ACC91210 Finance for Managers - Case Study 1: Risk and Return Analysis

VerifiedAdded on 2022/12/15

|12

|2439

|459

Case Study

AI Summary

This case study analyzes the risk and return of Boral Limited and a reference company, along with a portfolio comprised of both. It begins by calculating historical monthly returns, average returns, and standard deviations for each entity and the market index. The Capital Asset Pricing Model (CAPM) is then applied to determine expected returns, considering risk-free rates, market risk premium, and beta. The study calculates portfolio beta and expected return, followed by a discussion on the relationship between risk and return, explaining the use of CAPM. Finally, the assignment addresses the impact of systematic and unsystematic risk on Boral Limited's returns, concluding with a comprehensive analysis of risk and return dynamics within the context of financial management.

Case Study 1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Part A: Calculation of historical monthly rate of return, historical average rate of return and

standard deviation............................................................................................................................3

A.1: Historical monthly rate of return of market index...............................................................3

Part A.2: Historical average return and standard deviation.........................................................3

Part B: Expected Return and portfolio beta.....................................................................................5

B.1: Expected return of Boral Limited and Reference Company................................................5

Part B.2: Portfolio Beta and Expected Return.............................................................................6

Part C: Discussion on risk and return for the case company, Reference Company and portfolio...7

Use of CAPM to explain the risk and return relationship............................................................7

Impact of systematic risk and unsystematic risk on the return of Boral Limited........................8

References........................................................................................................................................9

Part A: Calculation of historical monthly rate of return, historical average rate of return and

standard deviation............................................................................................................................3

A.1: Historical monthly rate of return of market index...............................................................3

Part A.2: Historical average return and standard deviation.........................................................3

Part B: Expected Return and portfolio beta.....................................................................................5

B.1: Expected return of Boral Limited and Reference Company................................................5

Part B.2: Portfolio Beta and Expected Return.............................................................................6

Part C: Discussion on risk and return for the case company, Reference Company and portfolio...7

Use of CAPM to explain the risk and return relationship............................................................7

Impact of systematic risk and unsystematic risk on the return of Boral Limited........................8

References........................................................................................................................................9

Part A: Calculation of historical monthly rate of return, historical average rate of return

and standard deviation

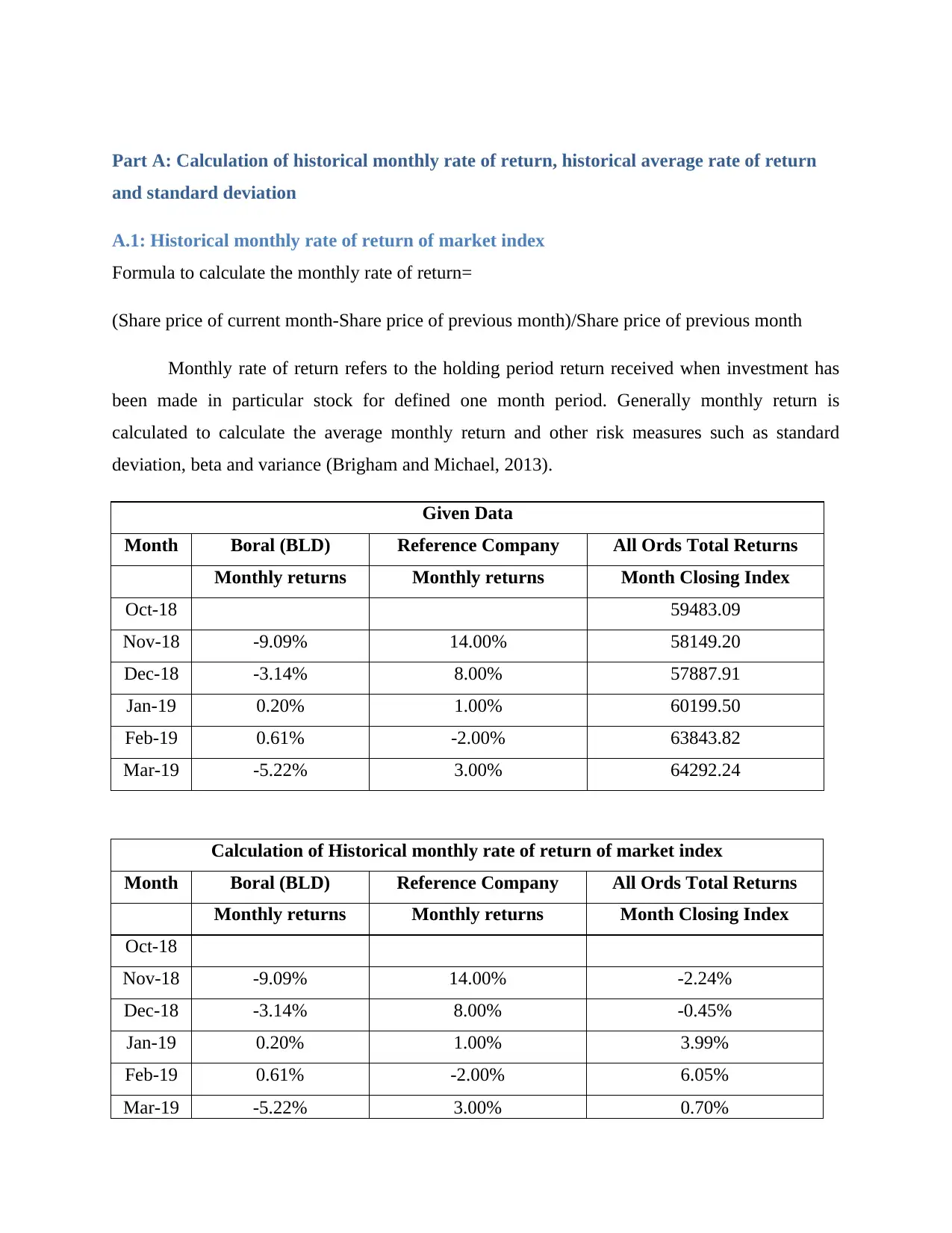

A.1: Historical monthly rate of return of market index

Formula to calculate the monthly rate of return=

(Share price of current month-Share price of previous month)/Share price of previous month

Monthly rate of return refers to the holding period return received when investment has

been made in particular stock for defined one month period. Generally monthly return is

calculated to calculate the average monthly return and other risk measures such as standard

deviation, beta and variance (Brigham and Michael, 2013).

Given Data

Month Boral (BLD) Reference Company All Ords Total Returns

Monthly returns Monthly returns Month Closing Index

Oct-18 59483.09

Nov-18 -9.09% 14.00% 58149.20

Dec-18 -3.14% 8.00% 57887.91

Jan-19 0.20% 1.00% 60199.50

Feb-19 0.61% -2.00% 63843.82

Mar-19 -5.22% 3.00% 64292.24

Calculation of Historical monthly rate of return of market index

Month Boral (BLD) Reference Company All Ords Total Returns

Monthly returns Monthly returns Month Closing Index

Oct-18

Nov-18 -9.09% 14.00% -2.24%

Dec-18 -3.14% 8.00% -0.45%

Jan-19 0.20% 1.00% 3.99%

Feb-19 0.61% -2.00% 6.05%

Mar-19 -5.22% 3.00% 0.70%

and standard deviation

A.1: Historical monthly rate of return of market index

Formula to calculate the monthly rate of return=

(Share price of current month-Share price of previous month)/Share price of previous month

Monthly rate of return refers to the holding period return received when investment has

been made in particular stock for defined one month period. Generally monthly return is

calculated to calculate the average monthly return and other risk measures such as standard

deviation, beta and variance (Brigham and Michael, 2013).

Given Data

Month Boral (BLD) Reference Company All Ords Total Returns

Monthly returns Monthly returns Month Closing Index

Oct-18 59483.09

Nov-18 -9.09% 14.00% 58149.20

Dec-18 -3.14% 8.00% 57887.91

Jan-19 0.20% 1.00% 60199.50

Feb-19 0.61% -2.00% 63843.82

Mar-19 -5.22% 3.00% 64292.24

Calculation of Historical monthly rate of return of market index

Month Boral (BLD) Reference Company All Ords Total Returns

Monthly returns Monthly returns Month Closing Index

Oct-18

Nov-18 -9.09% 14.00% -2.24%

Dec-18 -3.14% 8.00% -0.45%

Jan-19 0.20% 1.00% 3.99%

Feb-19 0.61% -2.00% 6.05%

Mar-19 -5.22% 3.00% 0.70%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

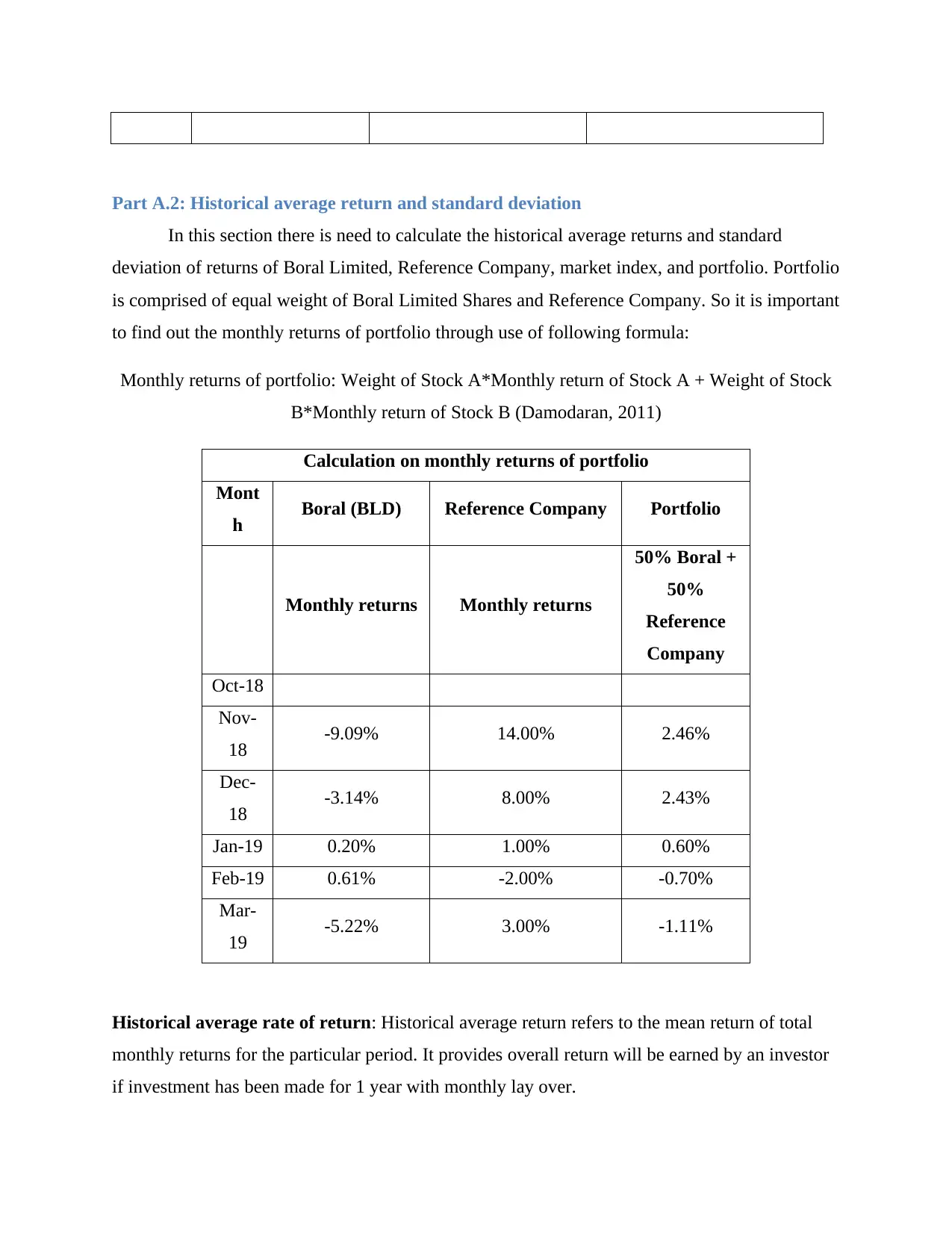

Part A.2: Historical average return and standard deviation

In this section there is need to calculate the historical average returns and standard

deviation of returns of Boral Limited, Reference Company, market index, and portfolio. Portfolio

is comprised of equal weight of Boral Limited Shares and Reference Company. So it is important

to find out the monthly returns of portfolio through use of following formula:

Monthly returns of portfolio: Weight of Stock A*Monthly return of Stock A + Weight of Stock

B*Monthly return of Stock B (Damodaran, 2011)

Calculation on monthly returns of portfolio

Mont

h Boral (BLD) Reference Company Portfolio

Monthly returns Monthly returns

50% Boral +

50%

Reference

Company

Oct-18

Nov-

18 -9.09% 14.00% 2.46%

Dec-

18 -3.14% 8.00% 2.43%

Jan-19 0.20% 1.00% 0.60%

Feb-19 0.61% -2.00% -0.70%

Mar-

19 -5.22% 3.00% -1.11%

Historical average rate of return: Historical average return refers to the mean return of total

monthly returns for the particular period. It provides overall return will be earned by an investor

if investment has been made for 1 year with monthly lay over.

In this section there is need to calculate the historical average returns and standard

deviation of returns of Boral Limited, Reference Company, market index, and portfolio. Portfolio

is comprised of equal weight of Boral Limited Shares and Reference Company. So it is important

to find out the monthly returns of portfolio through use of following formula:

Monthly returns of portfolio: Weight of Stock A*Monthly return of Stock A + Weight of Stock

B*Monthly return of Stock B (Damodaran, 2011)

Calculation on monthly returns of portfolio

Mont

h Boral (BLD) Reference Company Portfolio

Monthly returns Monthly returns

50% Boral +

50%

Reference

Company

Oct-18

Nov-

18 -9.09% 14.00% 2.46%

Dec-

18 -3.14% 8.00% 2.43%

Jan-19 0.20% 1.00% 0.60%

Feb-19 0.61% -2.00% -0.70%

Mar-

19 -5.22% 3.00% -1.11%

Historical average rate of return: Historical average return refers to the mean return of total

monthly returns for the particular period. It provides overall return will be earned by an investor

if investment has been made for 1 year with monthly lay over.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

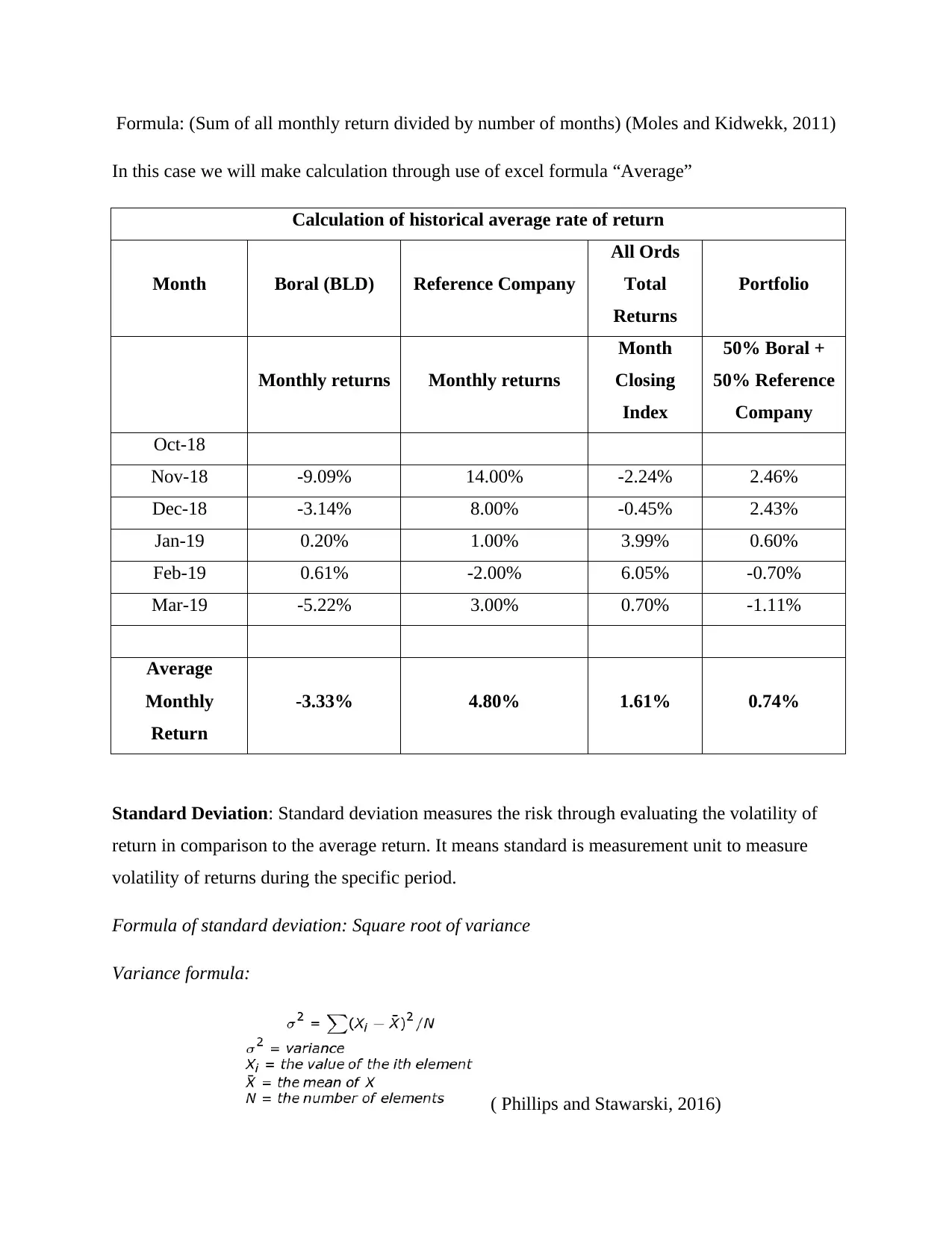

Formula: (Sum of all monthly return divided by number of months) (Moles and Kidwekk, 2011)

In this case we will make calculation through use of excel formula “Average”

Calculation of historical average rate of return

Month Boral (BLD) Reference Company

All Ords

Total

Returns

Portfolio

Monthly returns Monthly returns

Month

Closing

Index

50% Boral +

50% Reference

Company

Oct-18

Nov-18 -9.09% 14.00% -2.24% 2.46%

Dec-18 -3.14% 8.00% -0.45% 2.43%

Jan-19 0.20% 1.00% 3.99% 0.60%

Feb-19 0.61% -2.00% 6.05% -0.70%

Mar-19 -5.22% 3.00% 0.70% -1.11%

Average

Monthly

Return

-3.33% 4.80% 1.61% 0.74%

Standard Deviation: Standard deviation measures the risk through evaluating the volatility of

return in comparison to the average return. It means standard is measurement unit to measure

volatility of returns during the specific period.

Formula of standard deviation: Square root of variance

Variance formula:

( Phillips and Stawarski, 2016)

In this case we will make calculation through use of excel formula “Average”

Calculation of historical average rate of return

Month Boral (BLD) Reference Company

All Ords

Total

Returns

Portfolio

Monthly returns Monthly returns

Month

Closing

Index

50% Boral +

50% Reference

Company

Oct-18

Nov-18 -9.09% 14.00% -2.24% 2.46%

Dec-18 -3.14% 8.00% -0.45% 2.43%

Jan-19 0.20% 1.00% 3.99% 0.60%

Feb-19 0.61% -2.00% 6.05% -0.70%

Mar-19 -5.22% 3.00% 0.70% -1.11%

Average

Monthly

Return

-3.33% 4.80% 1.61% 0.74%

Standard Deviation: Standard deviation measures the risk through evaluating the volatility of

return in comparison to the average return. It means standard is measurement unit to measure

volatility of returns during the specific period.

Formula of standard deviation: Square root of variance

Variance formula:

( Phillips and Stawarski, 2016)

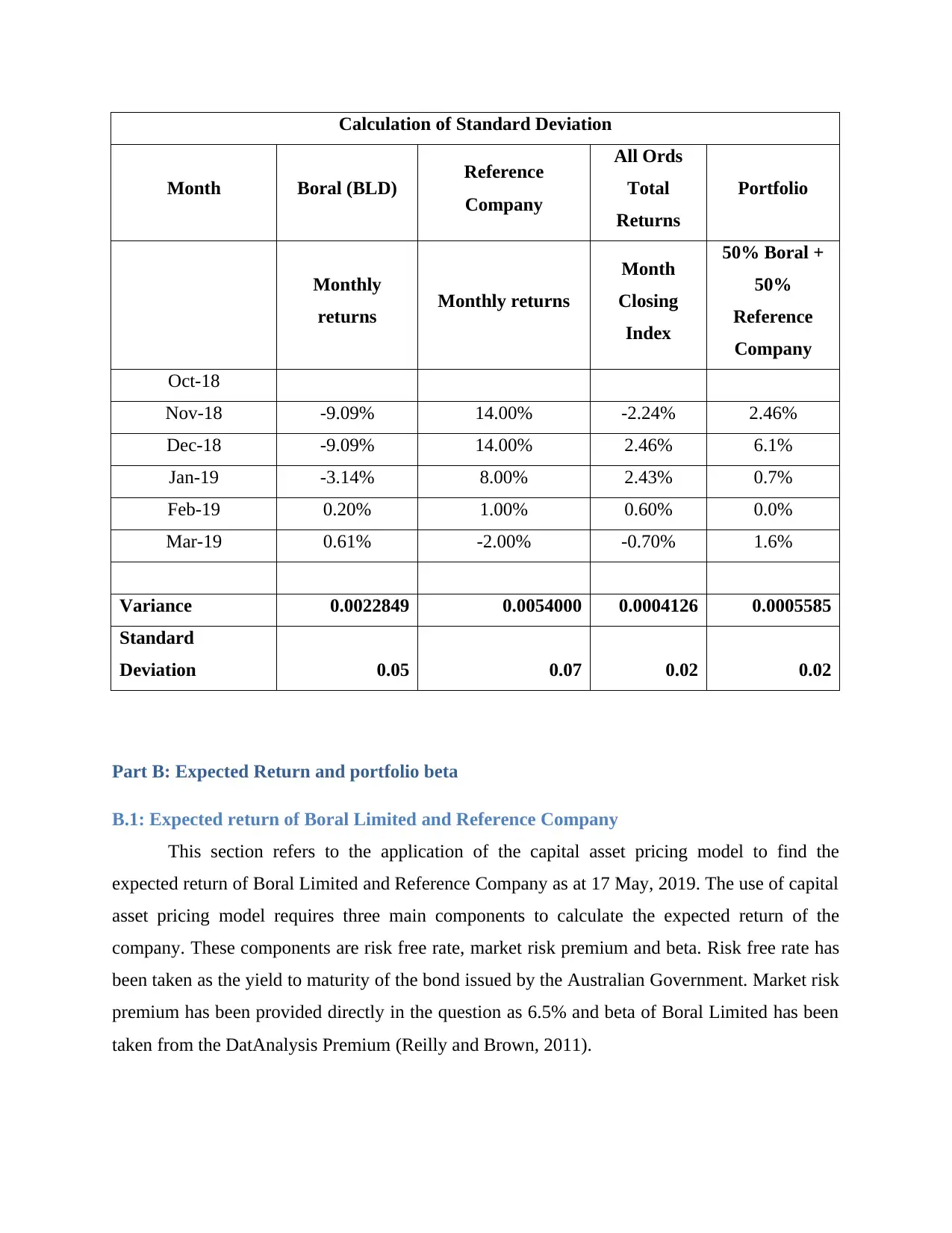

Calculation of Standard Deviation

Month Boral (BLD) Reference

Company

All Ords

Total

Returns

Portfolio

Monthly

returns Monthly returns

Month

Closing

Index

50% Boral +

50%

Reference

Company

Oct-18

Nov-18 -9.09% 14.00% -2.24% 2.46%

Dec-18 -9.09% 14.00% 2.46% 6.1%

Jan-19 -3.14% 8.00% 2.43% 0.7%

Feb-19 0.20% 1.00% 0.60% 0.0%

Mar-19 0.61% -2.00% -0.70% 1.6%

Variance 0.0022849 0.0054000 0.0004126 0.0005585

Standard

Deviation 0.05 0.07 0.02 0.02

Part B: Expected Return and portfolio beta

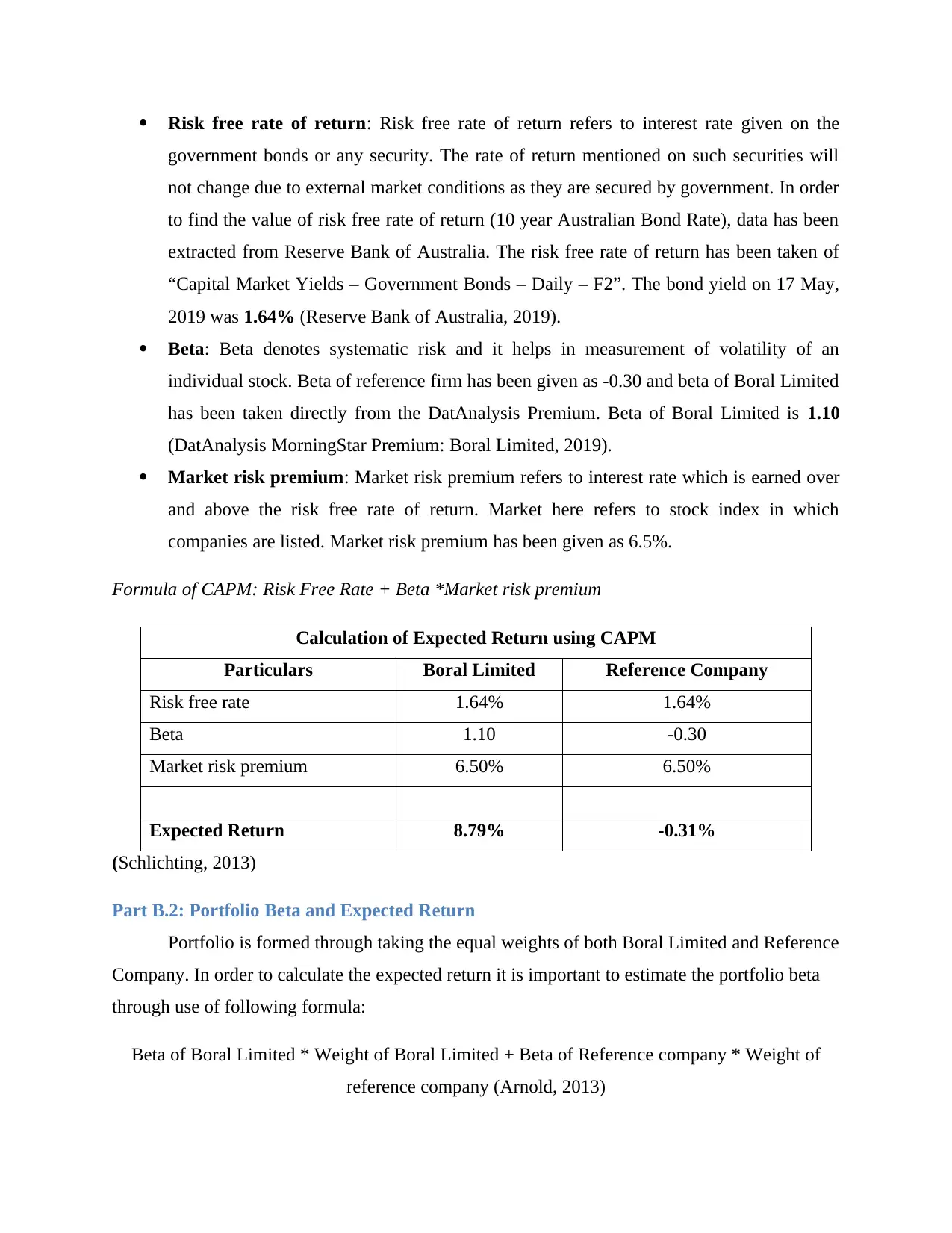

B.1: Expected return of Boral Limited and Reference Company

This section refers to the application of the capital asset pricing model to find the

expected return of Boral Limited and Reference Company as at 17 May, 2019. The use of capital

asset pricing model requires three main components to calculate the expected return of the

company. These components are risk free rate, market risk premium and beta. Risk free rate has

been taken as the yield to maturity of the bond issued by the Australian Government. Market risk

premium has been provided directly in the question as 6.5% and beta of Boral Limited has been

taken from the DatAnalysis Premium (Reilly and Brown, 2011).

Month Boral (BLD) Reference

Company

All Ords

Total

Returns

Portfolio

Monthly

returns Monthly returns

Month

Closing

Index

50% Boral +

50%

Reference

Company

Oct-18

Nov-18 -9.09% 14.00% -2.24% 2.46%

Dec-18 -9.09% 14.00% 2.46% 6.1%

Jan-19 -3.14% 8.00% 2.43% 0.7%

Feb-19 0.20% 1.00% 0.60% 0.0%

Mar-19 0.61% -2.00% -0.70% 1.6%

Variance 0.0022849 0.0054000 0.0004126 0.0005585

Standard

Deviation 0.05 0.07 0.02 0.02

Part B: Expected Return and portfolio beta

B.1: Expected return of Boral Limited and Reference Company

This section refers to the application of the capital asset pricing model to find the

expected return of Boral Limited and Reference Company as at 17 May, 2019. The use of capital

asset pricing model requires three main components to calculate the expected return of the

company. These components are risk free rate, market risk premium and beta. Risk free rate has

been taken as the yield to maturity of the bond issued by the Australian Government. Market risk

premium has been provided directly in the question as 6.5% and beta of Boral Limited has been

taken from the DatAnalysis Premium (Reilly and Brown, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risk free rate of return: Risk free rate of return refers to interest rate given on the

government bonds or any security. The rate of return mentioned on such securities will

not change due to external market conditions as they are secured by government. In order

to find the value of risk free rate of return (10 year Australian Bond Rate), data has been

extracted from Reserve Bank of Australia. The risk free rate of return has been taken of

“Capital Market Yields – Government Bonds – Daily – F2”. The bond yield on 17 May,

2019 was 1.64% (Reserve Bank of Australia, 2019).

Beta: Beta denotes systematic risk and it helps in measurement of volatility of an

individual stock. Beta of reference firm has been given as -0.30 and beta of Boral Limited

has been taken directly from the DatAnalysis Premium. Beta of Boral Limited is 1.10

(DatAnalysis MorningStar Premium: Boral Limited, 2019).

Market risk premium: Market risk premium refers to interest rate which is earned over

and above the risk free rate of return. Market here refers to stock index in which

companies are listed. Market risk premium has been given as 6.5%.

Formula of CAPM: Risk Free Rate + Beta *Market risk premium

Calculation of Expected Return using CAPM

Particulars Boral Limited Reference Company

Risk free rate 1.64% 1.64%

Beta 1.10 -0.30

Market risk premium 6.50% 6.50%

Expected Return 8.79% -0.31%

(Schlichting, 2013)

Part B.2: Portfolio Beta and Expected Return

Portfolio is formed through taking the equal weights of both Boral Limited and Reference

Company. In order to calculate the expected return it is important to estimate the portfolio beta

through use of following formula:

Beta of Boral Limited * Weight of Boral Limited + Beta of Reference company * Weight of

reference company (Arnold, 2013)

government bonds or any security. The rate of return mentioned on such securities will

not change due to external market conditions as they are secured by government. In order

to find the value of risk free rate of return (10 year Australian Bond Rate), data has been

extracted from Reserve Bank of Australia. The risk free rate of return has been taken of

“Capital Market Yields – Government Bonds – Daily – F2”. The bond yield on 17 May,

2019 was 1.64% (Reserve Bank of Australia, 2019).

Beta: Beta denotes systematic risk and it helps in measurement of volatility of an

individual stock. Beta of reference firm has been given as -0.30 and beta of Boral Limited

has been taken directly from the DatAnalysis Premium. Beta of Boral Limited is 1.10

(DatAnalysis MorningStar Premium: Boral Limited, 2019).

Market risk premium: Market risk premium refers to interest rate which is earned over

and above the risk free rate of return. Market here refers to stock index in which

companies are listed. Market risk premium has been given as 6.5%.

Formula of CAPM: Risk Free Rate + Beta *Market risk premium

Calculation of Expected Return using CAPM

Particulars Boral Limited Reference Company

Risk free rate 1.64% 1.64%

Beta 1.10 -0.30

Market risk premium 6.50% 6.50%

Expected Return 8.79% -0.31%

(Schlichting, 2013)

Part B.2: Portfolio Beta and Expected Return

Portfolio is formed through taking the equal weights of both Boral Limited and Reference

Company. In order to calculate the expected return it is important to estimate the portfolio beta

through use of following formula:

Beta of Boral Limited * Weight of Boral Limited + Beta of Reference company * Weight of

reference company (Arnold, 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

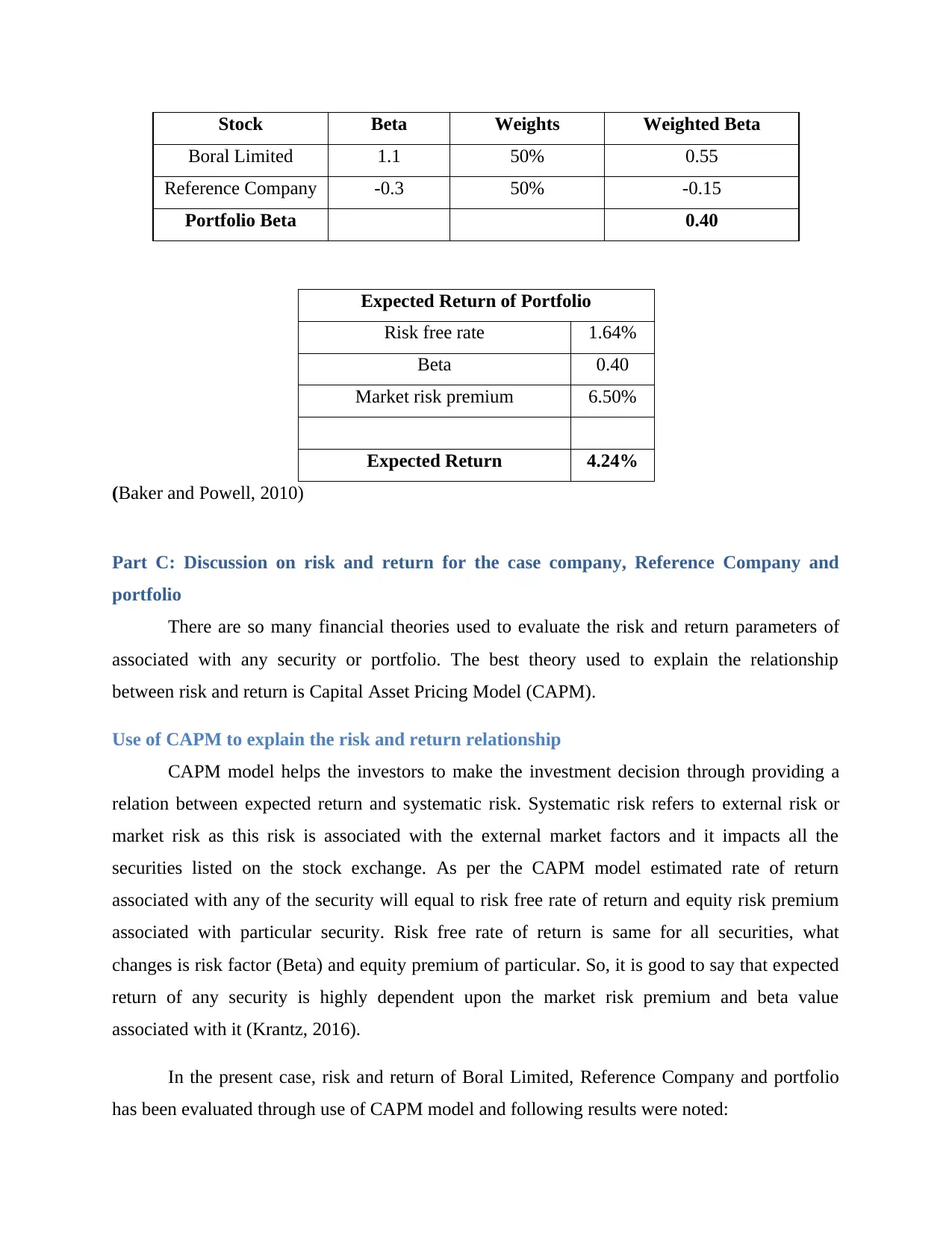

Stock Beta Weights Weighted Beta

Boral Limited 1.1 50% 0.55

Reference Company -0.3 50% -0.15

Portfolio Beta 0.40

Expected Return of Portfolio

Risk free rate 1.64%

Beta 0.40

Market risk premium 6.50%

Expected Return 4.24%

(Baker and Powell, 2010)

Part C: Discussion on risk and return for the case company, Reference Company and

portfolio

There are so many financial theories used to evaluate the risk and return parameters of

associated with any security or portfolio. The best theory used to explain the relationship

between risk and return is Capital Asset Pricing Model (CAPM).

Use of CAPM to explain the risk and return relationship

CAPM model helps the investors to make the investment decision through providing a

relation between expected return and systematic risk. Systematic risk refers to external risk or

market risk as this risk is associated with the external market factors and it impacts all the

securities listed on the stock exchange. As per the CAPM model estimated rate of return

associated with any of the security will equal to risk free rate of return and equity risk premium

associated with particular security. Risk free rate of return is same for all securities, what

changes is risk factor (Beta) and equity premium of particular. So, it is good to say that expected

return of any security is highly dependent upon the market risk premium and beta value

associated with it (Krantz, 2016).

In the present case, risk and return of Boral Limited, Reference Company and portfolio

has been evaluated through use of CAPM model and following results were noted:

Boral Limited 1.1 50% 0.55

Reference Company -0.3 50% -0.15

Portfolio Beta 0.40

Expected Return of Portfolio

Risk free rate 1.64%

Beta 0.40

Market risk premium 6.50%

Expected Return 4.24%

(Baker and Powell, 2010)

Part C: Discussion on risk and return for the case company, Reference Company and

portfolio

There are so many financial theories used to evaluate the risk and return parameters of

associated with any security or portfolio. The best theory used to explain the relationship

between risk and return is Capital Asset Pricing Model (CAPM).

Use of CAPM to explain the risk and return relationship

CAPM model helps the investors to make the investment decision through providing a

relation between expected return and systematic risk. Systematic risk refers to external risk or

market risk as this risk is associated with the external market factors and it impacts all the

securities listed on the stock exchange. As per the CAPM model estimated rate of return

associated with any of the security will equal to risk free rate of return and equity risk premium

associated with particular security. Risk free rate of return is same for all securities, what

changes is risk factor (Beta) and equity premium of particular. So, it is good to say that expected

return of any security is highly dependent upon the market risk premium and beta value

associated with it (Krantz, 2016).

In the present case, risk and return of Boral Limited, Reference Company and portfolio

has been evaluated through use of CAPM model and following results were noted:

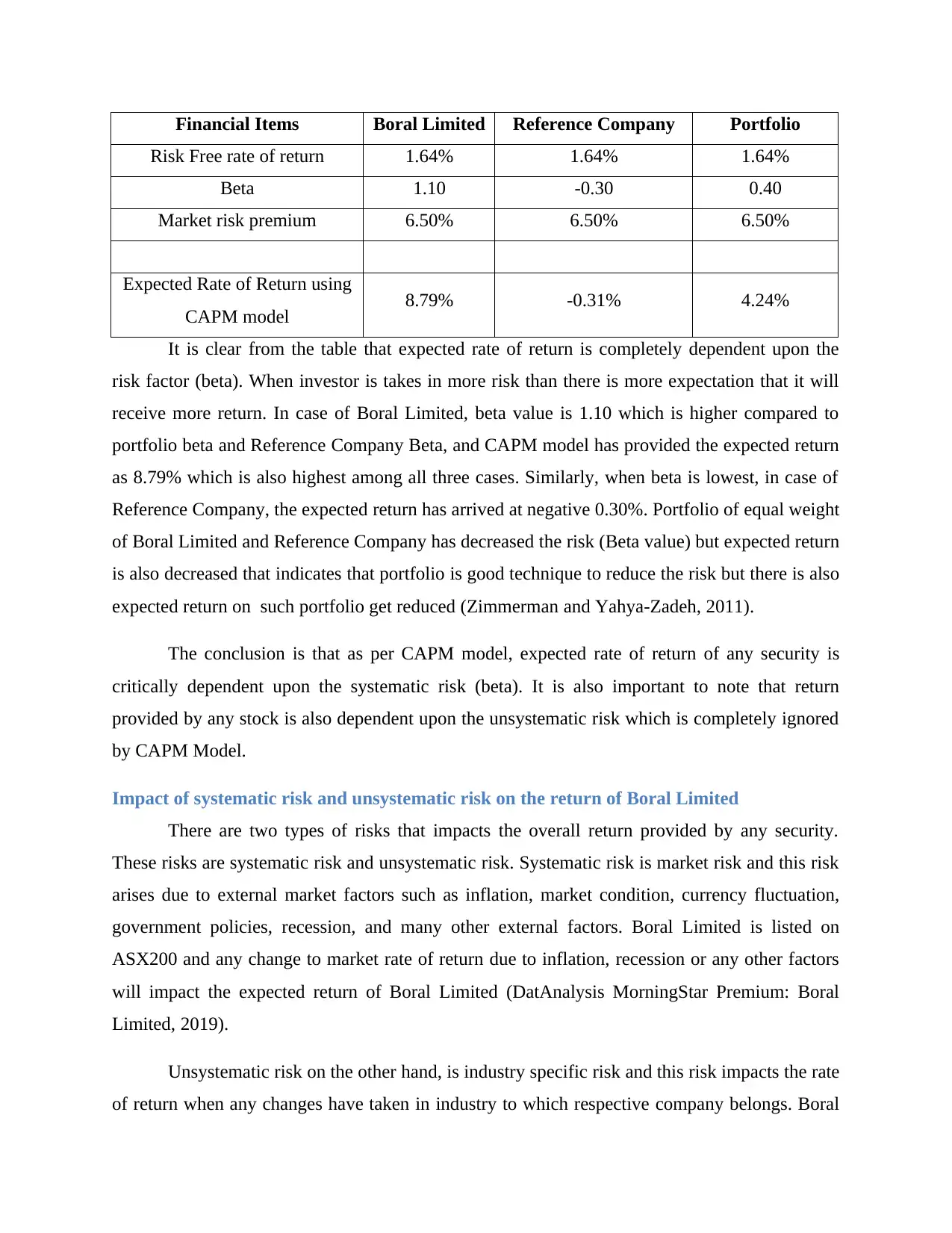

Financial Items Boral Limited Reference Company Portfolio

Risk Free rate of return 1.64% 1.64% 1.64%

Beta 1.10 -0.30 0.40

Market risk premium 6.50% 6.50% 6.50%

Expected Rate of Return using

CAPM model 8.79% -0.31% 4.24%

It is clear from the table that expected rate of return is completely dependent upon the

risk factor (beta). When investor is takes in more risk than there is more expectation that it will

receive more return. In case of Boral Limited, beta value is 1.10 which is higher compared to

portfolio beta and Reference Company Beta, and CAPM model has provided the expected return

as 8.79% which is also highest among all three cases. Similarly, when beta is lowest, in case of

Reference Company, the expected return has arrived at negative 0.30%. Portfolio of equal weight

of Boral Limited and Reference Company has decreased the risk (Beta value) but expected return

is also decreased that indicates that portfolio is good technique to reduce the risk but there is also

expected return on such portfolio get reduced (Zimmerman and Yahya-Zadeh, 2011).

The conclusion is that as per CAPM model, expected rate of return of any security is

critically dependent upon the systematic risk (beta). It is also important to note that return

provided by any stock is also dependent upon the unsystematic risk which is completely ignored

by CAPM Model.

Impact of systematic risk and unsystematic risk on the return of Boral Limited

There are two types of risks that impacts the overall return provided by any security.

These risks are systematic risk and unsystematic risk. Systematic risk is market risk and this risk

arises due to external market factors such as inflation, market condition, currency fluctuation,

government policies, recession, and many other external factors. Boral Limited is listed on

ASX200 and any change to market rate of return due to inflation, recession or any other factors

will impact the expected return of Boral Limited (DatAnalysis MorningStar Premium: Boral

Limited, 2019).

Unsystematic risk on the other hand, is industry specific risk and this risk impacts the rate

of return when any changes have taken in industry to which respective company belongs. Boral

Risk Free rate of return 1.64% 1.64% 1.64%

Beta 1.10 -0.30 0.40

Market risk premium 6.50% 6.50% 6.50%

Expected Rate of Return using

CAPM model 8.79% -0.31% 4.24%

It is clear from the table that expected rate of return is completely dependent upon the

risk factor (beta). When investor is takes in more risk than there is more expectation that it will

receive more return. In case of Boral Limited, beta value is 1.10 which is higher compared to

portfolio beta and Reference Company Beta, and CAPM model has provided the expected return

as 8.79% which is also highest among all three cases. Similarly, when beta is lowest, in case of

Reference Company, the expected return has arrived at negative 0.30%. Portfolio of equal weight

of Boral Limited and Reference Company has decreased the risk (Beta value) but expected return

is also decreased that indicates that portfolio is good technique to reduce the risk but there is also

expected return on such portfolio get reduced (Zimmerman and Yahya-Zadeh, 2011).

The conclusion is that as per CAPM model, expected rate of return of any security is

critically dependent upon the systematic risk (beta). It is also important to note that return

provided by any stock is also dependent upon the unsystematic risk which is completely ignored

by CAPM Model.

Impact of systematic risk and unsystematic risk on the return of Boral Limited

There are two types of risks that impacts the overall return provided by any security.

These risks are systematic risk and unsystematic risk. Systematic risk is market risk and this risk

arises due to external market factors such as inflation, market condition, currency fluctuation,

government policies, recession, and many other external factors. Boral Limited is listed on

ASX200 and any change to market rate of return due to inflation, recession or any other factors

will impact the expected return of Boral Limited (DatAnalysis MorningStar Premium: Boral

Limited, 2019).

Unsystematic risk on the other hand, is industry specific risk and this risk impacts the rate

of return when any changes have taken in industry to which respective company belongs. Boral

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limited belongs to construction industry in Australia and as per IBIS World report on

Construction industry of Australia, weal infrastructure and building investment has lead to

decline in revenue over the last 5 years. However there is heavy demand of construction material

in all of Australia due to ongoing project but government pricing policies and environmental

factors has led Boral Limited to limit their profits. So, it can be said that construction industry of

Australia is governed and regulated with competitive pricing and strict government policies with

regard to environment and other factors (IBIS World, 2019).

Construction industry of Australia, weal infrastructure and building investment has lead to

decline in revenue over the last 5 years. However there is heavy demand of construction material

in all of Australia due to ongoing project but government pricing policies and environmental

factors has led Boral Limited to limit their profits. So, it can be said that construction industry of

Australia is governed and regulated with competitive pricing and strict government policies with

regard to environment and other factors (IBIS World, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. and Powell, G. 2010. Understanding Financial Management: A Practical Guide.

USA: John Wiley & Sons.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

DatAnalysis MorningStar Premium: Boral Limited. 2019. Key Data. [Online]. Available at:

https://datanalysis-morningstar-com-au.ezproxy.uow.edu.au/af/company/pricesensmeasures?

ASXCode=BLD&xtm-licensee=datpremium [Accessed on: 22 May, 2019].

IBIS World. 2019. Commercial and Industrial Building Construction - Australia Market

Research Report. . [Online]. Available at: https://www.ibisworld.com.au/industry-trends/market-

research-reports/construction/building/commercial-industrial-building-construction.html

[Accessed on: 22 May, 2019].

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All Types

of Data. USA: John Wiley & Sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Reserve Bank of Australia. 2019. Interest rates. [Online]. Available at:

https://www.rba.gov.au/statistics/tables/ [Accessed on: 22 May, 2019].

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Baker, K. and Powell, G. 2010. Understanding Financial Management: A Practical Guide.

USA: John Wiley & Sons.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

DatAnalysis MorningStar Premium: Boral Limited. 2019. Key Data. [Online]. Available at:

https://datanalysis-morningstar-com-au.ezproxy.uow.edu.au/af/company/pricesensmeasures?

ASXCode=BLD&xtm-licensee=datpremium [Accessed on: 22 May, 2019].

IBIS World. 2019. Commercial and Industrial Building Construction - Australia Market

Research Report. . [Online]. Available at: https://www.ibisworld.com.au/industry-trends/market-

research-reports/construction/building/commercial-industrial-building-construction.html

[Accessed on: 22 May, 2019].

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Phillips, P.P. and Stawarski, C.A. 2016. Data Collection: Planning for and Collecting All Types

of Data. USA: John Wiley & Sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Reserve Bank of Australia. 2019. Interest rates. [Online]. Available at:

https://www.rba.gov.au/statistics/tables/ [Accessed on: 22 May, 2019].

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

control. Issues in Accounting Education, 26(1), pp.258-259.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.