Contemporary Issues in Accounting: AASB & Alexium International

VerifiedAdded on 2023/05/28

|12

|2212

|334

Report

AI Summary

This report provides an analysis of Alexium International Group Limited's financial statements in the context of the Australian Accounting Standards Board (AASB) conceptual framework. It examines the essential requirements, including recognition criteria for financial statement elements, and emphasizes the importance of adhering to the conceptual framework for transparency and uniformity. The report covers the company's overview, the objective of the conceptual framework, the fundamental and enhancing guidelines (relevance, verifiability, timeliness, and true representation), and the relationship between accounting research and professional practice. It concludes that following accounting guidelines is crucial for companies and stakeholders to understand business performance and make informed decisions, highlighting Alexium International Group Limited's adherence to relevant guidelines to enhance its performance.

CONTEMPORARY ISSUES IN ACCOUNTING

DECEMBER 12, 2018

SUBJECT TITLE _________

SUBJECT CODE _________

DECEMBER 12, 2018

SUBJECT TITLE _________

SUBJECT CODE _________

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The following work is aimed at shedding light on the conceptual framework of the AASB. In

addition it will analyse the various essential requirements such as the recognition criteria for

the elements of the financial statements. The assessment is based on the financial statements

of the company Alexium International Group Limited. The report backs that

conceptual framework is essential to abide by and brings transparency

and uniformity in the financial statements.

The following work is aimed at shedding light on the conceptual framework of the AASB. In

addition it will analyse the various essential requirements such as the recognition criteria for

the elements of the financial statements. The assessment is based on the financial statements

of the company Alexium International Group Limited. The report backs that

conceptual framework is essential to abide by and brings transparency

and uniformity in the financial statements.

Contents

INTRODUCTION......................................................................................................................2

OVERVIEW OF THE COMPANY...........................................................................................2

CONCEPTUAL FRAMEWORK OBJECTIVE-.......................................................................2

ESSENTIALITY OF FUNDAMENTAL AND ENHANCING GUIDELINES-......................4

RELEVANCE-.......................................................................................................................5

VERIFIABILITY...................................................................................................................5

TIMELESSNESS-..................................................................................................................5

TRUE REPRESENTATION-................................................................................................5

RECOGNITION CRITERIA.....................................................................................................5

RELATIONSHIP BETWEEN ACCOUNTING RESEARCH AND PROFESSIONAL

PRACTICE................................................................................................................................7

CONCLUSION-.........................................................................................................................8

INTRODUCTION......................................................................................................................2

OVERVIEW OF THE COMPANY...........................................................................................2

CONCEPTUAL FRAMEWORK OBJECTIVE-.......................................................................2

ESSENTIALITY OF FUNDAMENTAL AND ENHANCING GUIDELINES-......................4

RELEVANCE-.......................................................................................................................5

VERIFIABILITY...................................................................................................................5

TIMELESSNESS-..................................................................................................................5

TRUE REPRESENTATION-................................................................................................5

RECOGNITION CRITERIA.....................................................................................................5

RELATIONSHIP BETWEEN ACCOUNTING RESEARCH AND PROFESSIONAL

PRACTICE................................................................................................................................7

CONCLUSION-.........................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting refers to the process of recording, identifying and measuring the transactions and

the overall financial performance of an organisation. The process has to be compulsory

followed by the public companies, as required by the legal and regulatory framework, in the

interest of the stakeholders (Nobes, 2014). The accounting and financial reports are prepared

by the companies taking into account various guidelines, principles as laid down by the

accounting regulatory body to which the organisation belongs. These are the basic framework

for the preparation and presentation of the financial statements, which enable consistency and

comparability of the data referred therein. The report explores the various facets of the

accounting and financial reporting in relation to the company “Alexium International Group

Limited.” The report will shed light on the objective of the conceptual framework. In

addition, the report will also describe the recognition criteria, and the fundamental and

quality enhancement guidelines. The report will conclude with the description of the

relationship between the accounting research and the professional practice.

OVERVIEW OF THE COMPANY

The company Alexium International Group Limited, is a company engaged in the business of

development of chemical. The headquarters of the company are located in Australia.

Accordingly, the company is required to prepare its financial statements based on the

Australian Accounting Standards as pronounced by the Australian Accounting Standards

Board (AASB) and the Corporations Act 2001 (Cth).

CONCEPTUAL FRAMEWORK OBJECTIVE-

The conceptual framework can be described as the concepts or the purposes that leads to the

business to the set of standards in respect of preparing the good and proper report. The

conceptual framework suggests the better guidelines to every company in respect of making

reliable and comparable reports so that it can be simpler for shareholders of the corporation to

have the knowledge of the annual report of the corporation and relate it with other rival

company to reach over the end (Greenaway, Chan and Crossler, 2015).

In case of Alexium International Group Limited, it is found that this company has made the

annual reports with the help of conceptual framework. The Alexium International Group

Limited has followed proper guidelines and appropriate accounting standards to accumulate,

document, recognise, and evaluate the financial performance of the company. The company

Accounting refers to the process of recording, identifying and measuring the transactions and

the overall financial performance of an organisation. The process has to be compulsory

followed by the public companies, as required by the legal and regulatory framework, in the

interest of the stakeholders (Nobes, 2014). The accounting and financial reports are prepared

by the companies taking into account various guidelines, principles as laid down by the

accounting regulatory body to which the organisation belongs. These are the basic framework

for the preparation and presentation of the financial statements, which enable consistency and

comparability of the data referred therein. The report explores the various facets of the

accounting and financial reporting in relation to the company “Alexium International Group

Limited.” The report will shed light on the objective of the conceptual framework. In

addition, the report will also describe the recognition criteria, and the fundamental and

quality enhancement guidelines. The report will conclude with the description of the

relationship between the accounting research and the professional practice.

OVERVIEW OF THE COMPANY

The company Alexium International Group Limited, is a company engaged in the business of

development of chemical. The headquarters of the company are located in Australia.

Accordingly, the company is required to prepare its financial statements based on the

Australian Accounting Standards as pronounced by the Australian Accounting Standards

Board (AASB) and the Corporations Act 2001 (Cth).

CONCEPTUAL FRAMEWORK OBJECTIVE-

The conceptual framework can be described as the concepts or the purposes that leads to the

business to the set of standards in respect of preparing the good and proper report. The

conceptual framework suggests the better guidelines to every company in respect of making

reliable and comparable reports so that it can be simpler for shareholders of the corporation to

have the knowledge of the annual report of the corporation and relate it with other rival

company to reach over the end (Greenaway, Chan and Crossler, 2015).

In case of Alexium International Group Limited, it is found that this company has made the

annual reports with the help of conceptual framework. The Alexium International Group

Limited has followed proper guidelines and appropriate accounting standards to accumulate,

document, recognise, and evaluate the financial performance of the company. The company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

has made the financial statement of company according to the AASB rules. There are certain

examples of accounting and financial statement of company, which is made as per the

conceptual guidelines. These are as follows-

examples of accounting and financial statement of company, which is made as per the

conceptual guidelines. These are as follows-

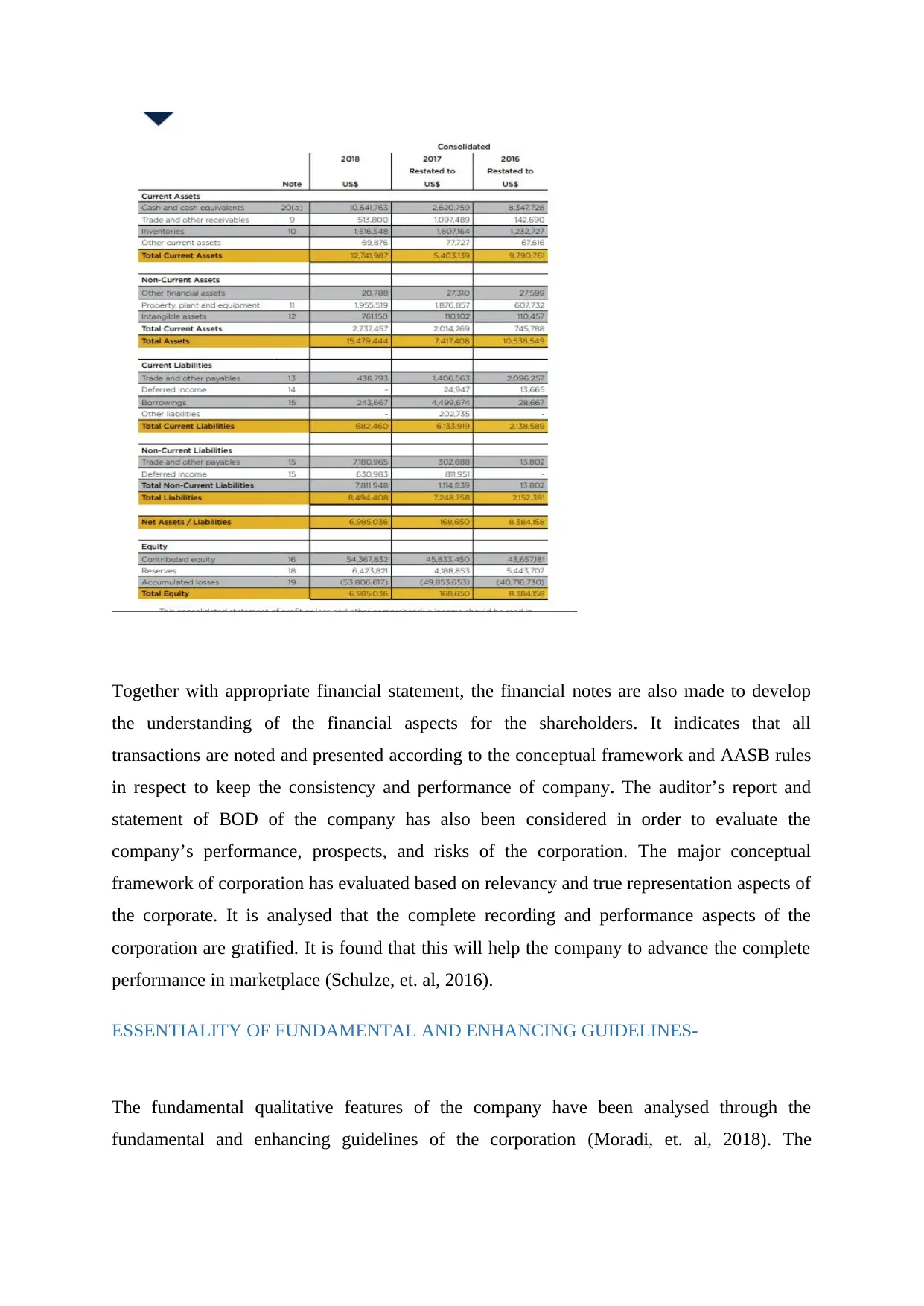

Together with appropriate financial statement, the financial notes are also made to develop

the understanding of the financial aspects for the shareholders. It indicates that all

transactions are noted and presented according to the conceptual framework and AASB rules

in respect to keep the consistency and performance of company. The auditor’s report and

statement of BOD of the company has also been considered in order to evaluate the

company’s performance, prospects, and risks of the corporation. The major conceptual

framework of corporation has evaluated based on relevancy and true representation aspects of

the corporate. It is analysed that the complete recording and performance aspects of the

corporation are gratified. It is found that this will help the company to advance the complete

performance in marketplace (Schulze, et. al, 2016).

ESSENTIALITY OF FUNDAMENTAL AND ENHANCING GUIDELINES-

The fundamental qualitative features of the company have been analysed through the

fundamental and enhancing guidelines of the corporation (Moradi, et. al, 2018). The

the understanding of the financial aspects for the shareholders. It indicates that all

transactions are noted and presented according to the conceptual framework and AASB rules

in respect to keep the consistency and performance of company. The auditor’s report and

statement of BOD of the company has also been considered in order to evaluate the

company’s performance, prospects, and risks of the corporation. The major conceptual

framework of corporation has evaluated based on relevancy and true representation aspects of

the corporate. It is analysed that the complete recording and performance aspects of the

corporation are gratified. It is found that this will help the company to advance the complete

performance in marketplace (Schulze, et. al, 2016).

ESSENTIALITY OF FUNDAMENTAL AND ENHANCING GUIDELINES-

The fundamental qualitative features of the company have been analysed through the

fundamental and enhancing guidelines of the corporation (Moradi, et. al, 2018). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fundamental and enhancing guidelines specify following features and its compliance in

business-

RELEVANCE-

The relevant data are capable to affect the judgements of the shareholders. The annual report

of Alexium International Group Limited states that the recording has stated in proper manner

by the corporation in the annual report so as to make good decisions by the shareholders of

the company (Yin and Kaynak, 2015).

VERIFIABILITY-

The Verifiability makes sure that all the information related to business have been truly

stated and it has authorised by the corporation. In the case of Alexium International Group

Limited, it is analysed that all information of the corporation have been authorised before

showing it in the company’s annual report.

TIMELESSNESS-

Timeliness shows to render all data to make decision timely in order to be capable to affect

the decision. By analysing the annual report of Alexium International Group Limited, it is

found that all data has timely stated in company’s annual report.

TRUE REPRESENTATION-

It is stated by the true representation that the financial performance and non-financial

performance in annual report should be stated with proof and fact so that shareholders can

found it true or realistic. All data and actions that have taken place in the corporation, are

required to be analysed and recorded in the company’s annual report. In the case of Alexium

International Group Limited, it is analysed that all the new developments, new processes, and

alterations in the companies have been defined in the company’s annual report concisely

(Lewandowski, 2016).

RECOGNITION CRITERIA

According to the paragraph 5.9 of the Conceptual Framework, a company should recognise

the assets and liabilities, income or expenses of the changes in equity as such (AASB, 2015).

business-

RELEVANCE-

The relevant data are capable to affect the judgements of the shareholders. The annual report

of Alexium International Group Limited states that the recording has stated in proper manner

by the corporation in the annual report so as to make good decisions by the shareholders of

the company (Yin and Kaynak, 2015).

VERIFIABILITY-

The Verifiability makes sure that all the information related to business have been truly

stated and it has authorised by the corporation. In the case of Alexium International Group

Limited, it is analysed that all information of the corporation have been authorised before

showing it in the company’s annual report.

TIMELESSNESS-

Timeliness shows to render all data to make decision timely in order to be capable to affect

the decision. By analysing the annual report of Alexium International Group Limited, it is

found that all data has timely stated in company’s annual report.

TRUE REPRESENTATION-

It is stated by the true representation that the financial performance and non-financial

performance in annual report should be stated with proof and fact so that shareholders can

found it true or realistic. All data and actions that have taken place in the corporation, are

required to be analysed and recorded in the company’s annual report. In the case of Alexium

International Group Limited, it is analysed that all the new developments, new processes, and

alterations in the companies have been defined in the company’s annual report concisely

(Lewandowski, 2016).

RECOGNITION CRITERIA

According to the paragraph 5.9 of the Conceptual Framework, a company should recognise

the assets and liabilities, income or expenses of the changes in equity as such (AASB, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This recognition must be capable of providing the stakeholders with the relevant financial

information, a true representation of the underlying transactions and the overall benefits of

provision of such information must exceed the cost of provision of such information. Thus, as

per the criteria of the recognition laid down by the conceptual framework text, if there is an

uncertainty in the existence of the asset or liability or in its separability form the goodwill, the

criteria of recognition is not met. In addition, when there is a low probability of the inflow or

outflow of the economic benefits form the asset or liability, it is not beneficial to recognise

the asset or liability in the financial statement.

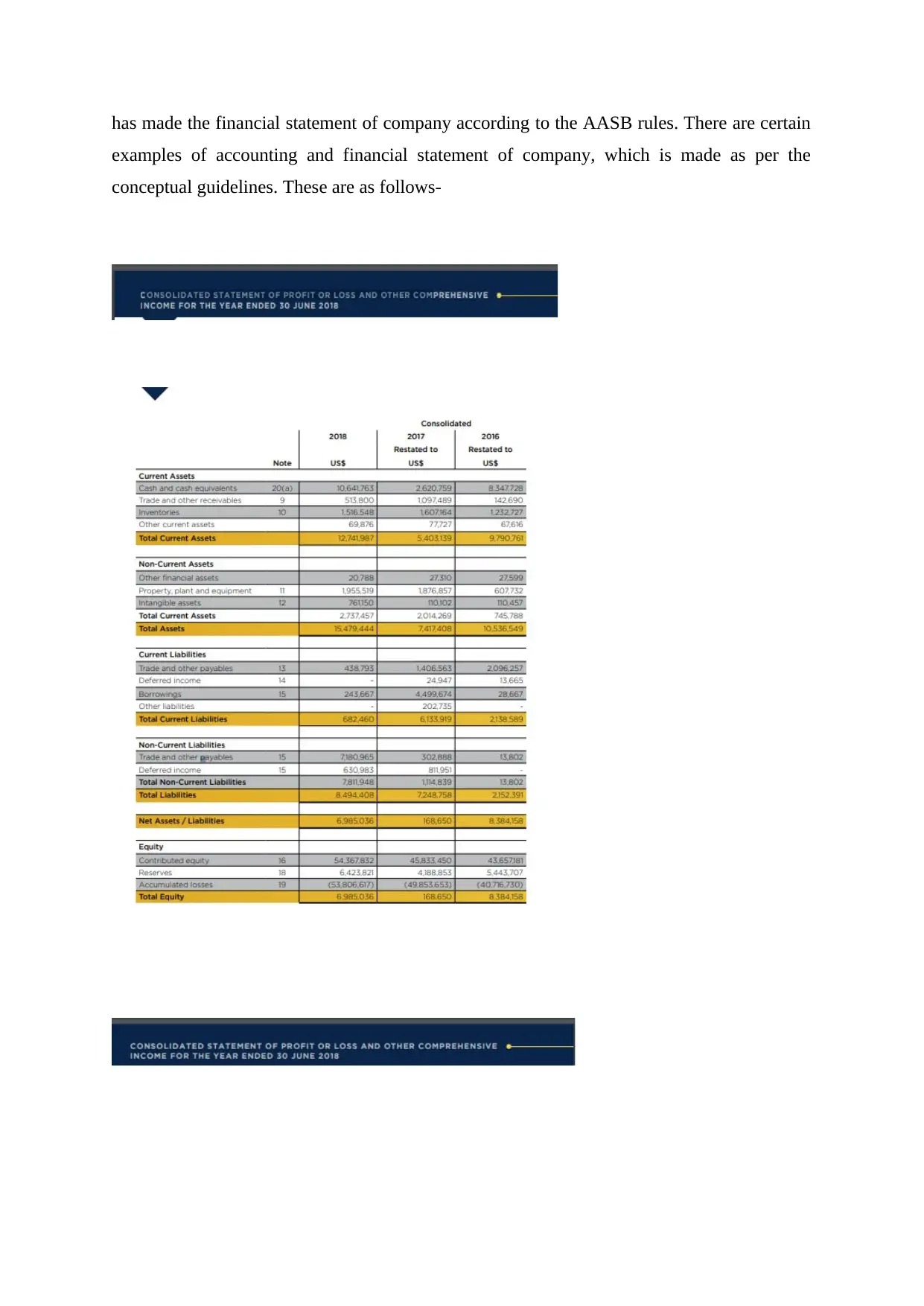

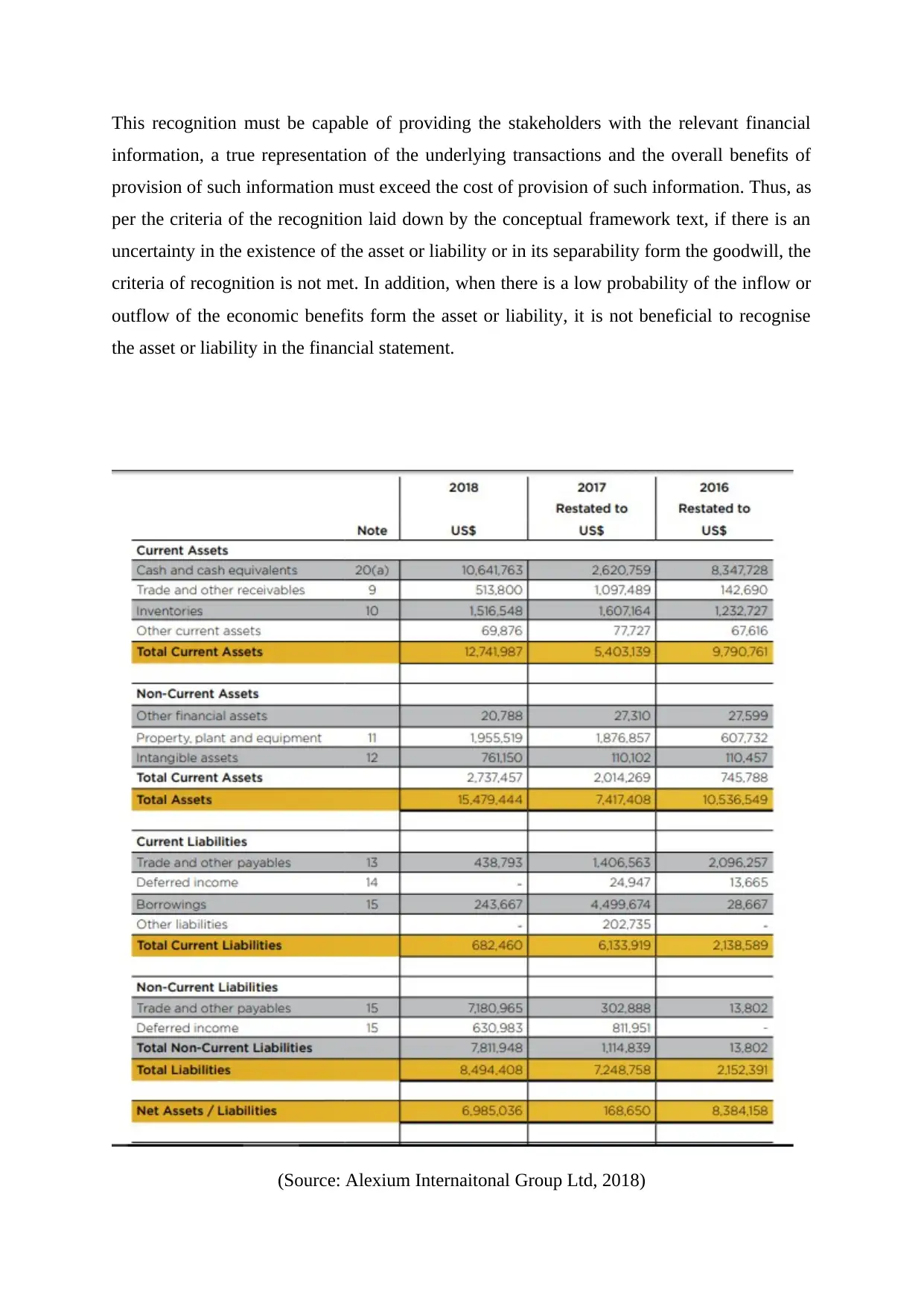

(Source: Alexium Internaitonal Group Ltd, 2018)

information, a true representation of the underlying transactions and the overall benefits of

provision of such information must exceed the cost of provision of such information. Thus, as

per the criteria of the recognition laid down by the conceptual framework text, if there is an

uncertainty in the existence of the asset or liability or in its separability form the goodwill, the

criteria of recognition is not met. In addition, when there is a low probability of the inflow or

outflow of the economic benefits form the asset or liability, it is not beneficial to recognise

the asset or liability in the financial statement.

(Source: Alexium Internaitonal Group Ltd, 2018)

In relation to the company Alexium International Group Ltd, the company has recognised

four major categories of the assets namely, the current assets, financial assets, property, plant,

and equipment, and the intangible assets. In addition, the liabilities are recognised as current

liabilities, and non-current liabilities including the deferred income. The amounts have been

depicted in the image above.

The above recognition is based on the guidelines on the recognition process as issued by the

AASB. The recognition of the assets and liabilities depicts the economic resources of the

entity and the claims. In addition, it enables the data to be comparable and understandable to

the stakeholders of the financial information. The recognition process aids in the

reconciliation of the opening and the closing values in the statements.

It must be noted that failure to recognise the items that meet the recognition criteria, as laid

down for the asset, liability, expense and income, may render the financial statements to be

incomplete. Thus, it is the judgement of the organisation’s management to decide whether an

item is worth the recognition or not, depending upon the amount, facts and circumstances in

each case. Further, it must be noted that sometimes an item meets the recognition criteria, but

is still not recognised in the financial statements, the disclosure for the same is required in the

notes to the financial statements. Thus, it can be stated that recognising an item of the

financial statement is essential.

RELATIONSHIP BETWEEN ACCOUNTING RESEARCH AND PROFESSIONAL

PRACTICE

Accounting research is a type of applied research. The focus of the study of the research is

that it is made up of the technologies and the practices, which are to be used, by the

management and the accounting practitioners in various social and organisational frameworks

(Parker, Guthrie and Linacre, 2011). The field of the research is agile. Therefore, the

practitioners must constantly update themselves with the latest pronouncements and

amendments, to make the statements legally acceptable and comparable in terms of the

industry stakeholders. Over the years, there have been constant gaps between the concerns of

the policy and framework formulators, practitioners and the academics; when it comes to the

need of the identification of the impact of the accounting study and the research, consistency

in the practices and social impact. Therefore in order to bring the uniformity in the same, the

regulatory bodies like AASB lays down the guidelines and principles for the preparation and

presentation of the financial statements. The company Alexium International Group Ltd has

four major categories of the assets namely, the current assets, financial assets, property, plant,

and equipment, and the intangible assets. In addition, the liabilities are recognised as current

liabilities, and non-current liabilities including the deferred income. The amounts have been

depicted in the image above.

The above recognition is based on the guidelines on the recognition process as issued by the

AASB. The recognition of the assets and liabilities depicts the economic resources of the

entity and the claims. In addition, it enables the data to be comparable and understandable to

the stakeholders of the financial information. The recognition process aids in the

reconciliation of the opening and the closing values in the statements.

It must be noted that failure to recognise the items that meet the recognition criteria, as laid

down for the asset, liability, expense and income, may render the financial statements to be

incomplete. Thus, it is the judgement of the organisation’s management to decide whether an

item is worth the recognition or not, depending upon the amount, facts and circumstances in

each case. Further, it must be noted that sometimes an item meets the recognition criteria, but

is still not recognised in the financial statements, the disclosure for the same is required in the

notes to the financial statements. Thus, it can be stated that recognising an item of the

financial statement is essential.

RELATIONSHIP BETWEEN ACCOUNTING RESEARCH AND PROFESSIONAL

PRACTICE

Accounting research is a type of applied research. The focus of the study of the research is

that it is made up of the technologies and the practices, which are to be used, by the

management and the accounting practitioners in various social and organisational frameworks

(Parker, Guthrie and Linacre, 2011). The field of the research is agile. Therefore, the

practitioners must constantly update themselves with the latest pronouncements and

amendments, to make the statements legally acceptable and comparable in terms of the

industry stakeholders. Over the years, there have been constant gaps between the concerns of

the policy and framework formulators, practitioners and the academics; when it comes to the

need of the identification of the impact of the accounting study and the research, consistency

in the practices and social impact. Therefore in order to bring the uniformity in the same, the

regulatory bodies like AASB lays down the guidelines and principles for the preparation and

presentation of the financial statements. The company Alexium International Group Ltd has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

prepared its statements according to the laid guidelines, which makes the statements uniform

and relevant.

CONCLUSION-

As per the above analysis, it can be concluded that the accounting report is made by the

companies by following the various accounting guidelines that creates it simpler for the

company and as well as stakeholders of the company to have knowledge of the business and

take proper decision in respect of the corporation. As per the study of AASB rules and

conceptual framework, it is found that the major purposes of all the accounting guidelines

and relevant policies are to render the true, substantial and the appropriate financial data to

the shareholders of the company so as to it could be easy to take proper and good decisions.

To conclude, the annual report of Alexium International Group Limited has made by focusing

on appropriate and relevant guidelines and point to handle and enhance the complete

performance of the company. In this way, it is clear that the policies related to conceptual

framework are necessarily required be adopted by each company to enhance the performance

of the company.

and relevant.

CONCLUSION-

As per the above analysis, it can be concluded that the accounting report is made by the

companies by following the various accounting guidelines that creates it simpler for the

company and as well as stakeholders of the company to have knowledge of the business and

take proper decision in respect of the corporation. As per the study of AASB rules and

conceptual framework, it is found that the major purposes of all the accounting guidelines

and relevant policies are to render the true, substantial and the appropriate financial data to

the shareholders of the company so as to it could be easy to take proper and good decisions.

To conclude, the annual report of Alexium International Group Limited has made by focusing

on appropriate and relevant guidelines and point to handle and enhance the complete

performance of the company. In this way, it is clear that the policies related to conceptual

framework are necessarily required be adopted by each company to enhance the performance

of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Alexium Internaitonal Group Ltd. (2018) Annual Report 2018 [online] Available from:

https://alexiuminternational.com/wp-content/uploads/2018/10/Alexium_Annual-

Report_October-2018_ASX.pdf [Accessed on 12 December 2018].

Australian Accounting Standards Board. (2015) Conceptual Framework for Financial

Reporting [online] Available from:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed on 12

December 2018].

Greenaway, K. E., Chan, Y. E., and Crossler, R.E. (2015) Company

information privacy orientation: a conceptual framework. Information

Systems Journal, 25(6), pp. 579-606.

Lewandowski, M. (2016) Designing the business models for circular

economy—Towards the conceptual framework. Sustainability, 8(1), p.43.

Moradi, M., Liu, L., Luchies, C., Patterson, M., and Darban, B. (2018)

Enhancing Teaching-Learning Effectiveness by Creating Online Interactive

Instructional Modules for Fundamental Concepts of Physics and

Mathematics. Education Sciences, 8(3), p. 109.

Nobes, C. (2014) International Classification of Financial Reporting. 3rd ed. UK: Routledge.

Parker, L., Guthrie, J. and Linacre, S. (2011) The relationship between academic accounting

research and professional practice. Accounting, Auditing & Accountability Journal, 24(1), pp.

5-14.

Schulze, M., Nehler, H., Ottosson, M., and Thollander, P. (2016) Energy

management in industry–a systematic review of previous findings and an

integrative conceptual framework. Journal of Cleaner Production, 112, pp.

3692-3708.

Alexium Internaitonal Group Ltd. (2018) Annual Report 2018 [online] Available from:

https://alexiuminternational.com/wp-content/uploads/2018/10/Alexium_Annual-

Report_October-2018_ASX.pdf [Accessed on 12 December 2018].

Australian Accounting Standards Board. (2015) Conceptual Framework for Financial

Reporting [online] Available from:

https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-15.pdf [Accessed on 12

December 2018].

Greenaway, K. E., Chan, Y. E., and Crossler, R.E. (2015) Company

information privacy orientation: a conceptual framework. Information

Systems Journal, 25(6), pp. 579-606.

Lewandowski, M. (2016) Designing the business models for circular

economy—Towards the conceptual framework. Sustainability, 8(1), p.43.

Moradi, M., Liu, L., Luchies, C., Patterson, M., and Darban, B. (2018)

Enhancing Teaching-Learning Effectiveness by Creating Online Interactive

Instructional Modules for Fundamental Concepts of Physics and

Mathematics. Education Sciences, 8(3), p. 109.

Nobes, C. (2014) International Classification of Financial Reporting. 3rd ed. UK: Routledge.

Parker, L., Guthrie, J. and Linacre, S. (2011) The relationship between academic accounting

research and professional practice. Accounting, Auditing & Accountability Journal, 24(1), pp.

5-14.

Schulze, M., Nehler, H., Ottosson, M., and Thollander, P. (2016) Energy

management in industry–a systematic review of previous findings and an

integrative conceptual framework. Journal of Cleaner Production, 112, pp.

3692-3708.

Yin, S., and Kaynak, O. (2015) Big data for modern industry: challenges

and trends [point of view]. Proceedings of the IEEE, 103(2), pp. 143-146.

and trends [point of view]. Proceedings of the IEEE, 103(2), pp. 143-146.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.