ACCT6003 - Financial Accounting: Non-Current Assets, AASB 138 Analysis

VerifiedAdded on 2023/06/09

|11

|1007

|261

Report

AI Summary

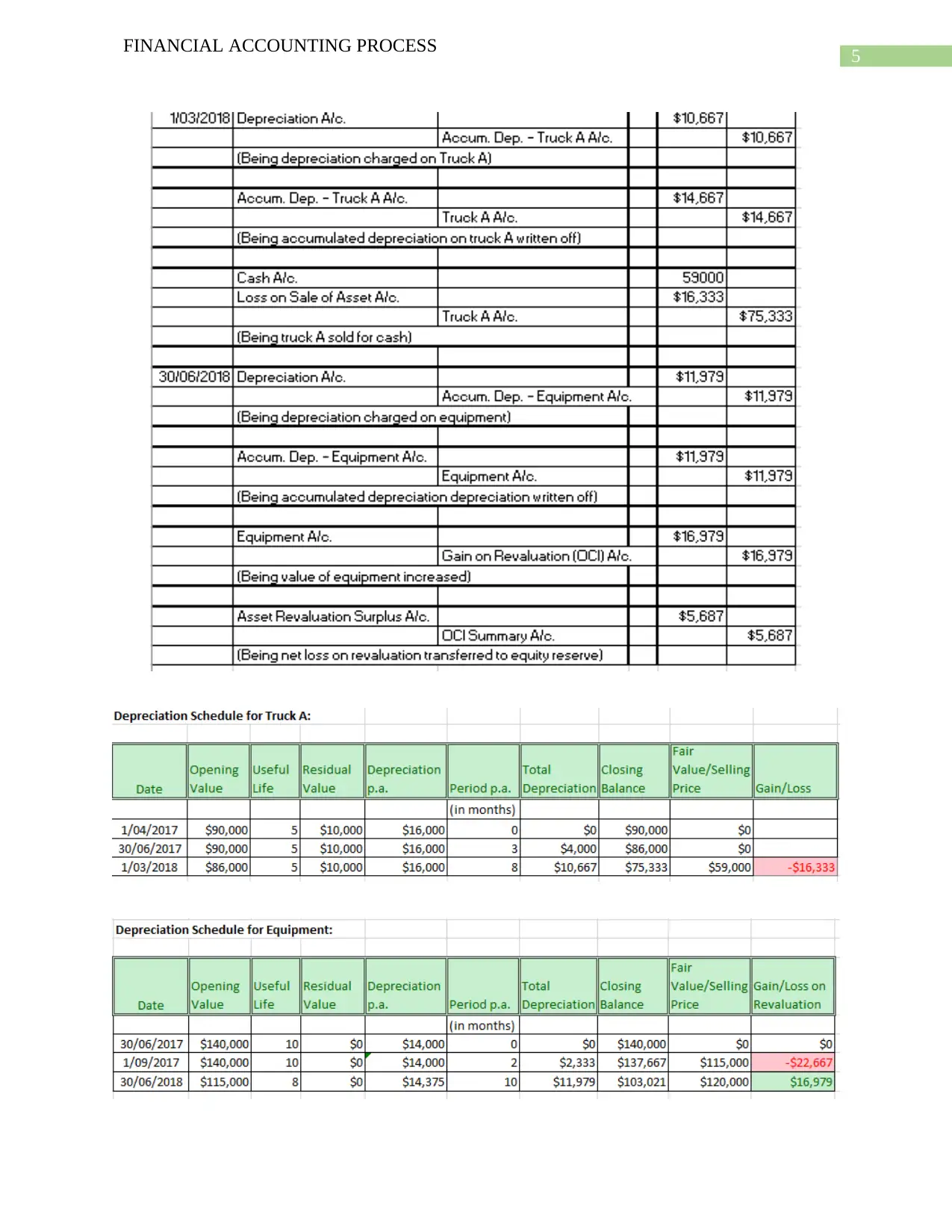

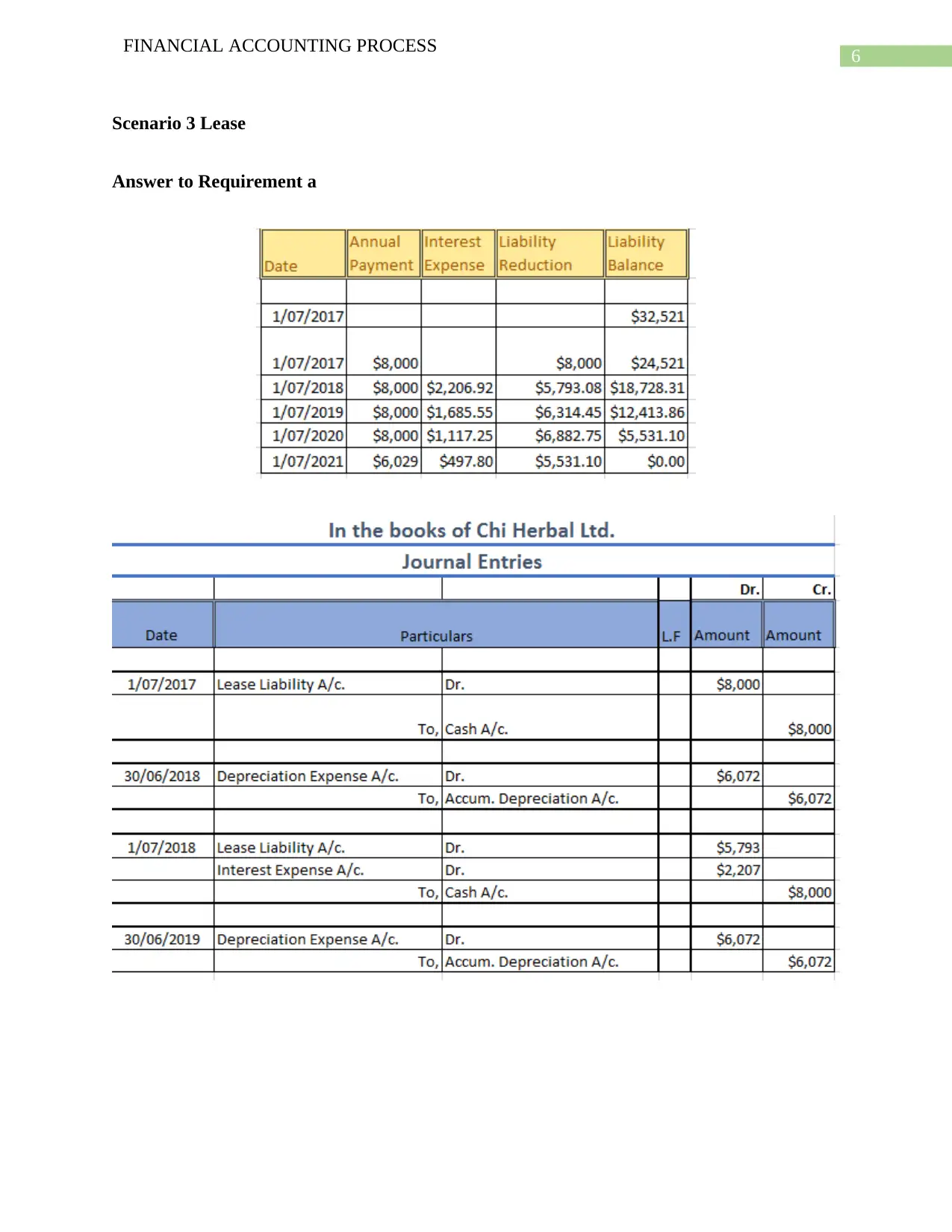

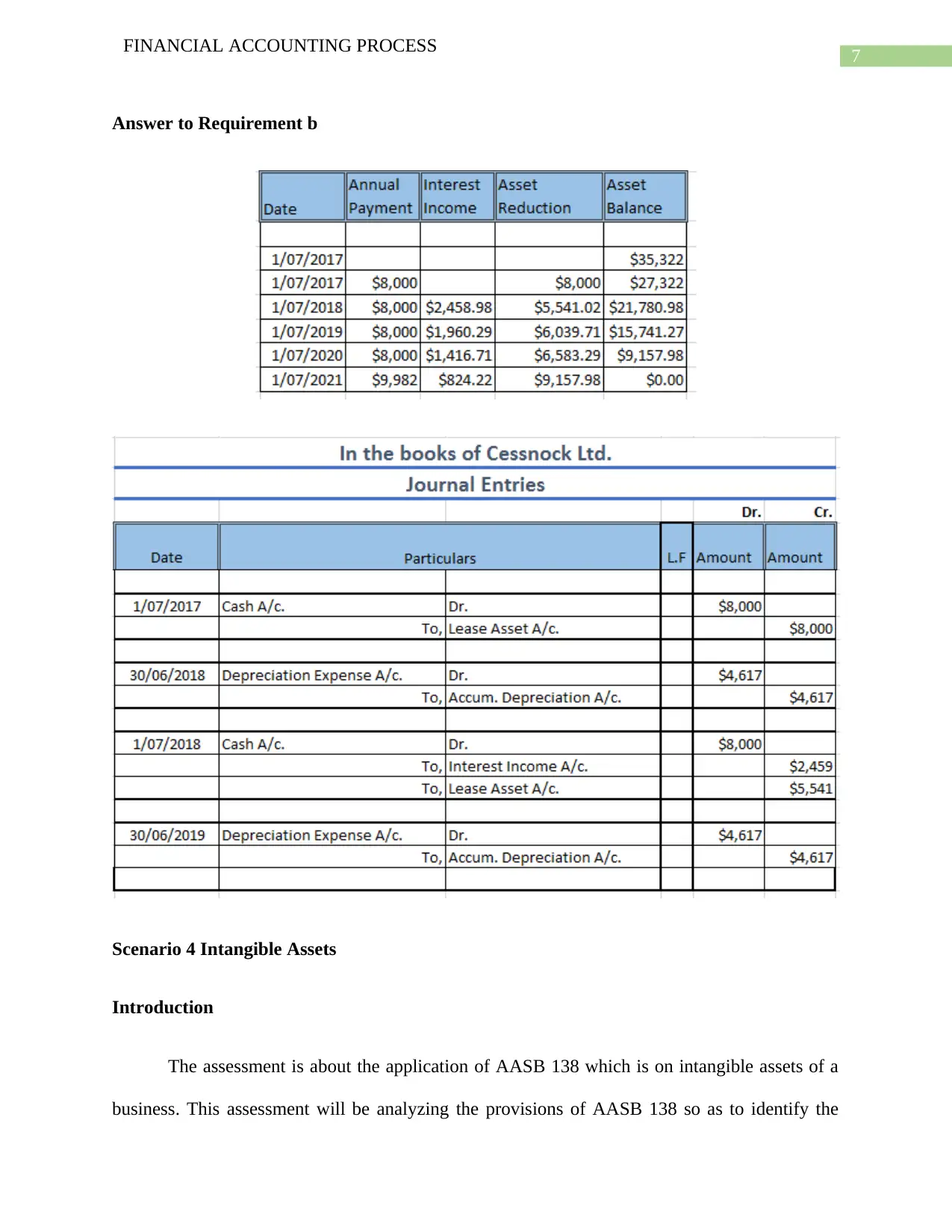

This report provides an analysis of financial accounting processes, focusing on the application of AASB 138 to intangible assets, particularly in the context of ChiHerbal Ltd. It discusses the identification and treatment of intangible assets, including the selective capitalization method for development expenditures. The report also touches upon property, plant, and equipment, lease accounting, and the distinction between development expenditure and expenses, offering a comprehensive overview of how AASB 138 guides the financial reporting of intangible assets and related expenses for businesses like ChiHerbal Ltd. Desklib provides similar solved assignments and resources for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.