ACCM4300 - Analyzing Fair Value and Equity Accounts in Business

VerifiedAdded on 2023/03/31

|12

|646

|192

Case Study

AI Summary

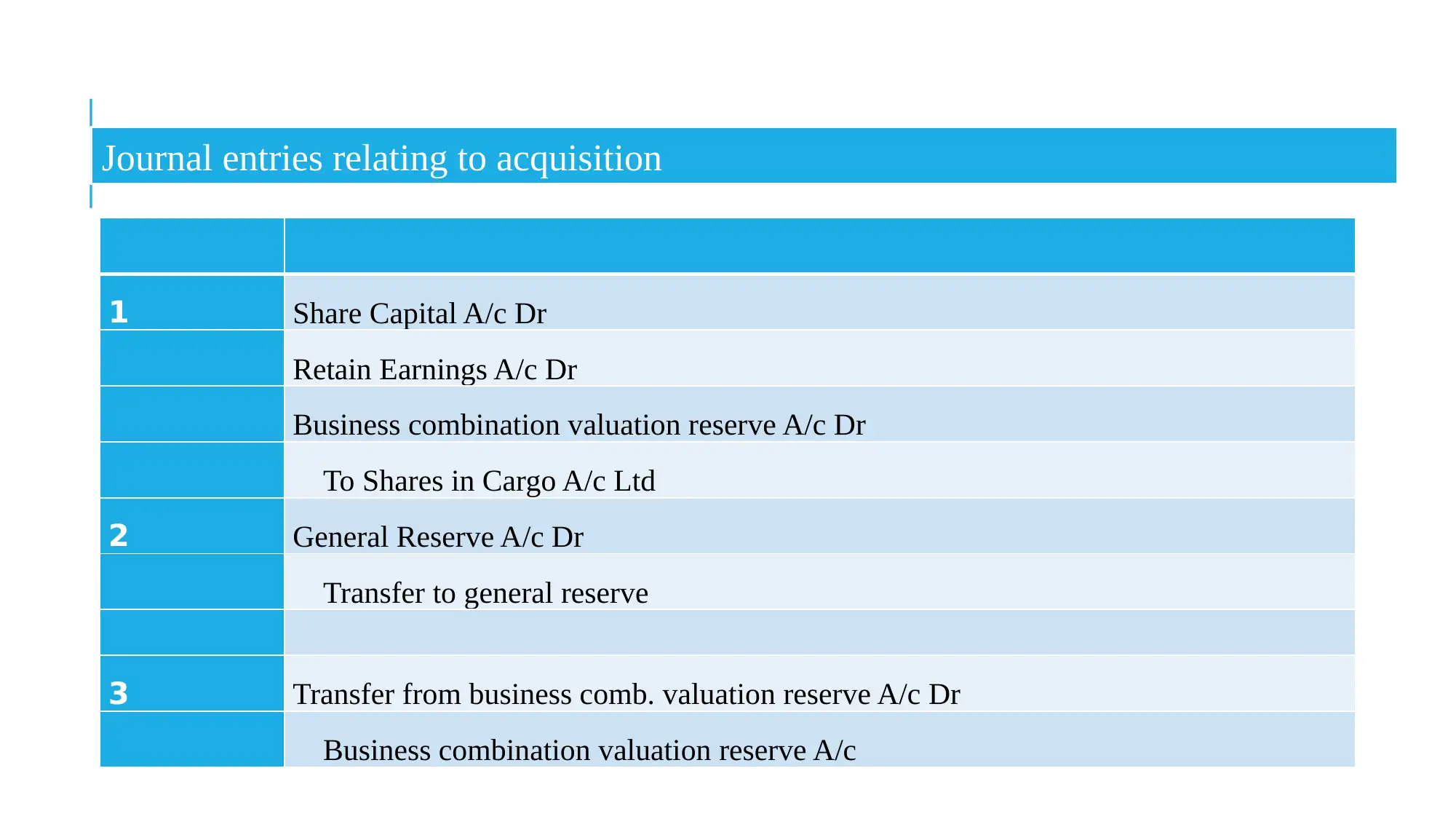

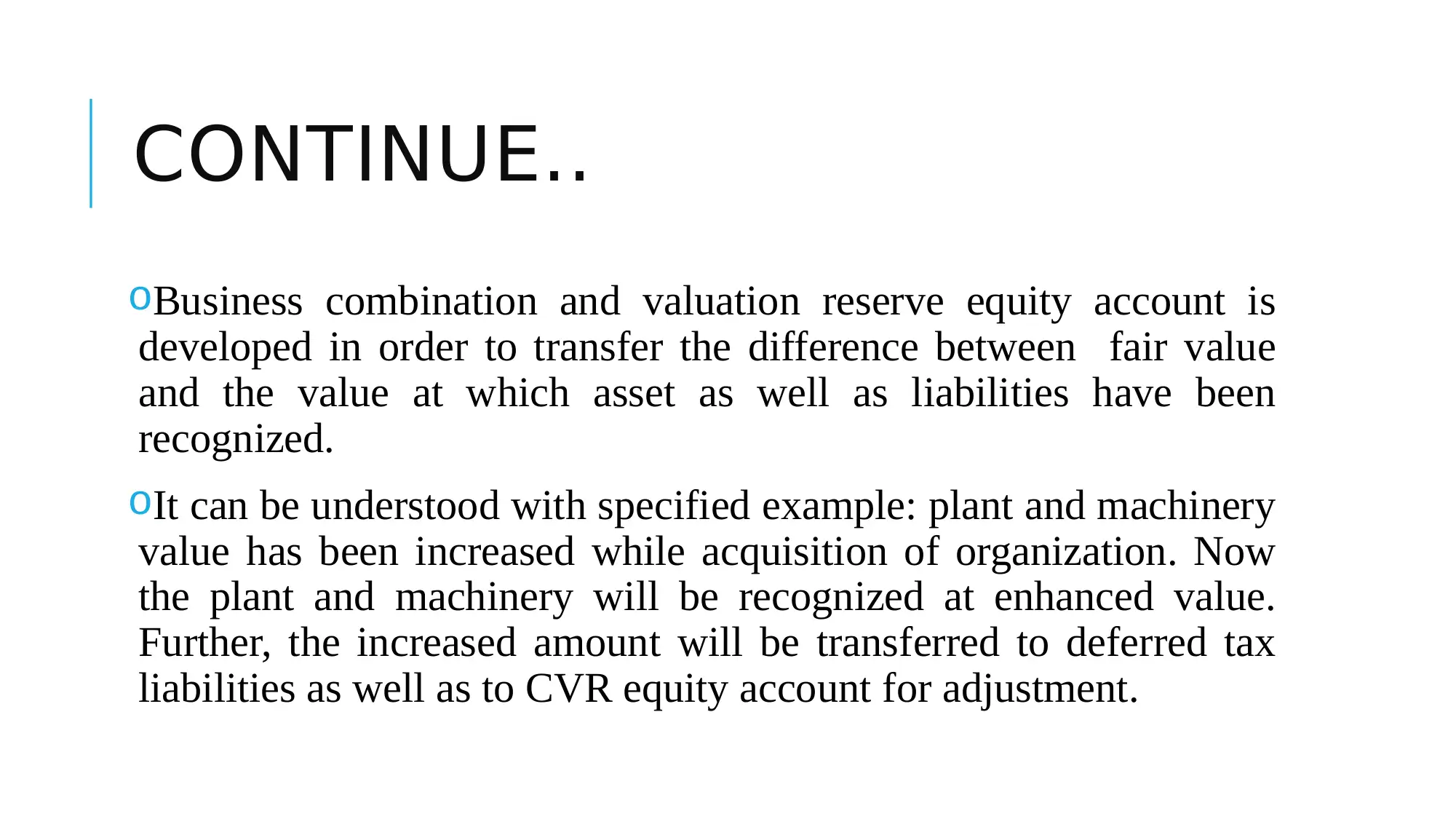

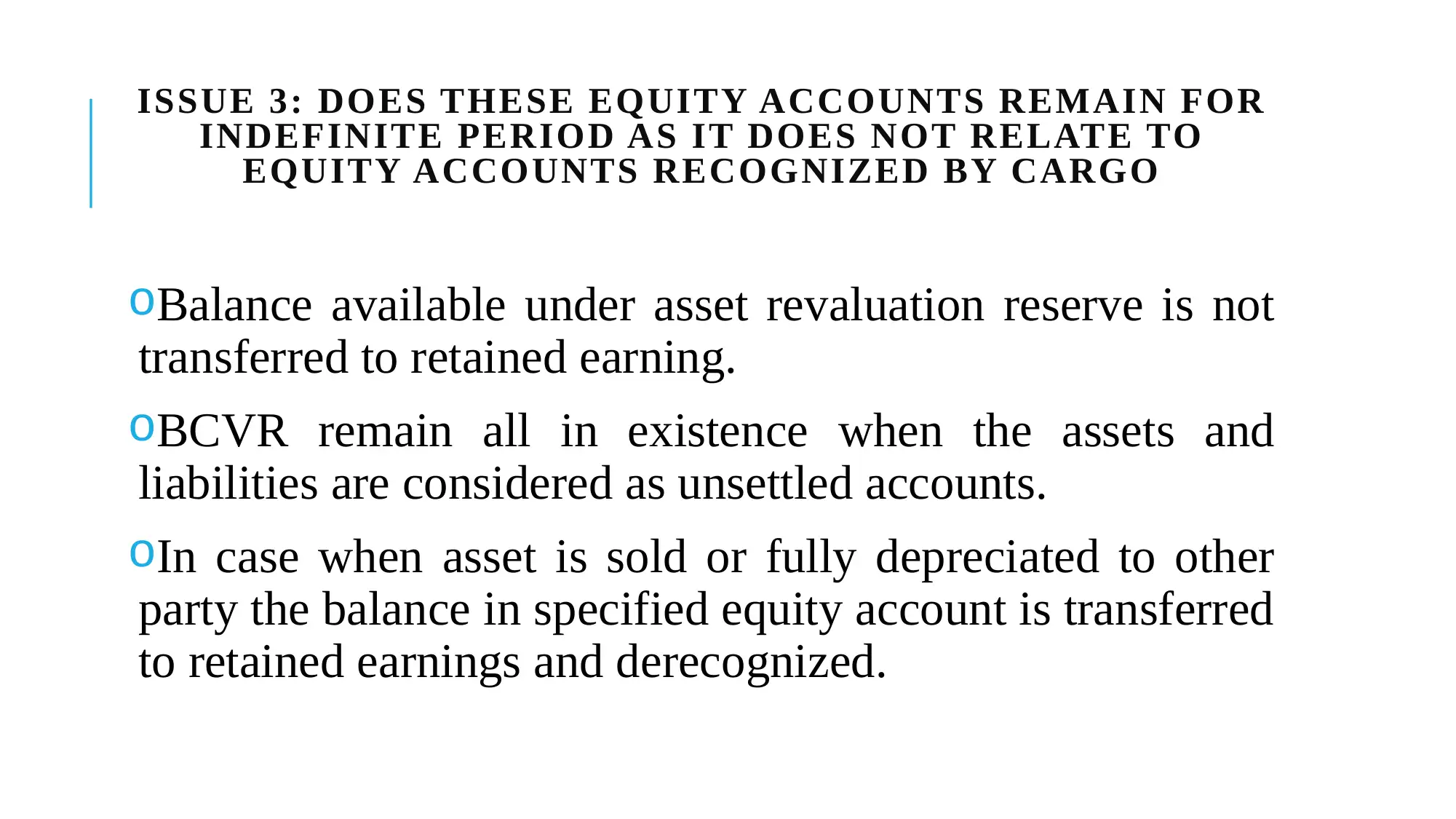

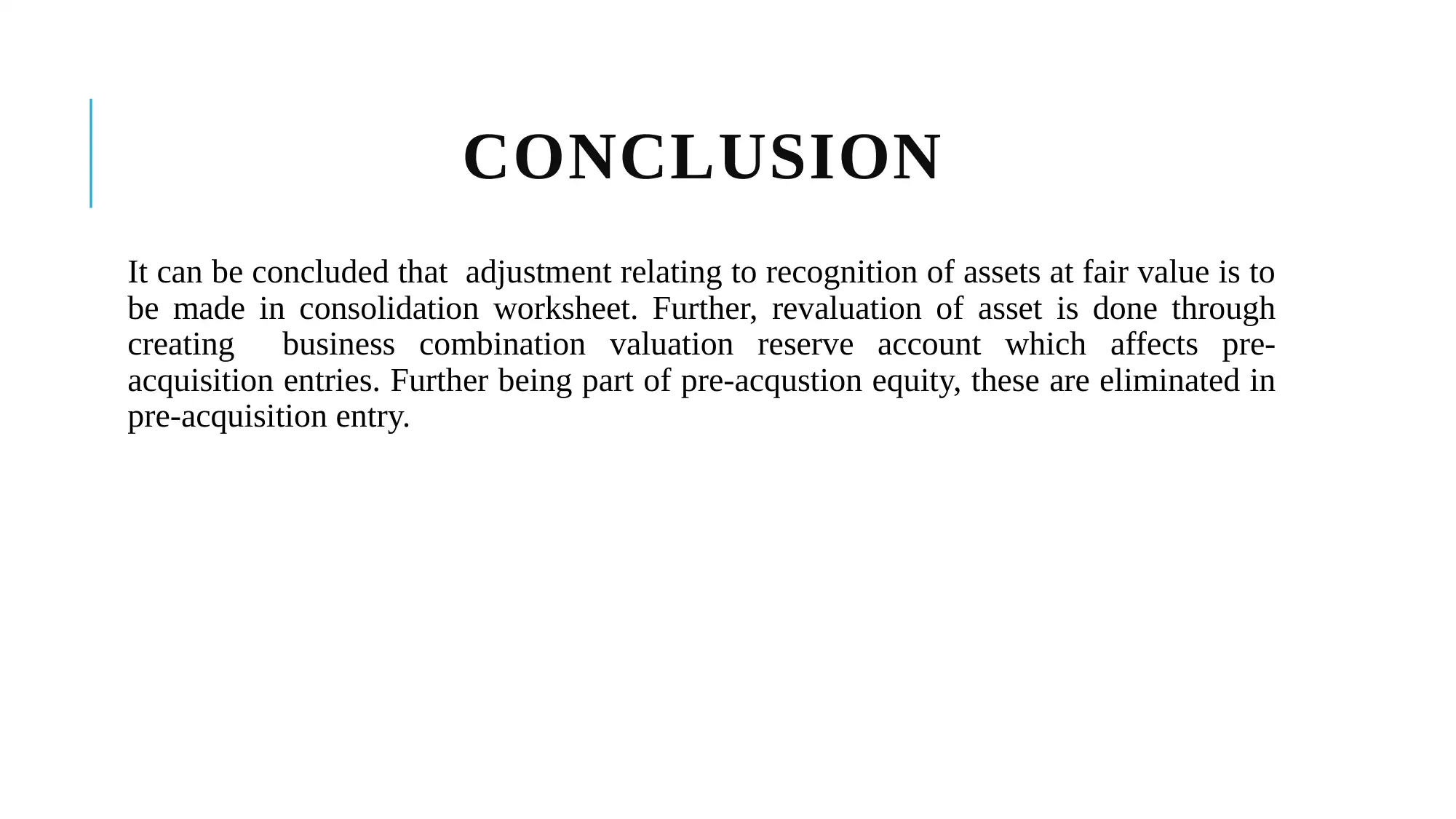

This case study provides an analysis of accounting issues related to business combinations and consolidations, specifically addressing where adjustments to fair value should be made, which equity accounts are used in revaluing assets and liabilities, and the existence of these equity accounts. It references AASB 3, which specifies provisions for transactions meeting the definition of a business combination, and discusses the recognition of assets and liabilities at fair value. The report suggests that adjustments to fair value are more appropriately made in the consolidation worksheet and that organizations typically use Asset Revaluation Surplus and Business Combination Valuation Reserve accounts during revaluation. It concludes that these pre-acquisition equity accounts are eliminated in pre-acquisition entries and that the balance in the asset revaluation reserve is transferred to retained earnings when the asset is sold or fully depreciated. The analysis is supported by references to accounting standards and textbooks.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.