ACC80019 Financial Accounting Theory: Conceptual Framework Essay

VerifiedAdded on 2022/10/13

|13

|3697

|449

Essay

AI Summary

This essay delves into the conceptual framework within financial accounting theory, focusing on Hines' argument that these frameworks serve as strategic maneuvers for standard-setting boards, particularly during periods of competition or potential government intervention. The essay examines the historical development of conceptual frameworks for financial reporting to assess the validity of Hines' position. It further explores the IASB's reasons for developing a conceptual framework, emphasizing the importance of reliability, transparency, and dispute resolution in financial reporting. Relevant accounting theories, such as relevance, reliability, and comparability, are discussed in relation to the framework's objectives. The essay references key academic sources and analyzes the roles of various regulatory bodies in shaping accounting standards and practices. It also considers the implications of the revised Conceptual Framework for Financial Reporting, highlighting its impact on fair value measurement, financial performance reporting, and the clarification of key concepts.

ACC80019 FINANCIAL ACCOUNTING THEORY

Name of the student:

Name of the university:

Authors note:

1

Name of the student:

Name of the university:

Authors note:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................3

1)The argument in support of the Hines....................................................................................3

2) IASB reason for developing a conceptual framework...........................................................5

Reports issued by professional accounting bodies.....................................................................9

Conclusion..................................................................................................................................9

Reference list............................................................................................................................11

2

Introduction................................................................................................................................3

1)The argument in support of the Hines....................................................................................3

2) IASB reason for developing a conceptual framework...........................................................5

Reports issued by professional accounting bodies.....................................................................9

Conclusion..................................................................................................................................9

Reference list............................................................................................................................11

2

Introduction

The conceptual framework has been recognised since 1973. It has been set up by FASB to

develop a coherent theoretical basis for the development and recognition of the accounting

standards in America (US). This provides the guidelines to the board in terms of preparing

the accounting standards. In this context, the major role is played by the IASB, AASB, IFRS

and other standard-setting bodies. There could be a greater role played by these accounting

firms in providing the constituents of the accounting reporting. This could help to manage the

consequences of the several accounting misconducts that could be done by the accounting

firms. The components of the conceptual framework like the qualitative features of the

accounting principles, the general purpose of financial reporting and many more other

activities. There could be a greater approach to analysing the conceptual framework. This

could provide information about the changes that have been occurred in the financial

reporting outcomes.

This paper has been designed to support the argument of the Hines that conceptual

framework ae the strategic manoeuvre that provides legitimacy to the boards during

government intervention ad competition. It protects the rights of the people during these

certainties. There will be an insight into the reason for developing the conceptual framework

for financial reporting. Use of the theories will provide better insight for the same. Four

regulatory bodies will be analysed and their requirement in the accounting field.

1)The argument in support of the Hines

A conceptual framework has always provided the way to provide better assistance in the

financial reporting for the firms. There could be greater use of the principles and concepts

issued by the framework. As opined by Toudas (2018) it helps the hoard to decide the best

outcome for the occurred financial events. The major ones are the accounting standards

which has played a significant role in assisting the companies for the monetary transactions

(Hines, 1989). There have been changes in order to support the transaction and provide

validity in the eyes of the users. IFRS is for those who have adopted it for the first time.

There is a set of guidelines and process to follow the IRS for the reporting entities. It is

required to have proper skill in using the accounting standards and have the knowledge and

updated with the changes (Trăistaru, 2016). This is required for the magnificent reporting and

get a competitive advantage.

3

The conceptual framework has been recognised since 1973. It has been set up by FASB to

develop a coherent theoretical basis for the development and recognition of the accounting

standards in America (US). This provides the guidelines to the board in terms of preparing

the accounting standards. In this context, the major role is played by the IASB, AASB, IFRS

and other standard-setting bodies. There could be a greater role played by these accounting

firms in providing the constituents of the accounting reporting. This could help to manage the

consequences of the several accounting misconducts that could be done by the accounting

firms. The components of the conceptual framework like the qualitative features of the

accounting principles, the general purpose of financial reporting and many more other

activities. There could be a greater approach to analysing the conceptual framework. This

could provide information about the changes that have been occurred in the financial

reporting outcomes.

This paper has been designed to support the argument of the Hines that conceptual

framework ae the strategic manoeuvre that provides legitimacy to the boards during

government intervention ad competition. It protects the rights of the people during these

certainties. There will be an insight into the reason for developing the conceptual framework

for financial reporting. Use of the theories will provide better insight for the same. Four

regulatory bodies will be analysed and their requirement in the accounting field.

1)The argument in support of the Hines

A conceptual framework has always provided the way to provide better assistance in the

financial reporting for the firms. There could be greater use of the principles and concepts

issued by the framework. As opined by Toudas (2018) it helps the hoard to decide the best

outcome for the occurred financial events. The major ones are the accounting standards

which has played a significant role in assisting the companies for the monetary transactions

(Hines, 1989). There have been changes in order to support the transaction and provide

validity in the eyes of the users. IFRS is for those who have adopted it for the first time.

There is a set of guidelines and process to follow the IRS for the reporting entities. It is

required to have proper skill in using the accounting standards and have the knowledge and

updated with the changes (Trăistaru, 2016). This is required for the magnificent reporting and

get a competitive advantage.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

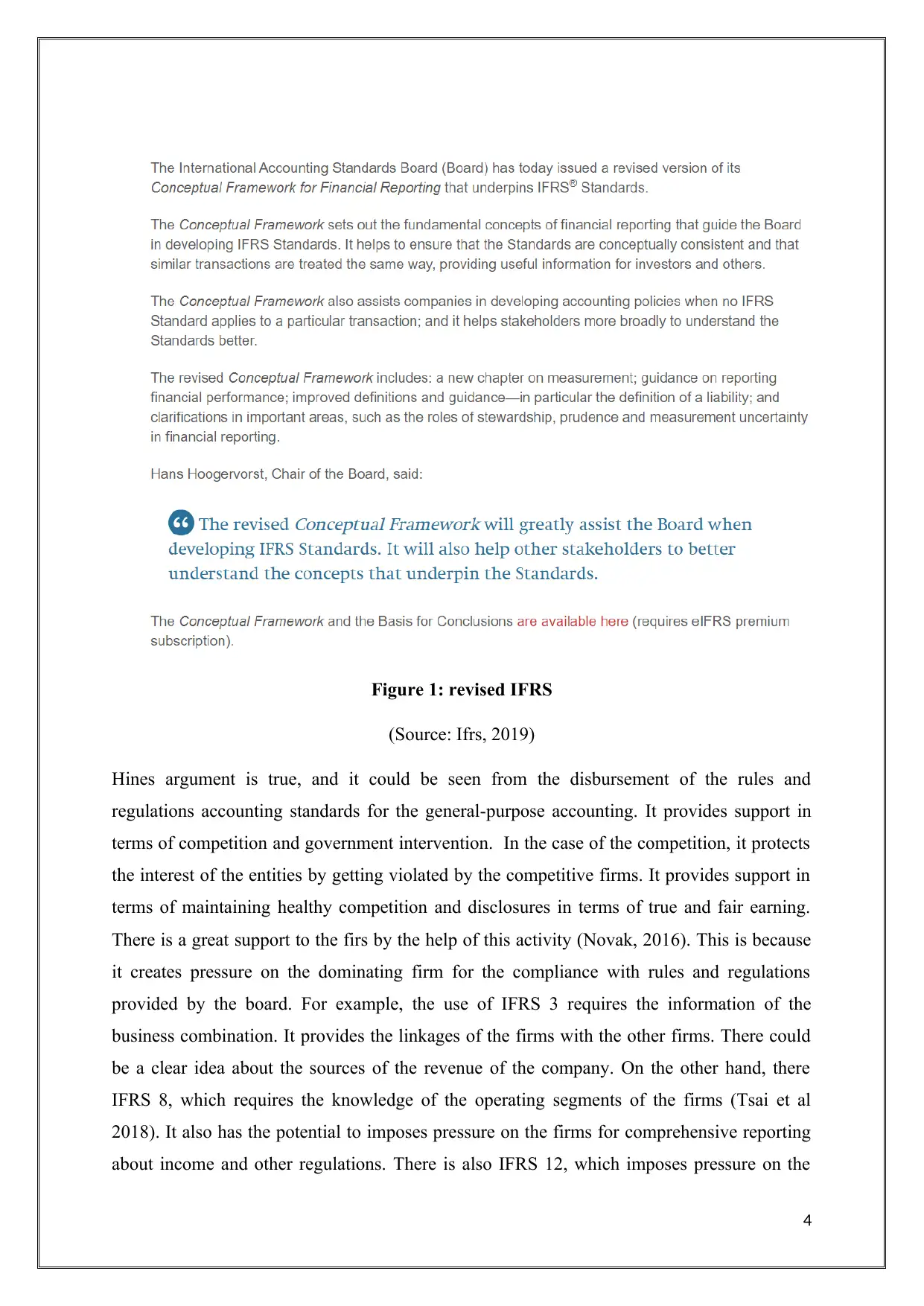

Figure 1: revised IFRS

(Source: Ifrs, 2019)

Hines argument is true, and it could be seen from the disbursement of the rules and

regulations accounting standards for the general-purpose accounting. It provides support in

terms of competition and government intervention. In the case of the competition, it protects

the interest of the entities by getting violated by the competitive firms. It provides support in

terms of maintaining healthy competition and disclosures in terms of true and fair earning.

There is a great support to the firs by the help of this activity (Novak, 2016). This is because

it creates pressure on the dominating firm for the compliance with rules and regulations

provided by the board. For example, the use of IFRS 3 requires the information of the

business combination. It provides the linkages of the firms with the other firms. There could

be a clear idea about the sources of the revenue of the company. On the other hand, there

IFRS 8, which requires the knowledge of the operating segments of the firms (Tsai et al

2018). It also has the potential to imposes pressure on the firms for comprehensive reporting

about income and other regulations. There is also IFRS 12, which imposes pressure on the

4

(Source: Ifrs, 2019)

Hines argument is true, and it could be seen from the disbursement of the rules and

regulations accounting standards for the general-purpose accounting. It provides support in

terms of competition and government intervention. In the case of the competition, it protects

the interest of the entities by getting violated by the competitive firms. It provides support in

terms of maintaining healthy competition and disclosures in terms of true and fair earning.

There is a great support to the firs by the help of this activity (Novak, 2016). This is because

it creates pressure on the dominating firm for the compliance with rules and regulations

provided by the board. For example, the use of IFRS 3 requires the information of the

business combination. It provides the linkages of the firms with the other firms. There could

be a clear idea about the sources of the revenue of the company. On the other hand, there

IFRS 8, which requires the knowledge of the operating segments of the firms (Tsai et al

2018). It also has the potential to imposes pressure on the firms for comprehensive reporting

about income and other regulations. There is also IFRS 12, which imposes pressure on the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

firms for the disclosure of interest in other entities. Thus, with the help of this, the companies

who are facing the pressure in the market due to the dominating firms could gain knowledge

about the strategies or any other relevant information for that situation (Hines, 1989).

Again, in the case of government intervention, there is a strategic approach to helping firms

with better reporting. This could help to be free from any legal matters that could affect the

life and property of the entities. The reporting entities have the pressure to discover all the

relevant areas which could help the stakeholders to get the information. The Comprehensive

income statement records the changes in the financial resources of the company and the

claims (Nieman and Fouché, 2016). There is IFS 13, which holds the disclosure about the fair

value easement. It has the requirement for the fair value in the financial statement of the

reporting entity. Thus, it has the potential to help the entities from the government

intervention if there is transparency in the financial reports served by the companies. They

employ the strategic ways to help the companies to deal with the requirements of the true and

far reporting (Danrimi et al, 2018).

Revised Conceptual Framework for Financial Reporting

The revised conceptual has put its light on several areas which were the need of the times.

This is because there was confusion along with the necessary compliance. Thus, in this

condition, it is not possible to follow the requirements of the board (Ong, 2018). The

conceptual framework has acted for the benefit of the entities from the day it has been

established. There have been periodical reforms among which the recent one was done in

2018. It has concentrated on the many requirements which are useful for the development of

several areas. (Ifrs, 2019)

The first change which has been made in the conceptual framework is when to use the fair

value and the historical cost concept in the financial statement. This is related to the

measurement technique of the transaction. It is required to have proper knowledge about the

changes by which the IFRS could be met. This is being done to maintain the consisted and to

make sure the similar transactions are treated in the same way (Cordery and Sinclair, 2016).

There have also been changed in the guidance for financial performance reporting.

There are also improved guidelines and definitions in terms of liability. There has bee

clarification made for the important areas. These include the steward's roles, measurement of

uncertainty in the financial reporting and prudence. There is required for the key audit

5

who are facing the pressure in the market due to the dominating firms could gain knowledge

about the strategies or any other relevant information for that situation (Hines, 1989).

Again, in the case of government intervention, there is a strategic approach to helping firms

with better reporting. This could help to be free from any legal matters that could affect the

life and property of the entities. The reporting entities have the pressure to discover all the

relevant areas which could help the stakeholders to get the information. The Comprehensive

income statement records the changes in the financial resources of the company and the

claims (Nieman and Fouché, 2016). There is IFS 13, which holds the disclosure about the fair

value easement. It has the requirement for the fair value in the financial statement of the

reporting entity. Thus, it has the potential to help the entities from the government

intervention if there is transparency in the financial reports served by the companies. They

employ the strategic ways to help the companies to deal with the requirements of the true and

far reporting (Danrimi et al, 2018).

Revised Conceptual Framework for Financial Reporting

The revised conceptual has put its light on several areas which were the need of the times.

This is because there was confusion along with the necessary compliance. Thus, in this

condition, it is not possible to follow the requirements of the board (Ong, 2018). The

conceptual framework has acted for the benefit of the entities from the day it has been

established. There have been periodical reforms among which the recent one was done in

2018. It has concentrated on the many requirements which are useful for the development of

several areas. (Ifrs, 2019)

The first change which has been made in the conceptual framework is when to use the fair

value and the historical cost concept in the financial statement. This is related to the

measurement technique of the transaction. It is required to have proper knowledge about the

changes by which the IFRS could be met. This is being done to maintain the consisted and to

make sure the similar transactions are treated in the same way (Cordery and Sinclair, 2016).

There have also been changed in the guidance for financial performance reporting.

There are also improved guidelines and definitions in terms of liability. There has bee

clarification made for the important areas. These include the steward's roles, measurement of

uncertainty in the financial reporting and prudence. There is required for the key audit

5

matters in order to reflect all the risks that are related to each accounting period of the

companies. The revised framework has a great role in assisting the board for the formulation

of the IFRS standards (Mbobo and Ekpo, 2016). It is going to help the other stakeholders in

understanding the concepts which are being employed by while formulating the standard.

Thus, it could be seen that there is a requirement for the greater changes as it has provided the

area of the confusion for the users. The measurement techniques are reliable and could

provide greater assistance in the reporting. There could be less intervention from the

government is irrelevant reporting (Fisher and Nehmer, 2016).

2) IASB reason for developing a conceptual framework

There are several reasons for developing the conceptual framework by IASB. The major

reason for developing the conceptual framework is protecting the interest of the stakeholders

to retrieve the revenant data for the purpose of investment. There is a greater requirement for

the development in the required field. The major reasons for the same are:

Figure 2: IASB reason for developing a conceptual framework

(Source: self-created)

Reliability- there could be the reliability of the financial statements. There are many

stakeholders who require the financial statement of the company. There could be the use of

the concepts which helps the companies to use the standards more accurately. There could be

the use of the several principles that help the entities to report accurately (Gordon et al,

6

Reliability

Transpa

rency

Accounti

ng

disputes

companies. The revised framework has a great role in assisting the board for the formulation

of the IFRS standards (Mbobo and Ekpo, 2016). It is going to help the other stakeholders in

understanding the concepts which are being employed by while formulating the standard.

Thus, it could be seen that there is a requirement for the greater changes as it has provided the

area of the confusion for the users. The measurement techniques are reliable and could

provide greater assistance in the reporting. There could be less intervention from the

government is irrelevant reporting (Fisher and Nehmer, 2016).

2) IASB reason for developing a conceptual framework

There are several reasons for developing the conceptual framework by IASB. The major

reason for developing the conceptual framework is protecting the interest of the stakeholders

to retrieve the revenant data for the purpose of investment. There is a greater requirement for

the development in the required field. The major reasons for the same are:

Figure 2: IASB reason for developing a conceptual framework

(Source: self-created)

Reliability- there could be the reliability of the financial statements. There are many

stakeholders who require the financial statement of the company. There could be the use of

the concepts which helps the companies to use the standards more accurately. There could be

the use of the several principles that help the entities to report accurately (Gordon et al,

6

Reliability

Transpa

rency

Accounti

ng

disputes

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2015). Based on the standards, it is required to have proper knowledge about the recording of

the transaction. There is a requirement for the stakeholders to understand the several

disclosers made by the entities. On the basis of the analysis they use to take a relevant

decision. For example, the investors are in using financial statement so that they could

retrieve the information about the dividend policy and the profit made by the entity.

Transparency- after the use of the accounting standards issued by IFRS, there could be use

of the true and fair reporting required by the board. Thus, on the basis of this, the firms used

to make their financial reports according to the requirement of the accounting standards. The

major requirement in the accounting standard is to maintain transparency in the financial

reports (Zeff, 2015). Thus, with the help of this, transparency is being made in the financial

reports by the help if the IFRS standards. It is a necessary compliance for those who follow

the IFRS principle and has adopted it to prepare the financial reports of the company.

Accounting disputes- again in case of any accounting dispute, this is significantly handled

by the boards. They used to imply the common set of rules which are imposed on both the

entities. Thus, with the help of a clear understanding of the rulers, the disputes used to get

solved. The firms have to take responsibility for any kind of misstatement in the financial

statement. Thus, with the help of accounting standards, any kind of query related to the

reporting could be solved (Kusano and Sanada, 2019). The government could also use this to

check whether a particular entity has performed according to the requirements of the

standards. In case the fail does so the government could nerve for the necessary compliance,

and it could prevent to get in the situation of a dispute with the government. The relevant

accounting theories that could help in this condition are:

7

the transaction. There is a requirement for the stakeholders to understand the several

disclosers made by the entities. On the basis of the analysis they use to take a relevant

decision. For example, the investors are in using financial statement so that they could

retrieve the information about the dividend policy and the profit made by the entity.

Transparency- after the use of the accounting standards issued by IFRS, there could be use

of the true and fair reporting required by the board. Thus, on the basis of this, the firms used

to make their financial reports according to the requirement of the accounting standards. The

major requirement in the accounting standard is to maintain transparency in the financial

reports (Zeff, 2015). Thus, with the help of this, transparency is being made in the financial

reports by the help if the IFRS standards. It is a necessary compliance for those who follow

the IFRS principle and has adopted it to prepare the financial reports of the company.

Accounting disputes- again in case of any accounting dispute, this is significantly handled

by the boards. They used to imply the common set of rules which are imposed on both the

entities. Thus, with the help of a clear understanding of the rulers, the disputes used to get

solved. The firms have to take responsibility for any kind of misstatement in the financial

statement. Thus, with the help of accounting standards, any kind of query related to the

reporting could be solved (Kusano and Sanada, 2019). The government could also use this to

check whether a particular entity has performed according to the requirements of the

standards. In case the fail does so the government could nerve for the necessary compliance,

and it could prevent to get in the situation of a dispute with the government. The relevant

accounting theories that could help in this condition are:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 3: IASB reason for developing a conceptual framework

(Source: self-created)

Relevant

The relevancy of the accounting reports is majorly required for the stakeholders. This is

because it provides the relevant data upon which they could rely. This is the basis of taking

the decisions for the investors in order to invest in the entity. Other stakeholders’ area also

presents who use the financial reports of the company. It is necessary in order to disburse the

information relevant (Hines, 1989). Otherwise, it could have a negative impact n the

company. There could be disputes, or the investors may lose interest in the company. The

conceptual framework helps the companies to present their financial reports in the best

possible way.

Reliable

It is the most important theory that is required for financial reporting. It needs to be reliable

for the users. The transparency in the report needs to be maintained. There are several

requirements under the conceptual framework, which helps the accounting reports to be

reliable. This could help to deal with the requirement of the users. This is why the entities are

also largely in use of this framework. IFRS has provided the uniformity, which helps to

8

Relevance

ReliableComparability

(Source: self-created)

Relevant

The relevancy of the accounting reports is majorly required for the stakeholders. This is

because it provides the relevant data upon which they could rely. This is the basis of taking

the decisions for the investors in order to invest in the entity. Other stakeholders’ area also

presents who use the financial reports of the company. It is necessary in order to disburse the

information relevant (Hines, 1989). Otherwise, it could have a negative impact n the

company. There could be disputes, or the investors may lose interest in the company. The

conceptual framework helps the companies to present their financial reports in the best

possible way.

Reliable

It is the most important theory that is required for financial reporting. It needs to be reliable

for the users. The transparency in the report needs to be maintained. There are several

requirements under the conceptual framework, which helps the accounting reports to be

reliable. This could help to deal with the requirement of the users. This is why the entities are

also largely in use of this framework. IFRS has provided the uniformity, which helps to

8

Relevance

ReliableComparability

compare the data of one entity from their competitors (Kabir and Rahman, 2018). The same

company report could be compared over the period of time.

Comparable

It is also maintained by the conceptual framework. It requires the entities to use the

accounting standards and keep updated with the revisions made in the conceptual framework.

It helps the entities to compare their own financial reports over the period of time. There

could be consistency in financial reporting. Users could easily make a comparison of the

financial reports by using the financial reports of different years (Palea and Scagnelli, 2017).

This is because there are some concepts and principle applied in the financial reports. It

makes the uses to have significant knowledge. There are simple words used in the financial

reports, which makes the financial statement more comparable without much effort.

Consistent

There is consistency in the financial reports because the same principles are being used in the

accounting periods. There could be the use of several principles and report at a constant rate

until there are amendments in the changes. It has the potential to bring consistency with the

reporting years as there is a requirement to follow a particular reporting period for financial

reporting. It could be half-yearly, yearly and quarterly. It is based on the suitability of the

entities that which period they are using to report. It also has the best way to provide help to

the reporting entities. There could be greater use of the standards and helping the companies

in decorating the financial reports.

Reports issued by professional accounting bodies

IFRS- international financial reporting standards used to issue the set of accounting

standards. IASB has developed this regulatory body in order to provide the guidelines for the

recording of the financial transaction. There could be greater use of this principle in order to

maintain the reliability and the relevance of the financial reports. It has the potential to solve

the disputes and maintain the uniformity in the accounting standards. It is a non-profit

organisation and independent body for the issuance of the accounting standards. (IFRS,

2019)

AIA- associations of international accountants were set up in 1928 to promote the concept of

international accounting. It helps to create the global network of the accountants in 85

countries across the world. It is the recognised body for the legal auditors which was verified

9

company report could be compared over the period of time.

Comparable

It is also maintained by the conceptual framework. It requires the entities to use the

accounting standards and keep updated with the revisions made in the conceptual framework.

It helps the entities to compare their own financial reports over the period of time. There

could be consistency in financial reporting. Users could easily make a comparison of the

financial reports by using the financial reports of different years (Palea and Scagnelli, 2017).

This is because there are some concepts and principle applied in the financial reports. It

makes the uses to have significant knowledge. There are simple words used in the financial

reports, which makes the financial statement more comparable without much effort.

Consistent

There is consistency in the financial reports because the same principles are being used in the

accounting periods. There could be the use of several principles and report at a constant rate

until there are amendments in the changes. It has the potential to bring consistency with the

reporting years as there is a requirement to follow a particular reporting period for financial

reporting. It could be half-yearly, yearly and quarterly. It is based on the suitability of the

entities that which period they are using to report. It also has the best way to provide help to

the reporting entities. There could be greater use of the standards and helping the companies

in decorating the financial reports.

Reports issued by professional accounting bodies

IFRS- international financial reporting standards used to issue the set of accounting

standards. IASB has developed this regulatory body in order to provide the guidelines for the

recording of the financial transaction. There could be greater use of this principle in order to

maintain the reliability and the relevance of the financial reports. It has the potential to solve

the disputes and maintain the uniformity in the accounting standards. It is a non-profit

organisation and independent body for the issuance of the accounting standards. (IFRS,

2019)

AIA- associations of international accountants were set up in 1928 to promote the concept of

international accounting. It helps to create the global network of the accountants in 85

countries across the world. It is the recognised body for the legal auditors which was verified

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the government of the UK under the companies act 2006. It helps the entities to get the

help of the professional in taking providing the best insight into the reporting activities. (aia,

2019)

IASB- it is the international accounting standard board which is an independent body. It is a

private-sector body that approves ad develops IFRS international financing reporting

standards. It operates in the regulation of the IFRS foundation. It helps to monitor the

changes that are required for the development of the accounting standards. There could be the

use of several insights in order to provide better knowledge about the accounting standards. It

has the potential to help the firms in better reporting. There could be the use of the accounting

standards by the firms, which could help to determine the best outcome for every transaction.

(Ifrs, 2019)

AASB- Australian accounting standard board has the responsibility to maintain, develop and

issue the Australian accounting standards. It operates under the Australian Securities and

investment commissions Act 2001. It has the responsibility to regulate and enforce company

laws of financial services. It is being done by the Act in order to protect the interest of the

Australian investors, consumers and creditors. (aasb, 2019)

Conclusion

Thus, it could be concluded that there is a requirement of the conceptual framework in order

to provide support to financial reporting. It helps the entities to rely on the standards to

prepare the financial reports. After this, the users of the financial report also find it easy to

compare the financial performance of the entity. The Comprehensive income statement

records the changes in the financial resources of the company and the claims. There is IFS 13,

which holds the disclosure about the fair value easement. It has the requirement for the fair

value in the financial statement of the reporting entity. Thus, it has the potential to help the

entities from the government intervention if there is transparency in the financial reports

served by the companies. They employ strategic ways to help the companies to deal with the

requirements of the true and far reporting. There could be the use of several principles and

report at a constant rate until there are amendments in the changes. It has the potential to

bring consistency with the reporting years as there is a requirement to follow a particular

reporting period for financial reporting. It could be half-yearly, yearly and quarterly. Thus,

with the help of accounting standards, any kind of query related to the reporting could be

solved.

10

help of the professional in taking providing the best insight into the reporting activities. (aia,

2019)

IASB- it is the international accounting standard board which is an independent body. It is a

private-sector body that approves ad develops IFRS international financing reporting

standards. It operates in the regulation of the IFRS foundation. It helps to monitor the

changes that are required for the development of the accounting standards. There could be the

use of several insights in order to provide better knowledge about the accounting standards. It

has the potential to help the firms in better reporting. There could be the use of the accounting

standards by the firms, which could help to determine the best outcome for every transaction.

(Ifrs, 2019)

AASB- Australian accounting standard board has the responsibility to maintain, develop and

issue the Australian accounting standards. It operates under the Australian Securities and

investment commissions Act 2001. It has the responsibility to regulate and enforce company

laws of financial services. It is being done by the Act in order to protect the interest of the

Australian investors, consumers and creditors. (aasb, 2019)

Conclusion

Thus, it could be concluded that there is a requirement of the conceptual framework in order

to provide support to financial reporting. It helps the entities to rely on the standards to

prepare the financial reports. After this, the users of the financial report also find it easy to

compare the financial performance of the entity. The Comprehensive income statement

records the changes in the financial resources of the company and the claims. There is IFS 13,

which holds the disclosure about the fair value easement. It has the requirement for the fair

value in the financial statement of the reporting entity. Thus, it has the potential to help the

entities from the government intervention if there is transparency in the financial reports

served by the companies. They employ strategic ways to help the companies to deal with the

requirements of the true and far reporting. There could be the use of several principles and

report at a constant rate until there are amendments in the changes. It has the potential to

bring consistency with the reporting years as there is a requirement to follow a particular

reporting period for financial reporting. It could be half-yearly, yearly and quarterly. Thus,

with the help of accounting standards, any kind of query related to the reporting could be

solved.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Reference list

Journals

Cordery, C.J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges. Available at SSRN 2918784.

Danrimi, M.L., Abdullah, M. and Alfan, E., 2018. IFRS and Investors’ Trading Pattern: A

Conceptual Framework. Asian Journal of Accounting Perspectives, 11(1), pp.72-107.

Fisher, I.E. and Nehmer, R.A., 2016. Using language processing to evaluate the equivalency

of the FASB and IASB standards. Journal of Emerging Technologies in Accounting, 13(2),

pp.129-144.

Gordon, E.A., Bischof, J., Daske, H., Munter, P., Saka, C., Smith, K.J. and Venter, E.R.,

2015. The IASB's discussion paper on the Conceptual framework for financial reporting: a

commentary and research review. Journal of International Financial Management &

Accounting, 26(1), pp.72-110.

Hines, R 1989, ‘Financial Accounting Knowledge, Conceptual Framework Projects and the

Social Construction of the Accounting Profession’, Accounting, Auditing & Accountability

Journal, vol. 2, no. 2.

Kusano, M and Sanada, M 2019, ‘Crisis and organizational change: IASB’s response to the

financial crisis’, Journal of Accounting & Organizational Change, vol. 15, no. 2, 278-301.

Mbobo, M.E. and Ekpo, N.B., 2016. Operationalising the qualitative characteristics of

financial reporting. International Journal of Finance and Accounting, 5(4), pp.184-192, 7(1),

pp.3-10.

Nieman, G. and Fouché, K., 2016. Developing a regulatory framework for the financial,

management performance and social reporting systems for co-operatives in developing

countries: A case study of South Africa. Acta Commercii, 16(1), pp.1-7.

Novak, A., 2016. Issues in the Recognition versus Disclosure of Financial Information

Debate. Naše gospodarstvo/Our economy, 62(4), pp.52-61.

Ong, A., 2018. The Failure of International Accounting Standards Convergence: A Brief

History. Review of Integrative Business and Economics Research, 7(3), pp.93-105.

12

Journals

Cordery, C.J. and Sinclair, R., 2016. Decision-Usefulness and Stewardship As Conceptual

Framework Objectives: Continuing Challenges. Available at SSRN 2918784.

Danrimi, M.L., Abdullah, M. and Alfan, E., 2018. IFRS and Investors’ Trading Pattern: A

Conceptual Framework. Asian Journal of Accounting Perspectives, 11(1), pp.72-107.

Fisher, I.E. and Nehmer, R.A., 2016. Using language processing to evaluate the equivalency

of the FASB and IASB standards. Journal of Emerging Technologies in Accounting, 13(2),

pp.129-144.

Gordon, E.A., Bischof, J., Daske, H., Munter, P., Saka, C., Smith, K.J. and Venter, E.R.,

2015. The IASB's discussion paper on the Conceptual framework for financial reporting: a

commentary and research review. Journal of International Financial Management &

Accounting, 26(1), pp.72-110.

Hines, R 1989, ‘Financial Accounting Knowledge, Conceptual Framework Projects and the

Social Construction of the Accounting Profession’, Accounting, Auditing & Accountability

Journal, vol. 2, no. 2.

Kusano, M and Sanada, M 2019, ‘Crisis and organizational change: IASB’s response to the

financial crisis’, Journal of Accounting & Organizational Change, vol. 15, no. 2, 278-301.

Mbobo, M.E. and Ekpo, N.B., 2016. Operationalising the qualitative characteristics of

financial reporting. International Journal of Finance and Accounting, 5(4), pp.184-192, 7(1),

pp.3-10.

Nieman, G. and Fouché, K., 2016. Developing a regulatory framework for the financial,

management performance and social reporting systems for co-operatives in developing

countries: A case study of South Africa. Acta Commercii, 16(1), pp.1-7.

Novak, A., 2016. Issues in the Recognition versus Disclosure of Financial Information

Debate. Naše gospodarstvo/Our economy, 62(4), pp.52-61.

Ong, A., 2018. The Failure of International Accounting Standards Convergence: A Brief

History. Review of Integrative Business and Economics Research, 7(3), pp.93-105.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.