ACCG315 Case Study: Navigating Ethics and Profit in Australian Retail

VerifiedAdded on 2023/06/07

|12

|3954

|332

Case Study

AI Summary

This case study delves into the ethical and financial challenges confronting the Australian retail sector, marked by pressures on sales growth and the need for cost reduction. It examines issues such as maintaining good faith in supplier relationships, the voluntary nature of the Food and Grocery Code of Conduct, and the appropriateness of decision-making power within organizations. The report further analyzes the impact of delayed payments to suppliers, the application of developed country employment standards in less developed countries, and the benefits of cost leadership models. It also explores integrated reporting, “at risk” remuneration components, and the importance of ethical behavior towards stakeholders. The study concludes by emphasizing the need for a balanced approach to profitability that considers ethical implications and stakeholder interests within the Australian retail landscape. Desklib provides students access to similar case studies and solutions.

Running head: ACCOUNTING IN PROFESSION

Accounting in Profession

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Accounting in Profession

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING IN PROFESSION

Table of Contents

Section 1: Abstract...........................................................................................................................2

Section 2: Introduction....................................................................................................................3

2.1 Summary for the case and background information of the industry:....................................3

2.2 Environment/context of the case:..........................................................................................3

2.3 Specific issues/challenges within the industry:.....................................................................4

Section 3: Responses to the case questions.....................................................................................5

3.1 Good faith:.............................................................................................................................5

3.2 Reason behind the thought of Food and Grocery of Conduct as a voluntary code:..............5

3.3 Appropriateness of decision making power as a senior manager and/or group and

assessment of its legitimacy:.......................................................................................................6

3.4 Techniques to respond to the provided situation and grounds to be used as bases:..............6

3.5 Ways of applying developed country standards of employment conditions to less

developed countries and information or frameworks for determining their appropriateness:.....6

3.6 Benefits to be enjoyed by the organisation by following cost (price) leadership model:......7

3.7 Techniques of conducting audit based on the provided situation:.........................................7

3.8 Integrated reporting, its achievements and use of this framework in changing performance

and remuneration system design:.................................................................................................8

3.9 Concept of “at risk” remuneration component and reason behind its larger component of

remuneration as found by the Productivity Commission report:.................................................8

3.10 Stakeholders and ethical behaviour from organisational perspective:................................9

Section 4: Conclusion....................................................................................................................10

References:....................................................................................................................................11

Table of Contents

Section 1: Abstract...........................................................................................................................2

Section 2: Introduction....................................................................................................................3

2.1 Summary for the case and background information of the industry:....................................3

2.2 Environment/context of the case:..........................................................................................3

2.3 Specific issues/challenges within the industry:.....................................................................4

Section 3: Responses to the case questions.....................................................................................5

3.1 Good faith:.............................................................................................................................5

3.2 Reason behind the thought of Food and Grocery of Conduct as a voluntary code:..............5

3.3 Appropriateness of decision making power as a senior manager and/or group and

assessment of its legitimacy:.......................................................................................................6

3.4 Techniques to respond to the provided situation and grounds to be used as bases:..............6

3.5 Ways of applying developed country standards of employment conditions to less

developed countries and information or frameworks for determining their appropriateness:.....6

3.6 Benefits to be enjoyed by the organisation by following cost (price) leadership model:......7

3.7 Techniques of conducting audit based on the provided situation:.........................................7

3.8 Integrated reporting, its achievements and use of this framework in changing performance

and remuneration system design:.................................................................................................8

3.9 Concept of “at risk” remuneration component and reason behind its larger component of

remuneration as found by the Productivity Commission report:.................................................8

3.10 Stakeholders and ethical behaviour from organisational perspective:................................9

Section 4: Conclusion....................................................................................................................10

References:....................................................................................................................................11

2ACCOUNTING IN PROFESSION

Section 1: Abstract

The report covers detailed analysis of the provided case study related to the Australian

retails sector with respect to the issues and challenges that the organisations are encountering in

carrying out their business operations along with the impact of such issues and challenges. It has

been gathered from the article that the retail sector in Australia is encountering a crisis due to the

fact that the prices of the commodities are still low in the retail outlets. Due to such lower prices,

it has become troublesome for the organisation to maintain the desired growth level. The

Australian economy has been blamed for this particular situation. Moreover, various case

questions have been discussed in this paper as well. The answers to the case questions have been

provided by using the information provided in the case study for arriving at an appropriate

response. The existing literature research has made contributions to the answer formulation as

well.

It is noteworthy to mention that the questions have been approached from an objective

viewpoint in order to avoid pegging the responses on an individual organisation, despite the fact

that they have direct relationship with the case study. Certain additional materials have been used

by using past researches associated with the retail business and the issues confronting the

business organisations including the techniques of managing and overcoming such challenges.

The particular paper provides the readers with critical knowledge of the various influential

dynamics confronting the retail sector in Australia. Most importantly, the paper assists the

readers in gaining an insight that even though there is existence of big multinational

organisations, the industry could encounter a number of critical issues, which might have adverse

impact on the overall sector of the nation. Such impact could affect the business operations of the

sector as well.

Section 1: Abstract

The report covers detailed analysis of the provided case study related to the Australian

retails sector with respect to the issues and challenges that the organisations are encountering in

carrying out their business operations along with the impact of such issues and challenges. It has

been gathered from the article that the retail sector in Australia is encountering a crisis due to the

fact that the prices of the commodities are still low in the retail outlets. Due to such lower prices,

it has become troublesome for the organisation to maintain the desired growth level. The

Australian economy has been blamed for this particular situation. Moreover, various case

questions have been discussed in this paper as well. The answers to the case questions have been

provided by using the information provided in the case study for arriving at an appropriate

response. The existing literature research has made contributions to the answer formulation as

well.

It is noteworthy to mention that the questions have been approached from an objective

viewpoint in order to avoid pegging the responses on an individual organisation, despite the fact

that they have direct relationship with the case study. Certain additional materials have been used

by using past researches associated with the retail business and the issues confronting the

business organisations including the techniques of managing and overcoming such challenges.

The particular paper provides the readers with critical knowledge of the various influential

dynamics confronting the retail sector in Australia. Most importantly, the paper assists the

readers in gaining an insight that even though there is existence of big multinational

organisations, the industry could encounter a number of critical issues, which might have adverse

impact on the overall sector of the nation. Such impact could affect the business operations of the

sector as well.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING IN PROFESSION

Section 2: Introduction

2.1 Summary for the case and background information of the industry:

According to the case study, it has been found that the Australian retail sector confronts a

number of challenges that have taken place in the recent past like minimisation in sales revenue.

This has mandated the need for the business organisations to search for cost minimisation

methods in order to increase profits (Canning & O'Dwyer, 2016). In this regard, it needs to be

mentioned that as majority of the Australian retail stores deal with consumer goods, the business

managers and owners need to make decisions after careful analysis of the possible challenges.

The retail sector in Australia has a developed system, in which a large number of

organisations are conducting their business operations. Along with this, the customers possess

adequate knowledge regarding the retail products and the organisations operating in the sector.

However, due to the initiation of online retail stores and the fall in the purchasing power of the

customers due to unfavourable in the financial markets over the past few years have created

enormous challenges for the retailers operating in the nation.

2.2 Environment/context of the case:

Both local and global brands operate in the retail environment in the market of Australia.

Thus, diversification could be observed in the retail environment of the nation due to

accommodation of various sub-sector specialising in particular product categories. The

significant sub-sectors of the industry constitute of the following:

Electronic appliance retailers

Clothing retailers

Computer retailers

Hardware and construction materials retailers

Furniture retailers

Shoes and footwear retailers

Pharmaceutical product retailers

Stationery and book retailers

Games and toys retailers

Section 2: Introduction

2.1 Summary for the case and background information of the industry:

According to the case study, it has been found that the Australian retail sector confronts a

number of challenges that have taken place in the recent past like minimisation in sales revenue.

This has mandated the need for the business organisations to search for cost minimisation

methods in order to increase profits (Canning & O'Dwyer, 2016). In this regard, it needs to be

mentioned that as majority of the Australian retail stores deal with consumer goods, the business

managers and owners need to make decisions after careful analysis of the possible challenges.

The retail sector in Australia has a developed system, in which a large number of

organisations are conducting their business operations. Along with this, the customers possess

adequate knowledge regarding the retail products and the organisations operating in the sector.

However, due to the initiation of online retail stores and the fall in the purchasing power of the

customers due to unfavourable in the financial markets over the past few years have created

enormous challenges for the retailers operating in the nation.

2.2 Environment/context of the case:

Both local and global brands operate in the retail environment in the market of Australia.

Thus, diversification could be observed in the retail environment of the nation due to

accommodation of various sub-sector specialising in particular product categories. The

significant sub-sectors of the industry constitute of the following:

Electronic appliance retailers

Clothing retailers

Computer retailers

Hardware and construction materials retailers

Furniture retailers

Shoes and footwear retailers

Pharmaceutical product retailers

Stationery and book retailers

Games and toys retailers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING IN PROFESSION

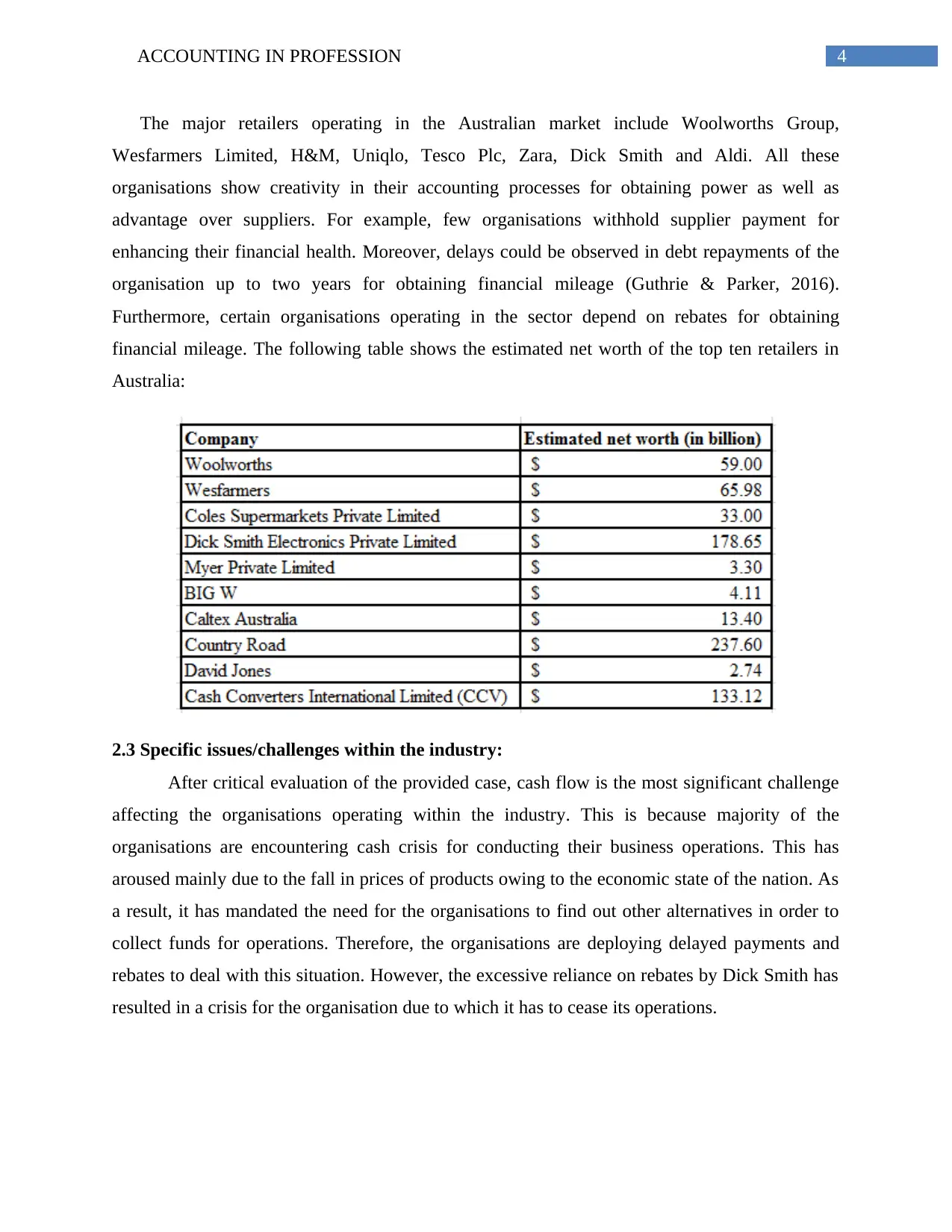

The major retailers operating in the Australian market include Woolworths Group,

Wesfarmers Limited, H&M, Uniqlo, Tesco Plc, Zara, Dick Smith and Aldi. All these

organisations show creativity in their accounting processes for obtaining power as well as

advantage over suppliers. For example, few organisations withhold supplier payment for

enhancing their financial health. Moreover, delays could be observed in debt repayments of the

organisation up to two years for obtaining financial mileage (Guthrie & Parker, 2016).

Furthermore, certain organisations operating in the sector depend on rebates for obtaining

financial mileage. The following table shows the estimated net worth of the top ten retailers in

Australia:

2.3 Specific issues/challenges within the industry:

After critical evaluation of the provided case, cash flow is the most significant challenge

affecting the organisations operating within the industry. This is because majority of the

organisations are encountering cash crisis for conducting their business operations. This has

aroused mainly due to the fall in prices of products owing to the economic state of the nation. As

a result, it has mandated the need for the organisations to find out other alternatives in order to

collect funds for operations. Therefore, the organisations are deploying delayed payments and

rebates to deal with this situation. However, the excessive reliance on rebates by Dick Smith has

resulted in a crisis for the organisation due to which it has to cease its operations.

The major retailers operating in the Australian market include Woolworths Group,

Wesfarmers Limited, H&M, Uniqlo, Tesco Plc, Zara, Dick Smith and Aldi. All these

organisations show creativity in their accounting processes for obtaining power as well as

advantage over suppliers. For example, few organisations withhold supplier payment for

enhancing their financial health. Moreover, delays could be observed in debt repayments of the

organisation up to two years for obtaining financial mileage (Guthrie & Parker, 2016).

Furthermore, certain organisations operating in the sector depend on rebates for obtaining

financial mileage. The following table shows the estimated net worth of the top ten retailers in

Australia:

2.3 Specific issues/challenges within the industry:

After critical evaluation of the provided case, cash flow is the most significant challenge

affecting the organisations operating within the industry. This is because majority of the

organisations are encountering cash crisis for conducting their business operations. This has

aroused mainly due to the fall in prices of products owing to the economic state of the nation. As

a result, it has mandated the need for the organisations to find out other alternatives in order to

collect funds for operations. Therefore, the organisations are deploying delayed payments and

rebates to deal with this situation. However, the excessive reliance on rebates by Dick Smith has

resulted in a crisis for the organisation due to which it has to cease its operations.

5ACCOUNTING IN PROFESSION

Section 3: Responses to the case questions

3.1 Good faith:

The concept of good faith, in this regard, is used for implying that it is necessary for the

two groups to work in harmony without making any sort of underhand dealings. It is noteworthy

to mention that the Australian retailers, particularly, supermarkets, are obtaining undue benefit

over the suppliers in order to raise their financial profits. Besides, the organisations need to take

into consideration the application of all ethical codes of conduct at the time of transactions so

that they do not lead to controversies. In other words, it is necessary for the organisations to

maintain fair competition and trading practices for providing adequate favour to the end

customers.

At the time the code lays stress on good faith, the issue related to trust is addressed

between the retailers and the suppliers. This is because it is crucial for both the parties to

maintain trust in each other so that it becomes easy for them to work in combination for

betterment of the Australian retail sector, which is confronted with numerous setbacks in the

current times.

3.2 Reason behind the thought of Food and Grocery of Conduct as a voluntary code:

The reason that the Food and Grocery Code of Conduct is termed as a voluntary code is

to enable the suppliers and retailers to reach an agreement on flexible business terms that would

assure benefits for both the parties (Cameron & O'Leary, 2015). It is to be noted that particular

retailers have suppliers associated with them for long time, which has helped in developing

understanding of the business dealings. The code of conduct is used as a medium for assuring

that both parties follow agreement terms thoroughly.

ACCC has not moved this code into law for enabling the retailers and suppliers to design

practices and policies favourable to both of them and the customers. This code only checks the

presence of honesty in the transactions. However, such agreements should be written formally to

make it easy for ACCC in enforcing contracts.

Section 3: Responses to the case questions

3.1 Good faith:

The concept of good faith, in this regard, is used for implying that it is necessary for the

two groups to work in harmony without making any sort of underhand dealings. It is noteworthy

to mention that the Australian retailers, particularly, supermarkets, are obtaining undue benefit

over the suppliers in order to raise their financial profits. Besides, the organisations need to take

into consideration the application of all ethical codes of conduct at the time of transactions so

that they do not lead to controversies. In other words, it is necessary for the organisations to

maintain fair competition and trading practices for providing adequate favour to the end

customers.

At the time the code lays stress on good faith, the issue related to trust is addressed

between the retailers and the suppliers. This is because it is crucial for both the parties to

maintain trust in each other so that it becomes easy for them to work in combination for

betterment of the Australian retail sector, which is confronted with numerous setbacks in the

current times.

3.2 Reason behind the thought of Food and Grocery of Conduct as a voluntary code:

The reason that the Food and Grocery Code of Conduct is termed as a voluntary code is

to enable the suppliers and retailers to reach an agreement on flexible business terms that would

assure benefits for both the parties (Cameron & O'Leary, 2015). It is to be noted that particular

retailers have suppliers associated with them for long time, which has helped in developing

understanding of the business dealings. The code of conduct is used as a medium for assuring

that both parties follow agreement terms thoroughly.

ACCC has not moved this code into law for enabling the retailers and suppliers to design

practices and policies favourable to both of them and the customers. This code only checks the

presence of honesty in the transactions. However, such agreements should be written formally to

make it easy for ACCC in enforcing contracts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING IN PROFESSION

3.3 Appropriateness of decision making power as a senior manager and/or group and

assessment of its legitimacy:

It is noteworthy to mention that relativeness needs to be present when power is applied at

the workplace. For example, at the time of managing any crisis affecting all the organisational

members, it would be better to avoid using power and approach needs to be made towards the

employees for coming up with one common solution (Jackson, 2015). However, power needs to

be applied during dispute resolution for the two conflict parties in order to regard the person in

the form of authority figure. Thus, evaluation of the managerial decisions would help in

identifying the legitimacy of power made by the individual in making decisions. As the business

managers undertake crucial decisions, it is necessary for them to assure the legitimacy of

decisions undertaken.

3.4 Techniques to respond to the provided situation and grounds to be used as bases:

It has been identified that the Australian retailers often delay in making payments to their

suppliers so that financial mileage could be gained. However, this move does not adhere to the

appropriate code of ethics, as it would not be fair to the suppliers (Mastracchio Jr, Jiménez-

Angueira & Toth, 2015). On the other hand, it could be ignored; in case, it assists the business

organisations in coming out of financial troubles. Under such situation, when the CEO

approaches an individual, a negative response is to be provided by the individual. This is because

delaying the supplier payments would lead to critical ethical issues, which would result in

additional cost burden for the organisation, instead of maximising cash expected from delayed

supplier payments. However, if the business sake is taken into consideration, acceptance could

be provided in terms of delay in supplier payments.

3.5 Ways of applying developed country standards of employment conditions to less

developed countries and information or frameworks for determining their

appropriateness:

A number of distinctions could be observed between a developed nation and a developing

nation. For instance, the developed nations have greater buying power, better economic

conditions and higher GDPs compared to the other nations (Mescall, Phillips & Schmidt, 2017).

This denotes that the labour standards and employment conditions are more effective in

developed nations compared to developing nations. This is due to the facilitation of

3.3 Appropriateness of decision making power as a senior manager and/or group and

assessment of its legitimacy:

It is noteworthy to mention that relativeness needs to be present when power is applied at

the workplace. For example, at the time of managing any crisis affecting all the organisational

members, it would be better to avoid using power and approach needs to be made towards the

employees for coming up with one common solution (Jackson, 2015). However, power needs to

be applied during dispute resolution for the two conflict parties in order to regard the person in

the form of authority figure. Thus, evaluation of the managerial decisions would help in

identifying the legitimacy of power made by the individual in making decisions. As the business

managers undertake crucial decisions, it is necessary for them to assure the legitimacy of

decisions undertaken.

3.4 Techniques to respond to the provided situation and grounds to be used as bases:

It has been identified that the Australian retailers often delay in making payments to their

suppliers so that financial mileage could be gained. However, this move does not adhere to the

appropriate code of ethics, as it would not be fair to the suppliers (Mastracchio Jr, Jiménez-

Angueira & Toth, 2015). On the other hand, it could be ignored; in case, it assists the business

organisations in coming out of financial troubles. Under such situation, when the CEO

approaches an individual, a negative response is to be provided by the individual. This is because

delaying the supplier payments would lead to critical ethical issues, which would result in

additional cost burden for the organisation, instead of maximising cash expected from delayed

supplier payments. However, if the business sake is taken into consideration, acceptance could

be provided in terms of delay in supplier payments.

3.5 Ways of applying developed country standards of employment conditions to less

developed countries and information or frameworks for determining their

appropriateness:

A number of distinctions could be observed between a developed nation and a developing

nation. For instance, the developed nations have greater buying power, better economic

conditions and higher GDPs compared to the other nations (Mescall, Phillips & Schmidt, 2017).

This denotes that the labour standards and employment conditions are more effective in

developed nations compared to developing nations. This is due to the facilitation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING IN PROFESSION

industrialisation as well as advanced economies in the nations. Therefore, the employment

standards need to be implemented in the developing nations. However, only partial application of

the standards could be applied. For example, the standards related to employee rights and basic

freedom could be adopted in the developing nations. Besides, the standards about relationships

between staffs and employers could be applied in the developing nations. However, cultural

differences would restrict the employment-related policies and legislations to be implemented in

the developing nations. The policies need to be country-specific.

3.6 Benefits to be enjoyed by the organisation by following cost (price) leadership model:

It is a common notion that when the customers intend to incur more prices for purchasing

the products of an organisation willingly, it is deemed to be favourable for the organisation, since

there would be increase in overall revenue. Moreover, the organisation would be able to enjoy

competitive advantage in the market. The customer demand confronting rise in supplier

payments in less developed nations are appropriate. As commented by Mintz (2016), the

suppliers in less developed nations live in substandard conditions because of verty and hardships.

Hence, increasing their payments is necessary for enhancing their living standards. Hence, the

CEO of the organisation needs to be convinced by providing a detailed evaluation.

As the customers incur more money as long as the suppliers are paid more in less

developed nations, a maximum level could be formed by the organisation for supplier payments

and the cost of garments manufactured. The cost of products needs to be increased in a way that

it caters for increased supplier payments and profit margin. For example, if the suppliers obtain

10% additional payments from the organisation, it is possible for the latter to increase the cost of

products by 13%. This move is considered to be favourable for both the organisation and the

suppliers, as the growth of both parties could be assured in the long-run. Hence, from the

economical and societal perspectives, this move seems to be feasible.

3.7 Techniques of conducting audit based on the provided situation:

Audit fraud is considered to be a big challenge in terms of effective audit practices. Even

though employees are blamed often to change the facts deliberately, more individuals need to be

engaged along with the employees (Voss, 2017). The staffs are needed to be coached in changing

the fact without the fear of job loss. In this regard, it is significant to assure that the facts are

provided confronting the audit procedure without any feeling of intimidation. At the time of

industrialisation as well as advanced economies in the nations. Therefore, the employment

standards need to be implemented in the developing nations. However, only partial application of

the standards could be applied. For example, the standards related to employee rights and basic

freedom could be adopted in the developing nations. Besides, the standards about relationships

between staffs and employers could be applied in the developing nations. However, cultural

differences would restrict the employment-related policies and legislations to be implemented in

the developing nations. The policies need to be country-specific.

3.6 Benefits to be enjoyed by the organisation by following cost (price) leadership model:

It is a common notion that when the customers intend to incur more prices for purchasing

the products of an organisation willingly, it is deemed to be favourable for the organisation, since

there would be increase in overall revenue. Moreover, the organisation would be able to enjoy

competitive advantage in the market. The customer demand confronting rise in supplier

payments in less developed nations are appropriate. As commented by Mintz (2016), the

suppliers in less developed nations live in substandard conditions because of verty and hardships.

Hence, increasing their payments is necessary for enhancing their living standards. Hence, the

CEO of the organisation needs to be convinced by providing a detailed evaluation.

As the customers incur more money as long as the suppliers are paid more in less

developed nations, a maximum level could be formed by the organisation for supplier payments

and the cost of garments manufactured. The cost of products needs to be increased in a way that

it caters for increased supplier payments and profit margin. For example, if the suppliers obtain

10% additional payments from the organisation, it is possible for the latter to increase the cost of

products by 13%. This move is considered to be favourable for both the organisation and the

suppliers, as the growth of both parties could be assured in the long-run. Hence, from the

economical and societal perspectives, this move seems to be feasible.

3.7 Techniques of conducting audit based on the provided situation:

Audit fraud is considered to be a big challenge in terms of effective audit practices. Even

though employees are blamed often to change the facts deliberately, more individuals need to be

engaged along with the employees (Voss, 2017). The staffs are needed to be coached in changing

the fact without the fear of job loss. In this regard, it is significant to assure that the facts are

provided confronting the audit procedure without any feeling of intimidation. At the time of

8ACCOUNTING IN PROFESSION

conducting the audit work, it is essential to reassure the staffs that the information would be kept

confidential for avoiding the fear of job loss. A friendly atmosphere needs to be developed to

assure that the employees would not be accused or victimised for the information provided.

Besides, the matter could be approached from a different perspective, in which fear could be

instilled in the staffs, if they do not provide accurate information. Audit fraud is considered as a

crime and any individual associated with such fraud could be convicted for wrong doing. This

could be used for overcoming the fear of job loss in the staffs; instead, fear could be instilled in

them to imprisonment, if they do not disclose the actual facts.

3.8 Integrated reporting, its achievements and use of this framework in changing

performance and remuneration system design:

Integrated reporting includes a precise report and description regarding the ways through

which the activities and operations of the organisation could result in value creation. The value

creation is discussed from the perspective of both short-term and long-term. With the help of

integrated reporting, an organisation could be benefitted from various aspects. For example, the

report could be utilised for undertaking key decisions regarding the future growth and operations

of the organisation. Thus, integrated reporting intends to provide meaning associated with the

performance-related data of an entity. Besides, with the help of this reporting, relationship could

be formed between the information disclosed in the reports of the entity and its overall

performance.

It is significant to use the framework of integrated reporting so that any change in

performance could be facilitated by detecting the accurate problem areas as well as points to the

precise aspects for ensuring better change. Moreover, the design of remuneration system could

be affected where the report would detect the deficiencies confronting salary payments along

with allowances at the organisation and addressing the same. In this regard, a positive change

would be initiated from the end of the framework for the business entity.

3.9 Concept of “at risk” remuneration component and reason behind its larger component

of remuneration as found by the Productivity Commission report:

This concept is a contract between an entity and its staffs for pegging portions of their

income on the organisational performance (West, 2018). It implies that at the time the entity is

performing effectively in financial matters, the staffs would have a part of the excess income

conducting the audit work, it is essential to reassure the staffs that the information would be kept

confidential for avoiding the fear of job loss. A friendly atmosphere needs to be developed to

assure that the employees would not be accused or victimised for the information provided.

Besides, the matter could be approached from a different perspective, in which fear could be

instilled in the staffs, if they do not provide accurate information. Audit fraud is considered as a

crime and any individual associated with such fraud could be convicted for wrong doing. This

could be used for overcoming the fear of job loss in the staffs; instead, fear could be instilled in

them to imprisonment, if they do not disclose the actual facts.

3.8 Integrated reporting, its achievements and use of this framework in changing

performance and remuneration system design:

Integrated reporting includes a precise report and description regarding the ways through

which the activities and operations of the organisation could result in value creation. The value

creation is discussed from the perspective of both short-term and long-term. With the help of

integrated reporting, an organisation could be benefitted from various aspects. For example, the

report could be utilised for undertaking key decisions regarding the future growth and operations

of the organisation. Thus, integrated reporting intends to provide meaning associated with the

performance-related data of an entity. Besides, with the help of this reporting, relationship could

be formed between the information disclosed in the reports of the entity and its overall

performance.

It is significant to use the framework of integrated reporting so that any change in

performance could be facilitated by detecting the accurate problem areas as well as points to the

precise aspects for ensuring better change. Moreover, the design of remuneration system could

be affected where the report would detect the deficiencies confronting salary payments along

with allowances at the organisation and addressing the same. In this regard, a positive change

would be initiated from the end of the framework for the business entity.

3.9 Concept of “at risk” remuneration component and reason behind its larger component

of remuneration as found by the Productivity Commission report:

This concept is a contract between an entity and its staffs for pegging portions of their

income on the organisational performance (West, 2018). It implies that at the time the entity is

performing effectively in financial matters, the staffs would have a part of the excess income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING IN PROFESSION

included in their salaries. However, in poor business conditions, the staffs feel the pinch, as the

identical rate would minimise their salaries. Based on the report of the Productivity Commission,

the arrangement of “at risk” is observed to be a significant issue for the large organisations.

Since the large organisations have numerous staffs, their remuneration and salaries might run in

millions based on their pay grades. On certain occasions, when the performance of an

organisation fails to meet the desired expectations, it might strain to increase the overall amount

of remuneration for all its staffs. Due to this, they might enter into agreement with their staffs for

having portion of their salaries placed at risk.

3.10 Stakeholders and ethical behaviour from organisational perspective:

As pointed out by Yarahmadi and Bohloli (2015), the stakeholders of a business

organisation comprise of all the individuals, which are associated with the organisation in a

variety of ways. For example, the management, investors, directors, employees, customers and

overall community that the organisation serves are considered to be its stakeholders. In a big

supermarket like that in Australia, the directors and investors are considered generally in the

form of the significant stakeholders because they are associated directly in creating the

organisation along with steering the same towards a specific direction. However, they require the

other individuals in increasing the efficiency and functionality of the business. For example, the

staffs communicate with the customers for generating adequate business opportunities for their

organisations. Besides, the ethical conduct issues in the organisations need all the associated

members of the organisation in stake holding matters. For example, in terms of corporate social

responsibility matters, the organisation requires the engagement of the community in order to

accomplish the same.

included in their salaries. However, in poor business conditions, the staffs feel the pinch, as the

identical rate would minimise their salaries. Based on the report of the Productivity Commission,

the arrangement of “at risk” is observed to be a significant issue for the large organisations.

Since the large organisations have numerous staffs, their remuneration and salaries might run in

millions based on their pay grades. On certain occasions, when the performance of an

organisation fails to meet the desired expectations, it might strain to increase the overall amount

of remuneration for all its staffs. Due to this, they might enter into agreement with their staffs for

having portion of their salaries placed at risk.

3.10 Stakeholders and ethical behaviour from organisational perspective:

As pointed out by Yarahmadi and Bohloli (2015), the stakeholders of a business

organisation comprise of all the individuals, which are associated with the organisation in a

variety of ways. For example, the management, investors, directors, employees, customers and

overall community that the organisation serves are considered to be its stakeholders. In a big

supermarket like that in Australia, the directors and investors are considered generally in the

form of the significant stakeholders because they are associated directly in creating the

organisation along with steering the same towards a specific direction. However, they require the

other individuals in increasing the efficiency and functionality of the business. For example, the

staffs communicate with the customers for generating adequate business opportunities for their

organisations. Besides, the ethical conduct issues in the organisations need all the associated

members of the organisation in stake holding matters. For example, in terms of corporate social

responsibility matters, the organisation requires the engagement of the community in order to

accomplish the same.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING IN PROFESSION

Section 4: Conclusion

The Australian retail sector is confronted with a variety of challenges, which mainly

constitute of income and cash flows. There are few organisations, which are shifting to the other

methods, so that their operating income could be increased. Such increase would assist them to

cope up with the increasing competition in the sector. These challenges are deemed to have

positive as well as negative effects on the consumers, retailers and the overall Australian

economy. Due to these challenges, the retailers have been compelled to shut down few

operations for meeting their production costs. This is identified as a negative impact, as the

organisations shrink rather than accomplishing growth.

Besides, the organisations are encountered with the risk of bankruptcy and eventually,

closures could occur, if the current situation does not change with the passage of time. The

income sources, which the organisations are moving, seem to be effective in the short-run. This

is because they would provide only temporary solutions, since the organisations need to wait for

the economy to recover at a faster rate. As a result, they need to minimise their production levels,

which would have influence on the customers directly. The product options for the customers

would decrease when they visit the retail stores for buying products. Due to this, the impact

would be negative on the economy of Australia, since it would fail to experience growth.

One positive effect of the situation in the retail sector of the nation is the fairness in

competition due to the fact that the organisations feel numerous challenges throughout the

overall industry. The organisations would not seek undue advantage over competition. Along

with this, they would make relevant and timely disclosures of the necessary information to the

stakeholders for maintaining favourable brand image in the market. Furthermore, the use of

integrated reporting framework has helped the organisations in identifying the deficiencies in the

business areas and accordingly, they could undertake necessary actions for minimising such

deficiencies. Finally, they would involve the community to ensure that appropriate corporate

social responsibility practices are in place in relation to sustainable development.

Section 4: Conclusion

The Australian retail sector is confronted with a variety of challenges, which mainly

constitute of income and cash flows. There are few organisations, which are shifting to the other

methods, so that their operating income could be increased. Such increase would assist them to

cope up with the increasing competition in the sector. These challenges are deemed to have

positive as well as negative effects on the consumers, retailers and the overall Australian

economy. Due to these challenges, the retailers have been compelled to shut down few

operations for meeting their production costs. This is identified as a negative impact, as the

organisations shrink rather than accomplishing growth.

Besides, the organisations are encountered with the risk of bankruptcy and eventually,

closures could occur, if the current situation does not change with the passage of time. The

income sources, which the organisations are moving, seem to be effective in the short-run. This

is because they would provide only temporary solutions, since the organisations need to wait for

the economy to recover at a faster rate. As a result, they need to minimise their production levels,

which would have influence on the customers directly. The product options for the customers

would decrease when they visit the retail stores for buying products. Due to this, the impact

would be negative on the economy of Australia, since it would fail to experience growth.

One positive effect of the situation in the retail sector of the nation is the fairness in

competition due to the fact that the organisations feel numerous challenges throughout the

overall industry. The organisations would not seek undue advantage over competition. Along

with this, they would make relevant and timely disclosures of the necessary information to the

stakeholders for maintaining favourable brand image in the market. Furthermore, the use of

integrated reporting framework has helped the organisations in identifying the deficiencies in the

business areas and accordingly, they could undertake necessary actions for minimising such

deficiencies. Finally, they would involve the community to ensure that appropriate corporate

social responsibility practices are in place in relation to sustainable development.

11ACCOUNTING IN PROFESSION

References:

Cameron, R. A., & O'Leary, C. (2015). Improving ethical attitudes or simply teaching ethical

codes? The reality of accounting ethics education. Accounting Education, 24(4), 275-290.

Canning, M., & O'Dwyer, B. (2016). Institutional work and regulatory change in the accounting

profession. Accounting, Organizations and Society, 54, 1-21.

Guthrie, J., & Parker, L. D. (2016). Whither the accounting profession, accountants and

accounting researchers? Commentary and projections. Accounting, Auditing &

Accountability Journal, 29(1), 2-10.

Jackson, C. W. (2015). Detecting Accounting Fraud: Analysis and Ethics. Pearson Higher Ed.

Mastracchio Jr, N. J., Jiménez-Angueira, C., & Toth, I. (2015). The state of ethics in business

and the accounting profession. The CPA Journal, 85(3), 48.

Mescall, D., Phillips, F., & Schmidt, R. N. (2017). Does the Accounting Profession Discipline Its

Members Differently After Public Scrutiny?. Journal of business ethics, 142(2), 285-309.

Mintz, S. (2016). Accounting for the public interest. Springer,.

Voss, G. (2017). Certificate of Ethics in Accounting and Professional Independence of

Accountants. European Journal of Economics and Business Studies, 9(1), 212-220.

West, A. (2018). After virtue and accounting ethics. Journal of Business Ethics, 148(1), 21-36.

Yarahmadi, H., & Bohloli, A. (2015). Ethics in Accounting. International Journal of Accounting

and Financial Reporting, 5(1), 356-360.

References:

Cameron, R. A., & O'Leary, C. (2015). Improving ethical attitudes or simply teaching ethical

codes? The reality of accounting ethics education. Accounting Education, 24(4), 275-290.

Canning, M., & O'Dwyer, B. (2016). Institutional work and regulatory change in the accounting

profession. Accounting, Organizations and Society, 54, 1-21.

Guthrie, J., & Parker, L. D. (2016). Whither the accounting profession, accountants and

accounting researchers? Commentary and projections. Accounting, Auditing &

Accountability Journal, 29(1), 2-10.

Jackson, C. W. (2015). Detecting Accounting Fraud: Analysis and Ethics. Pearson Higher Ed.

Mastracchio Jr, N. J., Jiménez-Angueira, C., & Toth, I. (2015). The state of ethics in business

and the accounting profession. The CPA Journal, 85(3), 48.

Mescall, D., Phillips, F., & Schmidt, R. N. (2017). Does the Accounting Profession Discipline Its

Members Differently After Public Scrutiny?. Journal of business ethics, 142(2), 285-309.

Mintz, S. (2016). Accounting for the public interest. Springer,.

Voss, G. (2017). Certificate of Ethics in Accounting and Professional Independence of

Accountants. European Journal of Economics and Business Studies, 9(1), 212-220.

West, A. (2018). After virtue and accounting ethics. Journal of Business Ethics, 148(1), 21-36.

Yarahmadi, H., & Bohloli, A. (2015). Ethics in Accounting. International Journal of Accounting

and Financial Reporting, 5(1), 356-360.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.