ACC621 Auditing Assignment: Audit Plan for Chartreuse Enterprises

VerifiedAdded on 2023/06/07

|13

|2478

|241

Report

AI Summary

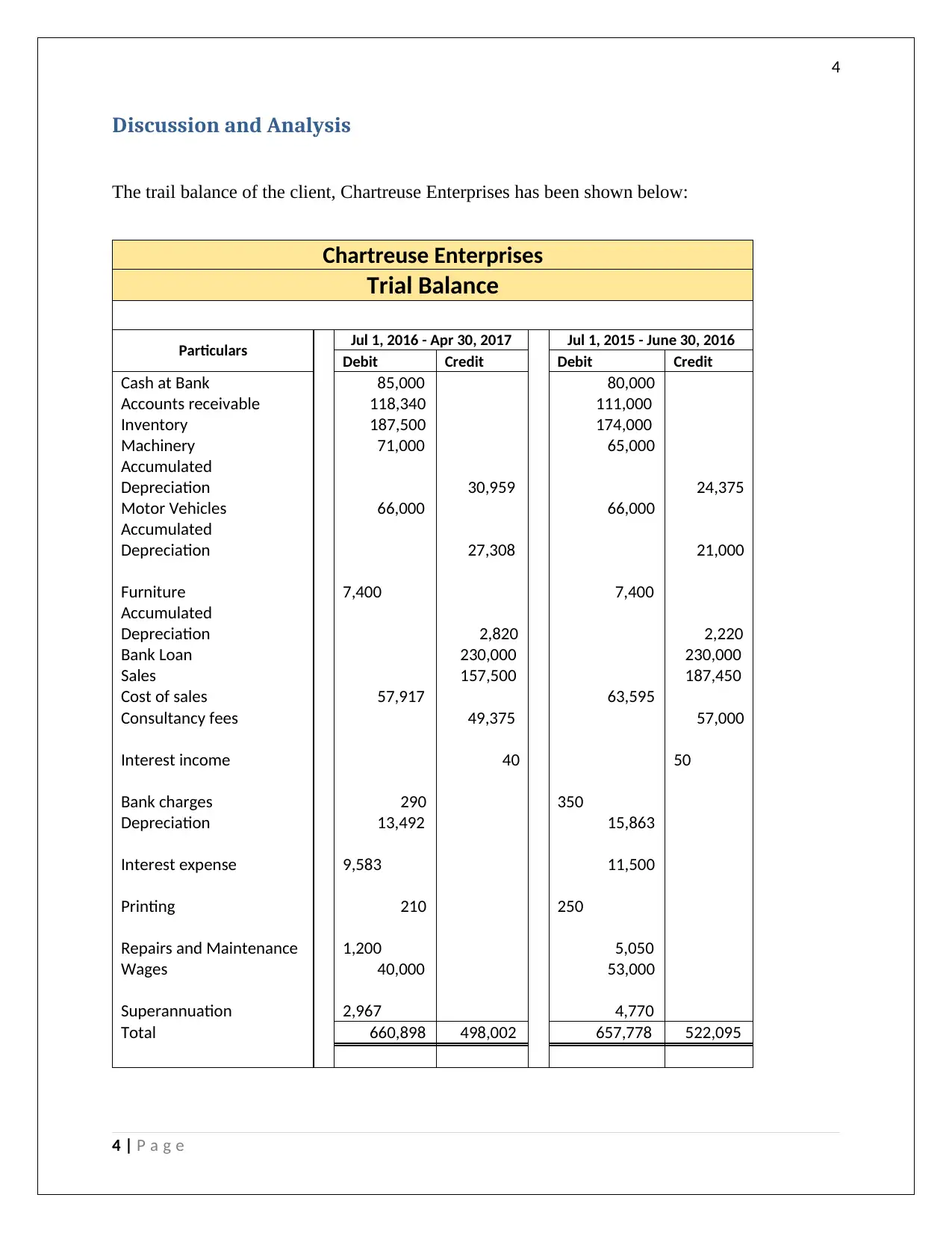

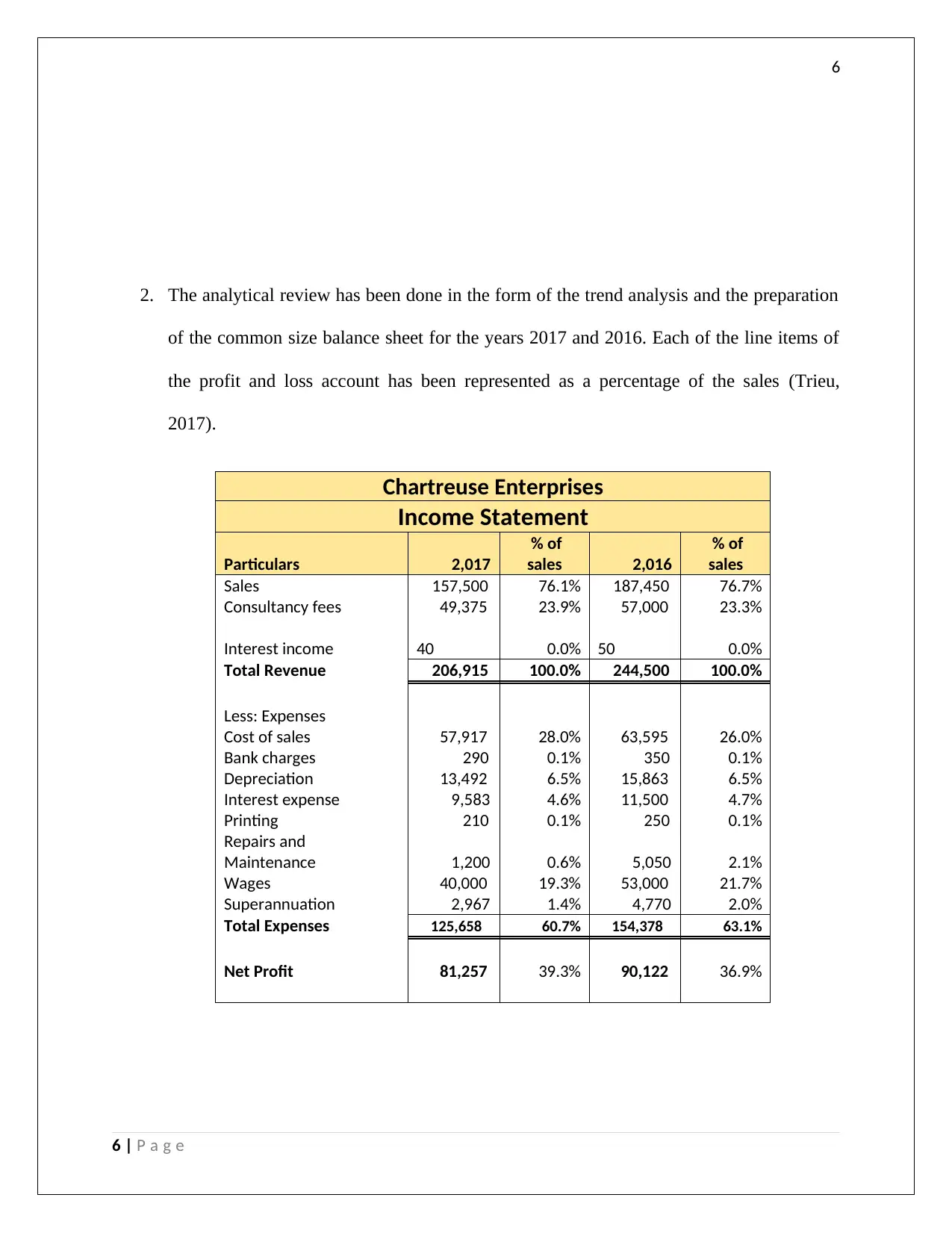

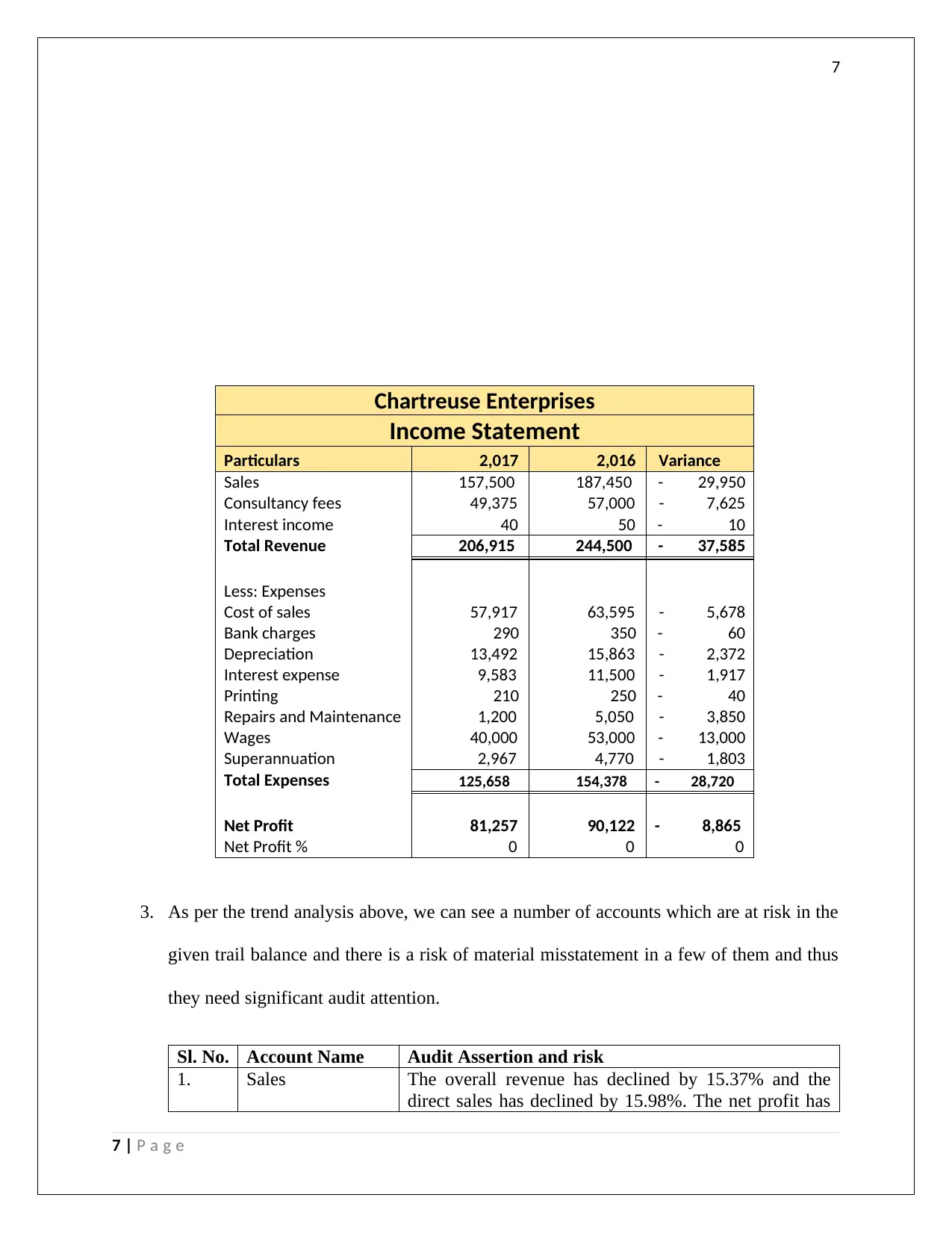

This assignment provides a comprehensive audit plan for Chartreuse Enterprises, addressing key aspects such as materiality assessment, analytical review, and fraud risk analysis. The document begins by revisiting and recalculating the materiality level, emphasizing the importance of setting appropriate limits to ensure that significant accounts are not overlooked during the audit process. A preliminary analytical review, including trend analysis, is conducted to identify potential risks of material misstatement, with justifications provided for selecting specific accounts for audit testing. The assignment outlines the necessary audit procedures for gathering evidence related to sales, depreciation expenses, and wages, including Pareto analysis, vouching of invoices, and scrutiny of depreciation methods and labor costs. Furthermore, it critiques the audit partner's suggestion to forego fraud risk checking, arguing for the importance of professional skepticism and highlighting specific areas where fraud analysis should be conducted, such as superannuation expenses, repairs and maintenance expenditure, and interest expense. This assignment is available on Desklib, where students can find a wide range of study resources, including past papers and solved assignments.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.