Report on Accounting Standards, AASB, and IFRS in Australia

VerifiedAdded on 2020/03/07

|10

|2613

|109

Report

AI Summary

This report provides a comprehensive overview of Australian accounting standards, focusing on the role of the Australian Accounting Standards Board (AASB) and the adoption of International Financial Reporting Standards (IFRS). It explores the importance of accounting standards in the corporate world, highlighting their role in standardizing financial reporting, enabling comparisons, and enhancing accountability. The report details the functions of the AASB, its standard-setting process, and its adoption of IFRS to increase the competitiveness of Australian entities. It also examines the impact of IFRS adoption on both profit and not-for-profit entities, including the amendments to AASB 116. The report further discusses the challenges and benefits of adopting IFRS globally, particularly in developing countries, and the influence of corruption and cultural differences on implementation. The standard setting process of AASB and the adoption of IFRS is common for all the local and other Australian issues as well. Being at the end the financial reporting is to be done considering the International accounting standards, it is important that at the end all the local and other Austin issues are in line with the International standards. Thus, the process that has been discussed above is common for all and to implement any changes in the existing accounting standards.

The accounting standards are very important current corporate world. Through the help of the

standards, the general purpose financial statements of the company which includes the profit and

loss account, balance sheet and cash flow statement are presented in a particular format which

becomes easier for the similar companies to make the comparison and further can be used by the

users and other stakeholders of the companies to make the comparison among similar companies

and take decisions relating to investment. Through the help of these accounting standards the

management of the companies tends to become more accountable to the stakeholders and

shareholders of the company about the financial feasibility of the companies.

Australian accounting standard board is a government agency that has been established by the

government to provide financial reporting android that can be used by public as well as private

entities in Australia. Powers and duties of Australian accounting standard board are set up by

Australian securities and investment Commission act 2001. In order to protect the interest of the

consumer, investors and creditors the Australian securities and investment commission was set

up. This governing body was set up to protect and regulate the companies and the financial

services law within Australia. Accounting standards and the interpretation that has been

developed by the accounting standard board is used by the entities that are required to prepare

the financial report as per the guidelines of Corporation Act 2001. The Government of the

country is also required to prepare financial statements for the entire government and for the

general government sectors as per the guidelines provided in the accounting standards issued by

the accounting standard board. Further private and public sector entities for working for profit or

nonprofit sectors are also required to prepare the general purpose financial statement as per the

guidelines provided in the accounting standards. (AASB)

standards, the general purpose financial statements of the company which includes the profit and

loss account, balance sheet and cash flow statement are presented in a particular format which

becomes easier for the similar companies to make the comparison and further can be used by the

users and other stakeholders of the companies to make the comparison among similar companies

and take decisions relating to investment. Through the help of these accounting standards the

management of the companies tends to become more accountable to the stakeholders and

shareholders of the company about the financial feasibility of the companies.

Australian accounting standard board is a government agency that has been established by the

government to provide financial reporting android that can be used by public as well as private

entities in Australia. Powers and duties of Australian accounting standard board are set up by

Australian securities and investment Commission act 2001. In order to protect the interest of the

consumer, investors and creditors the Australian securities and investment commission was set

up. This governing body was set up to protect and regulate the companies and the financial

services law within Australia. Accounting standards and the interpretation that has been

developed by the accounting standard board is used by the entities that are required to prepare

the financial report as per the guidelines of Corporation Act 2001. The Government of the

country is also required to prepare financial statements for the entire government and for the

general government sectors as per the guidelines provided in the accounting standards issued by

the accounting standard board. Further private and public sector entities for working for profit or

nonprofit sectors are also required to prepare the general purpose financial statement as per the

guidelines provided in the accounting standards. (AASB)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian accounting standard board has been set up in the country to perform the following

functions in the country:

In order to evaluate the standards that has been proposed they are likely to set up a

conceptual Framework around it.

The body has been authorized to develop accounting standards as per section 334 of the

Corporation Act 2001.

Authorized to make changes in the accounting standards for different purposes.

The body further has been authorized to participate and make contribution in the area of

development of single set up accounting standards that will be accepted worldwide.

The body has been authorized to promote the main objects of part 12 of ASIC act which

ensures to make the Australian entities more competitive world wide and increase the

confidence level of the investors in Australian economy and entities.

The mission of accounting standard board in Australia is to create reporting standards for the

country that help them to meet the needs of the uses. Further they are required to make

considerable contribution in developing the international reporting standards that will be

accepted worldwide. (AASB)

Case 1

The Australian accounting standard board has adopted international reporting financial

standards in the year 2005. This adoption has been done with an intention to make the

Australian entities more competitive in the international market. After the adoption of

international reporting accounting standards AASB has issued a mandate that all the profit

functions in the country:

In order to evaluate the standards that has been proposed they are likely to set up a

conceptual Framework around it.

The body has been authorized to develop accounting standards as per section 334 of the

Corporation Act 2001.

Authorized to make changes in the accounting standards for different purposes.

The body further has been authorized to participate and make contribution in the area of

development of single set up accounting standards that will be accepted worldwide.

The body has been authorized to promote the main objects of part 12 of ASIC act which

ensures to make the Australian entities more competitive world wide and increase the

confidence level of the investors in Australian economy and entities.

The mission of accounting standard board in Australia is to create reporting standards for the

country that help them to meet the needs of the uses. Further they are required to make

considerable contribution in developing the international reporting standards that will be

accepted worldwide. (AASB)

Case 1

The Australian accounting standard board has adopted international reporting financial

standards in the year 2005. This adoption has been done with an intention to make the

Australian entities more competitive in the international market. After the adoption of

international reporting accounting standards AASB has issued a mandate that all the profit

entities such as listed companies and the nonprofit organization public sector entities like the

Australian government and the non-profit private sector entities like charities etc is required

to carry out their financial reporting as per the international financial reporting standards.

The financial reporting Council, in the year 2005 has announced adoption of international

financial reporting standards in Australia. Financial reporting Council has been given

delegated powers by the government to ensure successful implementation of international

standards into the Australian accounting standards. This change has been done with an

intention so much the Australian market with the world financial markets. This option will

make a market more competitive for the Australian companies. Considering work that needs

to be done later on the date of implementation of IFRS date has been extended till Jan 2006.

Since the year 2004, IASB has started issuing exposure draft for entities in the extractive

industries. Later on certain stages has been determined for the implementation exercise

where the exposure draft has been presented for comments to the Australian board.

Australian accounting standard board has started incorporating IFRS aspect in their

accounting standards.

Being AASB has adopted international financial reporting standards, any technical issue that

has been identified by the IFRS interpretation committee or by international accounting

standard board will also included AASB change process. In this case the technical issue can

also be identified by international Public Sector Accounting Standards Board (IPSASB). The

AASB authorities’ places close watch on the program of IPSASB. Any Australian

stakeholders or investors can also identify issues to the authority. (AASB)

Australian government and the non-profit private sector entities like charities etc is required

to carry out their financial reporting as per the international financial reporting standards.

The financial reporting Council, in the year 2005 has announced adoption of international

financial reporting standards in Australia. Financial reporting Council has been given

delegated powers by the government to ensure successful implementation of international

standards into the Australian accounting standards. This change has been done with an

intention so much the Australian market with the world financial markets. This option will

make a market more competitive for the Australian companies. Considering work that needs

to be done later on the date of implementation of IFRS date has been extended till Jan 2006.

Since the year 2004, IASB has started issuing exposure draft for entities in the extractive

industries. Later on certain stages has been determined for the implementation exercise

where the exposure draft has been presented for comments to the Australian board.

Australian accounting standard board has started incorporating IFRS aspect in their

accounting standards.

Being AASB has adopted international financial reporting standards, any technical issue that

has been identified by the IFRS interpretation committee or by international accounting

standard board will also included AASB change process. In this case the technical issue can

also be identified by international Public Sector Accounting Standards Board (IPSASB). The

AASB authorities’ places close watch on the program of IPSASB. Any Australian

stakeholders or investors can also identify issues to the authority. (AASB)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Based on the technical issue that has been identified by the authorities, the AASB prepare

proposal agenda. Proposal the attached benefit that will be there if the issue has been

resolved, the associated cost, resources required and the time that will be taken to implement

the proposal. Once the proposal has been placed, the AASB authorities will take a decision

whether the proposal that has been put in place is worthwhile and if it is, then the same

should be put in their work flow agenda. It is at the discretion of the board whether to address

the technical issues in the agent or not. These issues are termed as “items not taken onto the

agenda”.

Once the technical issue has been added in the agenda, the AASB board will go through

agenda papers that have been presented in developed by the staff of the board. The person

that has been prepared by the staff members includes the scope of the issue, any alternative

approach and the expected time of the output. The working papers in this case can be made

considering the material that can be obtained from different boards light ISAB, IPSASB etc.

This discussion can be made jointly with the New Zealand accounting standard board official

is common in both the countries. (AASB)

Once the agent has been discussed and necessary research work has been completed, the

accounting standard board will issue the working papers for public comments and for the

stakeholders. There are different ways which we can be used by the board to present the

documents to the public which includes presentation of exposure draft which contains the

issue, through the help of invitation to comment, through draft interpretation, discussion

papers etc. The Australian accounting standard board sometimes form advisory panels which

includes members from different areas includes auditors, regulator, preparers and the users of

the financial statements which can give their opinion on the draft exposure. The main

proposal agenda. Proposal the attached benefit that will be there if the issue has been

resolved, the associated cost, resources required and the time that will be taken to implement

the proposal. Once the proposal has been placed, the AASB authorities will take a decision

whether the proposal that has been put in place is worthwhile and if it is, then the same

should be put in their work flow agenda. It is at the discretion of the board whether to address

the technical issues in the agent or not. These issues are termed as “items not taken onto the

agenda”.

Once the technical issue has been added in the agenda, the AASB board will go through

agenda papers that have been presented in developed by the staff of the board. The person

that has been prepared by the staff members includes the scope of the issue, any alternative

approach and the expected time of the output. The working papers in this case can be made

considering the material that can be obtained from different boards light ISAB, IPSASB etc.

This discussion can be made jointly with the New Zealand accounting standard board official

is common in both the countries. (AASB)

Once the agent has been discussed and necessary research work has been completed, the

accounting standard board will issue the working papers for public comments and for the

stakeholders. There are different ways which we can be used by the board to present the

documents to the public which includes presentation of exposure draft which contains the

issue, through the help of invitation to comment, through draft interpretation, discussion

papers etc. The Australian accounting standard board sometimes form advisory panels which

includes members from different areas includes auditors, regulator, preparers and the users of

the financial statements which can give their opinion on the draft exposure. The main

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

function of the advisory panel is to list down the alternative views that has been presented by

the public and if found reasonable can be presented along with their recommendation to the

board.

It is again at the discretion of the board whether to accept the public comments made in the

above case or not. In this case, the accounting standard board can issue pronouncements in

the form of conceptual framework, interpretation or in the form of standard. Any

pronouncement that has an impact on the profit entities should be in line with the

international financial reporting standards issued by the international accounting standard

board. This has been done in order to ensure that the financial statement that has been

prepared by the profit entities belonging to Australia is in line with the international

accounting standards. Further, the accounting standard board adopts a transaction neutrality

policy under which any similar transaction shall be accounted in a similar way in all entities

whether the same is a profit entity or a non-profit entry unless and until there is a sound

reason with states that transition should be accounted in a different manner. (AASB)

Once the interpretation and pronouncement has been finalized by APRA, they send the final

draft to the international organizations for the approval. This process will help in setting high

quality standards and process improvements. Sometimes after the draft exposes form has

been sent to the international organizations they suggest some comments and based on their

comments certain changes have been further implemented in the accounting standards. Once

the changes have been done, the exposure draft is against sent to the stakeholders for their

comments.

the public and if found reasonable can be presented along with their recommendation to the

board.

It is again at the discretion of the board whether to accept the public comments made in the

above case or not. In this case, the accounting standard board can issue pronouncements in

the form of conceptual framework, interpretation or in the form of standard. Any

pronouncement that has an impact on the profit entities should be in line with the

international financial reporting standards issued by the international accounting standard

board. This has been done in order to ensure that the financial statement that has been

prepared by the profit entities belonging to Australia is in line with the international

accounting standards. Further, the accounting standard board adopts a transaction neutrality

policy under which any similar transaction shall be accounted in a similar way in all entities

whether the same is a profit entity or a non-profit entry unless and until there is a sound

reason with states that transition should be accounted in a different manner. (AASB)

Once the interpretation and pronouncement has been finalized by APRA, they send the final

draft to the international organizations for the approval. This process will help in setting high

quality standards and process improvements. Sometimes after the draft exposes form has

been sent to the international organizations they suggest some comments and based on their

comments certain changes have been further implemented in the accounting standards. Once

the changes have been done, the exposure draft is against sent to the stakeholders for their

comments.

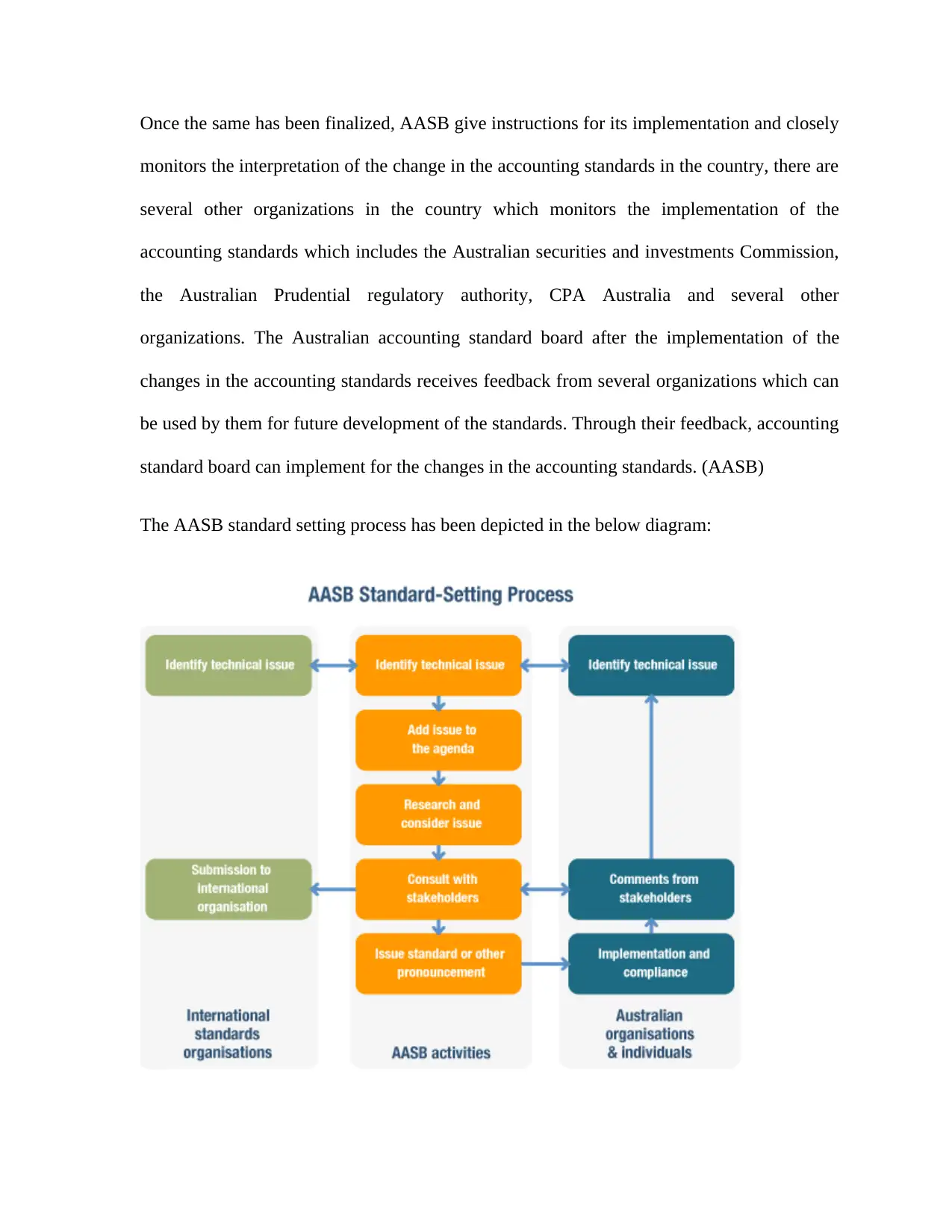

Once the same has been finalized, AASB give instructions for its implementation and closely

monitors the interpretation of the change in the accounting standards in the country, there are

several other organizations in the country which monitors the implementation of the

accounting standards which includes the Australian securities and investments Commission,

the Australian Prudential regulatory authority, CPA Australia and several other

organizations. The Australian accounting standard board after the implementation of the

changes in the accounting standards receives feedback from several organizations which can

be used by them for future development of the standards. Through their feedback, accounting

standard board can implement for the changes in the accounting standards. (AASB)

The AASB standard setting process has been depicted in the below diagram:

monitors the interpretation of the change in the accounting standards in the country, there are

several other organizations in the country which monitors the implementation of the

accounting standards which includes the Australian securities and investments Commission,

the Australian Prudential regulatory authority, CPA Australia and several other

organizations. The Australian accounting standard board after the implementation of the

changes in the accounting standards receives feedback from several organizations which can

be used by them for future development of the standards. Through their feedback, accounting

standard board can implement for the changes in the accounting standards. (AASB)

The AASB standard setting process has been depicted in the below diagram:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The process that has been followed by AASB to incorporate technical issues in the Australian

accounting standards is common for all the local and other Australian issues as well. Being at

the end the financial reporting is to be done considering the International accounting

standards, it is important that at the end all the local and other Austin issues are in line with

the International standards. Thus, the process that has been discussed above is common for

all and to implement any changes in the existing accounting standards.

Case 2

AASB 116 stands for property, plant and equipment. AASB 116 property plant and

equipment has been amended and incorporates IAS 16 as issued and implemented by

international accounting standard board. For profit entities, there has been no major change

being in this case, the provisions of AASB 116 are in line with the provisions of IAS 16.

However, in terms of not-for-profit entities, there has been some difference in the provisions

of AASB 116 and IAS 16. There are certain different provisions for determining a not-for-

profit entity in case of IAS 16.Thus, after Incorporation of IAS 16 with AASB 116, the rules

for determining a not-for-profit entity has changed which has resulted in change in

accounting for the entities. Thus, in order to ensure that a not-for-profit entity IAS 16 will

depend on whether the "AUS" paragraphs provide some additional guidelines for these

entities or some other requirements which are in line with the corresponding international

standard.

accounting standards is common for all the local and other Australian issues as well. Being at

the end the financial reporting is to be done considering the International accounting

standards, it is important that at the end all the local and other Austin issues are in line with

the International standards. Thus, the process that has been discussed above is common for

all and to implement any changes in the existing accounting standards.

Case 2

AASB 116 stands for property, plant and equipment. AASB 116 property plant and

equipment has been amended and incorporates IAS 16 as issued and implemented by

international accounting standard board. For profit entities, there has been no major change

being in this case, the provisions of AASB 116 are in line with the provisions of IAS 16.

However, in terms of not-for-profit entities, there has been some difference in the provisions

of AASB 116 and IAS 16. There are certain different provisions for determining a not-for-

profit entity in case of IAS 16.Thus, after Incorporation of IAS 16 with AASB 116, the rules

for determining a not-for-profit entity has changed which has resulted in change in

accounting for the entities. Thus, in order to ensure that a not-for-profit entity IAS 16 will

depend on whether the "AUS" paragraphs provide some additional guidelines for these

entities or some other requirements which are in line with the corresponding international

standard.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

There are so many research conducted all over the world to implement IFRS as the official

financial reporting standards for all countries including developing and developed countries.

However, there have been many obstacles being faced during this adoption which includes

corrupt and weak government, poor education level and most important cultural differences.

Looking at the positive side of the IFRS, if all countries in the world adopt recent they would

be no financial disparity. Comparison between the companies would become easier. Through

the help of IFRS, financial reports that can be generated tend to be more detailed. These

reports at the same time will offer better transparency and more viable compatibility.

Currently IFRS has been adopted by more than hundred countries in the world. There has

been multiple studies been carried out all over the world which at the same time complicates

and influence the movement of local accounting standards towards international financial

reporting standards. In case of developing countries, the adoption of International accounting

standards and their implementation/ enforcement are two different things. The growing

corruption in developing countries tends to be a hindrance which may impact the adoption of

International accounting standards in these countries. This correction tends to be done the

effectiveness of government institutions. (Albu, 2012)

Thus, does it is very difficult to adopt single accounting guidelines all across the globe. It is

very important to understand the context behind choosing a financial reporting system for a

country. We cannot just implement and international financial reporting standard to a

developing country when its people and government are not ready to accept the changes. The

cultural differences and the corruption in the developing countries and most important lack of

proper education impact this adoption process. However if there is a need and government of

the country is ready to adopt the standards and wanted to compete in the International

financial reporting standards for all countries including developing and developed countries.

However, there have been many obstacles being faced during this adoption which includes

corrupt and weak government, poor education level and most important cultural differences.

Looking at the positive side of the IFRS, if all countries in the world adopt recent they would

be no financial disparity. Comparison between the companies would become easier. Through

the help of IFRS, financial reports that can be generated tend to be more detailed. These

reports at the same time will offer better transparency and more viable compatibility.

Currently IFRS has been adopted by more than hundred countries in the world. There has

been multiple studies been carried out all over the world which at the same time complicates

and influence the movement of local accounting standards towards international financial

reporting standards. In case of developing countries, the adoption of International accounting

standards and their implementation/ enforcement are two different things. The growing

corruption in developing countries tends to be a hindrance which may impact the adoption of

International accounting standards in these countries. This correction tends to be done the

effectiveness of government institutions. (Albu, 2012)

Thus, does it is very difficult to adopt single accounting guidelines all across the globe. It is

very important to understand the context behind choosing a financial reporting system for a

country. We cannot just implement and international financial reporting standard to a

developing country when its people and government are not ready to accept the changes. The

cultural differences and the corruption in the developing countries and most important lack of

proper education impact this adoption process. However if there is a need and government of

the country is ready to adopt the standards and wanted to compete in the International

Financial Market, the adoption of IFRS can be a success. The effectiveness and fairness of

the concept "one size fits all" for international accounting standards can be a success only

when people and the government understand the actual importance behind the process. Force

full implementation of these standards will not help and may have its own repercussions. It is

a long process and may take considerable time. But looking at the current scenario, share

more than hundred countries have already adopted International standards, the motion of "

one size fits all" does not look impossible. (Bova, 2012)

References

AASB, Accounting standards, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB/For-students.aspx

AASB, About the Accounting standards, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB.aspx

AASB, 2009, IFRS adoption in Australia, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/admin/file/content102/c3/IFRS_adoption_in_Australia_Sept_2009.pdf

AASB, The Standard-Setting Process, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx

Williamson M, 2004, International Accounting Standards and their Impact on Resource

Industries in Australia, Viewed on 19th Aug 2017, Retrieved from

http://www.austlii.edu.au/au/journals/AUMPLawAYbk/2004/28.pdf

Albu., N., Albu N., C., & Girbina M., M. (2012). Educating accounting students in an emerging

the concept "one size fits all" for international accounting standards can be a success only

when people and the government understand the actual importance behind the process. Force

full implementation of these standards will not help and may have its own repercussions. It is

a long process and may take considerable time. But looking at the current scenario, share

more than hundred countries have already adopted International standards, the motion of "

one size fits all" does not look impossible. (Bova, 2012)

References

AASB, Accounting standards, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB/For-students.aspx

AASB, About the Accounting standards, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB.aspx

AASB, 2009, IFRS adoption in Australia, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/admin/file/content102/c3/IFRS_adoption_in_Australia_Sept_2009.pdf

AASB, The Standard-Setting Process, Viewed on 19th Aug 2017, Retrieved from

http://www.aasb.gov.au/About-the-AASB/The-standard-setting-process.aspx

Williamson M, 2004, International Accounting Standards and their Impact on Resource

Industries in Australia, Viewed on 19th Aug 2017, Retrieved from

http://www.austlii.edu.au/au/journals/AUMPLawAYbk/2004/28.pdf

Albu., N., Albu N., C., & Girbina M., M. (2012). Educating accounting students in an emerging

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

economy - An analysis of the importance of stereotypes in teaching IFRS. Internation Journal of

Academic Research,Vol. 4(No. 3), 51-57. Retrieved from Ebsco Host.

Bova, F., & Pereira, R. (2012). The determinanats and consequences of heterogeneous IFRS

compliance levels following mandatory IFRS adoption: Evidence form a developing country.

Journal of International Accounting Research,Vol. 11(No. 1), 83-111. Retrieved from Ebsco

Host.

Cardona J., R., Castro-Gonzalez C., K., & Rios-Figueroa B., C. (2014). The impact of culture

and economic factors on the implementation of IFRS. Accounting & Taxation,Vol. 6(No. 2), 29-

47. Retrieved from Ebsco Host.

Academic Research,Vol. 4(No. 3), 51-57. Retrieved from Ebsco Host.

Bova, F., & Pereira, R. (2012). The determinanats and consequences of heterogeneous IFRS

compliance levels following mandatory IFRS adoption: Evidence form a developing country.

Journal of International Accounting Research,Vol. 11(No. 1), 83-111. Retrieved from Ebsco

Host.

Cardona J., R., Castro-Gonzalez C., K., & Rios-Figueroa B., C. (2014). The impact of culture

and economic factors on the implementation of IFRS. Accounting & Taxation,Vol. 6(No. 2), 29-

47. Retrieved from Ebsco Host.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.