Accountancy Introduction Task Solution - Financial Analysis

VerifiedAdded on 2023/06/09

|8

|1134

|149

Homework Assignment

AI Summary

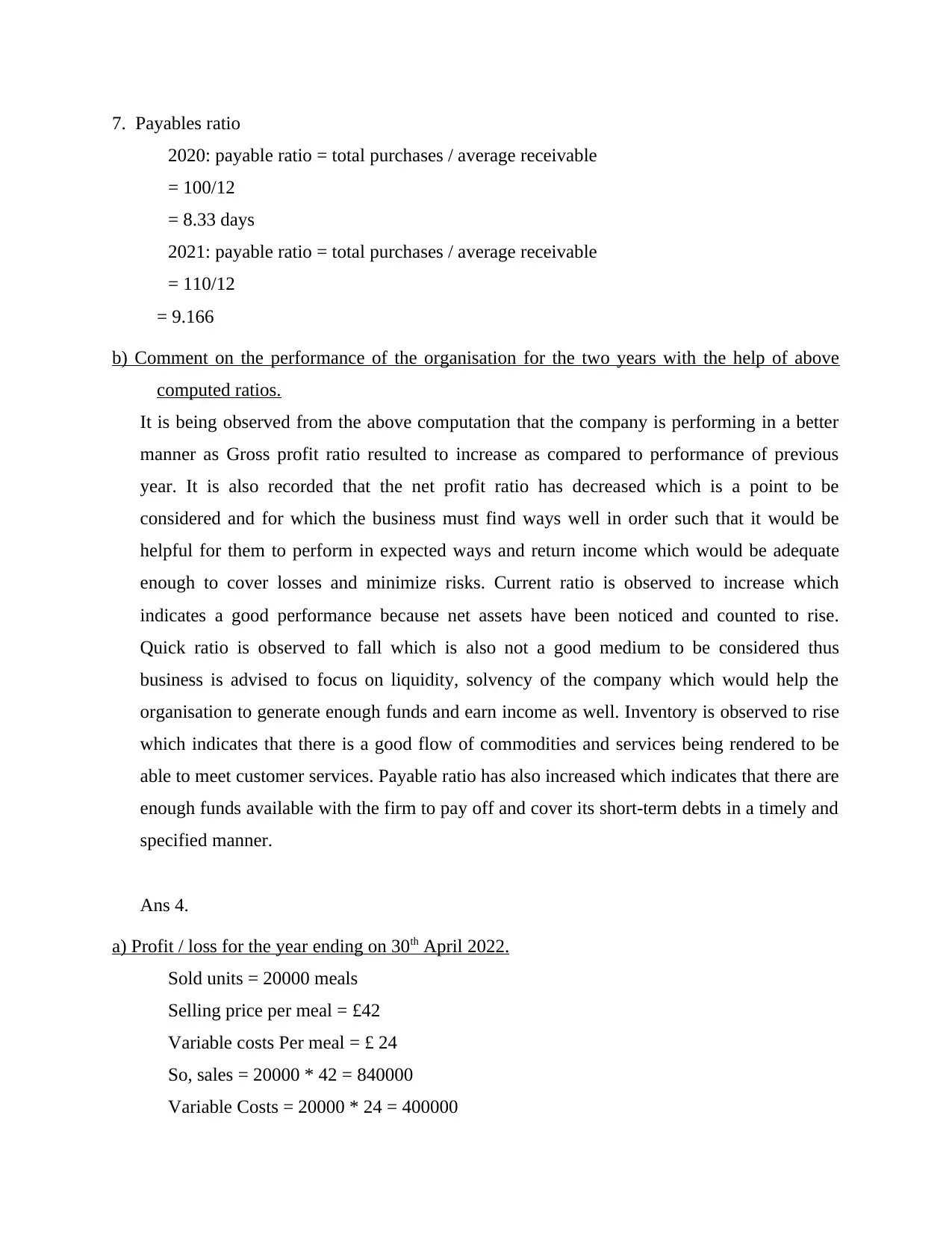

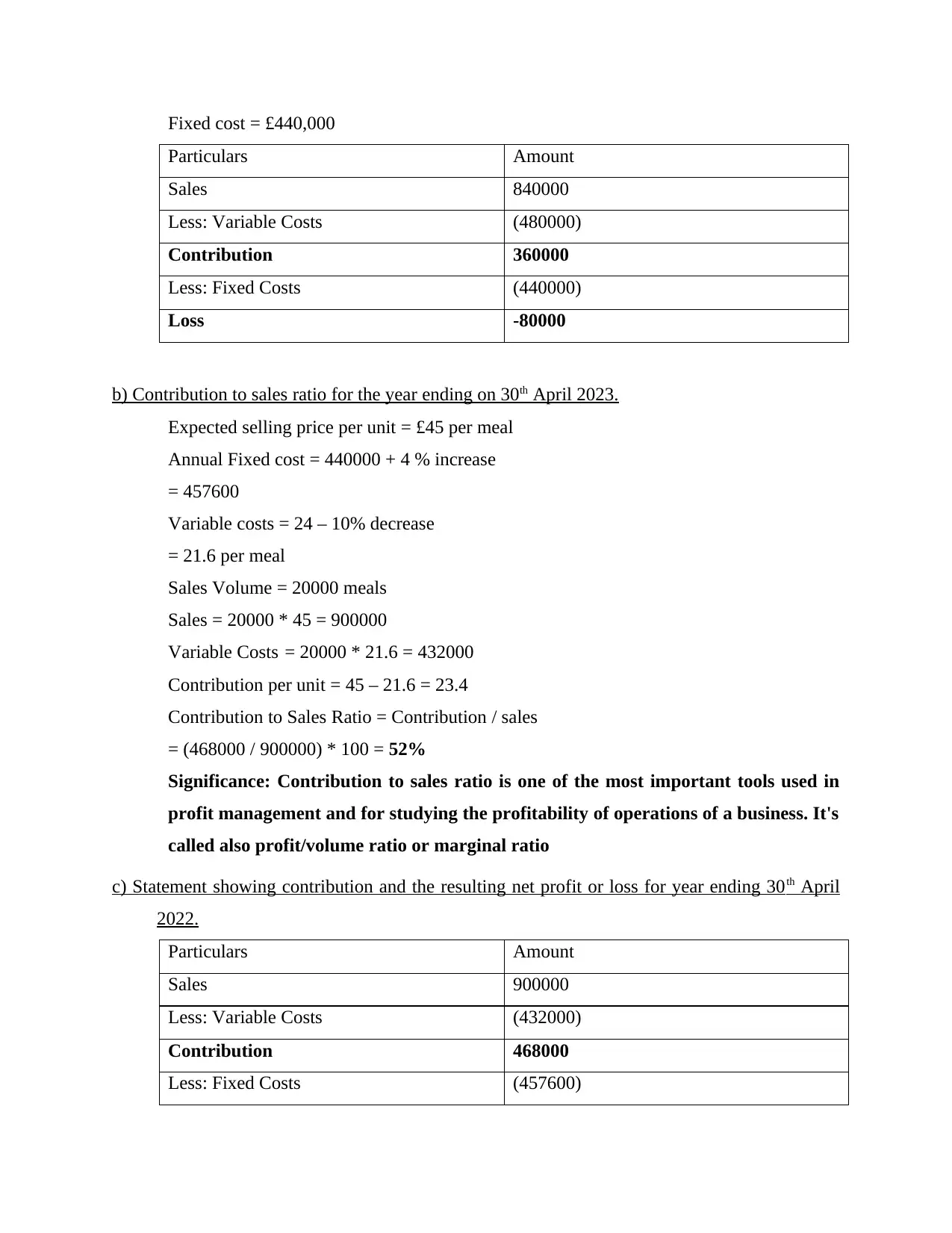

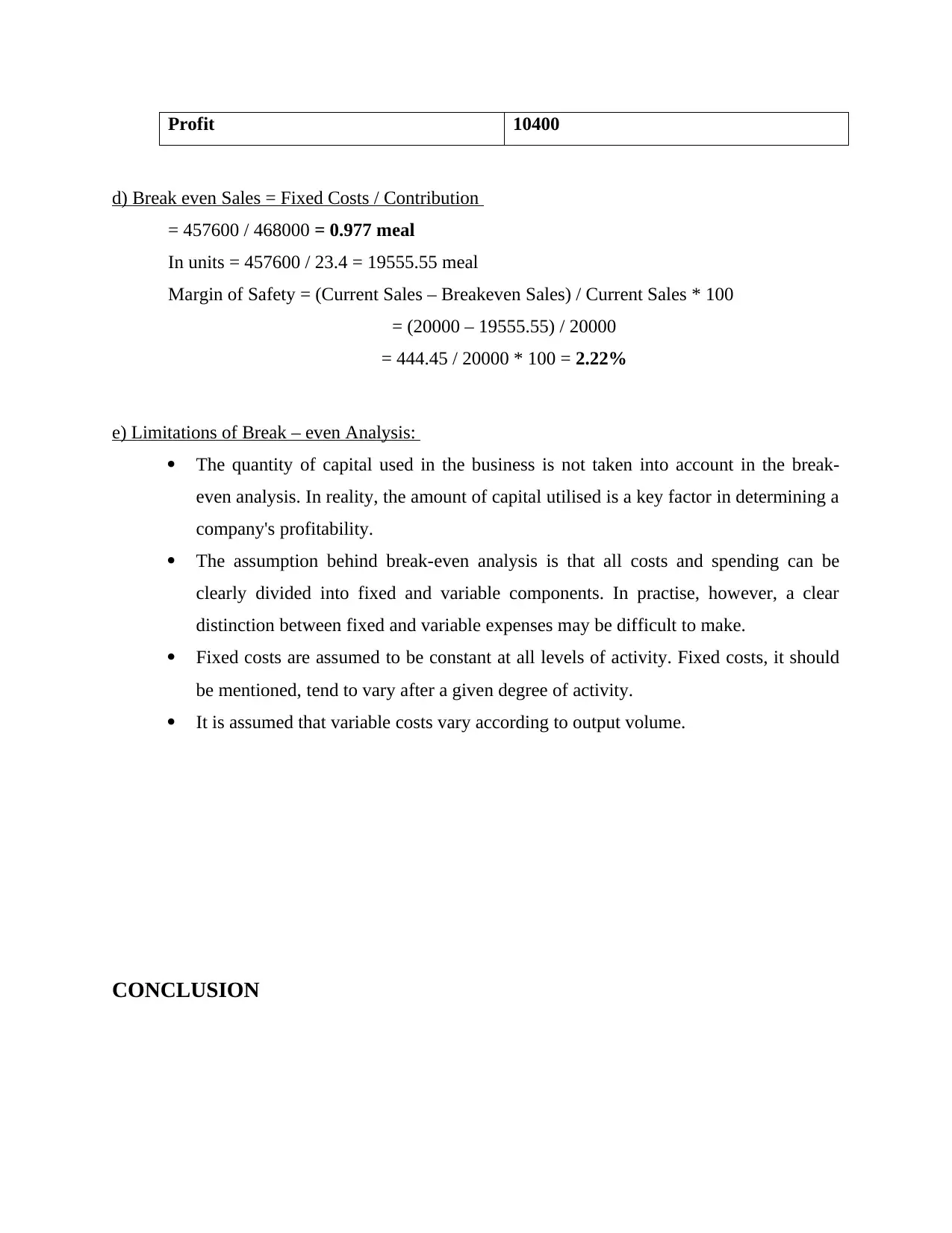

This accountancy assignment solution presents a comprehensive analysis of financial statements, ratio calculations, and break-even analysis. The solution begins with the preparation of an income statement and a statement of financial position. It then delves into ratio analysis, comparing gross profit, net profit, current, quick, inventory holding, receivables, and payables ratios for two years, with comments on the organization's performance. The assignment also includes a profit/loss calculation, contribution to sales ratio, and break-even analysis, followed by a discussion of the limitations of break-even analysis. The document concludes with references and is designed to help students understand financial accounting concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.