ACC707 Auditing & Assurance: Analysis of ASA 701 & 570 Standards

VerifiedAdded on 2024/06/03

|16

|3265

|424

Report

AI Summary

This report provides an analysis of auditing standards ASA 701 and ASA 570, focusing on key audit matters and the going concern concept. ASA 701, developed in response to the global financial crisis, aims to improve communication between auditors and shareholders regarding key audit matters. The report examines the key audit matters of energy companies like Caltex Australia, Origin Energy, and Santos Limited. The revision of ASA 570 is also discussed, addressing issues related to the going concern assumption. The report highlights the management and auditor responsibilities and recommends improvements to enhance organizational profitability by implementing these revised standards.

ACC707 Auditing and Assurance

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report explains about the auditing standards ASA701 which has been developed so as to

communicate the key audit matters which was developed in the global financial crisis. This

development is made so that the response can be gathered from the shareholders about their

decision related to the investment. The analysis has been done by evaluating the key audit

matters of the Energy industries such as Caltex Australia, Origin Energy and Santos Limited.

The standard of the ASA 570 was revised due to the reason that there were various issues with

the ability to use the going concern concept. The report basically focuses on the new standards

that have been revised so that the improvements can be made and the profitability of the

organization can be increased.

2

The report explains about the auditing standards ASA701 which has been developed so as to

communicate the key audit matters which was developed in the global financial crisis. This

development is made so that the response can be gathered from the shareholders about their

decision related to the investment. The analysis has been done by evaluating the key audit

matters of the Energy industries such as Caltex Australia, Origin Energy and Santos Limited.

The standard of the ASA 570 was revised due to the reason that there were various issues with

the ability to use the going concern concept. The report basically focuses on the new standards

that have been revised so that the improvements can be made and the profitability of the

organization can be increased.

2

Contents

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

ASA 701......................................................................................................................................................5

Key Auditing Matters of all companies.......................................................................................................7

Auditing Standards ASA 570....................................................................................................................10

Going Concern Disclosure for ASA 570 of all Companies.......................................................................12

Recommendations.....................................................................................................................................14

Conclusion.................................................................................................................................................15

References.................................................................................................................................................16

3

Executive Summary.....................................................................................................................................2

Introduction.................................................................................................................................................4

ASA 701......................................................................................................................................................5

Key Auditing Matters of all companies.......................................................................................................7

Auditing Standards ASA 570....................................................................................................................10

Going Concern Disclosure for ASA 570 of all Companies.......................................................................12

Recommendations.....................................................................................................................................14

Conclusion.................................................................................................................................................15

References.................................................................................................................................................16

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The report deals with the understanding of the new auditing standards of ASA701 which deals

with the communication of the Key Audit Matters according to the report of the Auditor. With

that the ASA 570 is also explained which deals with the Going Concern concept so that the

actual valuation of the new standards can be done. Caltex Australia is the ASX Listed

organization which is the energy industry which is used in more than 60 countries in the Asia

pacific region. With this the report also deals with the overview about the Key auditing matters

of the companies which are listed in the ASX. The ASA 570 which deals with the going concern

will also be highlighted in the analysis. The reports will explain about the applicability and the

management about the responsibilities of various directors. The understanding about the two

auditing standards will be gained after the analysis is done by deeply evaluating these two

standards.

4

The report deals with the understanding of the new auditing standards of ASA701 which deals

with the communication of the Key Audit Matters according to the report of the Auditor. With

that the ASA 570 is also explained which deals with the Going Concern concept so that the

actual valuation of the new standards can be done. Caltex Australia is the ASX Listed

organization which is the energy industry which is used in more than 60 countries in the Asia

pacific region. With this the report also deals with the overview about the Key auditing matters

of the companies which are listed in the ASX. The ASA 570 which deals with the going concern

will also be highlighted in the analysis. The reports will explain about the applicability and the

management about the responsibilities of various directors. The understanding about the two

auditing standards will be gained after the analysis is done by deeply evaluating these two

standards.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ASA 701

The ASA 701 includes all the financial statements which are related to the period after the

December 2016. They basically aim at describing the responsibilities of the organization and are

applicable to the financial reports which basically explain the key auditing matters in his report.

There are various modifications which are made in the accounting standards with that of the ISA

701 (Auditing and Assurance Standards Board, 2015). All the related matters of the ASA 701 are

described under the Auditing and assurance standard board.

Features:

There are various features of the ASA 701 such as:

This will help the managers of the organization to evaluate that the recommendations of

the other auditors are to be included or not (KPMG, 2014).

It has made mandatory for the organizations to include the key maters in their reports

which are prepared by the auditors of the organization (Auditing and Assurance

Standards Board, 2015).

The audit matter will also be prescribed which will help in determining the manner in

which the auditor has to prescribe those factors.

The standards also specify those factors clearly in which the disclosure has not to be

done by the auditors.

Key Audit Matters:

The Key auditing matters encloses those issues that have been of the most importance in the

reports or the financial papers within its auditing (Auditing and Assurance Standards Board,

2015). The matters which will be relevant in determining the key matters are:

Those areas in which there are the chances of risk in relation with that of the

misstatement or the other relevant risk factors.

Those matters which provides the major or the significant impact on the audit of the

organization (Auditing and Assurance Standards Board, 2015).

5

The ASA 701 includes all the financial statements which are related to the period after the

December 2016. They basically aim at describing the responsibilities of the organization and are

applicable to the financial reports which basically explain the key auditing matters in his report.

There are various modifications which are made in the accounting standards with that of the ISA

701 (Auditing and Assurance Standards Board, 2015). All the related matters of the ASA 701 are

described under the Auditing and assurance standard board.

Features:

There are various features of the ASA 701 such as:

This will help the managers of the organization to evaluate that the recommendations of

the other auditors are to be included or not (KPMG, 2014).

It has made mandatory for the organizations to include the key maters in their reports

which are prepared by the auditors of the organization (Auditing and Assurance

Standards Board, 2015).

The audit matter will also be prescribed which will help in determining the manner in

which the auditor has to prescribe those factors.

The standards also specify those factors clearly in which the disclosure has not to be

done by the auditors.

Key Audit Matters:

The Key auditing matters encloses those issues that have been of the most importance in the

reports or the financial papers within its auditing (Auditing and Assurance Standards Board,

2015). The matters which will be relevant in determining the key matters are:

Those areas in which there are the chances of risk in relation with that of the

misstatement or the other relevant risk factors.

Those matters which provides the major or the significant impact on the audit of the

organization (Auditing and Assurance Standards Board, 2015).

5

The areas which involve the judgment of the management are also included in the key

audit matters and will be considered by the auditors.

Reporting of the Key Audit Matters:

The companies which ask for the different individuals troubles in the key audit matter should

consist of the successful judgment (Auditing and Assurance Standards Board, 2015). By

considering the key audit matters in the proximity for the selection of the inspection will provide

the clean estimation for the obligations of the particular statistics to the customers and also

provide the unmistaken fine to such information (Australian National Audit Office, 2015).

Documents related to the Key Auditing Matter:

The auditors should have the proper documentation so that the supporting can be done for their

opinion according to the ASA 230. The judgments which are grasp which concerns the key

auditing matters should be the part of the conformation (Auditing and Assurance Standards

Board, 2015). The opinion of the evaluator is of the most importance for maintaing all the

documents which are required for the analyst’s exchange with which the survey documents

which are related with the each of the man and woman trouble and ensures that the other

documents of the audit documents should be rising inside the midst of the survey within the

organization (Australian National Audit Office, 2015).

The ASA 701 will help in maintaing the transparency within the organization as the proper

communication will be maintained (Auditing and Assurance Standards Board, 2015). The

shareholders of the organization will be receiving all the related information which is for the

particular purposes. This will help the shareholders in taking the investment decision by

analyzing the key factors. In the auditor’s report section of the company’s annual report the key

auditing matters are included (Australian National Audit Office, 2015).

6

audit matters and will be considered by the auditors.

Reporting of the Key Audit Matters:

The companies which ask for the different individuals troubles in the key audit matter should

consist of the successful judgment (Auditing and Assurance Standards Board, 2015). By

considering the key audit matters in the proximity for the selection of the inspection will provide

the clean estimation for the obligations of the particular statistics to the customers and also

provide the unmistaken fine to such information (Australian National Audit Office, 2015).

Documents related to the Key Auditing Matter:

The auditors should have the proper documentation so that the supporting can be done for their

opinion according to the ASA 230. The judgments which are grasp which concerns the key

auditing matters should be the part of the conformation (Auditing and Assurance Standards

Board, 2015). The opinion of the evaluator is of the most importance for maintaing all the

documents which are required for the analyst’s exchange with which the survey documents

which are related with the each of the man and woman trouble and ensures that the other

documents of the audit documents should be rising inside the midst of the survey within the

organization (Australian National Audit Office, 2015).

The ASA 701 will help in maintaing the transparency within the organization as the proper

communication will be maintained (Auditing and Assurance Standards Board, 2015). The

shareholders of the organization will be receiving all the related information which is for the

particular purposes. This will help the shareholders in taking the investment decision by

analyzing the key factors. In the auditor’s report section of the company’s annual report the key

auditing matters are included (Australian National Audit Office, 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

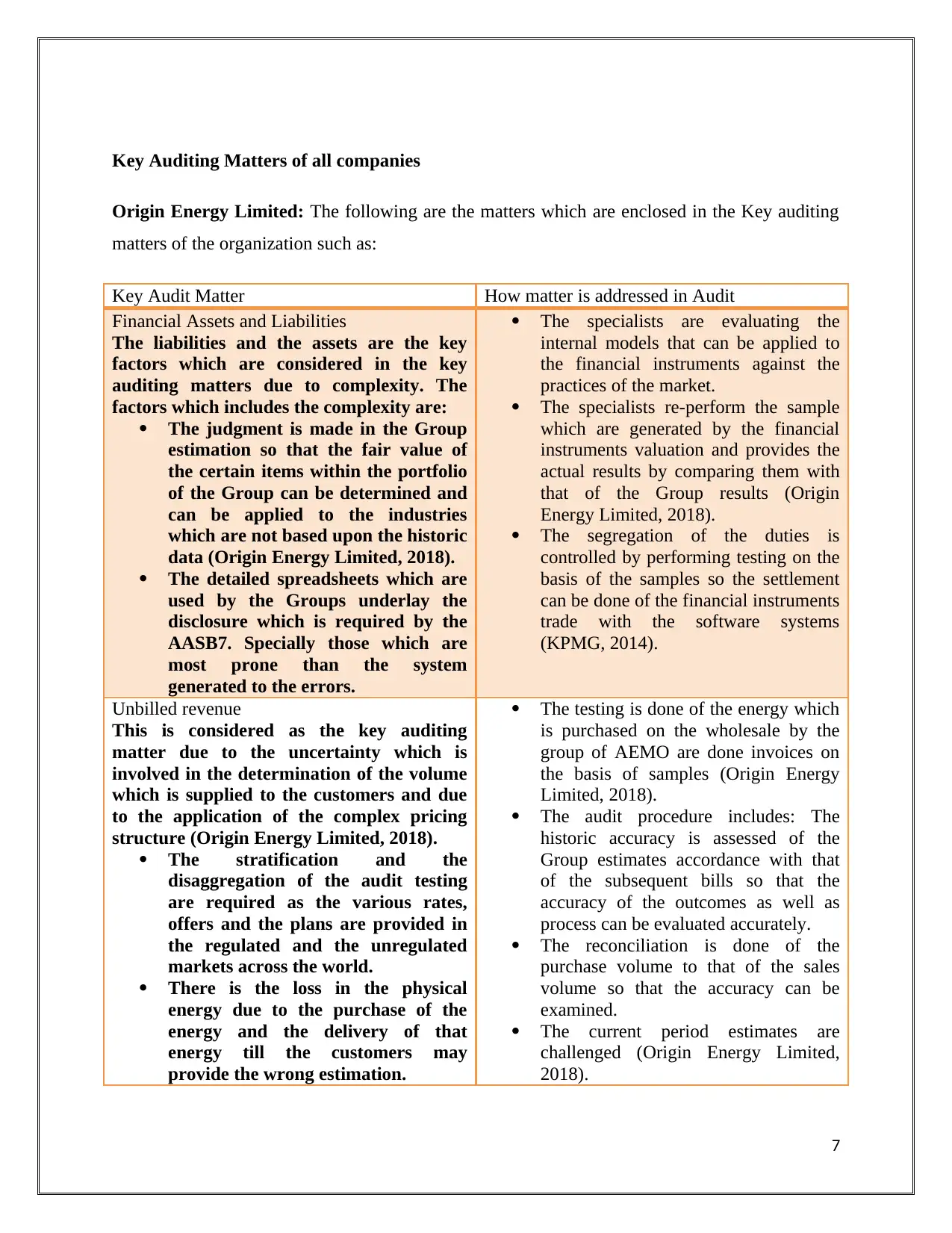

Key Auditing Matters of all companies

Origin Energy Limited: The following are the matters which are enclosed in the Key auditing

matters of the organization such as:

Key Audit Matter How matter is addressed in Audit

Financial Assets and Liabilities

The liabilities and the assets are the key

factors which are considered in the key

auditing matters due to complexity. The

factors which includes the complexity are:

The judgment is made in the Group

estimation so that the fair value of

the certain items within the portfolio

of the Group can be determined and

can be applied to the industries

which are not based upon the historic

data (Origin Energy Limited, 2018).

The detailed spreadsheets which are

used by the Groups underlay the

disclosure which is required by the

AASB7. Specially those which are

most prone than the system

generated to the errors.

The specialists are evaluating the

internal models that can be applied to

the financial instruments against the

practices of the market.

The specialists re-perform the sample

which are generated by the financial

instruments valuation and provides the

actual results by comparing them with

that of the Group results (Origin

Energy Limited, 2018).

The segregation of the duties is

controlled by performing testing on the

basis of the samples so the settlement

can be done of the financial instruments

trade with the software systems

(KPMG, 2014).

Unbilled revenue

This is considered as the key auditing

matter due to the uncertainty which is

involved in the determination of the volume

which is supplied to the customers and due

to the application of the complex pricing

structure (Origin Energy Limited, 2018).

The stratification and the

disaggregation of the audit testing

are required as the various rates,

offers and the plans are provided in

the regulated and the unregulated

markets across the world.

There is the loss in the physical

energy due to the purchase of the

energy and the delivery of that

energy till the customers may

provide the wrong estimation.

The testing is done of the energy which

is purchased on the wholesale by the

group of AEMO are done invoices on

the basis of samples (Origin Energy

Limited, 2018).

The audit procedure includes: The

historic accuracy is assessed of the

Group estimates accordance with that

of the subsequent bills so that the

accuracy of the outcomes as well as

process can be evaluated accurately.

The reconciliation is done of the

purchase volume to that of the sales

volume so that the accuracy can be

examined.

The current period estimates are

challenged (Origin Energy Limited,

2018).

7

Origin Energy Limited: The following are the matters which are enclosed in the Key auditing

matters of the organization such as:

Key Audit Matter How matter is addressed in Audit

Financial Assets and Liabilities

The liabilities and the assets are the key

factors which are considered in the key

auditing matters due to complexity. The

factors which includes the complexity are:

The judgment is made in the Group

estimation so that the fair value of

the certain items within the portfolio

of the Group can be determined and

can be applied to the industries

which are not based upon the historic

data (Origin Energy Limited, 2018).

The detailed spreadsheets which are

used by the Groups underlay the

disclosure which is required by the

AASB7. Specially those which are

most prone than the system

generated to the errors.

The specialists are evaluating the

internal models that can be applied to

the financial instruments against the

practices of the market.

The specialists re-perform the sample

which are generated by the financial

instruments valuation and provides the

actual results by comparing them with

that of the Group results (Origin

Energy Limited, 2018).

The segregation of the duties is

controlled by performing testing on the

basis of the samples so the settlement

can be done of the financial instruments

trade with the software systems

(KPMG, 2014).

Unbilled revenue

This is considered as the key auditing

matter due to the uncertainty which is

involved in the determination of the volume

which is supplied to the customers and due

to the application of the complex pricing

structure (Origin Energy Limited, 2018).

The stratification and the

disaggregation of the audit testing

are required as the various rates,

offers and the plans are provided in

the regulated and the unregulated

markets across the world.

There is the loss in the physical

energy due to the purchase of the

energy and the delivery of that

energy till the customers may

provide the wrong estimation.

The testing is done of the energy which

is purchased on the wholesale by the

group of AEMO are done invoices on

the basis of samples (Origin Energy

Limited, 2018).

The audit procedure includes: The

historic accuracy is assessed of the

Group estimates accordance with that

of the subsequent bills so that the

accuracy of the outcomes as well as

process can be evaluated accurately.

The reconciliation is done of the

purchase volume to that of the sales

volume so that the accuracy can be

examined.

The current period estimates are

challenged (Origin Energy Limited,

2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Caltex Australia: The below mentioned are the Key auditing matters which are disclosed in the

annual reports of 2017 in the Caltex Australia.

Key Matters: The organization has the current holdings which are assessable and are

determined of the holdings of the company’s belongings (Caltex Australia, 2018). The

recoverable measures are evaluated by the view of call of the excellent judgment which is helps

in ensuring that all the activities in the organization are in accordance with the compliance and

the utilization is also ensured by perceiving the inability for the recommendations (Caltex

Australia, 2018). The recoverable measure evaluation is the advantage which will help in

obtaining the ability so that the resources can help in obtaining the favorable position within the

organization.

Auditor’s Action: The auditors get the real view for the valuation of the models which are

associated with the control and are used so as to overview the degree of the Group which is held

on the petroleum which is received. The auditors challenged the current period network by

developing the estimation and distributing it at any variance which is not in the boundaries of the

organization. They also coordinated with various things so that the bargaining can be done and

the pending part can be passed on the satisfactory and the appropriateness for the collection

which will be favorable for the organization.

Santos Limited: The key audit matters of the Santos Limited are explained as below:

Image: Key Audit Matters

8

annual reports of 2017 in the Caltex Australia.

Key Matters: The organization has the current holdings which are assessable and are

determined of the holdings of the company’s belongings (Caltex Australia, 2018). The

recoverable measures are evaluated by the view of call of the excellent judgment which is helps

in ensuring that all the activities in the organization are in accordance with the compliance and

the utilization is also ensured by perceiving the inability for the recommendations (Caltex

Australia, 2018). The recoverable measure evaluation is the advantage which will help in

obtaining the ability so that the resources can help in obtaining the favorable position within the

organization.

Auditor’s Action: The auditors get the real view for the valuation of the models which are

associated with the control and are used so as to overview the degree of the Group which is held

on the petroleum which is received. The auditors challenged the current period network by

developing the estimation and distributing it at any variance which is not in the boundaries of the

organization. They also coordinated with various things so that the bargaining can be done and

the pending part can be passed on the satisfactory and the appropriateness for the collection

which will be favorable for the organization.

Santos Limited: The key audit matters of the Santos Limited are explained as below:

Image: Key Audit Matters

8

Source: Santos Limited, 2016

The key audit matters are those matters which are more significant in the professional

development of the annual reports of the current year (Santos Limited, 2016). The matters are

expressed in the context of the whole but the company does not provide the separate opinions on

the particular matters. All the responsibilities which are highlighted under the Auditor’s

Responsibilities for the Audit of the Financial Report Section are included in the relation to that

of the key matters. The audit procedures are designed in such a way that the performance and the

procedures can be increased by assessing the risky areas of the material misstatement according

to the financial report (Santos Limited, 2016). The capitalization of the expenditure and the

evaluation of the assets are done so that the diversification can be examined within the

organization. Both internal as well as the external auditors conduct the conduct the calculation of

the decommissioning (Santos Limited, 2016).

9

The key audit matters are those matters which are more significant in the professional

development of the annual reports of the current year (Santos Limited, 2016). The matters are

expressed in the context of the whole but the company does not provide the separate opinions on

the particular matters. All the responsibilities which are highlighted under the Auditor’s

Responsibilities for the Audit of the Financial Report Section are included in the relation to that

of the key matters. The audit procedures are designed in such a way that the performance and the

procedures can be increased by assessing the risky areas of the material misstatement according

to the financial report (Santos Limited, 2016). The capitalization of the expenditure and the

evaluation of the assets are done so that the diversification can be examined within the

organization. Both internal as well as the external auditors conduct the conduct the calculation of

the decommissioning (Santos Limited, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing Standards ASA 570

The Australian government has represented the auditing standards ASA 570. It was the revision

of the accounting standards from the ISA 570 to that of the ASA 570 Going Concern Concept

(Auditing and Assurance Standards Board, 2015). These are managed and maintained so that the

higher quality can be maintained and the Interest of the public can be given the more focus as

well as the priority. The ASA 570 is the statements which are prepared after the December, 2018

(Auditing and Assurance Standards Board, 2015).

Going Concern Concept Meaning:

This is the assumption which is concerned the accounting period. These are the reports which are

prepared so as to cease or liquidate the operations of the organization (Australian National Audit

Office, 2015). According to this assumption the assets as well as the liabilities of the

organization are recoded according to the entity basis and will be discharge or realize in the

business which is normal (Auditing and Assurance Standards Board, 2015).

Responsibility of Auditor for Going Concern:

The responsibility of the auditors is to maintain and manage the reports in accordance with that

of the accounting standards (Auditing and Assurance Standards Board, 2015). The going concern

concept is used so that the sufficient evidence can be provided of the going concern. The

responsibility of the auditor is also to maintain the sufficient amount of material (Gallizo and

Saladrigues, 2016).

Responsibility of the management:

The management is also responsible with that of the auditors. The management helps in ensuring

that the compliance of the going concern concept is maintained within the organization (Gallizo

and Saladrigues, 2016). The Australian Accounting Standards evaluates that the management

will help in ensuing that the ability is maintained within the organization for the maintenance of

the going concern (Auditing and Assurance Standards Board, 2015). The management also

10

The Australian government has represented the auditing standards ASA 570. It was the revision

of the accounting standards from the ISA 570 to that of the ASA 570 Going Concern Concept

(Auditing and Assurance Standards Board, 2015). These are managed and maintained so that the

higher quality can be maintained and the Interest of the public can be given the more focus as

well as the priority. The ASA 570 is the statements which are prepared after the December, 2018

(Auditing and Assurance Standards Board, 2015).

Going Concern Concept Meaning:

This is the assumption which is concerned the accounting period. These are the reports which are

prepared so as to cease or liquidate the operations of the organization (Australian National Audit

Office, 2015). According to this assumption the assets as well as the liabilities of the

organization are recoded according to the entity basis and will be discharge or realize in the

business which is normal (Auditing and Assurance Standards Board, 2015).

Responsibility of Auditor for Going Concern:

The responsibility of the auditors is to maintain and manage the reports in accordance with that

of the accounting standards (Auditing and Assurance Standards Board, 2015). The going concern

concept is used so that the sufficient evidence can be provided of the going concern. The

responsibility of the auditor is also to maintain the sufficient amount of material (Gallizo and

Saladrigues, 2016).

Responsibility of the management:

The management is also responsible with that of the auditors. The management helps in ensuring

that the compliance of the going concern concept is maintained within the organization (Gallizo

and Saladrigues, 2016). The Australian Accounting Standards evaluates that the management

will help in ensuing that the ability is maintained within the organization for the maintenance of

the going concern (Auditing and Assurance Standards Board, 2015). The management also

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ensures that all the activities in the organization are maintained according to the rules and the

regulations which are prescribed in the policies of the organization.

11

regulations which are prescribed in the policies of the organization.

11

Going Concern Disclosure for ASA 570 of all Companies

Origin Energy Limited:

The going concern disclosure made the directors of the organization responsible for the

preparation of the financial reports that provides the clear and the fair view about the financial

statements according to the Australian accounting Standards and the Corporation Act 2001

(Origin Energy Limited, 2018). It also ensures to disclose all the matters which are related with

the going concern using the basis of the going concern of accounting until and unless they are

intended to liquidate with no realistic alternative (Origin Energy Limited, 2018). This also

enables the fair view material misstatement which have occurred to fraud and errors (Australian

National Audit Office, 2015).

Caltex Australia:

The going concern concept of the Caltex Limited is as follows:

The examination of the gathering of the companies is the controlled element which may help in

bringing down the physical exercises (KPMG, 2014). According to the ability of the company it

can be said that the company has the enough capacity so as to satisfy the hosting guide of the

capital or the openings of the diverse financing (Caltex Australia, 2018). So, the directors of the

company assume that the company should go on forever. The financial data of the organization

are also showing the actual results and the details. The budgets of the variables show the

possibility that the company will be meeting its duties and through this way the ordinary

business practices and the liabilities settlement according to the course of actions (Caltex

Australia, 2018).

Santos Limited:

While preparing the financial report the directors are responsible for the assessing the ability of

the company so that the maters which are related to the going concern can be evaluated. The

accounting policies of the organization and the reasonableness of the estimates of the accounting

and disclose all the matters related to the going concern are disclosed (Origin Energy Limited,

12

Origin Energy Limited:

The going concern disclosure made the directors of the organization responsible for the

preparation of the financial reports that provides the clear and the fair view about the financial

statements according to the Australian accounting Standards and the Corporation Act 2001

(Origin Energy Limited, 2018). It also ensures to disclose all the matters which are related with

the going concern using the basis of the going concern of accounting until and unless they are

intended to liquidate with no realistic alternative (Origin Energy Limited, 2018). This also

enables the fair view material misstatement which have occurred to fraud and errors (Australian

National Audit Office, 2015).

Caltex Australia:

The going concern concept of the Caltex Limited is as follows:

The examination of the gathering of the companies is the controlled element which may help in

bringing down the physical exercises (KPMG, 2014). According to the ability of the company it

can be said that the company has the enough capacity so as to satisfy the hosting guide of the

capital or the openings of the diverse financing (Caltex Australia, 2018). So, the directors of the

company assume that the company should go on forever. The financial data of the organization

are also showing the actual results and the details. The budgets of the variables show the

possibility that the company will be meeting its duties and through this way the ordinary

business practices and the liabilities settlement according to the course of actions (Caltex

Australia, 2018).

Santos Limited:

While preparing the financial report the directors are responsible for the assessing the ability of

the company so that the maters which are related to the going concern can be evaluated. The

accounting policies of the organization and the reasonableness of the estimates of the accounting

and disclose all the matters related to the going concern are disclosed (Origin Energy Limited,

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.