ACCG101 Report: Inventory Management's Impact on Profitability

VerifiedAdded on 2023/06/06

|6

|1131

|84

Report

AI Summary

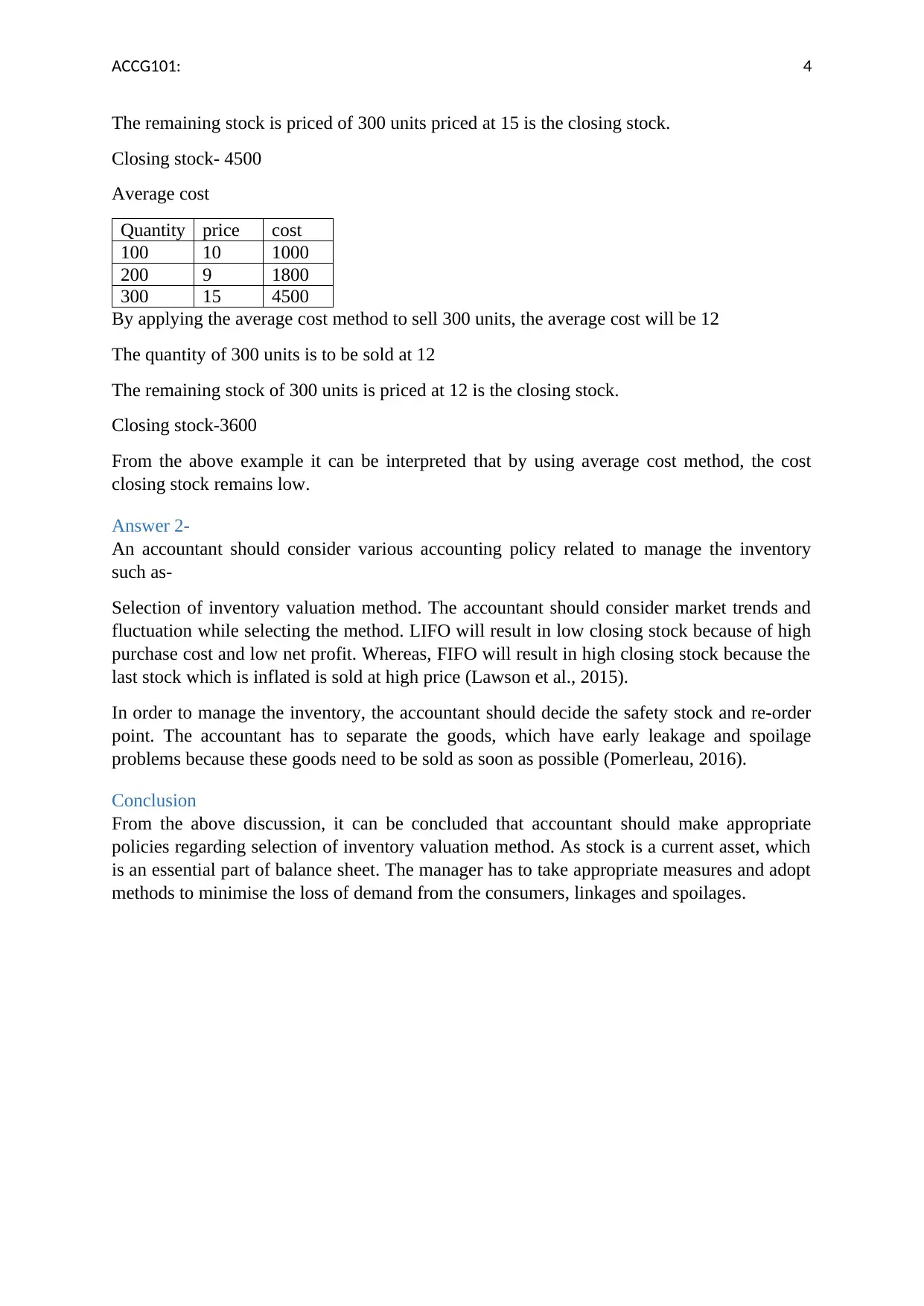

This report examines the impact of inventory management on profitability, particularly focusing on the Automotive Holdings Group. It discusses the average cost method and compares it with FIFO, analyzing their effects on the profit and loss statement. The report highlights how the average cost method influences quarterly and annual financial statements and explores the importance of selecting appropriate accounting policies for inventory valuation. It emphasizes considerations such as market trends, safety stock levels, and the handling of perishable goods to minimize losses and optimize inventory management practices. The document concludes that strategic inventory policies are crucial for maintaining accurate financial reporting and minimizing potential losses, with Desklib offering additional resources for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.