ACC8000 Research in Accounting: Agency Theory and Compensation

VerifiedAdded on 2023/06/10

|18

|4529

|281

Report

AI Summary

This report delves into the application of agency theory in structuring effective compensation packages for executives at Terrific Telephone Company. It addresses the limitations of fixed salaries in motivating employees, explores various components of compensation packages like salaries, bonuses, health insurance, stock options, 401(k) contributions, and life insurance, and discusses how these components can incentivize productivity. The report also examines the impact of an employee's risk tolerance on their desired compensation and identifies factors that may limit the effectiveness of performance-based compensation. Furthermore, it highlights the benefits of having an executive compensation committee. The report further explains the role of auditing accounts and financial statements in maintaining transparency and trust between principals and agents, especially concerning investments and regulatory compliance. The analysis integrates agency theory with stakeholder and stewardship theories, providing a comprehensive view of governance in non-profit organizations.

RUNNING HEAD: RESEARCH IN ACCOUNTING PRACTICE

Accounting Research

Accounting Research

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research in accounting practice 2

Question 1

Part A

The agency theory focuses on reducing the agency cost which arises due to the conflict of

interest between principal and agent. In order to make the employees work in best interest of

shareholders, company should motivate them by offering performance and equity based

compensation. The fixed salaries given to the managers and employee does not motivate

them anymore. Instead of that, employees start looking for their own benefits. So agency

theory suggest that the compensation package must be desirable and should also include

components other than fixed salaries. This will motivate the employees and will reduce

agency cost (Ims, Pedersen and Zsolnai, 2014).

Part B

A compensation package comprises of different components listed below:

Salary and wages

It is the largest part of a compensation package and is used as a point of comparison between

the potential employees. Salaries are been given as per the skills and performance of the

employee. This component motivate employees to work hard because salary increment take

place only when an individual improve his performance and meets his targets as well as

organizational objectives (Singh, 2007)).

Bonuses

These are basically the performance incentives which are usually paid to the employees in a

lump sum at the end of the year. Bonus is been given according to the performance of an

employee plus helps in motivating him (AllBusiness.com. 2018).

Health insurance

Question 1

Part A

The agency theory focuses on reducing the agency cost which arises due to the conflict of

interest between principal and agent. In order to make the employees work in best interest of

shareholders, company should motivate them by offering performance and equity based

compensation. The fixed salaries given to the managers and employee does not motivate

them anymore. Instead of that, employees start looking for their own benefits. So agency

theory suggest that the compensation package must be desirable and should also include

components other than fixed salaries. This will motivate the employees and will reduce

agency cost (Ims, Pedersen and Zsolnai, 2014).

Part B

A compensation package comprises of different components listed below:

Salary and wages

It is the largest part of a compensation package and is used as a point of comparison between

the potential employees. Salaries are been given as per the skills and performance of the

employee. This component motivate employees to work hard because salary increment take

place only when an individual improve his performance and meets his targets as well as

organizational objectives (Singh, 2007)).

Bonuses

These are basically the performance incentives which are usually paid to the employees in a

lump sum at the end of the year. Bonus is been given according to the performance of an

employee plus helps in motivating him (AllBusiness.com. 2018).

Health insurance

Research in accounting practice 3

It includes health insurance of an employee sponsored by employer. Moreover, it is a benefit

of great value to the employees. It save their money and provide them a sense of security that

they would not be denied in their existing health issues. This motivate them to work for

company with full interests (AllBusiness.com. 2018).

Stock options

These are been used by many companies in order to retain, attract and compensate best

employees in the organizations. Stock options are basically a contract between the employees

and employer in which workers or employees are allowed to purchase a specific number of

company’s shares for a given period of time and at a fixed price. This benefit them by

exercising their options when company’s stocks are traded at higher prices which earn them a

certain amount of profit. It motivates them and help the employer to keep them in the

organization (Olagues and Summa, 2010).

401(k) contribution

It is a type of pension plan which is less expensive and more popular. It is included in the

compensation packages of employees because it gives them some control over their

contribution and they have the right to know the manner in which money is invested. Such

plans offer employees a security regarding their contributed amount. As a result of which,

employees feel motivated and are focused (Francis and Schipper, 2011).

Life insurance

This is something related to securing the whole life of an employee. It also cost less when

purchased by the employer. An organization offering life insurance policies in its

compensation packages will definitely attract people and motivate its employees

(AllBusiness.com. 2018).

It includes health insurance of an employee sponsored by employer. Moreover, it is a benefit

of great value to the employees. It save their money and provide them a sense of security that

they would not be denied in their existing health issues. This motivate them to work for

company with full interests (AllBusiness.com. 2018).

Stock options

These are been used by many companies in order to retain, attract and compensate best

employees in the organizations. Stock options are basically a contract between the employees

and employer in which workers or employees are allowed to purchase a specific number of

company’s shares for a given period of time and at a fixed price. This benefit them by

exercising their options when company’s stocks are traded at higher prices which earn them a

certain amount of profit. It motivates them and help the employer to keep them in the

organization (Olagues and Summa, 2010).

401(k) contribution

It is a type of pension plan which is less expensive and more popular. It is included in the

compensation packages of employees because it gives them some control over their

contribution and they have the right to know the manner in which money is invested. Such

plans offer employees a security regarding their contributed amount. As a result of which,

employees feel motivated and are focused (Francis and Schipper, 2011).

Life insurance

This is something related to securing the whole life of an employee. It also cost less when

purchased by the employer. An organization offering life insurance policies in its

compensation packages will definitely attract people and motivate its employees

(AllBusiness.com. 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research in accounting practice 4

Perks

Other benefits like food and beverages, club memberships, company discounts and

conveyance facilities also helps the employer in keeping its employee motivated and

encouraged for meeting the set targets.

Part C

The identification of employee’s risk tolerance is one of the important factor for deciding a

compensation package for him or her. Keeping the right attitude towards risk benefits the

employees and make them feel secure and more valued. This also help them in becoming

more engaged in their work and remain positive for the same. As a result of which, their

productivity will be enhanced which ultimately affect the performance of the organization. If

the workers keep a positive attitude towards every type of business risk then it may also lead

to less absenteeism. All this will positively impact the desired compensation package of

employees and their overall performance. On the other hand, if employees have negative

attitude towards risk then it may result in decrease of their compensation (Searles, 2017).

Part D

Performance based compensation is a system under which employee’s pay is directly linked

to his or her performance. However, there are some factors which limit the effectiveness of

such performance based compensation. Three of them are as follows:

The effectiveness can be weakened due to the flaws in the design phase,

implementation and operational phase. Lack of adequate budget for funding

performance based increases can limit the effectiveness of the employee’s

compensation package. In addition to this, Biasness and favouritism are also the

factors which do affect employee’s compensation packages. Though it is performance

Perks

Other benefits like food and beverages, club memberships, company discounts and

conveyance facilities also helps the employer in keeping its employee motivated and

encouraged for meeting the set targets.

Part C

The identification of employee’s risk tolerance is one of the important factor for deciding a

compensation package for him or her. Keeping the right attitude towards risk benefits the

employees and make them feel secure and more valued. This also help them in becoming

more engaged in their work and remain positive for the same. As a result of which, their

productivity will be enhanced which ultimately affect the performance of the organization. If

the workers keep a positive attitude towards every type of business risk then it may also lead

to less absenteeism. All this will positively impact the desired compensation package of

employees and their overall performance. On the other hand, if employees have negative

attitude towards risk then it may result in decrease of their compensation (Searles, 2017).

Part D

Performance based compensation is a system under which employee’s pay is directly linked

to his or her performance. However, there are some factors which limit the effectiveness of

such performance based compensation. Three of them are as follows:

The effectiveness can be weakened due to the flaws in the design phase,

implementation and operational phase. Lack of adequate budget for funding

performance based increases can limit the effectiveness of the employee’s

compensation package. In addition to this, Biasness and favouritism are also the

factors which do affect employee’s compensation packages. Though it is performance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research in accounting practice 5

based but in every organization these two aspects plays a major role in measuring the

performance of an employee.

Another factor which affect or limit the efficacy is whether it is applied to managers

or non-managers. Majority of the research studies says that it is for the managers and

the performance based pay is best suitable for the positions in which the job

responsibilities are fairly assigned and are measureable. In addition to this, the

effectiveness of the compensation will be increased if they are applied at higher

organizational levels (Boachie-Mensah and Dogbe, 2011).

Employees generally found that the implementation of such performance based pay is

unfair because the perceptions related to it are different and difficult to identify. Also

it includes lack of transparency, low level of organizational trust, lack of trust in

performance rating systems and lack of managerial traits and leadership credibility.

All the above factors gave a significant impact on compensation packages which are based on

the performance of employees. In a way, the effectiveness is hindered and employees feel

demotivated. An undesirable pay can make employees feel unsecure and demoralized

towards their work (Potemski, Rowland and Witham, 2011).

Part E

Executive compensation committee is been made by company’s board of directors which

delegates its responsibility of framing an appropriate compensation package for executives

and other members. However, there are certain benefits of having such committee which

includes:

It determines and approve the compensation package for chief executive officer of

the company and other senior executives.

based but in every organization these two aspects plays a major role in measuring the

performance of an employee.

Another factor which affect or limit the efficacy is whether it is applied to managers

or non-managers. Majority of the research studies says that it is for the managers and

the performance based pay is best suitable for the positions in which the job

responsibilities are fairly assigned and are measureable. In addition to this, the

effectiveness of the compensation will be increased if they are applied at higher

organizational levels (Boachie-Mensah and Dogbe, 2011).

Employees generally found that the implementation of such performance based pay is

unfair because the perceptions related to it are different and difficult to identify. Also

it includes lack of transparency, low level of organizational trust, lack of trust in

performance rating systems and lack of managerial traits and leadership credibility.

All the above factors gave a significant impact on compensation packages which are based on

the performance of employees. In a way, the effectiveness is hindered and employees feel

demotivated. An undesirable pay can make employees feel unsecure and demoralized

towards their work (Potemski, Rowland and Witham, 2011).

Part E

Executive compensation committee is been made by company’s board of directors which

delegates its responsibility of framing an appropriate compensation package for executives

and other members. However, there are certain benefits of having such committee which

includes:

It determines and approve the compensation package for chief executive officer of

the company and other senior executives.

Research in accounting practice 6

It also design and implement company’s compensation strategy

(Content.next.westlaw.com. 2018).

The executive compensation committee select the components for the compensation

packages for executives. In addition to this, it also decides the amount for the same.

Another benefit is that it also establishes clear performance goals, targets and

mechanisms for measuring the performance of executives and identifying that

whether they have met the benchmark or not.

The committee also help in establishing a compensation philosophy for the company

which is been aligned with the mission and values of the company.

Others several benefits available to executives are also been approved by

compensation committees (Compensation Resources. 2015).

So in a way, executive compensation committee provide several benefits to the board while

determining the components of compensation package.

Question 2

Part A

The agency theory can be defined as the relationship between the principles and agents in the

business. Agency theory is concerned with resolving the problems that can exist in the

agency relation due to unaligned goals or different aversion levels to risk. The most common

agency relation has existed between the shareholders (principal) and company executives

(agents). The need for preparing the accounts lies in all the company irrespective of the

nature and size of the business is operating. The accounts are prepared to assess the financial

position of the company by taking into consideration all the cash flows and other increase and

decrease in the accounts in liabilities and assets. In the agency theory also, the shareholders

want the proper maintenance of the accounts so that they can invest in the company if they

It also design and implement company’s compensation strategy

(Content.next.westlaw.com. 2018).

The executive compensation committee select the components for the compensation

packages for executives. In addition to this, it also decides the amount for the same.

Another benefit is that it also establishes clear performance goals, targets and

mechanisms for measuring the performance of executives and identifying that

whether they have met the benchmark or not.

The committee also help in establishing a compensation philosophy for the company

which is been aligned with the mission and values of the company.

Others several benefits available to executives are also been approved by

compensation committees (Compensation Resources. 2015).

So in a way, executive compensation committee provide several benefits to the board while

determining the components of compensation package.

Question 2

Part A

The agency theory can be defined as the relationship between the principles and agents in the

business. Agency theory is concerned with resolving the problems that can exist in the

agency relation due to unaligned goals or different aversion levels to risk. The most common

agency relation has existed between the shareholders (principal) and company executives

(agents). The need for preparing the accounts lies in all the company irrespective of the

nature and size of the business is operating. The accounts are prepared to assess the financial

position of the company by taking into consideration all the cash flows and other increase and

decrease in the accounts in liabilities and assets. In the agency theory also, the shareholders

want the proper maintenance of the accounts so that they can invest in the company if they

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research in accounting practice 7

are satisfied with the performance and accounts made by the company executives (Ericsson,

2014).

Maintaining proper accounts by the company executives that are the agents of the company

helps the principal to make better decision making in investing his funds. The preparation and

review of accounts help to catch the mistakes earlier which are done by the company. It can

also help in detecting the error, theft, fraud done in the accounts. Financial Statements will

give shareholders the accurate and clear view of how the business is performing. Analysing

the accounts gives the true picture as well as help in identifying the opportunities for growth.

The progress of the company can also monitor by the analyzing and prepare the financial

statements so there is need to maintain the proper books of accounts by the company

executives (Rogers, 2014).

Part B

Agency theory states explain the needs for the audit of accounts. The primary goal of an audit

is to express an opinion on the two aspects of the financial statement. These statements are

related to that the accounts and statement are fairly presented and they should be in

accordance with the GAAP (Generally Accepted Accounting Principles). The audit of

accounts is necessary in every company irrespective of its nature and type of business. The

audit of accounts is necessary as they are made by the internal body of the organization, so

there should be one independent person who checks the accounts without any pressure of the

company. The audit of accounts is important they are used by the internal as well as the

external people by the organization. The audited reports and financial statement are used by

the stakeholders who include the suppliers, investors and governments etc. The financial

statements are seen by the investors to know the performance and check the creditworthiness

of the company. The Stakeholders wants to assess the accounts, as they are interested in the

are satisfied with the performance and accounts made by the company executives (Ericsson,

2014).

Maintaining proper accounts by the company executives that are the agents of the company

helps the principal to make better decision making in investing his funds. The preparation and

review of accounts help to catch the mistakes earlier which are done by the company. It can

also help in detecting the error, theft, fraud done in the accounts. Financial Statements will

give shareholders the accurate and clear view of how the business is performing. Analysing

the accounts gives the true picture as well as help in identifying the opportunities for growth.

The progress of the company can also monitor by the analyzing and prepare the financial

statements so there is need to maintain the proper books of accounts by the company

executives (Rogers, 2014).

Part B

Agency theory states explain the needs for the audit of accounts. The primary goal of an audit

is to express an opinion on the two aspects of the financial statement. These statements are

related to that the accounts and statement are fairly presented and they should be in

accordance with the GAAP (Generally Accepted Accounting Principles). The audit of

accounts is necessary in every company irrespective of its nature and type of business. The

audit of accounts is necessary as they are made by the internal body of the organization, so

there should be one independent person who checks the accounts without any pressure of the

company. The audit of accounts is important they are used by the internal as well as the

external people by the organization. The audited reports and financial statement are used by

the stakeholders who include the suppliers, investors and governments etc. The financial

statements are seen by the investors to know the performance and check the creditworthiness

of the company. The Stakeholders wants to assess the accounts, as they are interested in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research in accounting practice 8

financial capacity of the business. The financial capacity of the business reflects in the

accounts and reports made by the company (Thomson, 2015).

The auditing of accounting is mandatory for completing the regulatory purpose of the

business. The regulation also affects the demand for and the role of audit. In fact, the

regulators are active on behalf of the principals to ensure that their interest is appropriately

heeded and there may be more than one regulatory principal. Use of these regulations in the

business gives the more right to the principals that can help to maintain the confidence and

trust in the market (Duncan and Whittington, 2014).

Question 3

Part A

In the study conducted by Van Puyvelde et al. (2012), governance is defined as the system

through which an organization is been directed, controlled and accountable (Van Puyvelde, et

al. 2012).

Part B

It is mentioned in the research that the basic assumption of agency theory is that the goals of

the principal and the agent often conflict and it is difficult for the principal to identify or

figure out what is the agent is actually doing. Both the parties in the relationship wants to

increase their utilities, as a result of which, the behaviour and role of agent become

uncontrollable which lead to the partial fulfilment of principal’s goals and objectives.

However, non-profit organizations are not immune enough to deal with such shrinking

behaviour of the managers as well as of the employees. Therefore, Van Puyvelde et al. (2012)

uses a principal-agent framework in their study in order to identify the governance of non-

financial capacity of the business. The financial capacity of the business reflects in the

accounts and reports made by the company (Thomson, 2015).

The auditing of accounting is mandatory for completing the regulatory purpose of the

business. The regulation also affects the demand for and the role of audit. In fact, the

regulators are active on behalf of the principals to ensure that their interest is appropriately

heeded and there may be more than one regulatory principal. Use of these regulations in the

business gives the more right to the principals that can help to maintain the confidence and

trust in the market (Duncan and Whittington, 2014).

Question 3

Part A

In the study conducted by Van Puyvelde et al. (2012), governance is defined as the system

through which an organization is been directed, controlled and accountable (Van Puyvelde, et

al. 2012).

Part B

It is mentioned in the research that the basic assumption of agency theory is that the goals of

the principal and the agent often conflict and it is difficult for the principal to identify or

figure out what is the agent is actually doing. Both the parties in the relationship wants to

increase their utilities, as a result of which, the behaviour and role of agent become

uncontrollable which lead to the partial fulfilment of principal’s goals and objectives.

However, non-profit organizations are not immune enough to deal with such shrinking

behaviour of the managers as well as of the employees. Therefore, Van Puyvelde et al. (2012)

uses a principal-agent framework in their study in order to identify the governance of non-

Research in accounting practice 9

profit organizations. The study integrated agency theory with aspects of stakeholder and

stewardship theory (Puyvelde, 2013).

Part C

The alternative theory given by Van Puyvelade was an integration of agency theory with the

stakeholder theory. The literature suggested that many of the concepts of agency theory can

be easily applied to stakeholder relationships and also the principal-agent relationship can be

considered as a subset of general class of stakeholder relationships. As per the theory a

difference was made between external and internal non-profit principal-agent relationships.

In external relationships, external stakeholders play the role of agent or principal and in

internal relationships, internal stakeholders of non-profit organizations are involved.

In order to overcome the conflict of interest and minimize agency cost, the agency theory was

combined with stewardship theory. Under this theory, more focus is been given on agent’s

tendency in order to make it more collective and intrinsically motivated, as suggested by

stewardship theory. In addition to this, the external and internal non-profit organization

relationships are analysed from a stewardship-agency perspective. The study suggested that

both the theories are viewed as complement instead of considering them separately. This

implies that extended agency theory does not only require to consider standard agency

situations but also need to lay emphasis on limit situations where agents are motivated and

have same interest as the shareholders. They are focused to work in best interest of principal

(Van Puyvelde, et al. 2012).

Question 4

Part A

Mixed method study is a type of research methodology in which both the quantitative and

qualitative data is been research and analysed by respective methods. Najeb Masooud

profit organizations. The study integrated agency theory with aspects of stakeholder and

stewardship theory (Puyvelde, 2013).

Part C

The alternative theory given by Van Puyvelade was an integration of agency theory with the

stakeholder theory. The literature suggested that many of the concepts of agency theory can

be easily applied to stakeholder relationships and also the principal-agent relationship can be

considered as a subset of general class of stakeholder relationships. As per the theory a

difference was made between external and internal non-profit principal-agent relationships.

In external relationships, external stakeholders play the role of agent or principal and in

internal relationships, internal stakeholders of non-profit organizations are involved.

In order to overcome the conflict of interest and minimize agency cost, the agency theory was

combined with stewardship theory. Under this theory, more focus is been given on agent’s

tendency in order to make it more collective and intrinsically motivated, as suggested by

stewardship theory. In addition to this, the external and internal non-profit organization

relationships are analysed from a stewardship-agency perspective. The study suggested that

both the theories are viewed as complement instead of considering them separately. This

implies that extended agency theory does not only require to consider standard agency

situations but also need to lay emphasis on limit situations where agents are motivated and

have same interest as the shareholders. They are focused to work in best interest of principal

(Van Puyvelde, et al. 2012).

Question 4

Part A

Mixed method study is a type of research methodology in which both the quantitative and

qualitative data is been research and analysed by respective methods. Najeb Masooud

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Research in accounting practice 10

conducted a research addressing the audit expectation gap issue, in which he used the most

common research technique known as Surveys. Under survey method, questionaries were

formed to collect the required data. These questionaries were pilot tested and was followed

by 12 semi structured interviews (Masoud, 2017).

Part B

i. The understanding about audit expectation gap was gained from five groups which

include managers, preparers of financial statements, general auditing bureau,

regulators and policy makers and shareholders and financial institutions. It can be said

that appropriate people were used for conducting an interview because all of them

were from financial and accounting background and have a specified knowledge

about auditing (Masoud, 2017).

ii. Saunders et al. (2009), argued that usually a sample size of 30 or more is appropriate

for sample distribution but in this study, Masood sample size was of 988 respondents

out of which, there were 145 auditors, 320 audited, 238 financial community and 285

non-financial community. The sample also include the societies which were impacted

by the audit function. However the number was appropriate because a large sample

size was there and greater the same, more desirable the result would be (Masoud,

2017).

iii. A more inclusive analysis is been done of the qualitative data which includes a proper

study of the perceptions of relevant groups about the several auditing issues. However

the data was analysed by using both descriptive and inferential statistics. The analysis

was appropriate because it included the view point of all the interest groups to whom

the questionaries were mailed (Masoud, 2017).

iv. The analysis of qualitative data can be more enhanced by applying a deductive

approach. Under this, the data is been grouped and then the differences and

conducted a research addressing the audit expectation gap issue, in which he used the most

common research technique known as Surveys. Under survey method, questionaries were

formed to collect the required data. These questionaries were pilot tested and was followed

by 12 semi structured interviews (Masoud, 2017).

Part B

i. The understanding about audit expectation gap was gained from five groups which

include managers, preparers of financial statements, general auditing bureau,

regulators and policy makers and shareholders and financial institutions. It can be said

that appropriate people were used for conducting an interview because all of them

were from financial and accounting background and have a specified knowledge

about auditing (Masoud, 2017).

ii. Saunders et al. (2009), argued that usually a sample size of 30 or more is appropriate

for sample distribution but in this study, Masood sample size was of 988 respondents

out of which, there were 145 auditors, 320 audited, 238 financial community and 285

non-financial community. The sample also include the societies which were impacted

by the audit function. However the number was appropriate because a large sample

size was there and greater the same, more desirable the result would be (Masoud,

2017).

iii. A more inclusive analysis is been done of the qualitative data which includes a proper

study of the perceptions of relevant groups about the several auditing issues. However

the data was analysed by using both descriptive and inferential statistics. The analysis

was appropriate because it included the view point of all the interest groups to whom

the questionaries were mailed (Masoud, 2017).

iv. The analysis of qualitative data can be more enhanced by applying a deductive

approach. Under this, the data is been grouped and then the differences and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research in accounting practice 11

similarities are been noticed. Masoud can include in his analysis the differences in the

perceptions of different interest groups. It would have provided a better analysis of the

qualitative data (Masoud, 2017).

Part C

The researcher was successful in making analysis of the first phase of his study. In his main

analysis he showed that auditor group failed to recognize 12 of their existing duties leading to

knowledge gap. Also this gap exist for the users of financial statements and the society made

auditors responsible for such gap. In the first phase he also showed that the objectives of

auditing were not clear to the users and auditors were on a belief that it was not their

responsibility to detect fraud or error in reporting. All such findings are been analysed by

calculating proper mean and after that further analysis or next phase is been carried out

(Masoud, 2017).

Part D

Salifu and Mahama’ study

The questionnaires used was consist of two sections; section A included demographic data of

the respondents whereas section B deal with 15 questions in total out of which, 7 were related

to the responsibility factor, 5 were on reliability factor and 3 questions on decision usefulness

factor. The questions were not open ended and the respondents were required to give rating

on them from one to five as per their opinions. Moreover, these questionnaires were self-

administered by the researchers (Salifu and Mahama, 2015).

Najeb Masuod’s study

In his research the questionaries were first translated into the official language of Libya

which is Arabic. They were framed in English which was not widely spoken in Libya, so the

similarities are been noticed. Masoud can include in his analysis the differences in the

perceptions of different interest groups. It would have provided a better analysis of the

qualitative data (Masoud, 2017).

Part C

The researcher was successful in making analysis of the first phase of his study. In his main

analysis he showed that auditor group failed to recognize 12 of their existing duties leading to

knowledge gap. Also this gap exist for the users of financial statements and the society made

auditors responsible for such gap. In the first phase he also showed that the objectives of

auditing were not clear to the users and auditors were on a belief that it was not their

responsibility to detect fraud or error in reporting. All such findings are been analysed by

calculating proper mean and after that further analysis or next phase is been carried out

(Masoud, 2017).

Part D

Salifu and Mahama’ study

The questionnaires used was consist of two sections; section A included demographic data of

the respondents whereas section B deal with 15 questions in total out of which, 7 were related

to the responsibility factor, 5 were on reliability factor and 3 questions on decision usefulness

factor. The questions were not open ended and the respondents were required to give rating

on them from one to five as per their opinions. Moreover, these questionnaires were self-

administered by the researchers (Salifu and Mahama, 2015).

Najeb Masuod’s study

In his research the questionaries were first translated into the official language of Libya

which is Arabic. They were framed in English which was not widely spoken in Libya, so the

Research in accounting practice 12

translation was made in order to make respondents understand the questions. Once the

questionnaires were completed, they were pilot tested and followed by 12 semi-structured

interviews, taken from telephone, in written and meeting the relevant parties (Masoud, 2017).

From the above two, it can be said that the approach adopted by Masoud is superior to the

one of Salifu and Mahama. Reason being, his questionnaires were not limited to agree or

disagree aspects like the one in Salifu and Mahama’s research. It contained detail opinions of

all the respondents and has also used several forms like for collecting the data like telephonic

interview, meeting and consultations. Moreover, the questionnaire was piloted tested also.

Part E

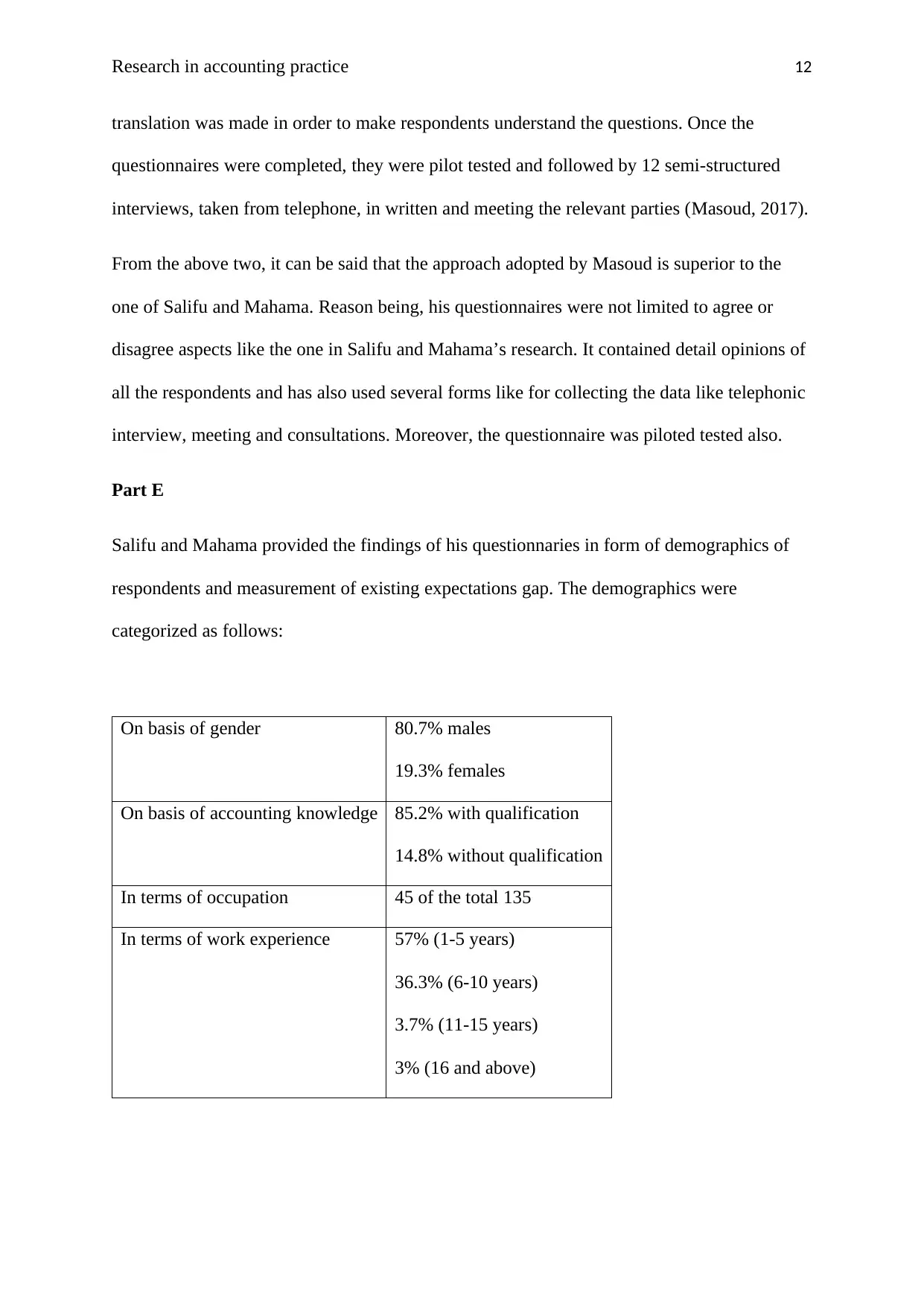

Salifu and Mahama provided the findings of his questionnaries in form of demographics of

respondents and measurement of existing expectations gap. The demographics were

categorized as follows:

On basis of gender 80.7% males

19.3% females

On basis of accounting knowledge 85.2% with qualification

14.8% without qualification

In terms of occupation 45 of the total 135

In terms of work experience 57% (1-5 years)

36.3% (6-10 years)

3.7% (11-15 years)

3% (16 and above)

translation was made in order to make respondents understand the questions. Once the

questionnaires were completed, they were pilot tested and followed by 12 semi-structured

interviews, taken from telephone, in written and meeting the relevant parties (Masoud, 2017).

From the above two, it can be said that the approach adopted by Masoud is superior to the

one of Salifu and Mahama. Reason being, his questionnaires were not limited to agree or

disagree aspects like the one in Salifu and Mahama’s research. It contained detail opinions of

all the respondents and has also used several forms like for collecting the data like telephonic

interview, meeting and consultations. Moreover, the questionnaire was piloted tested also.

Part E

Salifu and Mahama provided the findings of his questionnaries in form of demographics of

respondents and measurement of existing expectations gap. The demographics were

categorized as follows:

On basis of gender 80.7% males

19.3% females

On basis of accounting knowledge 85.2% with qualification

14.8% without qualification

In terms of occupation 45 of the total 135

In terms of work experience 57% (1-5 years)

36.3% (6-10 years)

3.7% (11-15 years)

3% (16 and above)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.