Ethical Dilemmas and Challenges for Accountants in Profession

VerifiedAdded on 2022/12/15

|16

|4244

|307

Essay

AI Summary

This essay analyzes ethical dilemmas faced by accountants, focusing on the International Federation of Accountants (IFAC). It explores how these dilemmas affect individuals, stakeholders, and organizations, examining issues like corporate ethics failures (Enron, WorldCom) and the impact of regulations (Sarbanes-Oxley Act). The essay discusses stakeholder theory, ethical awareness, and the influence of professional judgment, as well as challenges such as skill gaps, pressure from increasing demands, and the need for ethical behavior. It also highlights internal conflicts and safeguards like seeking advice and maintaining confidentiality. The study addresses specific ethical threats including self-interest, self-review, advocacy, familiarity, and intimidation, while suggesting measures to resolve them. The essay examines ethical culture, ethical accounting practices, and business issues like security and bribery, offering guidance and frameworks for accountants to address these challenges. Overall, the essay emphasizes the importance of ethical conduct in the accounting profession and provides insights into navigating complex issues and promoting public interest.

Running head: ACCOUNTANTS IN THE PROFESSION

Accountants in the profession

Name of the student

Name of the university

Authors note

Introduction

Accountants in the profession

Name of the student

Name of the university

Authors note

Introduction

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTANTS IN THE PROFESSION

The study assignment provides information about three articles related to the

international federation of accountants (IFAC). The main focus of this process is to serve the

public interest, improve the accounting process and contribute to the overall development of

the organisation. Therefore the study topic describes three ethical dilemmas from three

articles. Apart from this how these ethical dilemmas can affect the individuals, stakeholders

and key organisations. These ethical issues can well affect the overall fundamental rights and

obligations related to these fundamental principles.

On the other hand in the second part, the study discusses about two sustainability

challenges which are affecting the overall process and how to cope up with these issues.

Discussion

PART A: Ethical Dilemmas – Issues and Solutions

In the first article diversified role of the professional accountant in business have been

discussed by international federation of accountants. The overall mission of this process is to

serve the public interest, develop strong accounting connection between organisations,

industry, public and private sectors. Furthermore they always encourage the professionals to

develop knowledge and introduce best practises. However the theory also addressed certain

ethical issues or dilemmas. These issues are very much familiar with the accounting concepts

(Khan et al 2016).

The ethical issues addressed in this article define that in most of the cases the

accountant has been held responsible for the collapse of these companies. However cases like

Enron, WorldCom have occurred owing to the failure in maintaining the corporate ethics in

accounting (Strand 2014.). Therefore the recent Sarbanes- Oxley act has introduced certain

aspects to handle the accounting fraud from happening again. However all these cases have

affected the shareholders, parties and individuals. The share prices of this company have

ACCOUNTANTS IN THE PROFESSION

The study assignment provides information about three articles related to the

international federation of accountants (IFAC). The main focus of this process is to serve the

public interest, improve the accounting process and contribute to the overall development of

the organisation. Therefore the study topic describes three ethical dilemmas from three

articles. Apart from this how these ethical dilemmas can affect the individuals, stakeholders

and key organisations. These ethical issues can well affect the overall fundamental rights and

obligations related to these fundamental principles.

On the other hand in the second part, the study discusses about two sustainability

challenges which are affecting the overall process and how to cope up with these issues.

Discussion

PART A: Ethical Dilemmas – Issues and Solutions

In the first article diversified role of the professional accountant in business have been

discussed by international federation of accountants. The overall mission of this process is to

serve the public interest, develop strong accounting connection between organisations,

industry, public and private sectors. Furthermore they always encourage the professionals to

develop knowledge and introduce best practises. However the theory also addressed certain

ethical issues or dilemmas. These issues are very much familiar with the accounting concepts

(Khan et al 2016).

The ethical issues addressed in this article define that in most of the cases the

accountant has been held responsible for the collapse of these companies. However cases like

Enron, WorldCom have occurred owing to the failure in maintaining the corporate ethics in

accounting (Strand 2014.). Therefore the recent Sarbanes- Oxley act has introduced certain

aspects to handle the accounting fraud from happening again. However all these cases have

affected the shareholders, parties and individuals. The share prices of this company have

2

ACCOUNTANTS IN THE PROFESSION

degraded to a massive amount. Thus ultimately the companies had to stop their operation.

Therefore from the first article it is seen that political parties always have approached the

business and contributed thereto. But federal governments have also supported to takeover

community projects rather than ensuring support to those parties. As per van Leuwen,

different sectors face different issues. Further there are the peoples from entry level who seek

to earn the accounting rules and regulations related to the ethics and integrity (Lozano 2015).

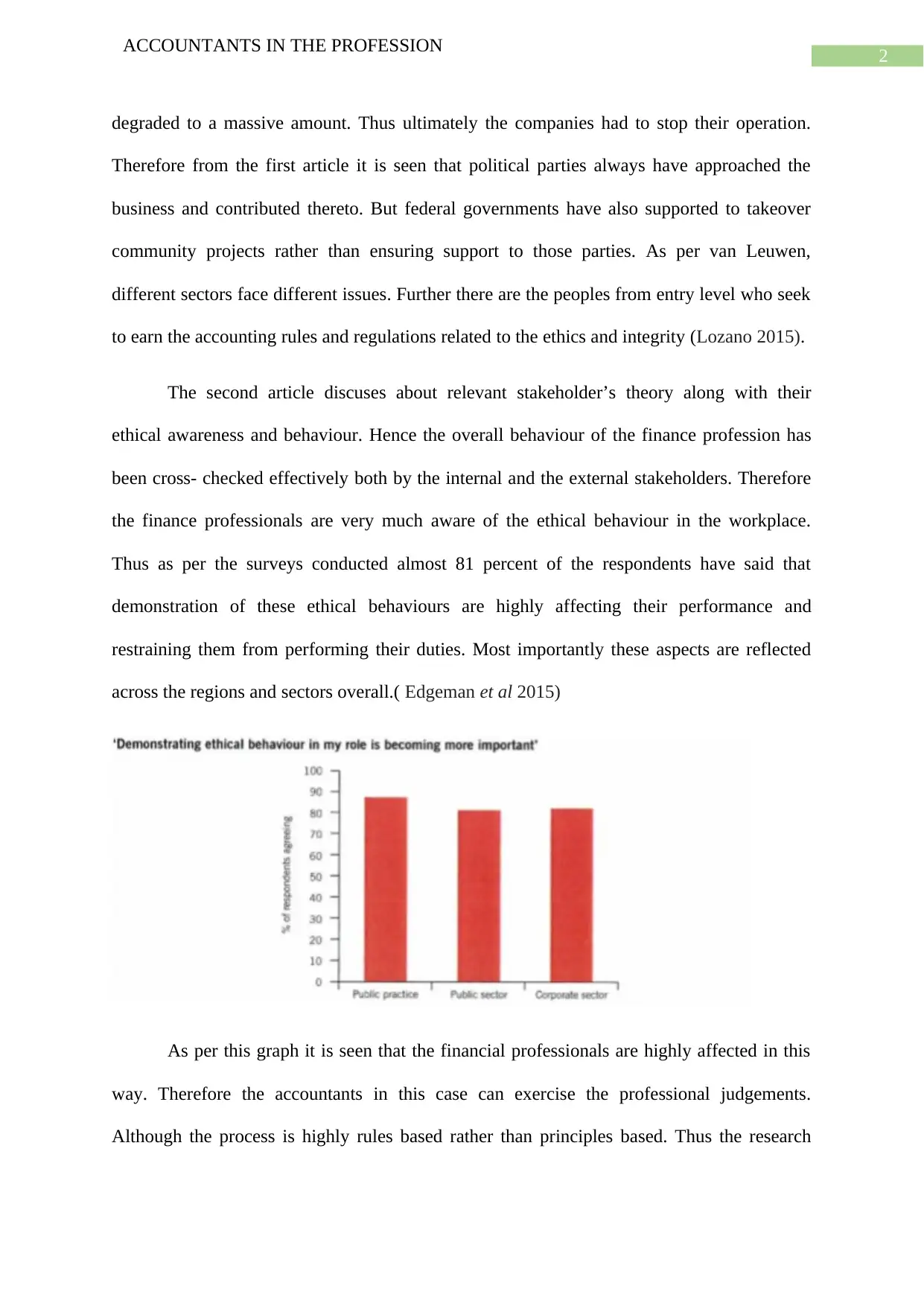

The second article discuses about relevant stakeholder’s theory along with their

ethical awareness and behaviour. Hence the overall behaviour of the finance profession has

been cross- checked effectively both by the internal and the external stakeholders. Therefore

the finance professionals are very much aware of the ethical behaviour in the workplace.

Thus as per the surveys conducted almost 81 percent of the respondents have said that

demonstration of these ethical behaviours are highly affecting their performance and

restraining them from performing their duties. Most importantly these aspects are reflected

across the regions and sectors overall.( Edgeman et al 2015)

As per this graph it is seen that the financial professionals are highly affected in this

way. Therefore the accountants in this case can exercise the professional judgements.

Although the process is highly rules based rather than principles based. Thus the research

ACCOUNTANTS IN THE PROFESSION

degraded to a massive amount. Thus ultimately the companies had to stop their operation.

Therefore from the first article it is seen that political parties always have approached the

business and contributed thereto. But federal governments have also supported to takeover

community projects rather than ensuring support to those parties. As per van Leuwen,

different sectors face different issues. Further there are the peoples from entry level who seek

to earn the accounting rules and regulations related to the ethics and integrity (Lozano 2015).

The second article discuses about relevant stakeholder’s theory along with their

ethical awareness and behaviour. Hence the overall behaviour of the finance profession has

been cross- checked effectively both by the internal and the external stakeholders. Therefore

the finance professionals are very much aware of the ethical behaviour in the workplace.

Thus as per the surveys conducted almost 81 percent of the respondents have said that

demonstration of these ethical behaviours are highly affecting their performance and

restraining them from performing their duties. Most importantly these aspects are reflected

across the regions and sectors overall.( Edgeman et al 2015)

As per this graph it is seen that the financial professionals are highly affected in this

way. Therefore the accountants in this case can exercise the professional judgements.

Although the process is highly rules based rather than principles based. Thus the research

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTANTS IN THE PROFESSION

suggests that the importance of existing sound professional judgements which could remain

and could turn out to be more important in the near future (Engert et al 2016.).

Further the focus is on the behaviour of accountants which could be heavily affective

to the management. Thus the focus is shaped on the fact that the financial stakeholders hold

interest in the financial interests in the overall financial performance of the organisations.

Thus the process has created wider and easier process to the stock markets. Thus it leads to

increase in the transparency to the business. Further in order to safeguard the interest a

response is collected to impose greater regulations and compliance to the financial activities

of the companies. Hence these regulations does not only restrain from the need to exercise the

overall professional judgement or to behave like an activate professional. Thus this topic

states that the increasing business complexity has continued to drive the force towards need

of accountants. Further effective judgement and overall transparency in this process.

Similarly there is also a need for the accountants to behave ethically and continue their

operation abiding the rules and responsibilities of the organisation. Further these findings

also state that the finance personals are not using their skills as effectively as they could have.

Therefore the training facility and intellectual ability of the accountants make those

judgements as one of the key assets. Furthermore the overall routine transaction oriented

tasks needs to be automated or otherwise can be assigned to the overall experienced

candidates (Benn et al.2014).

Apart from this aspect it can also be said that the implication of increased cross-

checking, high end user expectations and evolutions of the processes are also increasing the

pressures which the financial professionals are likely facing. Overall the surveys reveal that

almost 86 percent of the respondents have claimed that the overall increased demand are

putting pressure to the work finance undertaken within the company. Further 86 percent of

respondent had claimed that increasing pressures on the workplace are very much equivalent

ACCOUNTANTS IN THE PROFESSION

suggests that the importance of existing sound professional judgements which could remain

and could turn out to be more important in the near future (Engert et al 2016.).

Further the focus is on the behaviour of accountants which could be heavily affective

to the management. Thus the focus is shaped on the fact that the financial stakeholders hold

interest in the financial interests in the overall financial performance of the organisations.

Thus the process has created wider and easier process to the stock markets. Thus it leads to

increase in the transparency to the business. Further in order to safeguard the interest a

response is collected to impose greater regulations and compliance to the financial activities

of the companies. Hence these regulations does not only restrain from the need to exercise the

overall professional judgement or to behave like an activate professional. Thus this topic

states that the increasing business complexity has continued to drive the force towards need

of accountants. Further effective judgement and overall transparency in this process.

Similarly there is also a need for the accountants to behave ethically and continue their

operation abiding the rules and responsibilities of the organisation. Further these findings

also state that the finance personals are not using their skills as effectively as they could have.

Therefore the training facility and intellectual ability of the accountants make those

judgements as one of the key assets. Furthermore the overall routine transaction oriented

tasks needs to be automated or otherwise can be assigned to the overall experienced

candidates (Benn et al.2014).

Apart from this aspect it can also be said that the implication of increased cross-

checking, high end user expectations and evolutions of the processes are also increasing the

pressures which the financial professionals are likely facing. Overall the surveys reveal that

almost 86 percent of the respondents have claimed that the overall increased demand are

putting pressure to the work finance undertaken within the company. Further 86 percent of

respondent had claimed that increasing pressures on the workplace are very much equivalent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTANTS IN THE PROFESSION

to the overall accounting areas. Moreover 83 percent respondents have claimed that the

public figure could represent the discounted findings and the remedies related to the process.

Particularly the new productivity techniques could enforce new attractions rates and overall

productivity (Wolf 2014.).

Further as the roes of the accounting professionals change and then skills get to

evolve, further there is a gap between skills and the organisational skills sets. There are two

reasons on why such gap exists. This are-

A general shortage of professional accountants is seen currently.

The accountants do not meet the required skills to fill this gap.

The shortage of accountants is caused by a number of reasons.

Firstly there is a demographic shortage in many countries like Europe, North America

and other parts of Asia where there are fewer amounts of graduates. Therefore the companies

can face ethical issues if they select those candidates who do not possess the required

alignments. Hence this skill deficit can be effective to some extent to the big organisations.

Furthermore these skill deficiencies are considered as biggest problems. Treatments required

for the new legislations and to curb down booming economy by implementing new and

improved techniques (Baumgartner and Rauter 2017.).

ACCOUNTANTS IN THE PROFESSION

to the overall accounting areas. Moreover 83 percent respondents have claimed that the

public figure could represent the discounted findings and the remedies related to the process.

Particularly the new productivity techniques could enforce new attractions rates and overall

productivity (Wolf 2014.).

Further as the roes of the accounting professionals change and then skills get to

evolve, further there is a gap between skills and the organisational skills sets. There are two

reasons on why such gap exists. This are-

A general shortage of professional accountants is seen currently.

The accountants do not meet the required skills to fill this gap.

The shortage of accountants is caused by a number of reasons.

Firstly there is a demographic shortage in many countries like Europe, North America

and other parts of Asia where there are fewer amounts of graduates. Therefore the companies

can face ethical issues if they select those candidates who do not possess the required

alignments. Hence this skill deficit can be effective to some extent to the big organisations.

Furthermore these skill deficiencies are considered as biggest problems. Treatments required

for the new legislations and to curb down booming economy by implementing new and

improved techniques (Baumgartner and Rauter 2017.).

5

ACCOUNTANTS IN THE PROFESSION

Respond to the ethical challenges of ethics

Most of the accountants in the business and public sector face ethical dilemmas

during their professional careers. Hence these issues form in the way of supporting the

challenging complexities (Mass et al. 2016). Further the accountants may like to treat these

issues as business decisions rather not to utilise the professional codes to assess the potential

course of actions. Therefore the challenges faced in this case are as follows-

Ethical culture

The recent conducted survey has shown a 10 to 15 percent increase since 2008

relating to the ethical issues, training and provisions for hotlines, incentive makings and

rewards based on performance.

The corporate leadership is less activated and engaged in reviewing the organisational

performance. The corporate leaders held responsibility related to the business ethics. Thus the

leadership implies ethical operational culture related to the organisations.

Ethical accounting

The survey further shows that there is almost 20 percent increase in organisation by

further collecting the ethical information. Therefore the management feels that it is needful to

collect and analyse the ethical information.

Ethical issues and pressure

However due to the increase in the ethical codes, there is extreme pressure within the

organisations to act unethically. Thus pressure appears to be appearing for emerging

economics (Ioannou and Serafeim 2017).

ACCOUNTANTS IN THE PROFESSION

Respond to the ethical challenges of ethics

Most of the accountants in the business and public sector face ethical dilemmas

during their professional careers. Hence these issues form in the way of supporting the

challenging complexities (Mass et al. 2016). Further the accountants may like to treat these

issues as business decisions rather not to utilise the professional codes to assess the potential

course of actions. Therefore the challenges faced in this case are as follows-

Ethical culture

The recent conducted survey has shown a 10 to 15 percent increase since 2008

relating to the ethical issues, training and provisions for hotlines, incentive makings and

rewards based on performance.

The corporate leadership is less activated and engaged in reviewing the organisational

performance. The corporate leaders held responsibility related to the business ethics. Thus the

leadership implies ethical operational culture related to the organisations.

Ethical accounting

The survey further shows that there is almost 20 percent increase in organisation by

further collecting the ethical information. Therefore the management feels that it is needful to

collect and analyse the ethical information.

Ethical issues and pressure

However due to the increase in the ethical codes, there is extreme pressure within the

organisations to act unethically. Thus pressure appears to be appearing for emerging

economics (Ioannou and Serafeim 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTANTS IN THE PROFESSION

Business issues

The security information remains as the biggest issue of concern across all the market.

Thus the bribery has risen from the concerned issues. Therefore the anti-bribery and

corruption legislative process is formed.

However the IFAC members provide guidance, ethical resolution framework and

ways which can help the accountants deal with these issues.

A common aspect of guidance on resolving the ethical issues that can help the

accountants define and apply for the principles related to the professional code of ethics.

Therefore these ethical issues can act for the beneficiaries of public interest and professional

ethics. It places expectation to the accountants so that they can regulate the process by their

own.

This ethical issues are broadly threatened by the range of circumstances, self –

review, familiarity, advocacy etc.

There are certain threats which are faced by the professional accountants in this

regard. These are as follows-

Self-interest

As per the article these kind of threat occurs if any financial matter occurring in the

organisation goes against the interest of these professional accountants. Further these closed

family member interest is another process which sometimes faced by the professional

accountants. For example having a close relationship with the clients can be considered here

(Siew 2015).

ACCOUNTANTS IN THE PROFESSION

Business issues

The security information remains as the biggest issue of concern across all the market.

Thus the bribery has risen from the concerned issues. Therefore the anti-bribery and

corruption legislative process is formed.

However the IFAC members provide guidance, ethical resolution framework and

ways which can help the accountants deal with these issues.

A common aspect of guidance on resolving the ethical issues that can help the

accountants define and apply for the principles related to the professional code of ethics.

Therefore these ethical issues can act for the beneficiaries of public interest and professional

ethics. It places expectation to the accountants so that they can regulate the process by their

own.

This ethical issues are broadly threatened by the range of circumstances, self –

review, familiarity, advocacy etc.

There are certain threats which are faced by the professional accountants in this

regard. These are as follows-

Self-interest

As per the article these kind of threat occurs if any financial matter occurring in the

organisation goes against the interest of these professional accountants. Further these closed

family member interest is another process which sometimes faced by the professional

accountants. For example having a close relationship with the clients can be considered here

(Siew 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTANTS IN THE PROFESSION

Self- review

This situation occurs if a previous financial report is re- evaluated by the professional

accountants. Therefore if a professional accountant is held responsible for this judgement,

then these kinds of threats may come into existence. For example- reporting of the financial

system after involving the implementation.

Threat of advocacy

This kind of situation occurs in case of the professional accountants, if they

compromise the opinion of the extensive position relating to the financial manner. Therefore

the professional accountant has the opportunity to argue for previous financial position. For

example listing shares for promoting an entity and later on the entity is found to be guilty for

using the statements of his clients (Peters and Romi 2014).

Familiarity threat

It is another situation which is often faced by the professional accountant. Thus as per

IFAC guidelines the accountants are seem to be sympathetic to their close relatives who are

quite used to this process. For this case the professional accounts needs to be favourable to its

close members. For example an employee is in the position to exercise the overall influence

over the subject matter of this engagement (Ihlen and Rope 2014.).

Threat to intimidation

Lastly the intimidation threat is also considered in this aspect. For this aspect the

professional accountants may think about some kind of threats which are directing affecting

the achievements of the company in a negative way. However this situation may or may not

affect the professional accountants, but surely it is a threat to the company accountants. For

example the dismissal in related to the client engagement (Formentini and Taticchi 2016)

ACCOUNTANTS IN THE PROFESSION

Self- review

This situation occurs if a previous financial report is re- evaluated by the professional

accountants. Therefore if a professional accountant is held responsible for this judgement,

then these kinds of threats may come into existence. For example- reporting of the financial

system after involving the implementation.

Threat of advocacy

This kind of situation occurs in case of the professional accountants, if they

compromise the opinion of the extensive position relating to the financial manner. Therefore

the professional accountant has the opportunity to argue for previous financial position. For

example listing shares for promoting an entity and later on the entity is found to be guilty for

using the statements of his clients (Peters and Romi 2014).

Familiarity threat

It is another situation which is often faced by the professional accountant. Thus as per

IFAC guidelines the accountants are seem to be sympathetic to their close relatives who are

quite used to this process. For this case the professional accounts needs to be favourable to its

close members. For example an employee is in the position to exercise the overall influence

over the subject matter of this engagement (Ihlen and Rope 2014.).

Threat to intimidation

Lastly the intimidation threat is also considered in this aspect. For this aspect the

professional accountants may think about some kind of threats which are directing affecting

the achievements of the company in a negative way. However this situation may or may not

affect the professional accountants, but surely it is a threat to the company accountants. For

example the dismissal in related to the client engagement (Formentini and Taticchi 2016)

8

ACCOUNTANTS IN THE PROFESSION

Safeguards to these issues

Internal conflicts

The internal conflicts are directly related to the accounting policies and procedures.

Therefore some measurements needs to be taken in this case. These are as follows-

The accountants need to take advices from the employer, professional entities or other

professional advisors who are associated with this field for a long time.

The employer is providing a formal disruptive resolution process(Grimm et al 2016).

Lastly the accountant’s needs to ensure that the advices they are getting are legal

(Bansal and Song 2017).

Reporting of information

Accountants must prepare the information fairly and with honesty. However the

accountants can be sued for providing misleading information. Therefore the accountants can

keep themselves safe in the way of –

Accountants can consult with the seniors of the company to resolve any issue.

Consulting with the governing body is also a good option for them.

The professional governing bodies can also be helpful to resolve problems.

Keeping confidential information

There are often some information’s which are kept confidential by the company

officials. These information’s are only accessible from the end of employees. Further the

accountant may be in a lot of pressure to disclose those information as a compliance with the

legal process such as anti- money laundering or act of terrorism. Thus these conflicting

situation could create a bad situation for the professional accountants. Therefore in order to

ACCOUNTANTS IN THE PROFESSION

Safeguards to these issues

Internal conflicts

The internal conflicts are directly related to the accounting policies and procedures.

Therefore some measurements needs to be taken in this case. These are as follows-

The accountants need to take advices from the employer, professional entities or other

professional advisors who are associated with this field for a long time.

The employer is providing a formal disruptive resolution process(Grimm et al 2016).

Lastly the accountant’s needs to ensure that the advices they are getting are legal

(Bansal and Song 2017).

Reporting of information

Accountants must prepare the information fairly and with honesty. However the

accountants can be sued for providing misleading information. Therefore the accountants can

keep themselves safe in the way of –

Accountants can consult with the seniors of the company to resolve any issue.

Consulting with the governing body is also a good option for them.

The professional governing bodies can also be helpful to resolve problems.

Keeping confidential information

There are often some information’s which are kept confidential by the company

officials. These information’s are only accessible from the end of employees. Further the

accountant may be in a lot of pressure to disclose those information as a compliance with the

legal process such as anti- money laundering or act of terrorism. Thus these conflicting

situation could create a bad situation for the professional accountants. Therefore in order to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTANTS IN THE PROFESSION

solve this issue, the management needs to disclose the information complying with relevant

stakeholder theory, money laundering and other regulations (Klettner et al 2014).

Whistle blowing

Whistle blowing in auditing is an aspect which is given negative social attributes to

the whistle blowers and informers. This in general can be more harmful to the professions

and other individual practitioners. Therefore a recent published general purpose definition of

whistle blowing is provided. It states that it is a disclosure which expresses ethical dilemma

of diversified loyalty. This is highly related to the property rights of the organisation. Further

it also argues that the internal audit disclosures which are arising from these dominant

external statutory audit does not qualify as the case maybe.

PART B: Sustainability – Challenges and Solutions

The sustainability reporting is one of the most important topics currently. Almost each

and every company tries to implement sustainability accounting within the companies.

Further in attention to the social, environmental and the other economic factors relating to

business performance will be increasing from the investors, accountants, governments,

customers and the society in general. Therefore as a result the professional accountants in the

business will be taking an active part in implementing sustainability in the business. Thus

tom help the business, the professional accountants and IFAC committee have published two

different report where the information’s are kept.

Therefore in the first article the interview conducted from senior accountants

associated with various enterprise around the world have imposed new challenges in

promoting and implementing the sustainable developmental strategies. Thus it can be said

that the sustainability will vary based on the organisation employed according to the nature of

ACCOUNTANTS IN THE PROFESSION

solve this issue, the management needs to disclose the information complying with relevant

stakeholder theory, money laundering and other regulations (Klettner et al 2014).

Whistle blowing

Whistle blowing in auditing is an aspect which is given negative social attributes to

the whistle blowers and informers. This in general can be more harmful to the professions

and other individual practitioners. Therefore a recent published general purpose definition of

whistle blowing is provided. It states that it is a disclosure which expresses ethical dilemma

of diversified loyalty. This is highly related to the property rights of the organisation. Further

it also argues that the internal audit disclosures which are arising from these dominant

external statutory audit does not qualify as the case maybe.

PART B: Sustainability – Challenges and Solutions

The sustainability reporting is one of the most important topics currently. Almost each

and every company tries to implement sustainability accounting within the companies.

Further in attention to the social, environmental and the other economic factors relating to

business performance will be increasing from the investors, accountants, governments,

customers and the society in general. Therefore as a result the professional accountants in the

business will be taking an active part in implementing sustainability in the business. Thus

tom help the business, the professional accountants and IFAC committee have published two

different report where the information’s are kept.

Therefore in the first article the interview conducted from senior accountants

associated with various enterprise around the world have imposed new challenges in

promoting and implementing the sustainable developmental strategies. Thus it can be said

that the sustainability will vary based on the organisation employed according to the nature of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTANTS IN THE PROFESSION

the job. Thus the significant agreement between the processes regarding this field will be

helping to implement and exercise their job roles in a positive way.

Furthermore these two articles will be helpful to promote the professional accounting.

Since in the current era, sustainability is an important topic, therefore it will help to increase

agendas of the business. Therefore the aim of this aspect is develop and exchange the

knowledge and other best practises. The IFAC is a worldwide organisation that deals with

professional accounting in order to serve public interest by strengthening the profession and

contributing towards the overall development of the business. Through the help of accounting

bodies serving for the sake of public interest, education, government service, industry and

commerce overall. In this way they ensure corporate sustainability and ethics by maintaining

the performance relating to the professional standard.

Therefore there are certain sustainability challenges which are directly related.

Sustainability in professional accounting is major step. Therefore the corporate are

highly responsible to enforce sustainability within the accounting. These includes risk

management, capital productivity innovation and growth.

Thus as per the overall sustainability business reporting related to the upcoming

challenges and solutions, it can be said that finance takes a greater part for protecting and

strengthening the foundations for a long term process. Since it is related to the companies, the

rise in such reporting will directly affect the company stakeholders seeking more information

from the business and respond to the social matters. Further the customers make decisions on

how the environmentally and friendly economical companies are. Apart from this the

investors are serious about the company’s sustainability and expect that they will cut cost

when needed. Thus the main benefits are discussed below-

ACCOUNTANTS IN THE PROFESSION

the job. Thus the significant agreement between the processes regarding this field will be

helping to implement and exercise their job roles in a positive way.

Furthermore these two articles will be helpful to promote the professional accounting.

Since in the current era, sustainability is an important topic, therefore it will help to increase

agendas of the business. Therefore the aim of this aspect is develop and exchange the

knowledge and other best practises. The IFAC is a worldwide organisation that deals with

professional accounting in order to serve public interest by strengthening the profession and

contributing towards the overall development of the business. Through the help of accounting

bodies serving for the sake of public interest, education, government service, industry and

commerce overall. In this way they ensure corporate sustainability and ethics by maintaining

the performance relating to the professional standard.

Therefore there are certain sustainability challenges which are directly related.

Sustainability in professional accounting is major step. Therefore the corporate are

highly responsible to enforce sustainability within the accounting. These includes risk

management, capital productivity innovation and growth.

Thus as per the overall sustainability business reporting related to the upcoming

challenges and solutions, it can be said that finance takes a greater part for protecting and

strengthening the foundations for a long term process. Since it is related to the companies, the

rise in such reporting will directly affect the company stakeholders seeking more information

from the business and respond to the social matters. Further the customers make decisions on

how the environmentally and friendly economical companies are. Apart from this the

investors are serious about the company’s sustainability and expect that they will cut cost

when needed. Thus the main benefits are discussed below-

11

ACCOUNTANTS IN THE PROFESSION

Risk and uncertainty in technological innovation

The public sector organisations in the accounting and finance filed is acting on the

behalf of community. Further they can accept projects in the private sectors also. Since more

amount of capital is involved, therefore project duration is also high. Risks are also high at

the same time. The new process discovers and invents new technologies for a clean and safe

accounting and production process. These circumstances encourage the development of the

sustainability accounting in public sector accounting.

Again on the other hand the process which are developed by the accountants

introduce the accounting systems which provides information about certain ecological and

other social risks simultaneously. Thus such measures may be recorded in the physical terms.

Considering an example of this case will be of Australia where half of the accountants are

trying tom implement new ways so that the sustainability reporting becomes easy to describe.

It further assesses the ecological benefits, possible risks and the other factors related to the

business and sustainability accounting.

Solutions

Provide accurate information

The accountants can help to improve the company communications with its

stakeholders by innovating the overall process. For example use of integrative reporting

framework for disclosing the relevant financial and non- financial reporting standard.

Therefore this involves focusing on the matters by linking the financial aspects.

New public management and financial sustainability

The articles further provide insights on new public management and financial

sustainability accounting within the business. The new pubic management has brought

ACCOUNTANTS IN THE PROFESSION

Risk and uncertainty in technological innovation

The public sector organisations in the accounting and finance filed is acting on the

behalf of community. Further they can accept projects in the private sectors also. Since more

amount of capital is involved, therefore project duration is also high. Risks are also high at

the same time. The new process discovers and invents new technologies for a clean and safe

accounting and production process. These circumstances encourage the development of the

sustainability accounting in public sector accounting.

Again on the other hand the process which are developed by the accountants

introduce the accounting systems which provides information about certain ecological and

other social risks simultaneously. Thus such measures may be recorded in the physical terms.

Considering an example of this case will be of Australia where half of the accountants are

trying tom implement new ways so that the sustainability reporting becomes easy to describe.

It further assesses the ecological benefits, possible risks and the other factors related to the

business and sustainability accounting.

Solutions

Provide accurate information

The accountants can help to improve the company communications with its

stakeholders by innovating the overall process. For example use of integrative reporting

framework for disclosing the relevant financial and non- financial reporting standard.

Therefore this involves focusing on the matters by linking the financial aspects.

New public management and financial sustainability

The articles further provide insights on new public management and financial

sustainability accounting within the business. The new pubic management has brought

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.