Detailed Cash Flow Analysis of Accent Group Ltd - HI5020 Report

VerifiedAdded on 2024/05/31

|13

|2788

|316

Report

AI Summary

This report provides a detailed analysis of Accent Group Limited's cash flow statements for the financial years 2015, 2016, and 2017. It examines cash flow from operating, investing, and financing activities, highlighting trends and their implications for the company's financial health. The analysis covers the impact of operating activities on net profit, the company's investment strategies in fixed assets, and the effects of financing activities, including debt issuance and common stock offerings. Additionally, the report discusses other comprehensive income items, such as foreign exchange translation, and addresses accounting for corporate income tax. The report concludes that Accent Group has shown sound financial performance over the period, with positive cash flows from operating activities indicating strong core business earnings.

HI5020

Corporate Accounting

1

Corporate Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction:....................................................................................................................................3

Cash flow statement.........................................................................................................................4

Analysis of cash flow generated from operating activities..............................................................5

Analysis of cash flow from investing activities...............................................................................6

Analysis of cash flow from financing activities..............................................................................7

Analysis...........................................................................................................................................7

Cash flow from operating activities –..............................................................................................7

Cash flow from investing activities.................................................................................................7

Cash flow from financing activities-...............................................................................................8

Other comprehensive income statement:.........................................................................................9

Accounting for corporate income tax:...........................................................................................10

Conclusion:....................................................................................................................................11

References......................................................................................................................................12

2

Introduction:....................................................................................................................................3

Cash flow statement.........................................................................................................................4

Analysis of cash flow generated from operating activities..............................................................5

Analysis of cash flow from investing activities...............................................................................6

Analysis of cash flow from financing activities..............................................................................7

Analysis...........................................................................................................................................7

Cash flow from operating activities –..............................................................................................7

Cash flow from investing activities.................................................................................................7

Cash flow from financing activities-...............................................................................................8

Other comprehensive income statement:.........................................................................................9

Accounting for corporate income tax:...........................................................................................10

Conclusion:....................................................................................................................................11

References......................................................................................................................................12

2

Introduction:

Accent group Limited is a listed company on the Australian securities exchange board and is

the regional leader in the retail and distribution of various footwears with around 420 spaces

situated in 10 different part of the country. The company has huge market in Australia and New

Zealand. The company believes in customer satisfaction and providing a class of footwear. It

was founded in the year 2000 and since then the company is unstoppable. The company has

many brands running under the name of the same company. In the financial year 2017 the

company has witnessed good profits and plus enhancing shareholders wealth.

3

Accent group Limited is a listed company on the Australian securities exchange board and is

the regional leader in the retail and distribution of various footwears with around 420 spaces

situated in 10 different part of the country. The company has huge market in Australia and New

Zealand. The company believes in customer satisfaction and providing a class of footwear. It

was founded in the year 2000 and since then the company is unstoppable. The company has

many brands running under the name of the same company. In the financial year 2017 the

company has witnessed good profits and plus enhancing shareholders wealth.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

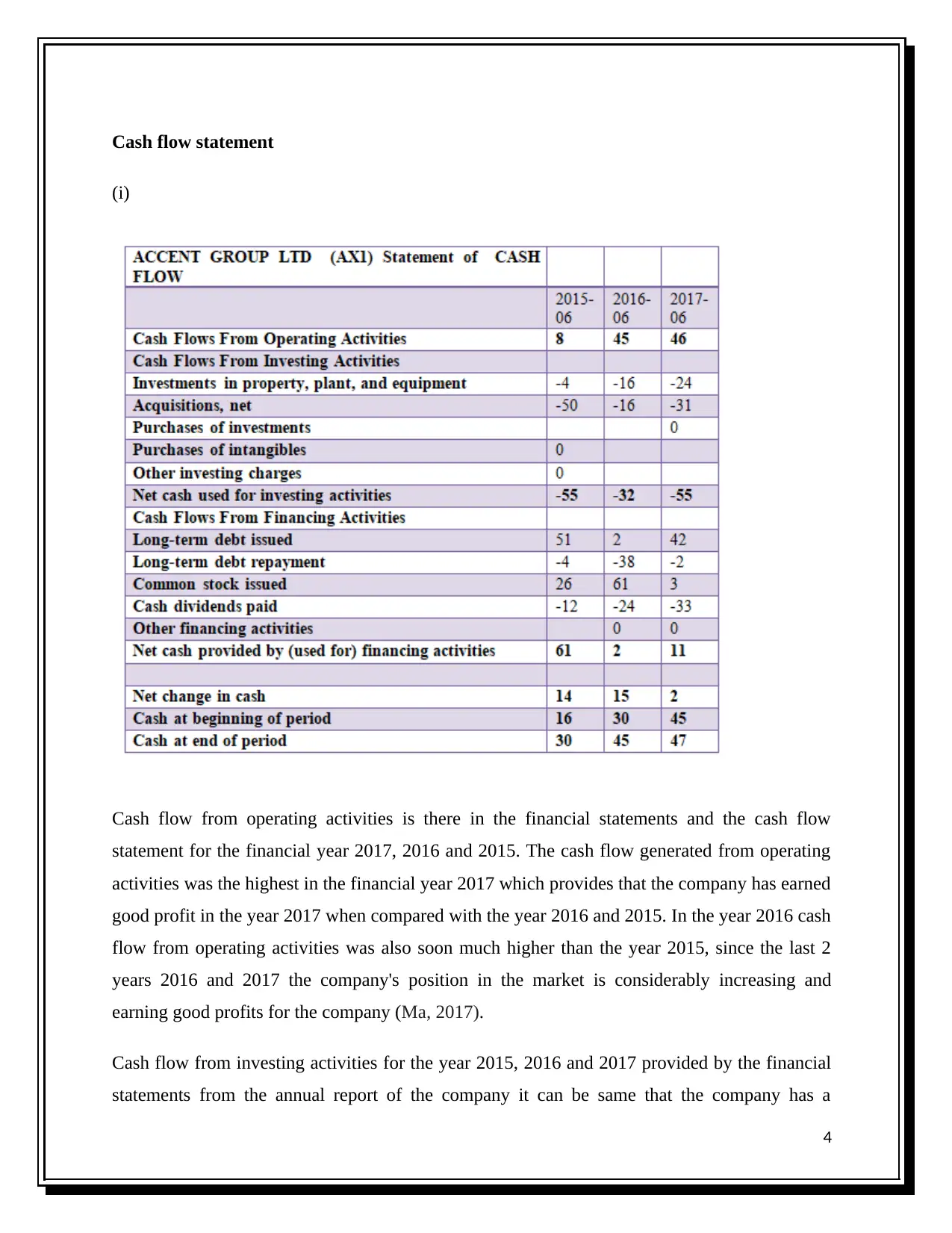

Cash flow statement

(i)

Cash flow from operating activities is there in the financial statements and the cash flow

statement for the financial year 2017, 2016 and 2015. The cash flow generated from operating

activities was the highest in the financial year 2017 which provides that the company has earned

good profit in the year 2017 when compared with the year 2016 and 2015. In the year 2016 cash

flow from operating activities was also soon much higher than the year 2015, since the last 2

years 2016 and 2017 the company's position in the market is considerably increasing and

earning good profits for the company (Ma, 2017).

Cash flow from investing activities for the year 2015, 2016 and 2017 provided by the financial

statements from the annual report of the company it can be same that the company has a

4

(i)

Cash flow from operating activities is there in the financial statements and the cash flow

statement for the financial year 2017, 2016 and 2015. The cash flow generated from operating

activities was the highest in the financial year 2017 which provides that the company has earned

good profit in the year 2017 when compared with the year 2016 and 2015. In the year 2016 cash

flow from operating activities was also soon much higher than the year 2015, since the last 2

years 2016 and 2017 the company's position in the market is considerably increasing and

earning good profits for the company (Ma, 2017).

Cash flow from investing activities for the year 2015, 2016 and 2017 provided by the financial

statements from the annual report of the company it can be same that the company has a

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

negative cash flow from operating activities which provide that the company is more of

investing then selling such Investments. The company has made huge Investments for the

purpose of increasing its business premises the company has invested in plant, property and

equipment the most. The purpose behind investing in such areas is that the company is clear

with its intentions that it has to increase its business in the upcoming future and that is our

company is investing in such plant, property and equipments. In all the three years the

investment is done by the company but in 2017 the company has made huge Investments in

property, plant and equipment. The company has made no investment in the intangible and

other investing charges for all the financial years’ data 2016, 2015 and 2017.

Cash flow from financing activities for the financial year 2015, 2016 and 2017 from the cash

flow statement that is provided by the Annual General report of the company for the financial

year 2017 is found that cash flow from financing activities or the net cash flow from financing

activities was the highest in the year 2015 that means issuance of long term debt was done most

in the year 2015 and the repayment was not done in the year 2015. The purpose behind the issue

of debt in all the years ‘is to provide cash for the company to run its business and to enhance his

business.

(ii)

Analysis of cash flow generated from operating activities-

When the various items that are given in the cash flow statements are influenced with the net

profit of the company the operating cash flow can be generated. The operating income for the

organization can be provided by reducing depreciation and the working capital that has been

properly calculated has to be monitored with the net profit of the entity. For the purpose of

calculating the various cash flows generated from the operating activities is not to include the

items which fall under the heading cash flow generated from investing activities and cash flow

generated from financing activities (McInnis, 2018). With the help of such bifurcation there

shall be no confusion in the calculation of cash flow generated from operating activities as only

the items that are to be adjusted with their cash flow from operating activities shall be placed

together.

5

investing then selling such Investments. The company has made huge Investments for the

purpose of increasing its business premises the company has invested in plant, property and

equipment the most. The purpose behind investing in such areas is that the company is clear

with its intentions that it has to increase its business in the upcoming future and that is our

company is investing in such plant, property and equipments. In all the three years the

investment is done by the company but in 2017 the company has made huge Investments in

property, plant and equipment. The company has made no investment in the intangible and

other investing charges for all the financial years’ data 2016, 2015 and 2017.

Cash flow from financing activities for the financial year 2015, 2016 and 2017 from the cash

flow statement that is provided by the Annual General report of the company for the financial

year 2017 is found that cash flow from financing activities or the net cash flow from financing

activities was the highest in the year 2015 that means issuance of long term debt was done most

in the year 2015 and the repayment was not done in the year 2015. The purpose behind the issue

of debt in all the years ‘is to provide cash for the company to run its business and to enhance his

business.

(ii)

Analysis of cash flow generated from operating activities-

When the various items that are given in the cash flow statements are influenced with the net

profit of the company the operating cash flow can be generated. The operating income for the

organization can be provided by reducing depreciation and the working capital that has been

properly calculated has to be monitored with the net profit of the entity. For the purpose of

calculating the various cash flows generated from the operating activities is not to include the

items which fall under the heading cash flow generated from investing activities and cash flow

generated from financing activities (McInnis, 2018). With the help of such bifurcation there

shall be no confusion in the calculation of cash flow generated from operating activities as only

the items that are to be adjusted with their cash flow from operating activities shall be placed

together.

5

As per the cash flow provided by the annual General report of the companies it can be evaluated

that cash flow from operating activities are present for the company and the company is running

a successful business and day by day the company is enhancing and increasing its business

opportunities. The objective behind the cash flow from operating activities to ascertain the

company's actual position to repay its actual debts that the company is going through. Operating

expenses are referring a nature and division of the financial statements of the company can with

the help of the cash flow ascertain that whether the company is in the position to pay off its

operating expenses and have sufficient working capital requirement to fulfill its daily needs of

cash outflow.

Analysis of cash flow from investing activities- All the line items under the heading of cash

flow from investing activities have to be considered together by bringing them together under

this heading. When all the activities relating to cash flow from investing activities are held

together then the final amount which is to be receivable or payable by the company can be

calculated separately. The sale of fixed assets and Investments that are held by the company

during the financial year have to be considered for the purpose of cash flow from investing

activities and the purchase of fixed assets and investment which the company does from the

cash flows that the company has generated during the financial year are also considered for the

purpose of cash flow from investing activities. When the company brings in fixed assets and

sells them the net cash flow from such activities can be identified and reported and under cash

flows by investment activities (Annual Report, 2017).

The cash flow from investment activities can be up to type when negative cash flow is and the

other is positive cash flow. Negative cash flow occurs when there is a purchase or an outflow of

cash is made by the company during the financial year. This could be done by making an

investment for the company through which the cash availability in the company gets reduced.

Whereas cash flow from investment activities can be positive as well, when sale or cash inflow

takes place within the company it is called as quality cashless of the company. With the help of

positive cash flow because availability in the company gets increased and such increased cash

the company can repay its other expenses.

6

that cash flow from operating activities are present for the company and the company is running

a successful business and day by day the company is enhancing and increasing its business

opportunities. The objective behind the cash flow from operating activities to ascertain the

company's actual position to repay its actual debts that the company is going through. Operating

expenses are referring a nature and division of the financial statements of the company can with

the help of the cash flow ascertain that whether the company is in the position to pay off its

operating expenses and have sufficient working capital requirement to fulfill its daily needs of

cash outflow.

Analysis of cash flow from investing activities- All the line items under the heading of cash

flow from investing activities have to be considered together by bringing them together under

this heading. When all the activities relating to cash flow from investing activities are held

together then the final amount which is to be receivable or payable by the company can be

calculated separately. The sale of fixed assets and Investments that are held by the company

during the financial year have to be considered for the purpose of cash flow from investing

activities and the purchase of fixed assets and investment which the company does from the

cash flows that the company has generated during the financial year are also considered for the

purpose of cash flow from investing activities. When the company brings in fixed assets and

sells them the net cash flow from such activities can be identified and reported and under cash

flows by investment activities (Annual Report, 2017).

The cash flow from investment activities can be up to type when negative cash flow is and the

other is positive cash flow. Negative cash flow occurs when there is a purchase or an outflow of

cash is made by the company during the financial year. This could be done by making an

investment for the company through which the cash availability in the company gets reduced.

Whereas cash flow from investment activities can be positive as well, when sale or cash inflow

takes place within the company it is called as quality cashless of the company. With the help of

positive cash flow because availability in the company gets increased and such increased cash

the company can repay its other expenses.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysis of cash flow from financing activities- Transactions that involve the stakeholder in

the owner of the company results in the cash flow from financing activities. Such transactions

have to be mentioned in the cash flow from financing activities. Cash flow from financing

activities can be of two types when was positive cash flow and the other is negative cash flow.

When the company issues debt instrument then there is an inflow of cash in the company. When

the company receives various dividends from different companies in which the company has its

stake/ investment then it leads to positive cash flow for the company as the cash flows within

the company as the company receives dividend from another company which leads to positive

cash inflow for the company.

Analysis

Cash flow from operating activities –

For the company the cash flow generated from operating business present in the cash flow

statement that the company has provided in the annual report of the year 2015, 2016 and 2017.

Because of which it can be said that the company's current position and the company's position

in the past few years is very sound. The company has good earnings from their core business

and the company is running smoothly. For the past 3 years the company has cash flows from

operating activities through which the reports can be generated by the department managers and

should be provided to the uses of the reports. The report generated is the new closed by the

investors/ borrowers so that they can invest or lend money to the company by analyzing the

company's position of repaying its debts.

Cash flow from investing activities –

The company provided has sufficient cash flows regulations from the activities that belong to

investments. When cash flow statements of the company that are provided in the annual reports

of the year 2015,2016 and 2017 are viewed, it can be found out that the organization has

purchased/ invested in various fixed assets during the three fiscal years. Huge investments are

made by the company in all the three financial years in the fixed assets of the company through

which it can be analyzed that the company might not have sufficient funds to pay off its

operating expenses, debt liabilities for the upcoming future. But on analyzing the funds of the

7

the owner of the company results in the cash flow from financing activities. Such transactions

have to be mentioned in the cash flow from financing activities. Cash flow from financing

activities can be of two types when was positive cash flow and the other is negative cash flow.

When the company issues debt instrument then there is an inflow of cash in the company. When

the company receives various dividends from different companies in which the company has its

stake/ investment then it leads to positive cash flow for the company as the cash flows within

the company as the company receives dividend from another company which leads to positive

cash inflow for the company.

Analysis

Cash flow from operating activities –

For the company the cash flow generated from operating business present in the cash flow

statement that the company has provided in the annual report of the year 2015, 2016 and 2017.

Because of which it can be said that the company's current position and the company's position

in the past few years is very sound. The company has good earnings from their core business

and the company is running smoothly. For the past 3 years the company has cash flows from

operating activities through which the reports can be generated by the department managers and

should be provided to the uses of the reports. The report generated is the new closed by the

investors/ borrowers so that they can invest or lend money to the company by analyzing the

company's position of repaying its debts.

Cash flow from investing activities –

The company provided has sufficient cash flows regulations from the activities that belong to

investments. When cash flow statements of the company that are provided in the annual reports

of the year 2015,2016 and 2017 are viewed, it can be found out that the organization has

purchased/ invested in various fixed assets during the three fiscal years. Huge investments are

made by the company in all the three financial years in the fixed assets of the company through

which it can be analyzed that the company might not have sufficient funds to pay off its

operating expenses, debt liabilities for the upcoming future. But on analyzing the funds of the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

companies it was found that the company has negative cash flow from investment activities for

all the three financial years that have been provided in the cash flow statement. The concert in

the world investment in the various causes effects and has not told anything they said during the

last three accounting years. Do cash flow from investing activities from the company is

negative.

Cash flow from financing activities-

For the company that has been provided it can be found that cash flow from financing activities

are provided in the cash flow statement of the company for the last years 2015, 2016 and 2017

as per the statement provided in the annual report provided by the company. The company has

positive cash flow from financing activities as the company is issuing more and more long term

debt when repaying them through which the countries cash inflow is higher than the cash

outflow which is resulting in operating cash flow for the company. With the help of such

positive cash flow which has been generated from financing activities can be used to pay

various dividend and other financing activities can be paid off with the help of be positive cash

flow that has been generated from the financing activities. Cash flow from financing activities

was generated from common stock by the company in all the three financial year. Issuance of

common stock led to a positive cash flow for the company.

8

all the three financial years that have been provided in the cash flow statement. The concert in

the world investment in the various causes effects and has not told anything they said during the

last three accounting years. Do cash flow from investing activities from the company is

negative.

Cash flow from financing activities-

For the company that has been provided it can be found that cash flow from financing activities

are provided in the cash flow statement of the company for the last years 2015, 2016 and 2017

as per the statement provided in the annual report provided by the company. The company has

positive cash flow from financing activities as the company is issuing more and more long term

debt when repaying them through which the countries cash inflow is higher than the cash

outflow which is resulting in operating cash flow for the company. With the help of such

positive cash flow which has been generated from financing activities can be used to pay

various dividend and other financing activities can be paid off with the help of be positive cash

flow that has been generated from the financing activities. Cash flow from financing activities

was generated from common stock by the company in all the three financial year. Issuance of

common stock led to a positive cash flow for the company.

8

Other comprehensive income statement:

(iii) Other comprehensive items are the part of the company financial statements. That the

company provided movement in net change in cash flow value as been made in all the 3 years

that are 2015, 2016 and 2017. Because of such foreign hedge reserves there have been a foreign

exchange translation in the other comprehensive income which has been reported in all the three

financial years by the company. It is expected from the company that such foreign exchange

translation has to be reported every year by the company as company is involved in foreign

hedge Reserves which are the part of the company's business (Graham, et. al., 2012).

(iv) The risk associated with recognition of asset or liabilities that are the part of the cash flow

statement have to be reported as hedge. Such hedge has to be reported separately as other

comprehensive income. The income which do not form part of the income statement of the

company has to be reported as other comprehensive income. Foreign exchange escalation on

The Hedge reserve is due to the export and the import conducted by the company during all the

three financial years that are reported in the Annual report.

(v) The income that is reported under the heading other comprehensive income have to be

reported separately because there recognition is not certain and being confused about full for the

company are to be reported under the heading other comprehensive income.

9

(iii) Other comprehensive items are the part of the company financial statements. That the

company provided movement in net change in cash flow value as been made in all the 3 years

that are 2015, 2016 and 2017. Because of such foreign hedge reserves there have been a foreign

exchange translation in the other comprehensive income which has been reported in all the three

financial years by the company. It is expected from the company that such foreign exchange

translation has to be reported every year by the company as company is involved in foreign

hedge Reserves which are the part of the company's business (Graham, et. al., 2012).

(iv) The risk associated with recognition of asset or liabilities that are the part of the cash flow

statement have to be reported as hedge. Such hedge has to be reported separately as other

comprehensive income. The income which do not form part of the income statement of the

company has to be reported as other comprehensive income. Foreign exchange escalation on

The Hedge reserve is due to the export and the import conducted by the company during all the

three financial years that are reported in the Annual report.

(v) The income that is reported under the heading other comprehensive income have to be

reported separately because there recognition is not certain and being confused about full for the

company are to be reported under the heading other comprehensive income.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for corporate income tax:

(vi)

The tax expense for the company for the year 2017 as per the annual report of the company is

12,072 thousand dollars.

(vii)

The company comes in the Tax slab of 30% tax rate and the company has to pay taxes as per

the income that has been calculated as per the tax requirement. But there's a difference in the

income calculated as per the requirement of tax and the income as per the accounts of the

company. This difference is because of the deferred tax liability of 8,716 thousand dollars,

because of the deferred tax liability there is a difference between the accounting income and

income reported by the company and its annual report (Brouwer and Naarding, 2018).

(viii)

Deferred tax liability of 8,716 thousand dollars weather winter side by the company due to

which there was the tax effect. This is .because of the timing difference that has reduced the

accounting income of the company (Mgammal and Ismail, 2015)

(ix)

For the financial year 2017 the company has to pay taxes as per the requirement of the law of

Australia. The tax rate applicable is 30%.

(x)

No, the income tax shown in the cash flow statement of the company and the income tax that

has been paid by the company is different because of the deferred tax liability and the various

timing differences that have caused this difference.

(xi)

10

(vi)

The tax expense for the company for the year 2017 as per the annual report of the company is

12,072 thousand dollars.

(vii)

The company comes in the Tax slab of 30% tax rate and the company has to pay taxes as per

the income that has been calculated as per the tax requirement. But there's a difference in the

income calculated as per the requirement of tax and the income as per the accounts of the

company. This difference is because of the deferred tax liability of 8,716 thousand dollars,

because of the deferred tax liability there is a difference between the accounting income and

income reported by the company and its annual report (Brouwer and Naarding, 2018).

(viii)

Deferred tax liability of 8,716 thousand dollars weather winter side by the company due to

which there was the tax effect. This is .because of the timing difference that has reduced the

accounting income of the company (Mgammal and Ismail, 2015)

(ix)

For the financial year 2017 the company has to pay taxes as per the requirement of the law of

Australia. The tax rate applicable is 30%.

(x)

No, the income tax shown in the cash flow statement of the company and the income tax that

has been paid by the company is different because of the deferred tax liability and the various

timing differences that have caused this difference.

(xi)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There were no tax expenses that the company has paid where shown in the cash flow from

operating activities as per the annual report of 2017. Also it is such a big company and the

revenues and expenses that the company conducted in the financial year are low (Noor, et. al.,

2012).

Conclusion:

Accent group limited is a company in which cash flow statement I prepared by the management

and the cash flow from operating and financing activities are found to be positive through

which the company's various expenses can be made on timely basis. Whereas the company's

financial statements in which class flow from investing activities were considered it was found

that the company is investing more the prevention negative factors of the company. Overall

band company was taken the company is successfully growing every year and has good future

aspects. The company should increase its products to increase its revenues in the upcoming

future.

11

operating activities as per the annual report of 2017. Also it is such a big company and the

revenues and expenses that the company conducted in the financial year are low (Noor, et. al.,

2012).

Conclusion:

Accent group limited is a company in which cash flow statement I prepared by the management

and the cash flow from operating and financing activities are found to be positive through

which the company's various expenses can be made on timely basis. Whereas the company's

financial statements in which class flow from investing activities were considered it was found

that the company is investing more the prevention negative factors of the company. Overall

band company was taken the company is successfully growing every year and has good future

aspects. The company should increase its products to increase its revenues in the upcoming

future.

11

References

Annual Report, 2017. Accent Group Limited. Available at:

http://www.accentgroup.org/media/258546/report-and-accounts-2017.pdf Accessed on

May 24, 2018

Brouwer, A. and Naarding, E., 2018. Making Deferred Taxes Relevant. Accounting in

Europe, pp.1-31

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434

Ma, X., 2017. Advancing Direct Corporate Accountability in International Human

Rights Law: The Role of State-Owned Enterprises (Master's thesis)

McInnis, M., 2018. An Analysis of Managerial Accounting and Corporate Reporting

Practices (Doctoral dissertation, University of Mississippi)

Mgammal, M.H. and Ismail, K.N.I.K., 2015. Corporate tax planning activities: overview

of concepts, theories, restrictions, motivations and approaches. Mediterranean Journal

of Social Sciences, 6(6 S4), p.350.

Noor, M.I., Nour, A. and Musa, S., 2012. The Role of Cash Flow in Explaining the

Change in Company Liquidity. Journal of Advanced Social Research Vol, 2(4), pp.231-

243.

12

Annual Report, 2017. Accent Group Limited. Available at:

http://www.accentgroup.org/media/258546/report-and-accounts-2017.pdf Accessed on

May 24, 2018

Brouwer, A. and Naarding, E., 2018. Making Deferred Taxes Relevant. Accounting in

Europe, pp.1-31

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434

Ma, X., 2017. Advancing Direct Corporate Accountability in International Human

Rights Law: The Role of State-Owned Enterprises (Master's thesis)

McInnis, M., 2018. An Analysis of Managerial Accounting and Corporate Reporting

Practices (Doctoral dissertation, University of Mississippi)

Mgammal, M.H. and Ismail, K.N.I.K., 2015. Corporate tax planning activities: overview

of concepts, theories, restrictions, motivations and approaches. Mediterranean Journal

of Social Sciences, 6(6 S4), p.350.

Noor, M.I., Nour, A. and Musa, S., 2012. The Role of Cash Flow in Explaining the

Change in Company Liquidity. Journal of Advanced Social Research Vol, 2(4), pp.231-

243.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.