Accounting 3020: Solved Form 8949 for Capital Gains & Losses

VerifiedAdded on 2023/06/11

|2

|1351

|467

Homework Assignment

AI Summary

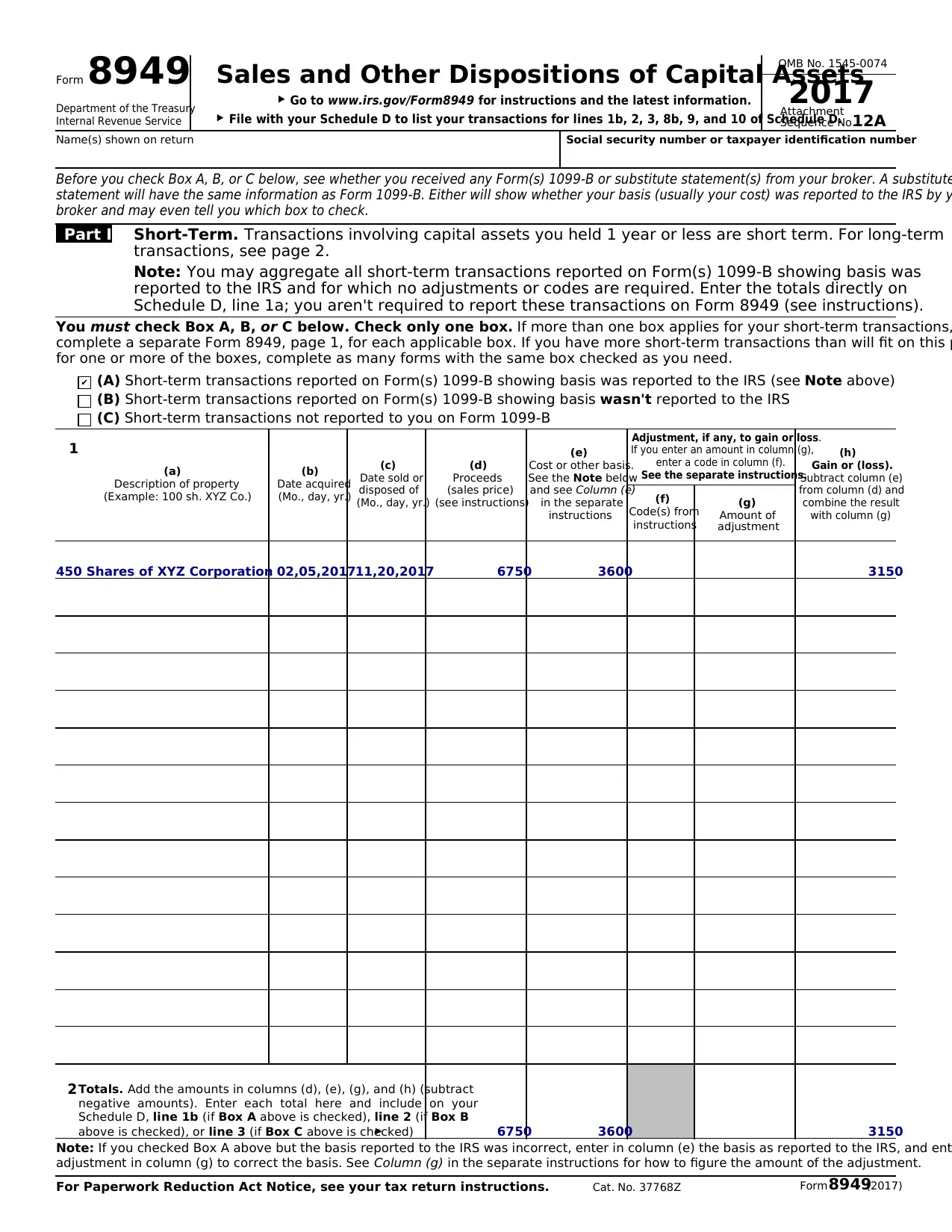

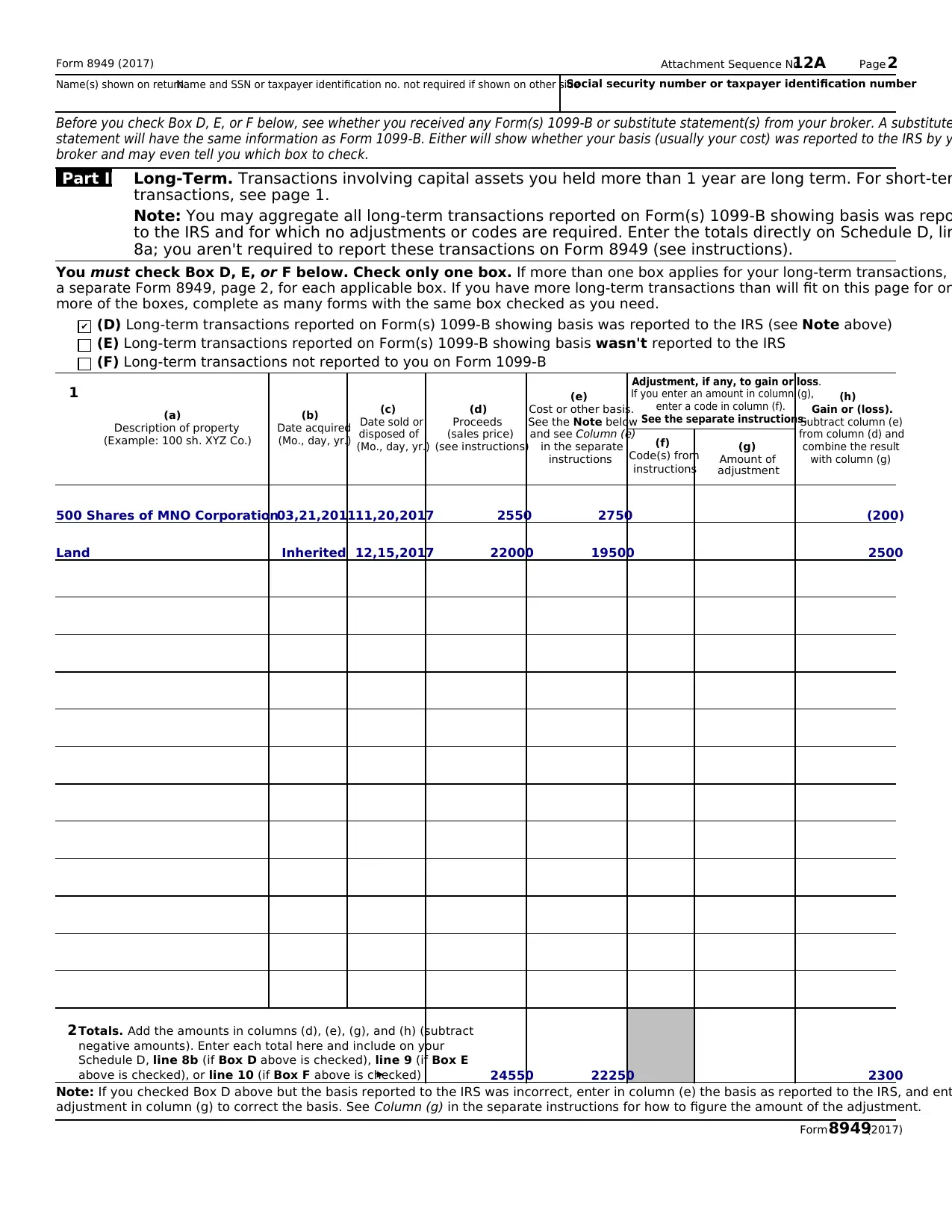

This document presents a solved Form 8949, which is used to report capital gains and losses from the sale or exchange of capital assets. The form is divided into two parts: Part I for short-term transactions (assets held for one year or less) and Part II for long-term transactions (assets held for more than one year). The example includes transactions involving the sale of XYZ Corporation shares (short-term) and MNO Corporation shares and inherited land (long-term). The document demonstrates how to calculate the gain or loss for each transaction, taking into account the proceeds from the sale, the cost basis of the asset, and any adjustments. The totals from each part are then calculated and would be reported on Schedule D of Form 1040. The assignment is related to Accounting 3020 and the Summer 2018 semester.

1 out of 2

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.