Comprehensive Account and Finance Report: Financial Analysis

VerifiedAdded on 2023/01/17

|20

|3923

|47

Report

AI Summary

This report provides a detailed analysis of account and finance principles, encompassing key elements of financial statements such as assets, liabilities, equity, revenue, and expenses. It explores the functions of an auditor's report, including the different types of opinions (clean, qualified, adverse, and disclaimer) and their implications. The report also examines qualitative information within annual reports, focusing on the objectives of notes to financial statements and company overviews. Furthermore, it includes a consolidated statement of financial position and performs a thorough financial ratio analysis, calculating and interpreting ratios like current ratio, acid test ratio, accounts receivable turnover, inventory turnover, and accounts payable turnover to assess the financial health and performance of a company. The report concludes with common-size comparative statements of financial position, offering insights into financial trends.

ACCOUNT AND

FINANCE

Contents

FINANCE

Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Task 1.....................................................................................................................................3

Task 2.....................................................................................................................................6

Task 3.....................................................................................................................................7

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

MAIN BODY...................................................................................................................................3

Task 1.....................................................................................................................................3

Task 2.....................................................................................................................................6

Task 3.....................................................................................................................................7

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION

The term accounts and finance both are key aspects. Accounts can be defined as measure, storing

and interaction of monetary and anti-financial data on financial entities such as companies and

corporations (Anandarajan, Anandarajan and Srinivasan, 2012). Accounting is often alluded to as

"the business language". While the finance is value of monetary resources which are needed to

complete different operations. The report covers information about different elements of

financial statements, role of auditor’s report. In the further part of report various calculations are

done as accordance of given data.

MAIN BODY

Task 1.

(a) Element of financial statements.

Financial statements- Financial statements are documents compiled by the company's

management to show the financial results and role at a time. It has below mentioned

elements which are as follows:

Assets- Assets are the possessions or legal protections of a company for which

value of fund can be attached. In other terms, this is a value object that is expected

to produce benefits in the future. These assets can be classified into many types

such as tangible, intangible, current and noncurrent assets.

Liabilities- It can be defined as current responsibility of the company resulting

from previous events, the resolution of which is expected to occur in the outflow

from the corporation of assets reflecting economic benefits (Hillier, Westerfield,

Jaffe and Jordan, 2013). There are various types of liabilities such as current and

noncurrent liabilities.

Equity- Equity is the financial interest of a corporation in the type of a portfolio.

In financial terms, it is the contrast between the asset value and the expense of

debt of anything owned. This is primarily the remaining sum balanced by the

assets toward liabilities.

Investment by owners- This indicates the gain in capital arising from the sale of

assets in return for ownership stake (Czarniawska, 2012). This describes the

The term accounts and finance both are key aspects. Accounts can be defined as measure, storing

and interaction of monetary and anti-financial data on financial entities such as companies and

corporations (Anandarajan, Anandarajan and Srinivasan, 2012). Accounting is often alluded to as

"the business language". While the finance is value of monetary resources which are needed to

complete different operations. The report covers information about different elements of

financial statements, role of auditor’s report. In the further part of report various calculations are

done as accordance of given data.

MAIN BODY

Task 1.

(a) Element of financial statements.

Financial statements- Financial statements are documents compiled by the company's

management to show the financial results and role at a time. It has below mentioned

elements which are as follows:

Assets- Assets are the possessions or legal protections of a company for which

value of fund can be attached. In other terms, this is a value object that is expected

to produce benefits in the future. These assets can be classified into many types

such as tangible, intangible, current and noncurrent assets.

Liabilities- It can be defined as current responsibility of the company resulting

from previous events, the resolution of which is expected to occur in the outflow

from the corporation of assets reflecting economic benefits (Hillier, Westerfield,

Jaffe and Jordan, 2013). There are various types of liabilities such as current and

noncurrent liabilities.

Equity- Equity is the financial interest of a corporation in the type of a portfolio.

In financial terms, it is the contrast between the asset value and the expense of

debt of anything owned. This is primarily the remaining sum balanced by the

assets toward liabilities.

Investment by owners- This indicates the gain in capital arising from the sale of

assets in return for ownership stake (Czarniawska, 2012). This describes the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

commitment of any owner to the company. The issue of shareholdings by a

company for money is expenditure by the owners.

Distribution to owners- It reflects a reduction in capital arising from the sale to the

owners. It shall assess the drawdown of the owner from the ownership stake of

the firm. An example of payment to owners is the monetary dividends paid by a

corporation to its investors.

Revenue- Revenue is the money a company receives from its regular business

operations. It is the inflow of capital, which results in an improvement in the

equity of the shareholder. Trade of goods and services for exchange of cash is an

example of income.

Gains- Gain is an improvement in the assets of the owner of secondary

transactions that are sporadic and non-recurring in nature (Power, 2012).

Expenses- Expenditures are the gross outflows of income generated by the

business venture. The total expenditures are charged to the profit and loss ledger.

Losses- Loss is a reduction in owner's capital as a result of secondary transactions

that are frequent and non-recurring in nature.

Comprehensive income- Comprehensive income is a shift in the company's assets

from non-owner origin transactions. That covers all adjustments in the company's

capital, other than those arising from acquisitions by investors and transfers to

owners (Chan, Tong and Zhang, 2012).

(b) The functions of the auditor’s report in an annual report.

The auditor's report expresses an opinion on the accuracy and quality of the firm's

monetary results. Within the report, the auditor may express any concerns about the

financial position of the business or any additional details related to it. There are basically

four types of auditor’s report which are as:

The clean or unqualified opinion- This report shows the auditor's view that all the

documents released for the analysis show that the financial transactions and records of

the company are accurate and appropriate (Byrne, Flood and Willis, 2012).

Qualified opinion- This report is usually positive because it shows that the auditor

has found no problems with the monetary documentation.

company for money is expenditure by the owners.

Distribution to owners- It reflects a reduction in capital arising from the sale to the

owners. It shall assess the drawdown of the owner from the ownership stake of

the firm. An example of payment to owners is the monetary dividends paid by a

corporation to its investors.

Revenue- Revenue is the money a company receives from its regular business

operations. It is the inflow of capital, which results in an improvement in the

equity of the shareholder. Trade of goods and services for exchange of cash is an

example of income.

Gains- Gain is an improvement in the assets of the owner of secondary

transactions that are sporadic and non-recurring in nature (Power, 2012).

Expenses- Expenditures are the gross outflows of income generated by the

business venture. The total expenditures are charged to the profit and loss ledger.

Losses- Loss is a reduction in owner's capital as a result of secondary transactions

that are frequent and non-recurring in nature.

Comprehensive income- Comprehensive income is a shift in the company's assets

from non-owner origin transactions. That covers all adjustments in the company's

capital, other than those arising from acquisitions by investors and transfers to

owners (Chan, Tong and Zhang, 2012).

(b) The functions of the auditor’s report in an annual report.

The auditor's report expresses an opinion on the accuracy and quality of the firm's

monetary results. Within the report, the auditor may express any concerns about the

financial position of the business or any additional details related to it. There are basically

four types of auditor’s report which are as:

The clean or unqualified opinion- This report shows the auditor's view that all the

documents released for the analysis show that the financial transactions and records of

the company are accurate and appropriate (Byrne, Flood and Willis, 2012).

Qualified opinion- This report is usually positive because it shows that the auditor

has found no problems with the monetary documentation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Adverse opinion- The unfavourable judgment means the company has not

complied with the standards by the UK GAAP and that the auditor has found a

gap in the firm's statements.

Disclaimer of opinion- This implies that the auditor was not able to finish the

audit due to a specific reason.

It has below mentioned functions which are as follows:

If any of the issues needed to be included in the audit report have been addressed

in the adverse or eligible form, the auditor's report shall also state the explanations

for them (Jones, 2014).

The findings or remarks on business transactions or matters that have a negative

effect on the ability to function of the firm referred to in the report of the auditor

shall be perused by the auditor in the general assembly before the firm. It can be

inspected by any representative of the firm.

The auditor should have a comment on the following matters in his report on

behalf of the businesses covered by that order: fixed assets, stock, fraud reporting

etc.

(c) Qualitative information in annual reports and its objectives.

In the annual report, different types of qualitative information are included such as notes of

financial statements, about company and many more (Van Hoepen, 2013). Herein, below

objectives of these information is done below:

Objective of notes of financial statements- The main purpose of the notes to the financial

reports is to further explain the accounting processes used by firm and to reveal

information that happened during and instantly after the end of the financial reporting

period.

Objective of information about company- Annual reports include details on the firm's

mission and history and review the company's accomplishments over the past year

(Hellmann, 2013). Due to which users can access information about industry in which

company deals.

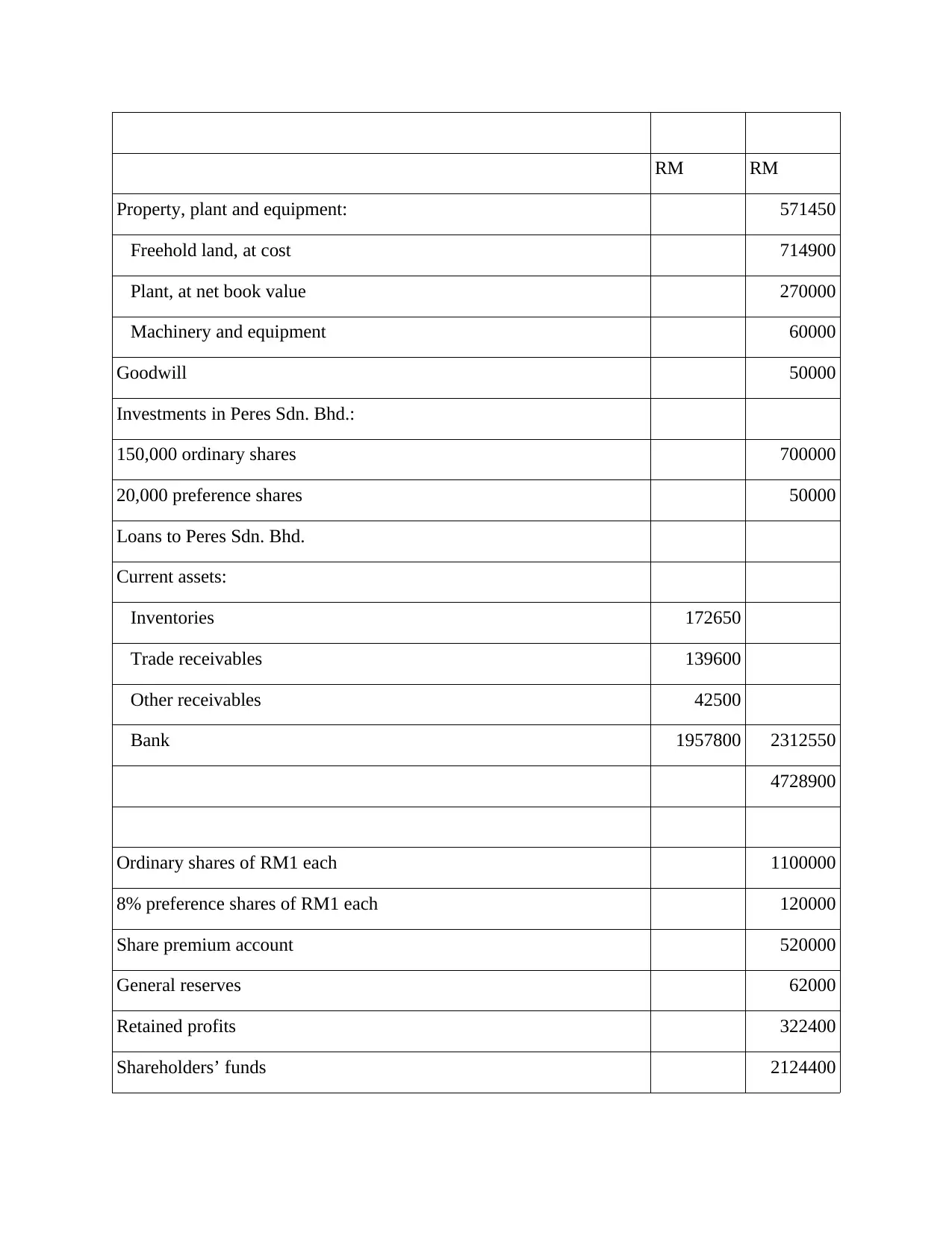

Task 2.

Consolidated statement of financial position of Simone Bhd. as at 31 December 2018.

complied with the standards by the UK GAAP and that the auditor has found a

gap in the firm's statements.

Disclaimer of opinion- This implies that the auditor was not able to finish the

audit due to a specific reason.

It has below mentioned functions which are as follows:

If any of the issues needed to be included in the audit report have been addressed

in the adverse or eligible form, the auditor's report shall also state the explanations

for them (Jones, 2014).

The findings or remarks on business transactions or matters that have a negative

effect on the ability to function of the firm referred to in the report of the auditor

shall be perused by the auditor in the general assembly before the firm. It can be

inspected by any representative of the firm.

The auditor should have a comment on the following matters in his report on

behalf of the businesses covered by that order: fixed assets, stock, fraud reporting

etc.

(c) Qualitative information in annual reports and its objectives.

In the annual report, different types of qualitative information are included such as notes of

financial statements, about company and many more (Van Hoepen, 2013). Herein, below

objectives of these information is done below:

Objective of notes of financial statements- The main purpose of the notes to the financial

reports is to further explain the accounting processes used by firm and to reveal

information that happened during and instantly after the end of the financial reporting

period.

Objective of information about company- Annual reports include details on the firm's

mission and history and review the company's accomplishments over the past year

(Hellmann, 2013). Due to which users can access information about industry in which

company deals.

Task 2.

Consolidated statement of financial position of Simone Bhd. as at 31 December 2018.

RM RM

Property, plant and equipment: 571450

Freehold land, at cost 714900

Plant, at net book value 270000

Machinery and equipment 60000

Goodwill 50000

Investments in Peres Sdn. Bhd.:

150,000 ordinary shares 700000

20,000 preference shares 50000

Loans to Peres Sdn. Bhd.

Current assets:

Inventories 172650

Trade receivables 139600

Other receivables 42500

Bank 1957800 2312550

4728900

Ordinary shares of RM1 each 1100000

8% preference shares of RM1 each 120000

Share premium account 520000

General reserves 62000

Retained profits 322400

Shareholders’ funds 2124400

Property, plant and equipment: 571450

Freehold land, at cost 714900

Plant, at net book value 270000

Machinery and equipment 60000

Goodwill 50000

Investments in Peres Sdn. Bhd.:

150,000 ordinary shares 700000

20,000 preference shares 50000

Loans to Peres Sdn. Bhd.

Current assets:

Inventories 172650

Trade receivables 139600

Other receivables 42500

Bank 1957800 2312550

4728900

Ordinary shares of RM1 each 1100000

8% preference shares of RM1 each 120000

Share premium account 520000

General reserves 62000

Retained profits 322400

Shareholders’ funds 2124400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Loan from Simone Bhd. 59000

Current liabilities:

Trade payables 151100

Other payables 130000

Taxation 140000 421100

4728900

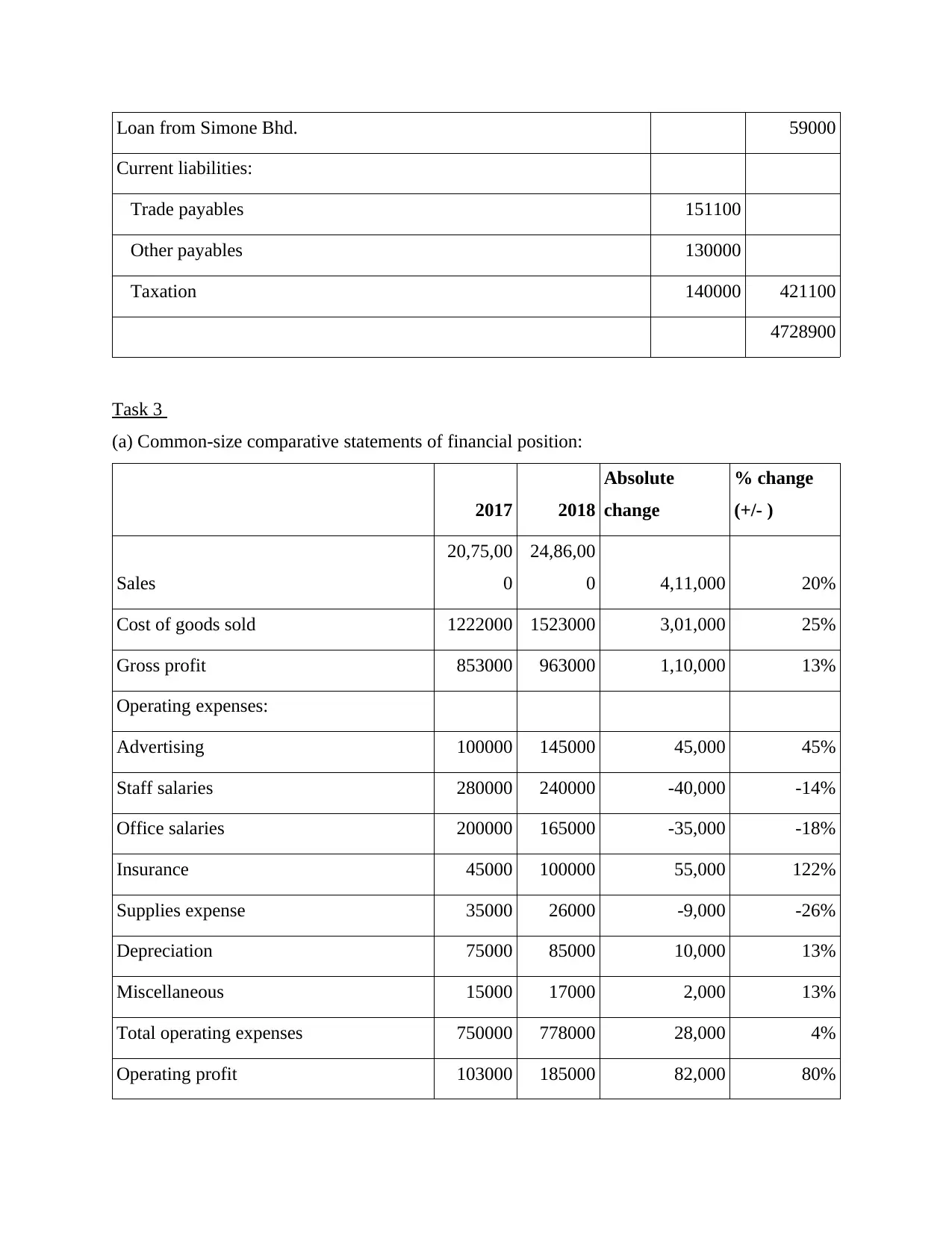

Task 3

(a) Common-size comparative statements of financial position:

2017 2018

Absolute

change

% change

(+/- )

Sales

20,75,00

0

24,86,00

0 4,11,000 20%

Cost of goods sold 1222000 1523000 3,01,000 25%

Gross profit 853000 963000 1,10,000 13%

Operating expenses:

Advertising 100000 145000 45,000 45%

Staff salaries 280000 240000 -40,000 -14%

Office salaries 200000 165000 -35,000 -18%

Insurance 45000 100000 55,000 122%

Supplies expense 35000 26000 -9,000 -26%

Depreciation 75000 85000 10,000 13%

Miscellaneous 15000 17000 2,000 13%

Total operating expenses 750000 778000 28,000 4%

Operating profit 103000 185000 82,000 80%

Current liabilities:

Trade payables 151100

Other payables 130000

Taxation 140000 421100

4728900

Task 3

(a) Common-size comparative statements of financial position:

2017 2018

Absolute

change

% change

(+/- )

Sales

20,75,00

0

24,86,00

0 4,11,000 20%

Cost of goods sold 1222000 1523000 3,01,000 25%

Gross profit 853000 963000 1,10,000 13%

Operating expenses:

Advertising 100000 145000 45,000 45%

Staff salaries 280000 240000 -40,000 -14%

Office salaries 200000 165000 -35,000 -18%

Insurance 45000 100000 55,000 122%

Supplies expense 35000 26000 -9,000 -26%

Depreciation 75000 85000 10,000 13%

Miscellaneous 15000 17000 2,000 13%

Total operating expenses 750000 778000 28,000 4%

Operating profit 103000 185000 82,000 80%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interest expense 46000 44000 -2,000 -4%

Profit before tax 57000 141000 84,000 147%

Income tax expense 19000 47000 28,000 147%

Net profit 38,000 94,000 56,000 147%

Earnings per share 0.99 0.99 0 0%

Precise Company

Comparative Statements of Financial Position

As at 31 December 2018 and 2017

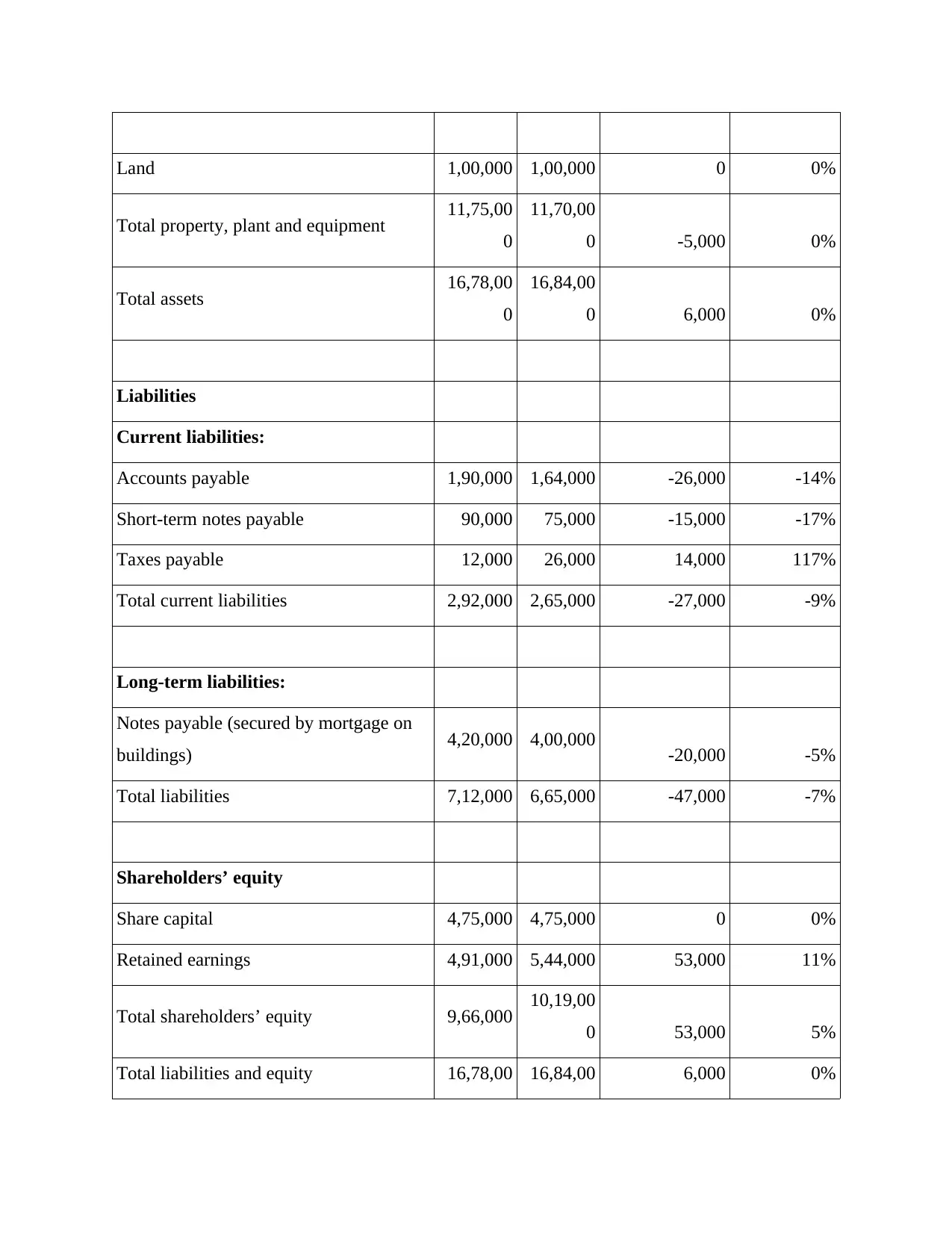

Assets 2017 2018 Absolute

change

(+/-) change

in %

Current Assets:

Cash 42,000 79,000 37,000 88%

Short-term investments 96,000 65,000 -31,000 -32%

Accounts receivable 1,00,000 1,20,000 20,000 20%

Merchandise inventory 2,65,000 2,50,000 -15,000 -6%

Total current assets 5,03,000 5,14,000 11,000 2%

Property, plant and equipment

Store equipment 3,50,000 4,00,000 50,000 14%

Office equipment 50,000 45,000 -5,000 -10%

Buildings 6,75,000 6,25,000 -50,000 -7%

Profit before tax 57000 141000 84,000 147%

Income tax expense 19000 47000 28,000 147%

Net profit 38,000 94,000 56,000 147%

Earnings per share 0.99 0.99 0 0%

Precise Company

Comparative Statements of Financial Position

As at 31 December 2018 and 2017

Assets 2017 2018 Absolute

change

(+/-) change

in %

Current Assets:

Cash 42,000 79,000 37,000 88%

Short-term investments 96,000 65,000 -31,000 -32%

Accounts receivable 1,00,000 1,20,000 20,000 20%

Merchandise inventory 2,65,000 2,50,000 -15,000 -6%

Total current assets 5,03,000 5,14,000 11,000 2%

Property, plant and equipment

Store equipment 3,50,000 4,00,000 50,000 14%

Office equipment 50,000 45,000 -5,000 -10%

Buildings 6,75,000 6,25,000 -50,000 -7%

Land 1,00,000 1,00,000 0 0%

Total property, plant and equipment 11,75,00

0

11,70,00

0 -5,000 0%

Total assets 16,78,00

0

16,84,00

0 6,000 0%

Liabilities

Current liabilities:

Accounts payable 1,90,000 1,64,000 -26,000 -14%

Short-term notes payable 90,000 75,000 -15,000 -17%

Taxes payable 12,000 26,000 14,000 117%

Total current liabilities 2,92,000 2,65,000 -27,000 -9%

Long-term liabilities:

Notes payable (secured by mortgage on

buildings) 4,20,000 4,00,000 -20,000 -5%

Total liabilities 7,12,000 6,65,000 -47,000 -7%

Shareholders’ equity

Share capital 4,75,000 4,75,000 0 0%

Retained earnings 4,91,000 5,44,000 53,000 11%

Total shareholders’ equity 9,66,000 10,19,00

0 53,000 5%

Total liabilities and equity 16,78,00 16,84,00 6,000 0%

Total property, plant and equipment 11,75,00

0

11,70,00

0 -5,000 0%

Total assets 16,78,00

0

16,84,00

0 6,000 0%

Liabilities

Current liabilities:

Accounts payable 1,90,000 1,64,000 -26,000 -14%

Short-term notes payable 90,000 75,000 -15,000 -17%

Taxes payable 12,000 26,000 14,000 117%

Total current liabilities 2,92,000 2,65,000 -27,000 -9%

Long-term liabilities:

Notes payable (secured by mortgage on

buildings) 4,20,000 4,00,000 -20,000 -5%

Total liabilities 7,12,000 6,65,000 -47,000 -7%

Shareholders’ equity

Share capital 4,75,000 4,75,000 0 0%

Retained earnings 4,91,000 5,44,000 53,000 11%

Total shareholders’ equity 9,66,000 10,19,00

0 53,000 5%

Total liabilities and equity 16,78,00 16,84,00 6,000 0%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 0

(b) Calculations of ratios:

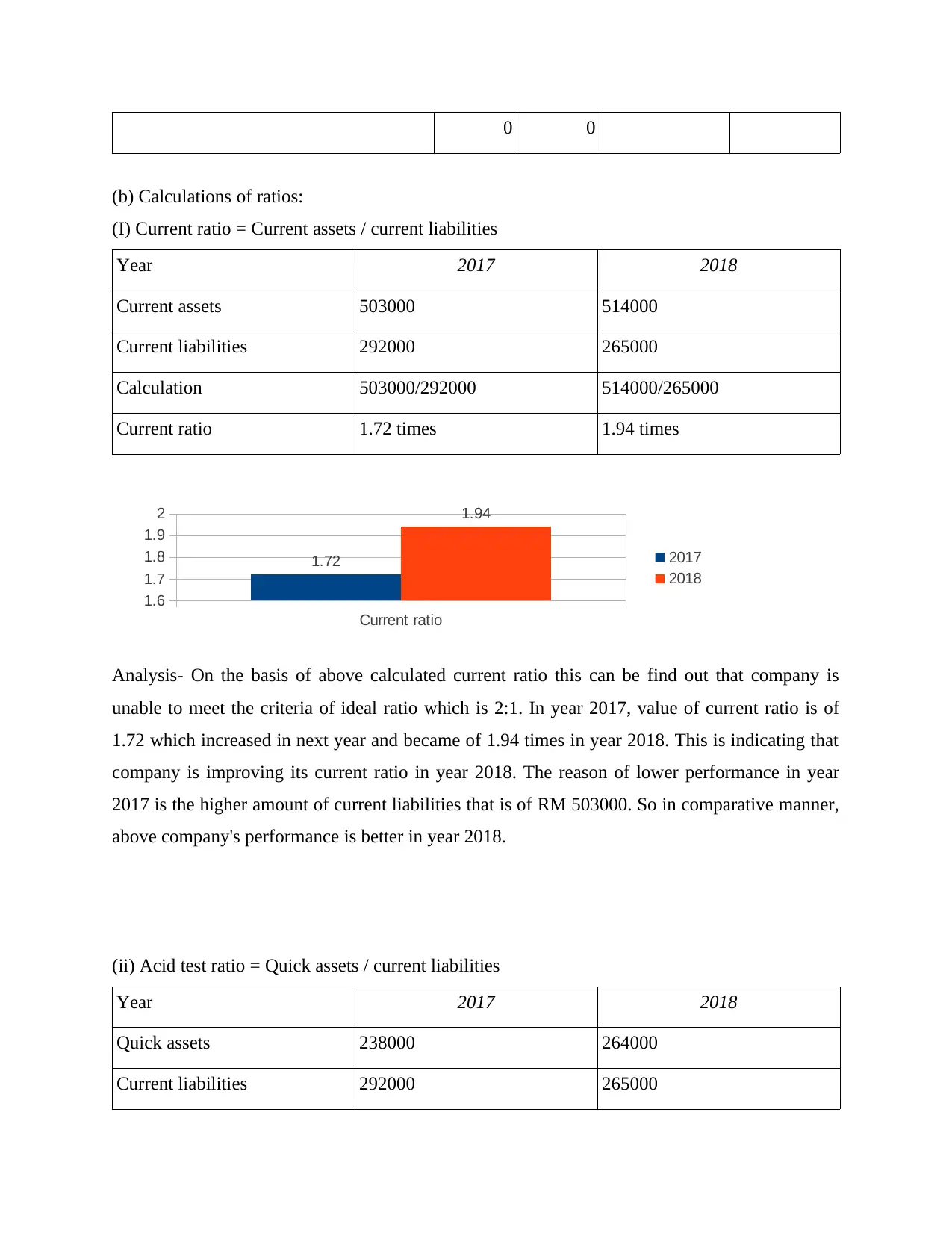

(I) Current ratio = Current assets / current liabilities

Year 2017 2018

Current assets 503000 514000

Current liabilities 292000 265000

Calculation 503000/292000 514000/265000

Current ratio 1.72 times 1.94 times

Current ratio

1.6

1.7

1.8

1.9

2

1.72

1.94

2017

2018

Analysis- On the basis of above calculated current ratio this can be find out that company is

unable to meet the criteria of ideal ratio which is 2:1. In year 2017, value of current ratio is of

1.72 which increased in next year and became of 1.94 times in year 2018. This is indicating that

company is improving its current ratio in year 2018. The reason of lower performance in year

2017 is the higher amount of current liabilities that is of RM 503000. So in comparative manner,

above company's performance is better in year 2018.

(ii) Acid test ratio = Quick assets / current liabilities

Year 2017 2018

Quick assets 238000 264000

Current liabilities 292000 265000

(b) Calculations of ratios:

(I) Current ratio = Current assets / current liabilities

Year 2017 2018

Current assets 503000 514000

Current liabilities 292000 265000

Calculation 503000/292000 514000/265000

Current ratio 1.72 times 1.94 times

Current ratio

1.6

1.7

1.8

1.9

2

1.72

1.94

2017

2018

Analysis- On the basis of above calculated current ratio this can be find out that company is

unable to meet the criteria of ideal ratio which is 2:1. In year 2017, value of current ratio is of

1.72 which increased in next year and became of 1.94 times in year 2018. This is indicating that

company is improving its current ratio in year 2018. The reason of lower performance in year

2017 is the higher amount of current liabilities that is of RM 503000. So in comparative manner,

above company's performance is better in year 2018.

(ii) Acid test ratio = Quick assets / current liabilities

Year 2017 2018

Quick assets 238000 264000

Current liabilities 292000 265000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

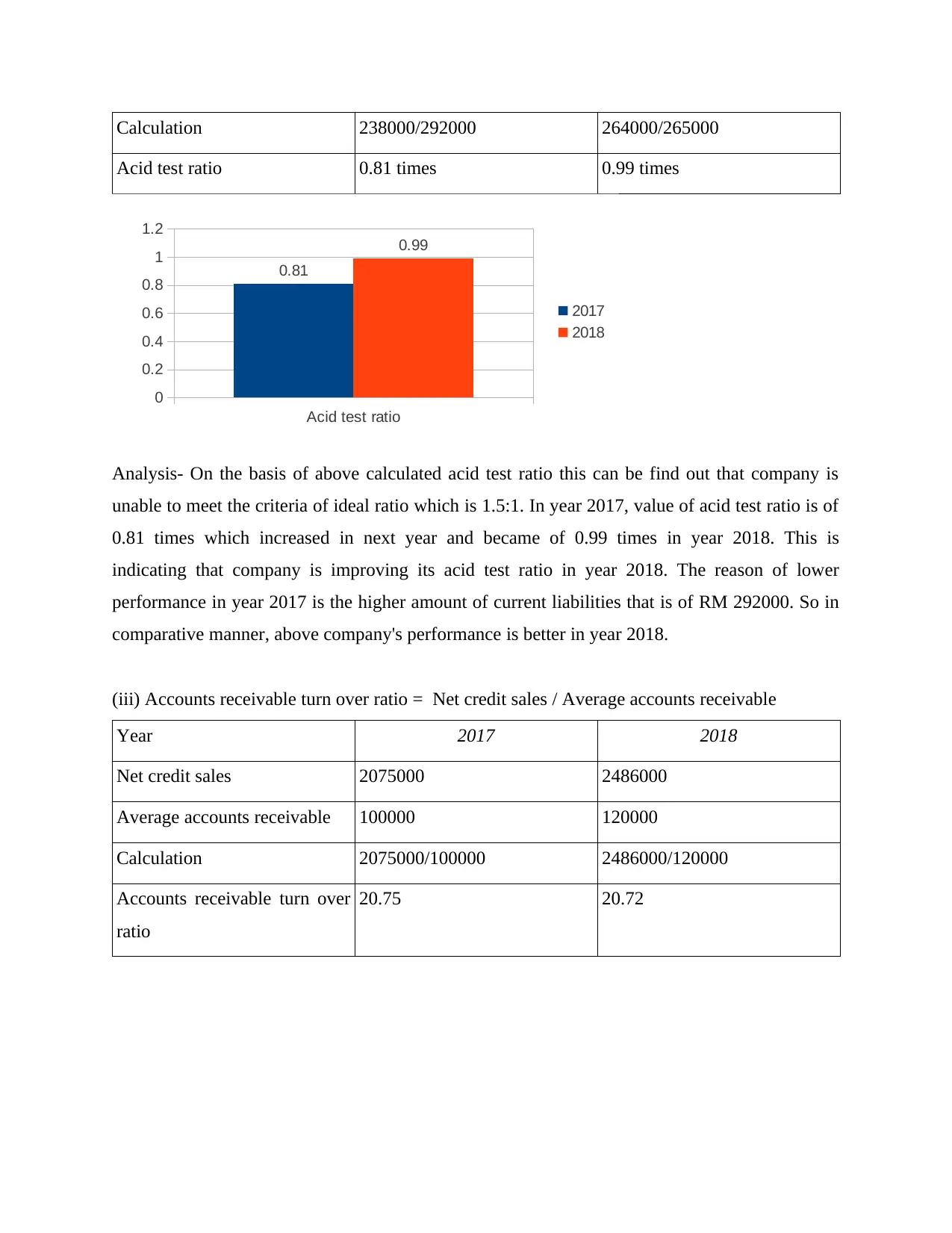

Calculation 238000/292000 264000/265000

Acid test ratio 0.81 times 0.99 times

Acid test ratio

0

0.2

0.4

0.6

0.8

1

1.2

0.81

0.99

2017

2018

Analysis- On the basis of above calculated acid test ratio this can be find out that company is

unable to meet the criteria of ideal ratio which is 1.5:1. In year 2017, value of acid test ratio is of

0.81 times which increased in next year and became of 0.99 times in year 2018. This is

indicating that company is improving its acid test ratio in year 2018. The reason of lower

performance in year 2017 is the higher amount of current liabilities that is of RM 292000. So in

comparative manner, above company's performance is better in year 2018.

(iii) Accounts receivable turn over ratio = Net credit sales / Average accounts receivable

Year 2017 2018

Net credit sales 2075000 2486000

Average accounts receivable 100000 120000

Calculation 2075000/100000 2486000/120000

Accounts receivable turn over

ratio

20.75 20.72

Acid test ratio 0.81 times 0.99 times

Acid test ratio

0

0.2

0.4

0.6

0.8

1

1.2

0.81

0.99

2017

2018

Analysis- On the basis of above calculated acid test ratio this can be find out that company is

unable to meet the criteria of ideal ratio which is 1.5:1. In year 2017, value of acid test ratio is of

0.81 times which increased in next year and became of 0.99 times in year 2018. This is

indicating that company is improving its acid test ratio in year 2018. The reason of lower

performance in year 2017 is the higher amount of current liabilities that is of RM 292000. So in

comparative manner, above company's performance is better in year 2018.

(iii) Accounts receivable turn over ratio = Net credit sales / Average accounts receivable

Year 2017 2018

Net credit sales 2075000 2486000

Average accounts receivable 100000 120000

Calculation 2075000/100000 2486000/120000

Accounts receivable turn over

ratio

20.75 20.72

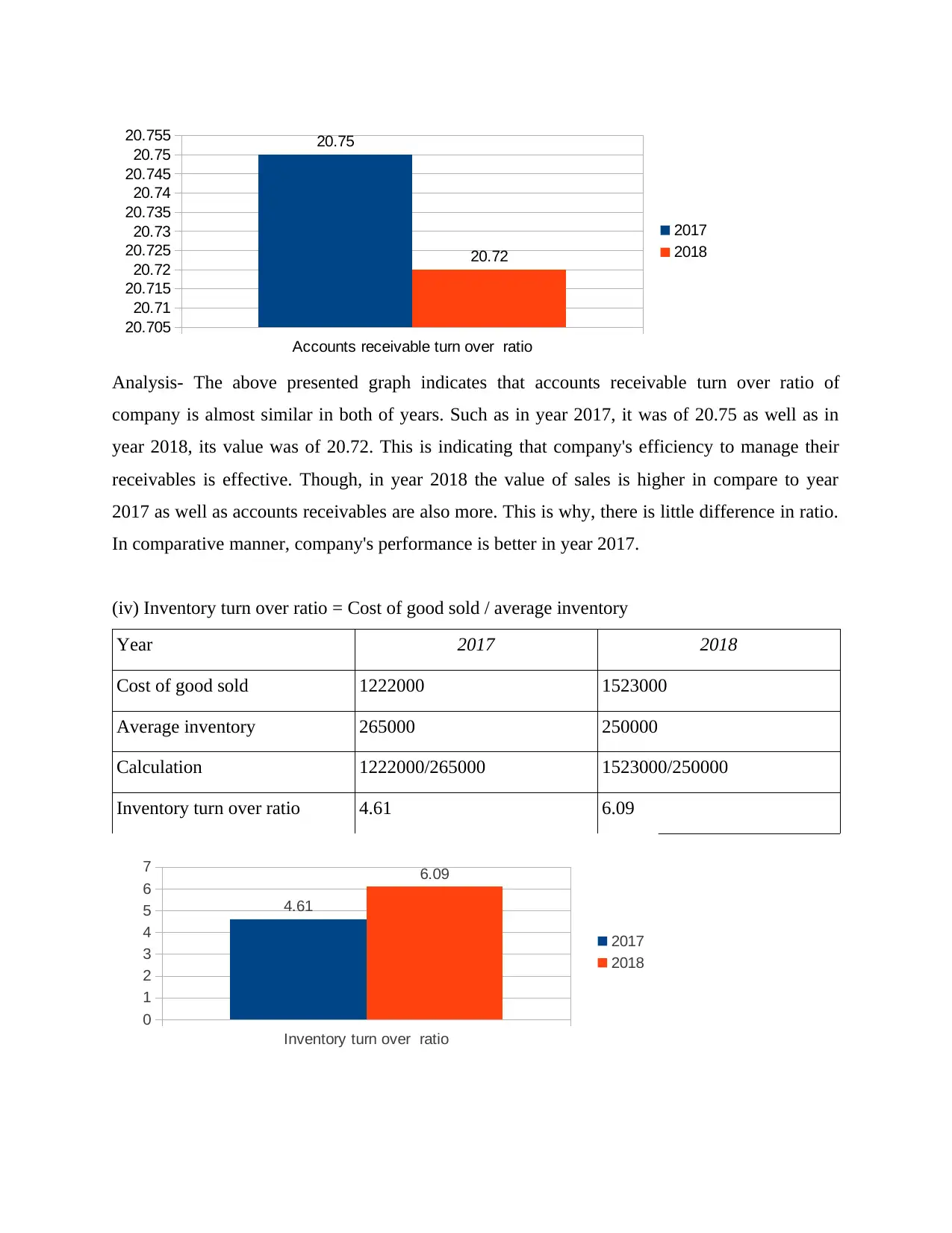

Analysis- The above presented graph indicates that accounts receivable turn over ratio of

company is almost similar in both of years. Such as in year 2017, it was of 20.75 as well as in

year 2018, its value was of 20.72. This is indicating that company's efficiency to manage their

receivables is effective. Though, in year 2018 the value of sales is higher in compare to year

2017 as well as accounts receivables are also more. This is why, there is little difference in ratio.

In comparative manner, company's performance is better in year 2017.

(iv) Inventory turn over ratio = Cost of good sold / average inventory

Year 2017 2018

Cost of good sold 1222000 1523000

Average inventory 265000 250000

Calculation 1222000/265000 1523000/250000

Inventory turn over ratio 4.61 6.09

Inventory turn over ratio

0

1

2

3

4

5

6

7

4.61

6.09

2017

2018

Accounts receivable turn over ratio

20.705

20.71

20.715

20.72

20.725

20.73

20.735

20.74

20.745

20.75

20.755 20.75

20.72

2017

2018

company is almost similar in both of years. Such as in year 2017, it was of 20.75 as well as in

year 2018, its value was of 20.72. This is indicating that company's efficiency to manage their

receivables is effective. Though, in year 2018 the value of sales is higher in compare to year

2017 as well as accounts receivables are also more. This is why, there is little difference in ratio.

In comparative manner, company's performance is better in year 2017.

(iv) Inventory turn over ratio = Cost of good sold / average inventory

Year 2017 2018

Cost of good sold 1222000 1523000

Average inventory 265000 250000

Calculation 1222000/265000 1523000/250000

Inventory turn over ratio 4.61 6.09

Inventory turn over ratio

0

1

2

3

4

5

6

7

4.61

6.09

2017

2018

Accounts receivable turn over ratio

20.705

20.71

20.715

20.72

20.725

20.73

20.735

20.74

20.745

20.75

20.755 20.75

20.72

2017

2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.