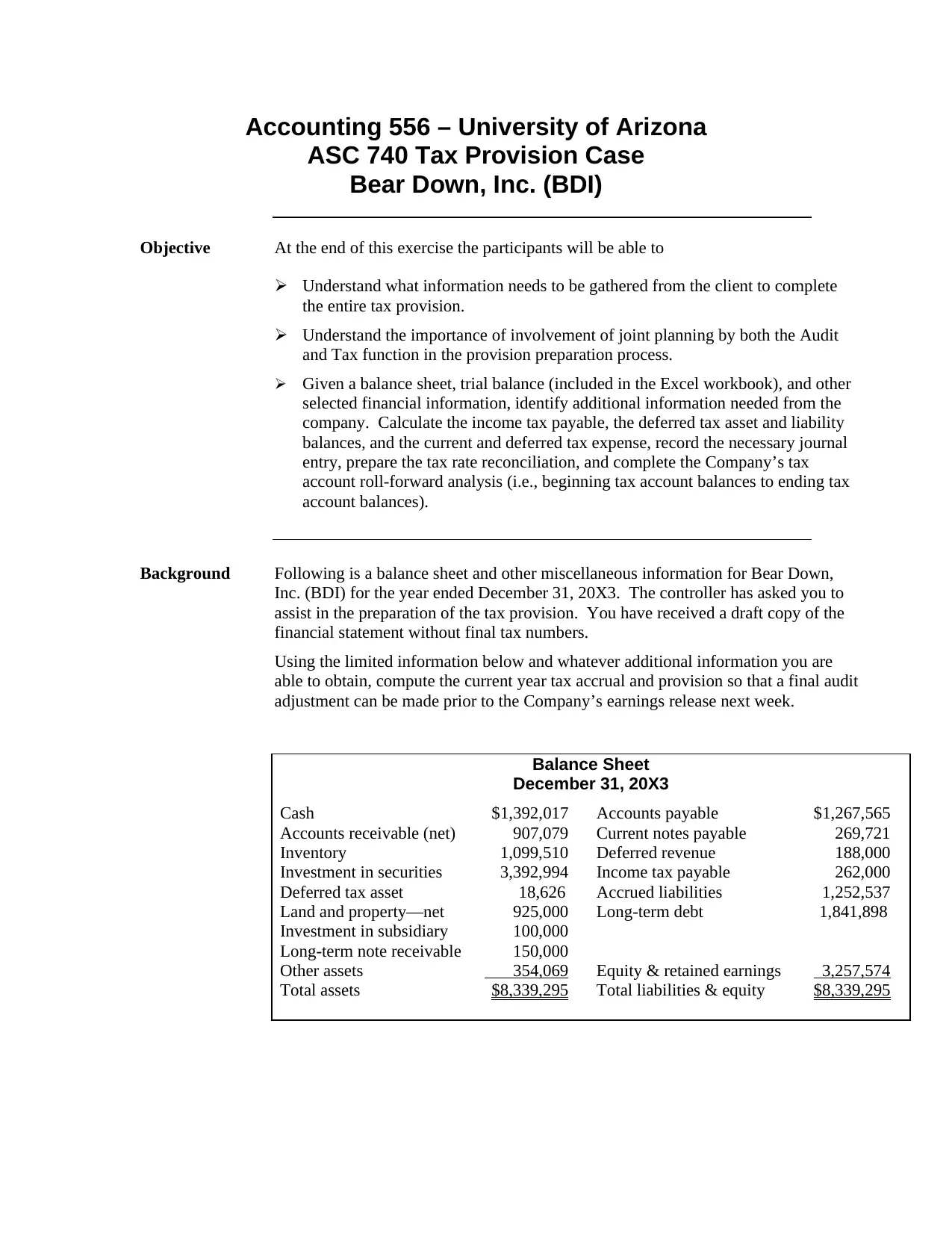

Accounting 556 Tax Provision Case

VerifiedAdded on 2019/10/09

|3

|1042

|84

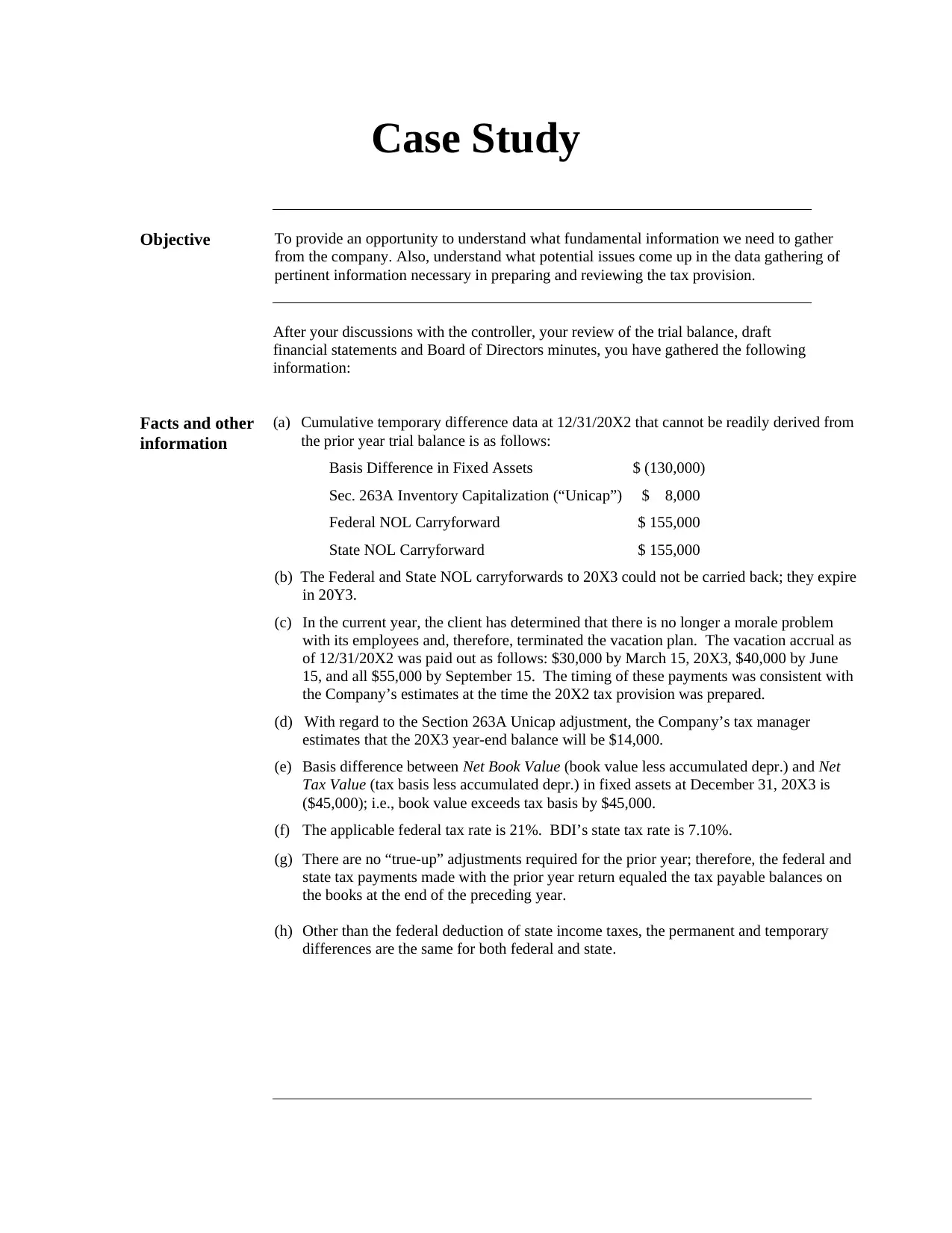

Case Study

AI Summary

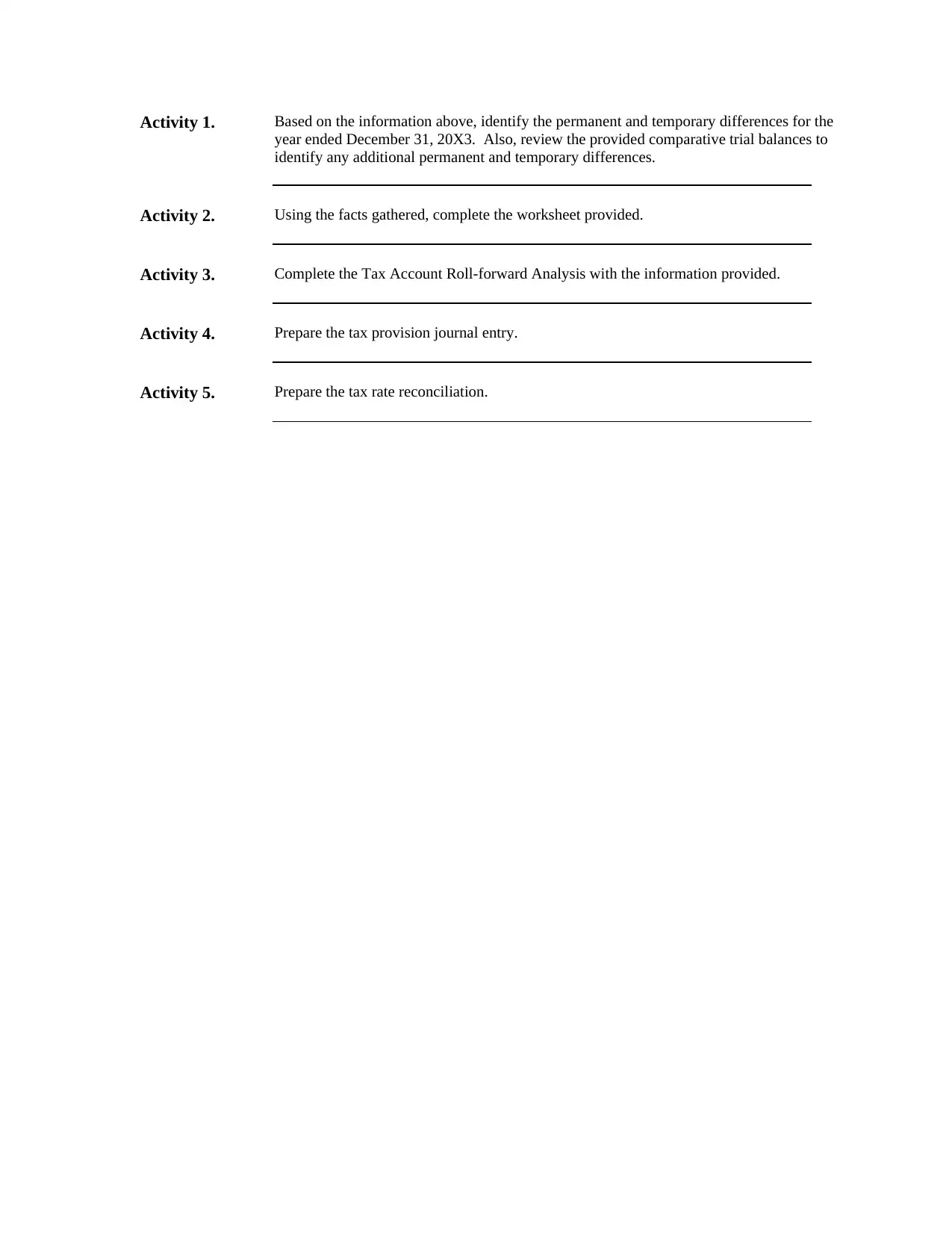

This case study, part of Accounting 556 at the University of Arizona, challenges students to prepare a tax provision for Bear Down, Inc. (BDI). Students are given a balance sheet, trial balance, and other financial information for BDI for the year ended December 31, 20X3. The case requires students to identify additional information needed from the company, calculate the income tax payable, deferred tax assets and liabilities, and current and deferred tax expenses. Furthermore, students must record the necessary journal entry, prepare the tax rate reconciliation, and complete the company's tax account roll-forward analysis. The case includes activities focusing on identifying permanent and temporary differences, completing worksheets and tax account roll-forward analysis, preparing the tax provision journal entry, and preparing the tax rate reconciliation. The case provides a realistic scenario for students to apply their knowledge of tax accounting principles.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.