger Electric

Vehicle Limited”.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

References

Buckless, F.A., Krawczyk, K. and Showalter, D.S., 2014. Using virtual worlds to simulate real-

world audit procedures. Issues in Accounting Education, 29(3), pp.389-417.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future Audit

1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing Limited.

Cao, M., Chychyla, R. and Stewart, T., 2015. Big Data analytics in financial statement audits.

Accounting Horizons, 29(2), pp.423-429.

Chan, D.Y. and Vasarhelyi, M.A., 2018. Innovation and practice of continuous auditing. In

Continuous Auditing: Theory and Application (pp. 271-283). Emerald Publishing Limited.

De Villiers, C., Rinaldi, L. and Unerman, J., 2014. Integrated Reporting: Insights, gaps and an

agenda for future research. Accounting, Auditing & Accountability Journal, 27(7), pp.1042-1067.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2-3), pp.275-326.

Hąbek, P. and Wolniak, R., 2016. Assessing the quality of corporate social responsibility reports:

the case of reporting practices in selected European Union member states. Quality & quantity,

50(1), pp.399-420.

Hossain, M., 2018. Internship Report On “Audit Planning & Procedures of Green Tiger Electric

Vehicle Limited”.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.