ACCG923 - Analysis of AASB 136 Impairment of Assets for Ansell Limited

VerifiedAdded on 2023/06/12

|9

|2119

|56

Report

AI Summary

This report provides a detailed analysis of AASB 136, focusing on the impairment of assets and its application to Ansell Limited, a company listed on the ASX. It examines the objectives of AASB 136, including the procedures for ensuring assets are recorded at their recoverable amount, and discusses the impairment and amortization of intangible assets. The report identifies indicators of impairment, relevant disclosures in financial reports, and major complexities involved in impairment assessments. It also covers the disclosure requirements for impairment as per AASB 136, the main objectives of General Purpose Financial Reporting (GPFR), and offers recommendations for improved financial reporting. The analysis includes specific examples from Ansell Limited's 2017 annual report, highlighting how the company addresses impairment of trade receivables and intangible assets, and meets the disclosure requirements of AASB 136.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

ACCOUNTING STATEMENT ANALYSIS

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

ACCOUNTING STATEMENT ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impairment of Assets

Executive summary

When it comes to the financial report of a listed entity there are various regulations that need

to be followed. To ensure that the valuation of the assets are in conformity with the procedure

and is properly disclosed in the annual report, the relevant treatment needs to be properly

scrutinized. To ensure this, Ansell Limited that is listed on the ASX and is a constituent of

ASX 300 is selected. Further, AASB 136 that is impairment of assets is studied in the light of

Ansell Limited.

2

Executive summary

When it comes to the financial report of a listed entity there are various regulations that need

to be followed. To ensure that the valuation of the assets are in conformity with the procedure

and is properly disclosed in the annual report, the relevant treatment needs to be properly

scrutinized. To ensure this, Ansell Limited that is listed on the ASX and is a constituent of

ASX 300 is selected. Further, AASB 136 that is impairment of assets is studied in the light of

Ansell Limited.

2

Impairment of Assets

Contents

Objectives of AASB 136- Impairment of Assets.....................................................................................4

Impairment and Amortisation of Intangible Assets.......................................................................5

Indicators of impairment...............................................................................................................5

Relevant disclosures in the financial report...................................................................................6

Major complexities and key issues involved in the impairment............................................................6

Disclosure requirement for Impairment as per AASB 136.....................................................................7

Main objectives of the General Purpose Financial Reporting (GPFR)....................................................8

Recommendation..................................................................................................................................8

References.............................................................................................................................................9

3

Contents

Objectives of AASB 136- Impairment of Assets.....................................................................................4

Impairment and Amortisation of Intangible Assets.......................................................................5

Indicators of impairment...............................................................................................................5

Relevant disclosures in the financial report...................................................................................6

Major complexities and key issues involved in the impairment............................................................6

Disclosure requirement for Impairment as per AASB 136.....................................................................7

Main objectives of the General Purpose Financial Reporting (GPFR)....................................................8

Recommendation..................................................................................................................................8

References.............................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impairment of Assets

Objectives of AASB 136- Impairment of Assets

This standard was made by Australian Accounting Standard Board under section 334 of

Corporation Act 2001 on 15th July 2004. The objective of this standard is to deal with the

procedures used by an organization to ensure that assets are recorded at their recoverable

amount only. This standard prescribes that in case the carrying amount is more than the

recoverable amount, then in such a case, the difference between the carrying amount and the

recoverable or saleable amount is termed as an impairment loss. In case the carrying amount

is lesser than the recoverable amount then in such case the impairment losses shall be

reversed (Ansell, 2017). The company shall disclose entire impairment information in its

annual reports.

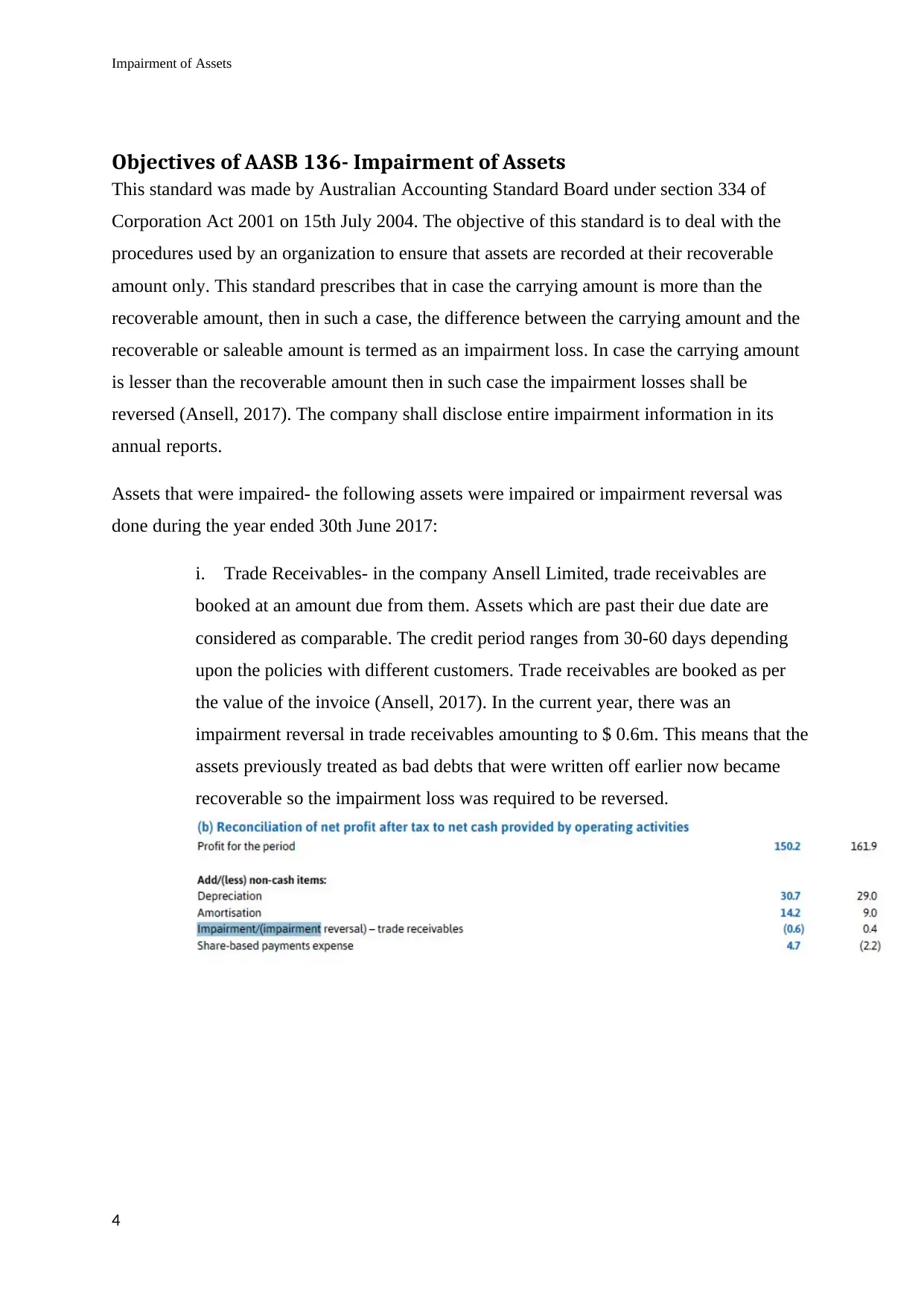

Assets that were impaired- the following assets were impaired or impairment reversal was

done during the year ended 30th June 2017:

i. Trade Receivables- in the company Ansell Limited, trade receivables are

booked at an amount due from them. Assets which are past their due date are

considered as comparable. The credit period ranges from 30-60 days depending

upon the policies with different customers. Trade receivables are booked as per

the value of the invoice (Ansell, 2017). In the current year, there was an

impairment reversal in trade receivables amounting to $ 0.6m. This means that the

assets previously treated as bad debts that were written off earlier now became

recoverable so the impairment loss was required to be reversed.

4

Objectives of AASB 136- Impairment of Assets

This standard was made by Australian Accounting Standard Board under section 334 of

Corporation Act 2001 on 15th July 2004. The objective of this standard is to deal with the

procedures used by an organization to ensure that assets are recorded at their recoverable

amount only. This standard prescribes that in case the carrying amount is more than the

recoverable amount, then in such a case, the difference between the carrying amount and the

recoverable or saleable amount is termed as an impairment loss. In case the carrying amount

is lesser than the recoverable amount then in such case the impairment losses shall be

reversed (Ansell, 2017). The company shall disclose entire impairment information in its

annual reports.

Assets that were impaired- the following assets were impaired or impairment reversal was

done during the year ended 30th June 2017:

i. Trade Receivables- in the company Ansell Limited, trade receivables are

booked at an amount due from them. Assets which are past their due date are

considered as comparable. The credit period ranges from 30-60 days depending

upon the policies with different customers. Trade receivables are booked as per

the value of the invoice (Ansell, 2017). In the current year, there was an

impairment reversal in trade receivables amounting to $ 0.6m. This means that the

assets previously treated as bad debts that were written off earlier now became

recoverable so the impairment loss was required to be reversed.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impairment of Assets

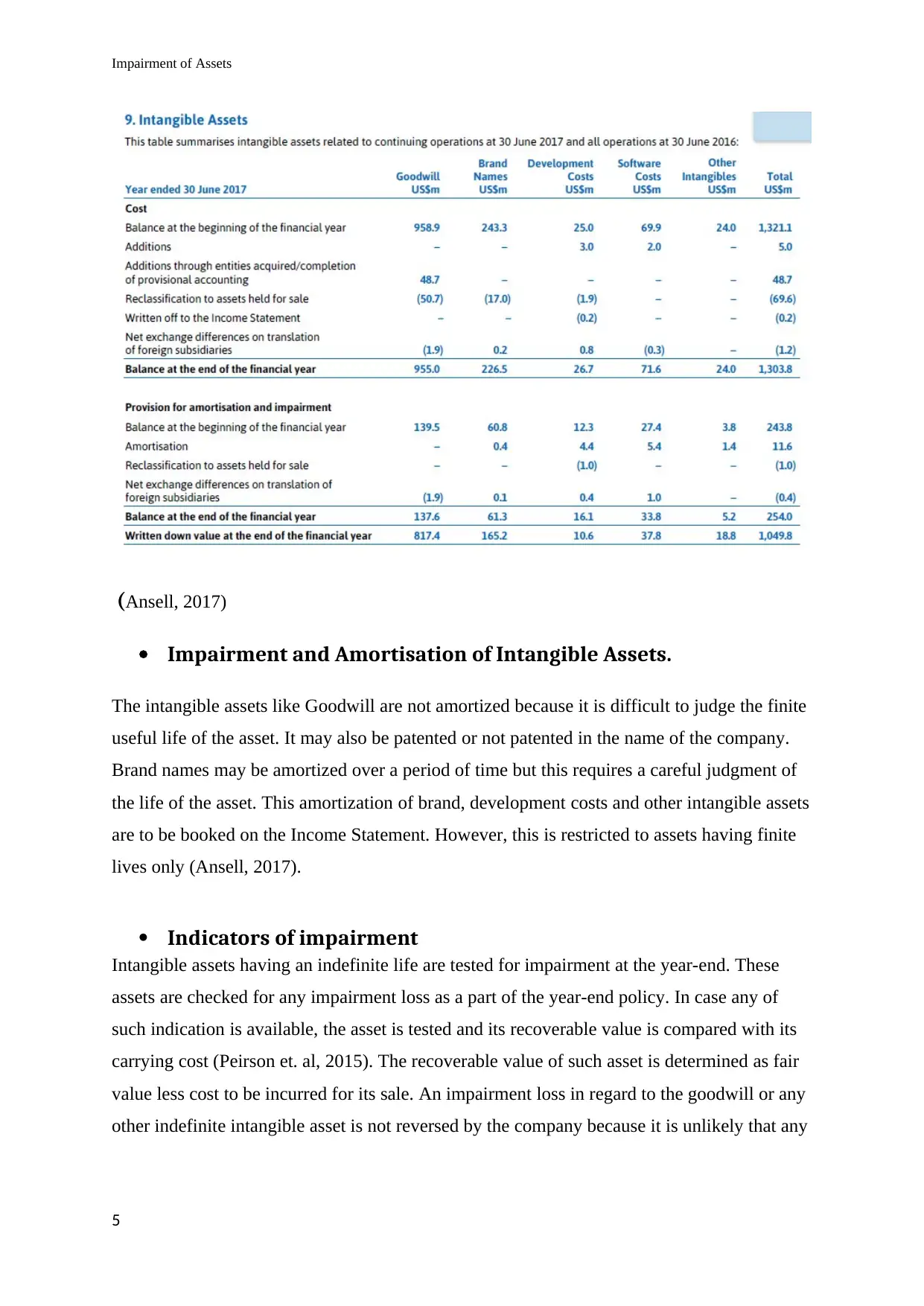

(Ansell, 2017)

Impairment and Amortisation of Intangible Assets.

The intangible assets like Goodwill are not amortized because it is difficult to judge the finite

useful life of the asset. It may also be patented or not patented in the name of the company.

Brand names may be amortized over a period of time but this requires a careful judgment of

the life of the asset. This amortization of brand, development costs and other intangible assets

are to be booked on the Income Statement. However, this is restricted to assets having finite

lives only (Ansell, 2017).

Indicators of impairment

Intangible assets having an indefinite life are tested for impairment at the year-end. These

assets are checked for any impairment loss as a part of the year-end policy. In case any of

such indication is available, the asset is tested and its recoverable value is compared with its

carrying cost (Peirson et. al, 2015). The recoverable value of such asset is determined as fair

value less cost to be incurred for its sale. An impairment loss in regard to the goodwill or any

other indefinite intangible asset is not reversed by the company because it is unlikely that any

5

(Ansell, 2017)

Impairment and Amortisation of Intangible Assets.

The intangible assets like Goodwill are not amortized because it is difficult to judge the finite

useful life of the asset. It may also be patented or not patented in the name of the company.

Brand names may be amortized over a period of time but this requires a careful judgment of

the life of the asset. This amortization of brand, development costs and other intangible assets

are to be booked on the Income Statement. However, this is restricted to assets having finite

lives only (Ansell, 2017).

Indicators of impairment

Intangible assets having an indefinite life are tested for impairment at the year-end. These

assets are checked for any impairment loss as a part of the year-end policy. In case any of

such indication is available, the asset is tested and its recoverable value is compared with its

carrying cost (Peirson et. al, 2015). The recoverable value of such asset is determined as fair

value less cost to be incurred for its sale. An impairment loss in regard to the goodwill or any

other indefinite intangible asset is not reversed by the company because it is unlikely that any

5

Impairment of Assets

increase in the recoverable value can be linked with any event occurring after the impairment

loss has been booked (Ansell, 2017).

Relevant disclosures in the financial report

The company Ansell limited has done the relevant disclosures wherever the impairment of

assets has taken place. Also, the auditors have disclosed their concerns with regard to any

future impairment of intangible assets in the key audit matters (Ansell, 2017).

Major complexities and key issues involved in the impairment

As impairment or amortization is a major hit on the financial position of the company, it has

to be adequately backed up by facts and figures or any material event which takes place at the

year-end. Any impairment loss can also be recognized before the year-end provided it is

backed up by the material event and approved by the management. However, it is more

appropriate that impairment is tested for the assets at the year-end but in the view of

continuity, it should be tested at the same time every year. At the time of impairment, the

cash flows, the growth rate, discount rate and the financial statements should be prepared and

approved by the management (Kieso et. al, 2010). So this involves a careful assessment of the

financial statements and the significant events surrounding the company.

The judgment as to impairment of any asset requires the judgment of finite life of an asset

and its utility to the company. It becomes all the more complex when the life of an intangible

asset has to be judged (Shoaf & Zaldivar, 2005). Also, a cost incurred for attaining or

building an intangible asset is difficult to determine because sometimes the intangible assets

are self-constructed and there is hardly any cost attached to the acquisition of intangible

assets other than patenting costs.

The company has to extensively disclose all the material events, rates applicable, assumptions

made regarding the impairment of the assets. Impairment can be positive or negative

depending upon the carrying value and the recoverable value of the asset. But in both the

cases, the management has to disclose the information with underlying assumptions and

documents with the company shareholders (McKaig, 2011). So the impairment event is a

complex issue which has to be critically analyzed in the light of various events as it is an

event which affects the going concern of the company.

6

increase in the recoverable value can be linked with any event occurring after the impairment

loss has been booked (Ansell, 2017).

Relevant disclosures in the financial report

The company Ansell limited has done the relevant disclosures wherever the impairment of

assets has taken place. Also, the auditors have disclosed their concerns with regard to any

future impairment of intangible assets in the key audit matters (Ansell, 2017).

Major complexities and key issues involved in the impairment

As impairment or amortization is a major hit on the financial position of the company, it has

to be adequately backed up by facts and figures or any material event which takes place at the

year-end. Any impairment loss can also be recognized before the year-end provided it is

backed up by the material event and approved by the management. However, it is more

appropriate that impairment is tested for the assets at the year-end but in the view of

continuity, it should be tested at the same time every year. At the time of impairment, the

cash flows, the growth rate, discount rate and the financial statements should be prepared and

approved by the management (Kieso et. al, 2010). So this involves a careful assessment of the

financial statements and the significant events surrounding the company.

The judgment as to impairment of any asset requires the judgment of finite life of an asset

and its utility to the company. It becomes all the more complex when the life of an intangible

asset has to be judged (Shoaf & Zaldivar, 2005). Also, a cost incurred for attaining or

building an intangible asset is difficult to determine because sometimes the intangible assets

are self-constructed and there is hardly any cost attached to the acquisition of intangible

assets other than patenting costs.

The company has to extensively disclose all the material events, rates applicable, assumptions

made regarding the impairment of the assets. Impairment can be positive or negative

depending upon the carrying value and the recoverable value of the asset. But in both the

cases, the management has to disclose the information with underlying assumptions and

documents with the company shareholders (McKaig, 2011). So the impairment event is a

complex issue which has to be critically analyzed in the light of various events as it is an

event which affects the going concern of the company.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Impairment of Assets

Disclosure requirement for Impairment as per AASB 136

As per the provisions of AASB 136 the company needs to extensively disclose all the matters

related to the impairment of assets. The company Ansell Ltd. has in the following ways

disclosed the impairment information in relevance with the AASB 136:

i. Recognising of impairment losses and reversal of impairment losses in books of

accounts- the company has an impairment reversal in trade receivables which it has

disclosed in its annexure to Income Statement. Also, the provision for allowances has been

disclosed by the company in its financial statements.

ii. Amount of impairment losses and reversal of impairment losses on the revalued assets

have been duly disclosed by the company in its annual reporting.

iii. As per the disclosure requirements of AASB 136, the disclosure of impairment must

be different for different classes of assets. The company has given different disclosures for

non-current assets impaired during the year and for the intangible assets impaired or

amortised during the year (Hamilton et. al, 2011).

iv. As per the disclosure requirements of AASB 136, the assets should be defined with

regard to its finite and infinite lives. The company Ansell Limited has in its annual report

and financial reports notes to account disclosed the recognition and measurement of its

tangible and intangible assets (Hamilton et. al, 2011).

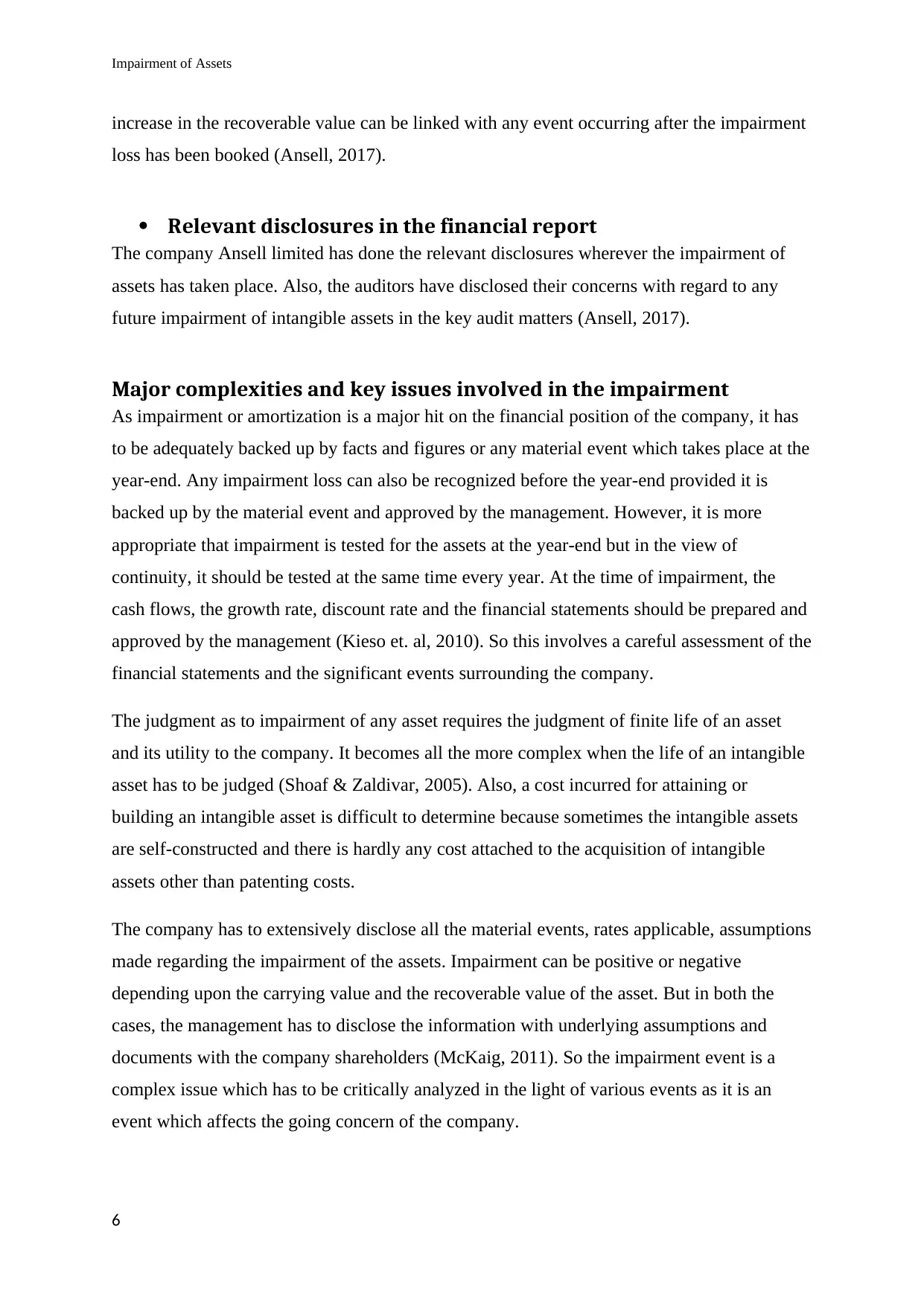

v. The other disclosure requirements are the discount rate, growth rate, etc which have

been duly defined in the annual report of the company which is clear from the following

image

Hence, it can be said that the company Ansell Limited has incorporated its disclosure

requirements for the year ending reports. The company is very particular in fulfilling its

disclosure requirements

7

Disclosure requirement for Impairment as per AASB 136

As per the provisions of AASB 136 the company needs to extensively disclose all the matters

related to the impairment of assets. The company Ansell Ltd. has in the following ways

disclosed the impairment information in relevance with the AASB 136:

i. Recognising of impairment losses and reversal of impairment losses in books of

accounts- the company has an impairment reversal in trade receivables which it has

disclosed in its annexure to Income Statement. Also, the provision for allowances has been

disclosed by the company in its financial statements.

ii. Amount of impairment losses and reversal of impairment losses on the revalued assets

have been duly disclosed by the company in its annual reporting.

iii. As per the disclosure requirements of AASB 136, the disclosure of impairment must

be different for different classes of assets. The company has given different disclosures for

non-current assets impaired during the year and for the intangible assets impaired or

amortised during the year (Hamilton et. al, 2011).

iv. As per the disclosure requirements of AASB 136, the assets should be defined with

regard to its finite and infinite lives. The company Ansell Limited has in its annual report

and financial reports notes to account disclosed the recognition and measurement of its

tangible and intangible assets (Hamilton et. al, 2011).

v. The other disclosure requirements are the discount rate, growth rate, etc which have

been duly defined in the annual report of the company which is clear from the following

image

Hence, it can be said that the company Ansell Limited has incorporated its disclosure

requirements for the year ending reports. The company is very particular in fulfilling its

disclosure requirements

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impairment of Assets

Main objectives of the General Purpose Financial Reporting (GPFR)

It focuses on providing the relevant information to the users of financial statements as the

users cannot amend or organize the information given in the financial statements according to

their needs. Such users include banks, taxation authorities, shareholders, etc. The GPFR also

help the management in defining their responsibility and accountability with regard to the

presentation of financial statements to its users (Deegan, 2011). The GPFR should disclose

the relevant information regarding profitability of the company, its correct financial position,

financing and investing activities during the year, the compliances required and compliances

done during the year, etc.

The disclosures did by the company Ansell Ltd. in the year 2017 with regard to the

impairment of assets in the annual reports are compatible with the objectives of the General

Purpose Financial Reporting. This can be seen from the fact that the company has disclosed

all the impairment losses and reversal of impairment losses during the year in its annual

report. Not only this, but the company has also clearly explained and disclosed the method of

calculation and recognition of such impairment losses in the financial statements (Kieso et.

al, 2010). The company has defined the treatment of all kinds of assets, the meanings of

impairment losses for each class of assets of the company, the discount rates, the growth rates

used by the company for the purpose and all the self-explanatory information relevant to the

impairment.

Recommendation

The above information and disclosures are very helpful for the users of financial statements

such as investors, financial institutions, shareholders, taxation authorities etc. as the

company’s correct financial position gets disclosed in the annual report. The same is also

required for the valuation of assets of the company. Valuation of assets is required for various

purposes and reporting of the company. In case the rating of the company is to be measured

then also the valuation of the assets is required. Hence, the company is efficient in meeting

out its requirement of disclosure of relevant information.

8

Main objectives of the General Purpose Financial Reporting (GPFR)

It focuses on providing the relevant information to the users of financial statements as the

users cannot amend or organize the information given in the financial statements according to

their needs. Such users include banks, taxation authorities, shareholders, etc. The GPFR also

help the management in defining their responsibility and accountability with regard to the

presentation of financial statements to its users (Deegan, 2011). The GPFR should disclose

the relevant information regarding profitability of the company, its correct financial position,

financing and investing activities during the year, the compliances required and compliances

done during the year, etc.

The disclosures did by the company Ansell Ltd. in the year 2017 with regard to the

impairment of assets in the annual reports are compatible with the objectives of the General

Purpose Financial Reporting. This can be seen from the fact that the company has disclosed

all the impairment losses and reversal of impairment losses during the year in its annual

report. Not only this, but the company has also clearly explained and disclosed the method of

calculation and recognition of such impairment losses in the financial statements (Kieso et.

al, 2010). The company has defined the treatment of all kinds of assets, the meanings of

impairment losses for each class of assets of the company, the discount rates, the growth rates

used by the company for the purpose and all the self-explanatory information relevant to the

impairment.

Recommendation

The above information and disclosures are very helpful for the users of financial statements

such as investors, financial institutions, shareholders, taxation authorities etc. as the

company’s correct financial position gets disclosed in the annual report. The same is also

required for the valuation of assets of the company. Valuation of assets is required for various

purposes and reporting of the company. In case the rating of the company is to be measured

then also the valuation of the assets is required. Hence, the company is efficient in meeting

out its requirement of disclosure of relevant information.

8

Impairment of Assets

References

Ansell Limited. (2017) Ansell Limited annual report and accounts 2017 [online]. Avilabnle

from http://www.ansell.com/en/About/Media-Center/Press-Releases/Ansell-Limited-

Announces-2017-Full-Year-Results.aspx [Accessed 29 April 2018]

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Hamilton, K., Hyland, B. and Dodd, J. L. (2011) Impairment: IASB-FASB Comparison.

Drake Management Review. [online]. 1(1), p. 55–67. Available from:

https://pdfs.semanticscholar.org/8d8f/5fd070193d6fa52e79d1dee9cc6632159d8a.pdf

[Accessed 29 April 2018]

Kieso, D., Weygandt, J., Warfield, T., Young, N and Wiecek, I . (2010) Intermediate

accounting, Toronto: John Wiley & Sons Canada.

Kieso, D., Weygandt, J., Warfield, T; Young, N. and Wiecek, I . (2010) Intermediate

accounting. Toronto: John Wiley & Sons Canada.

McKaig, T 2011, Understanding Impairment Accounting: What It Is and When It Is Used.

Available from: http://www.financepractitioner.com/accountancy-checklists/understanding-

impairment-accounting-what-it-is-and-when-it-is-used [Accessed 29 April 2018]

Parrino, R, Kidwell, D. and Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

NJ: Wiley

Peirson, G, Brown, R., Easton, S, Howard, P. and Pinder, S. (2015) Business Finance, 12th

ed. North Ryde: McGraw-Hill Australia.

Shoaf, V. and Zaldivar, I.P. (2005) Goodwill impairment: convergence not yet achieved.

Available from: http://www.freepatentsonline.com/article/Review-Business/133756140.html

[Accessed 29 April 2018]

9

References

Ansell Limited. (2017) Ansell Limited annual report and accounts 2017 [online]. Avilabnle

from http://www.ansell.com/en/About/Media-Center/Press-Releases/Ansell-Limited-

Announces-2017-Full-Year-Results.aspx [Accessed 29 April 2018]

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Hamilton, K., Hyland, B. and Dodd, J. L. (2011) Impairment: IASB-FASB Comparison.

Drake Management Review. [online]. 1(1), p. 55–67. Available from:

https://pdfs.semanticscholar.org/8d8f/5fd070193d6fa52e79d1dee9cc6632159d8a.pdf

[Accessed 29 April 2018]

Kieso, D., Weygandt, J., Warfield, T., Young, N and Wiecek, I . (2010) Intermediate

accounting, Toronto: John Wiley & Sons Canada.

Kieso, D., Weygandt, J., Warfield, T; Young, N. and Wiecek, I . (2010) Intermediate

accounting. Toronto: John Wiley & Sons Canada.

McKaig, T 2011, Understanding Impairment Accounting: What It Is and When It Is Used.

Available from: http://www.financepractitioner.com/accountancy-checklists/understanding-

impairment-accounting-what-it-is-and-when-it-is-used [Accessed 29 April 2018]

Parrino, R, Kidwell, D. and Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

NJ: Wiley

Peirson, G, Brown, R., Easton, S, Howard, P. and Pinder, S. (2015) Business Finance, 12th

ed. North Ryde: McGraw-Hill Australia.

Shoaf, V. and Zaldivar, I.P. (2005) Goodwill impairment: convergence not yet achieved.

Available from: http://www.freepatentsonline.com/article/Review-Business/133756140.html

[Accessed 29 April 2018]

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.