Business Accounting Report: Trial Balance, Adjustments, and Statements

VerifiedAdded on 2023/03/30

|10

|2144

|125

Report

AI Summary

This business accounting report comprehensively covers key aspects of financial accounting, including the preparation and analysis of trial balances, the application of adjusting journal entries, and the creation of essential financial statements such as the income statement, balance sheet, and statement of changes in equity. The report details the process of journalizing adjusting transactions, provides a trial balance, and explains the reasons for creating and recording adjusting entries. It also clarifies the purpose of an adjusted trial balance and differentiates between adjusting and closing journal entries. The report includes a detailed income statement and balance sheet, along with a statement of changes in equity, offering a practical application of accounting principles. Finally, it provides a detailed explanation of the trial balance, its importance, and the impact of the adjusting entries on the financial statements.

Running Head: BUSINESS ACCOUNTING 0

Business Accounting

Business Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 1

Table of Contents

Adjusting journal entries.......................................................................................................................2

Trial balance..........................................................................................................................................2

Income Statement..................................................................................................................................4

Balance Sheet........................................................................................................................................4

Statement of Changes in Equity.............................................................................................................5

Trial balance......................................................................................................................................5

Reason for Creation...........................................................................................................................6

Reason for recording.........................................................................................................................7

Purpose of writing an adjusted trial balance......................................................................................7

Difference between the adjustment entries and closing journal entries..............................................8

References.............................................................................................................................................9

Table of Contents

Adjusting journal entries.......................................................................................................................2

Trial balance..........................................................................................................................................2

Income Statement..................................................................................................................................4

Balance Sheet........................................................................................................................................4

Statement of Changes in Equity.............................................................................................................5

Trial balance......................................................................................................................................5

Reason for Creation...........................................................................................................................6

Reason for recording.........................................................................................................................7

Purpose of writing an adjusted trial balance......................................................................................7

Difference between the adjustment entries and closing journal entries..............................................8

References.............................................................................................................................................9

BUSINESS ACCOUNTING 2

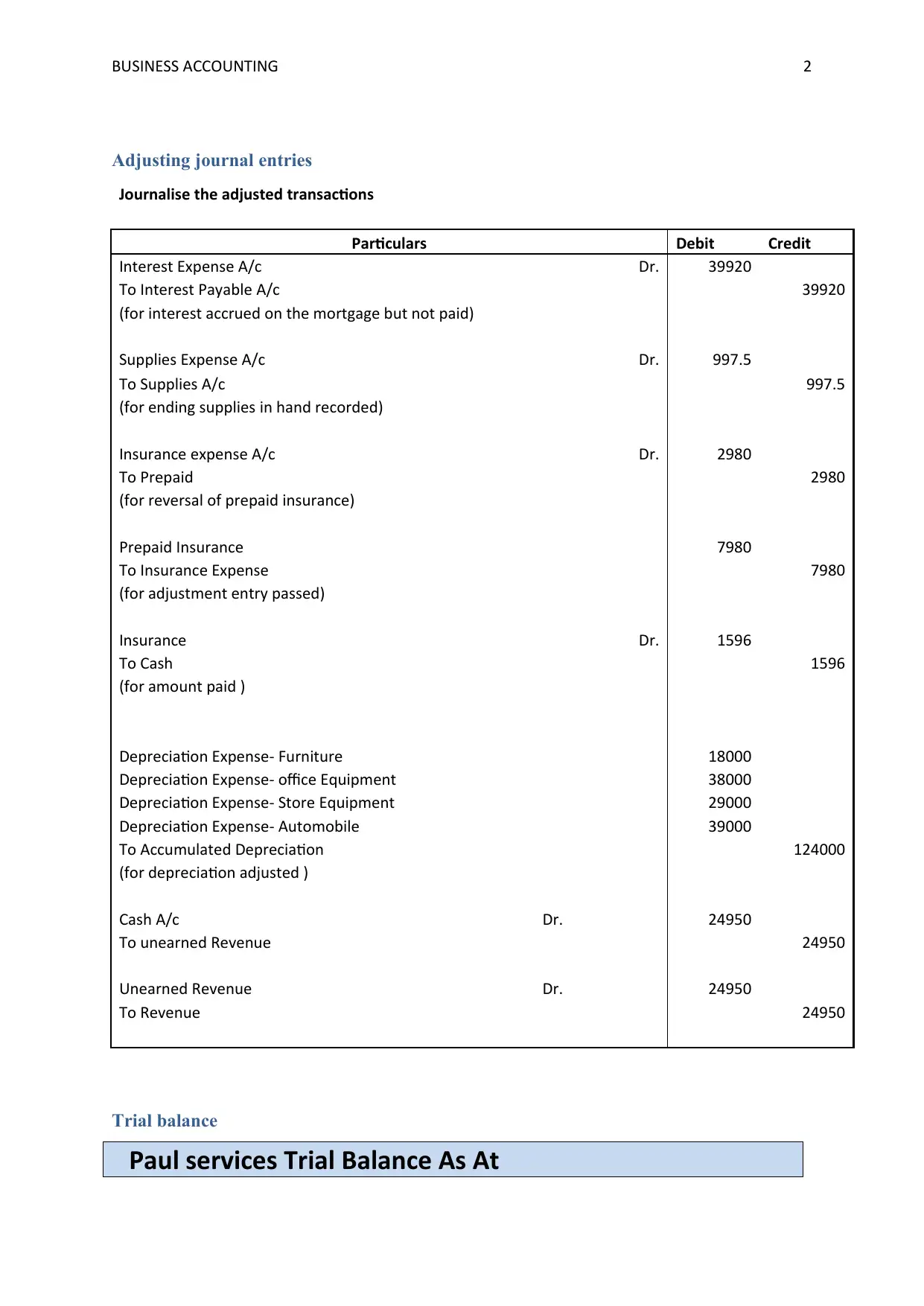

Adjusting journal entries

Journalise the adjusted transactions

Particulars Debit Credit

Interest Expense A/c Dr. 39920

To Interest Payable A/c 39920

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 997.5

To Supplies A/c 997.5

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 2980

To Prepaid 2980

(for reversal of prepaid insurance)

Prepaid Insurance 7980

To Insurance Expense 7980

(for adjustment entry passed)

Insurance Dr. 1596

To Cash 1596

(for amount paid )

Depreciation Expense- Furniture 18000

Depreciation Expense- office Equipment 38000

Depreciation Expense- Store Equipment 29000

Depreciation Expense- Automobile 39000

To Accumulated Depreciation 124000

(for depreciation adjusted )

Cash A/c Dr. 24950

To unearned Revenue 24950

Unearned Revenue Dr. 24950

To Revenue 24950

Trial balance

Paul services Trial Balance As At

Adjusting journal entries

Journalise the adjusted transactions

Particulars Debit Credit

Interest Expense A/c Dr. 39920

To Interest Payable A/c 39920

(for interest accrued on the mortgage but not paid)

Supplies Expense A/c Dr. 997.5

To Supplies A/c 997.5

(for ending supplies in hand recorded)

Insurance expense A/c Dr. 2980

To Prepaid 2980

(for reversal of prepaid insurance)

Prepaid Insurance 7980

To Insurance Expense 7980

(for adjustment entry passed)

Insurance Dr. 1596

To Cash 1596

(for amount paid )

Depreciation Expense- Furniture 18000

Depreciation Expense- office Equipment 38000

Depreciation Expense- Store Equipment 29000

Depreciation Expense- Automobile 39000

To Accumulated Depreciation 124000

(for depreciation adjusted )

Cash A/c Dr. 24950

To unearned Revenue 24950

Unearned Revenue Dr. 24950

To Revenue 24950

Trial balance

Paul services Trial Balance As At

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 3

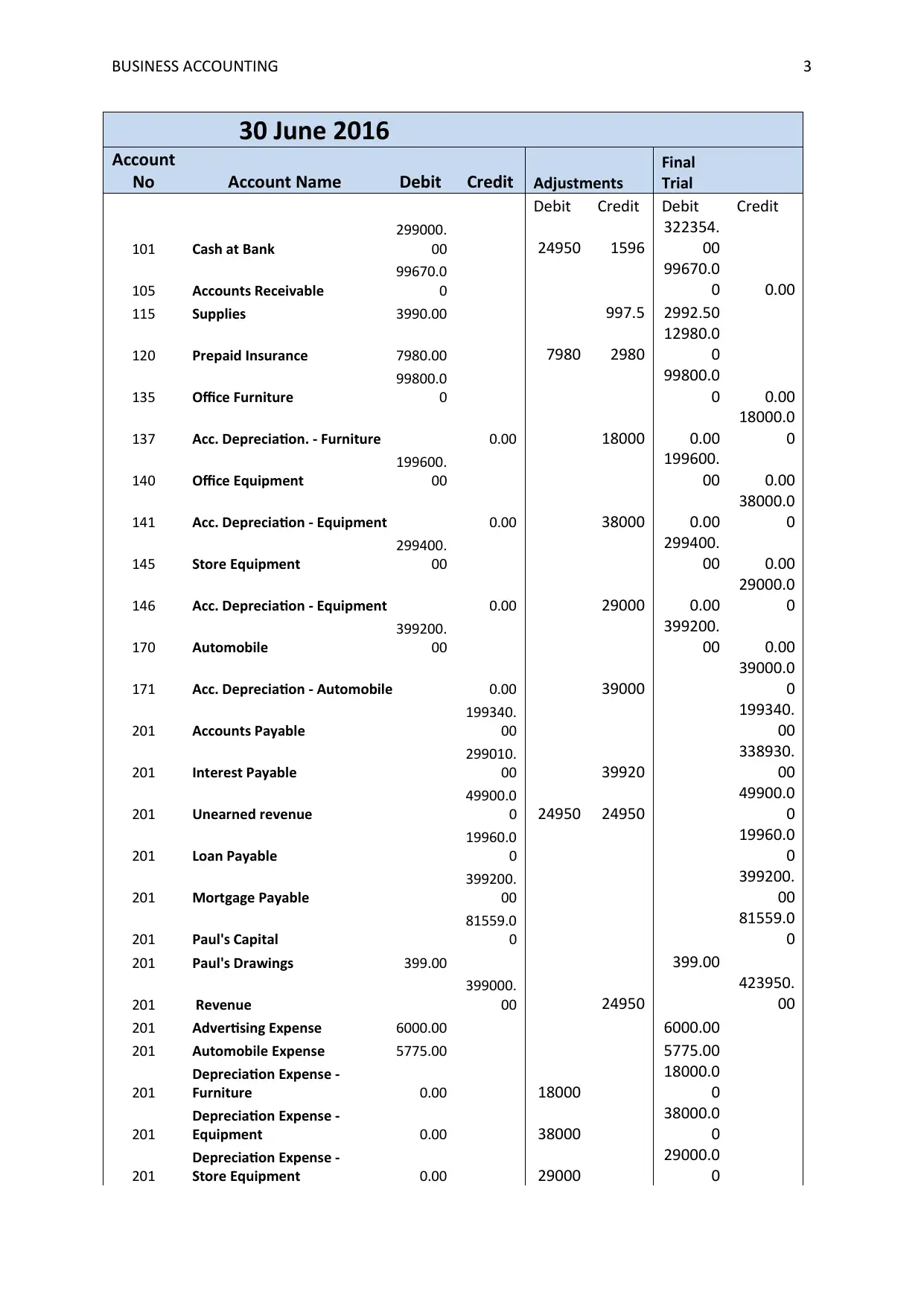

30 June 2016

Account

No Account Name Debit Credit Adjustments

Final

Trial

Debit Credit Debit Credit

101 Cash at Bank

299000.

00 24950 1596

322354.

00

105 Accounts Receivable

99670.0

0

99670.0

0 0.00

115 Supplies 3990.00 997.5 2992.50

120 Prepaid Insurance 7980.00 7980 2980

12980.0

0

135 Office Furniture

99800.0

0

99800.0

0 0.00

137 Acc. Depreciation. - Furniture 0.00 18000 0.00

18000.0

0

140 Office Equipment

199600.

00

199600.

00 0.00

141 Acc. Depreciation - Equipment 0.00 38000 0.00

38000.0

0

145 Store Equipment

299400.

00

299400.

00 0.00

146 Acc. Depreciation - Equipment 0.00 29000 0.00

29000.0

0

170 Automobile

399200.

00

399200.

00 0.00

171 Acc. Depreciation - Automobile 0.00 39000

39000.0

0

201 Accounts Payable

199340.

00

199340.

00

201 Interest Payable

299010.

00 39920

338930.

00

201 Unearned revenue

49900.0

0 24950 24950

49900.0

0

201 Loan Payable

19960.0

0

19960.0

0

201 Mortgage Payable

399200.

00

399200.

00

201 Paul's Capital

81559.0

0

81559.0

0

201 Paul's Drawings 399.00 399.00

201 Revenue

399000.

00 24950

423950.

00

201 Advertising Expense 6000.00 6000.00

201 Automobile Expense 5775.00 5775.00

201

Depreciation Expense -

Furniture 0.00 18000

18000.0

0

201

Depreciation Expense -

Equipment 0.00 38000

38000.0

0

201

Depreciation Expense -

Store Equipment 0.00 29000

29000.0

0

30 June 2016

Account

No Account Name Debit Credit Adjustments

Final

Trial

Debit Credit Debit Credit

101 Cash at Bank

299000.

00 24950 1596

322354.

00

105 Accounts Receivable

99670.0

0

99670.0

0 0.00

115 Supplies 3990.00 997.5 2992.50

120 Prepaid Insurance 7980.00 7980 2980

12980.0

0

135 Office Furniture

99800.0

0

99800.0

0 0.00

137 Acc. Depreciation. - Furniture 0.00 18000 0.00

18000.0

0

140 Office Equipment

199600.

00

199600.

00 0.00

141 Acc. Depreciation - Equipment 0.00 38000 0.00

38000.0

0

145 Store Equipment

299400.

00

299400.

00 0.00

146 Acc. Depreciation - Equipment 0.00 29000 0.00

29000.0

0

170 Automobile

399200.

00

399200.

00 0.00

171 Acc. Depreciation - Automobile 0.00 39000

39000.0

0

201 Accounts Payable

199340.

00

199340.

00

201 Interest Payable

299010.

00 39920

338930.

00

201 Unearned revenue

49900.0

0 24950 24950

49900.0

0

201 Loan Payable

19960.0

0

19960.0

0

201 Mortgage Payable

399200.

00

399200.

00

201 Paul's Capital

81559.0

0

81559.0

0

201 Paul's Drawings 399.00 399.00

201 Revenue

399000.

00 24950

423950.

00

201 Advertising Expense 6000.00 6000.00

201 Automobile Expense 5775.00 5775.00

201

Depreciation Expense -

Furniture 0.00 18000

18000.0

0

201

Depreciation Expense -

Equipment 0.00 38000

38000.0

0

201

Depreciation Expense -

Store Equipment 0.00 29000

29000.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

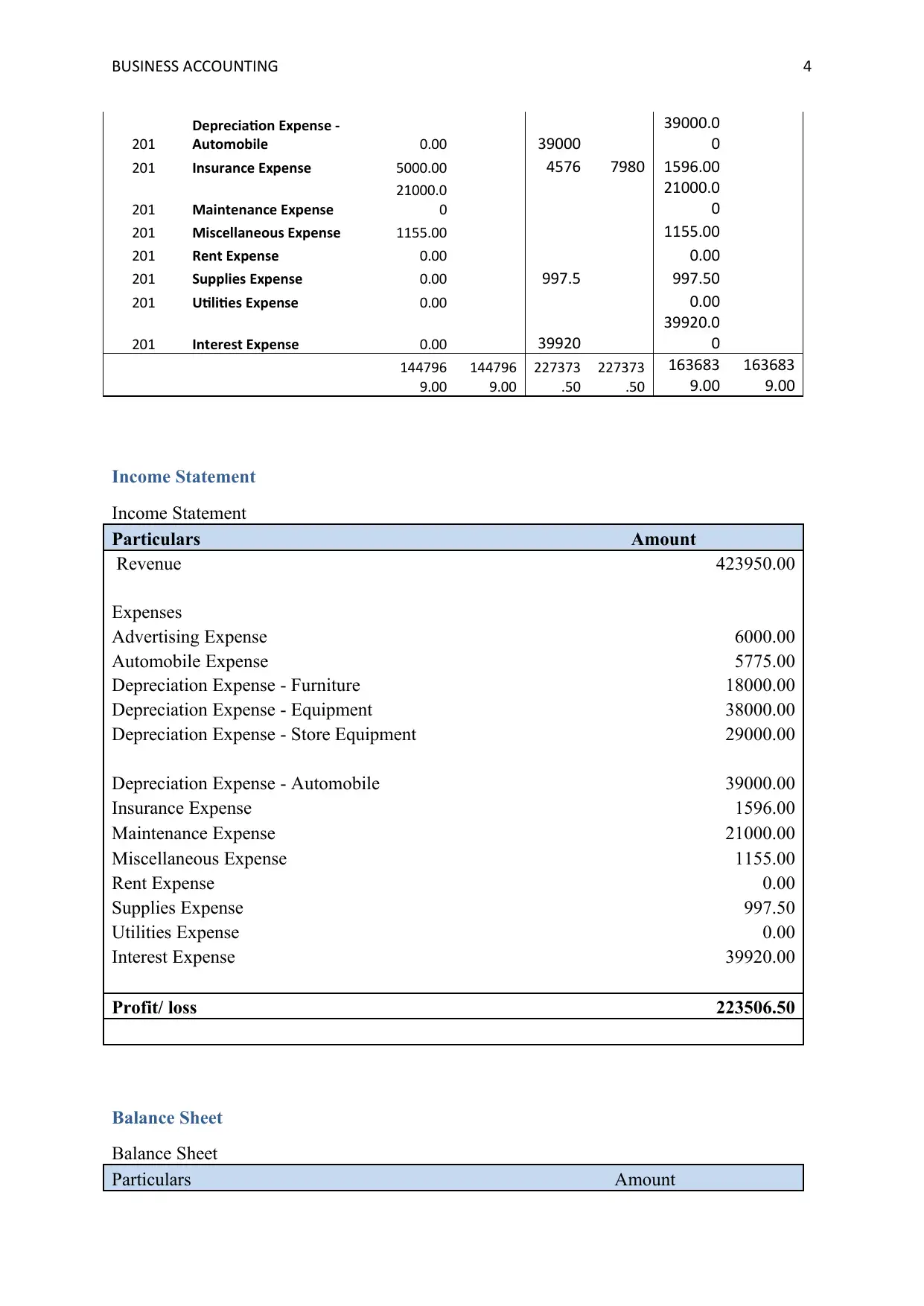

BUSINESS ACCOUNTING 4

201

Depreciation Expense -

Automobile 0.00 39000

39000.0

0

201 Insurance Expense 5000.00 4576 7980 1596.00

201 Maintenance Expense

21000.0

0

21000.0

0

201 Miscellaneous Expense 1155.00 1155.00

201 Rent Expense 0.00 0.00

201 Supplies Expense 0.00 997.5 997.50

201 Utilities Expense 0.00 0.00

201 Interest Expense 0.00 39920

39920.0

0

144796

9.00

144796

9.00

227373

.50

227373

.50

163683

9.00

163683

9.00

Income Statement

Income Statement

Particulars Amount

Revenue 423950.00

Expenses

Advertising Expense 6000.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 18000.00

Depreciation Expense - Equipment 38000.00

Depreciation Expense - Store Equipment 29000.00

Depreciation Expense - Automobile 39000.00

Insurance Expense 1596.00

Maintenance Expense 21000.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 997.50

Utilities Expense 0.00

Interest Expense 39920.00

Profit/ loss 223506.50

Balance Sheet

Balance Sheet

Particulars Amount

201

Depreciation Expense -

Automobile 0.00 39000

39000.0

0

201 Insurance Expense 5000.00 4576 7980 1596.00

201 Maintenance Expense

21000.0

0

21000.0

0

201 Miscellaneous Expense 1155.00 1155.00

201 Rent Expense 0.00 0.00

201 Supplies Expense 0.00 997.5 997.50

201 Utilities Expense 0.00 0.00

201 Interest Expense 0.00 39920

39920.0

0

144796

9.00

144796

9.00

227373

.50

227373

.50

163683

9.00

163683

9.00

Income Statement

Income Statement

Particulars Amount

Revenue 423950.00

Expenses

Advertising Expense 6000.00

Automobile Expense 5775.00

Depreciation Expense - Furniture 18000.00

Depreciation Expense - Equipment 38000.00

Depreciation Expense - Store Equipment 29000.00

Depreciation Expense - Automobile 39000.00

Insurance Expense 1596.00

Maintenance Expense 21000.00

Miscellaneous Expense 1155.00

Rent Expense 0.00

Supplies Expense 997.50

Utilities Expense 0.00

Interest Expense 39920.00

Profit/ loss 223506.50

Balance Sheet

Balance Sheet

Particulars Amount

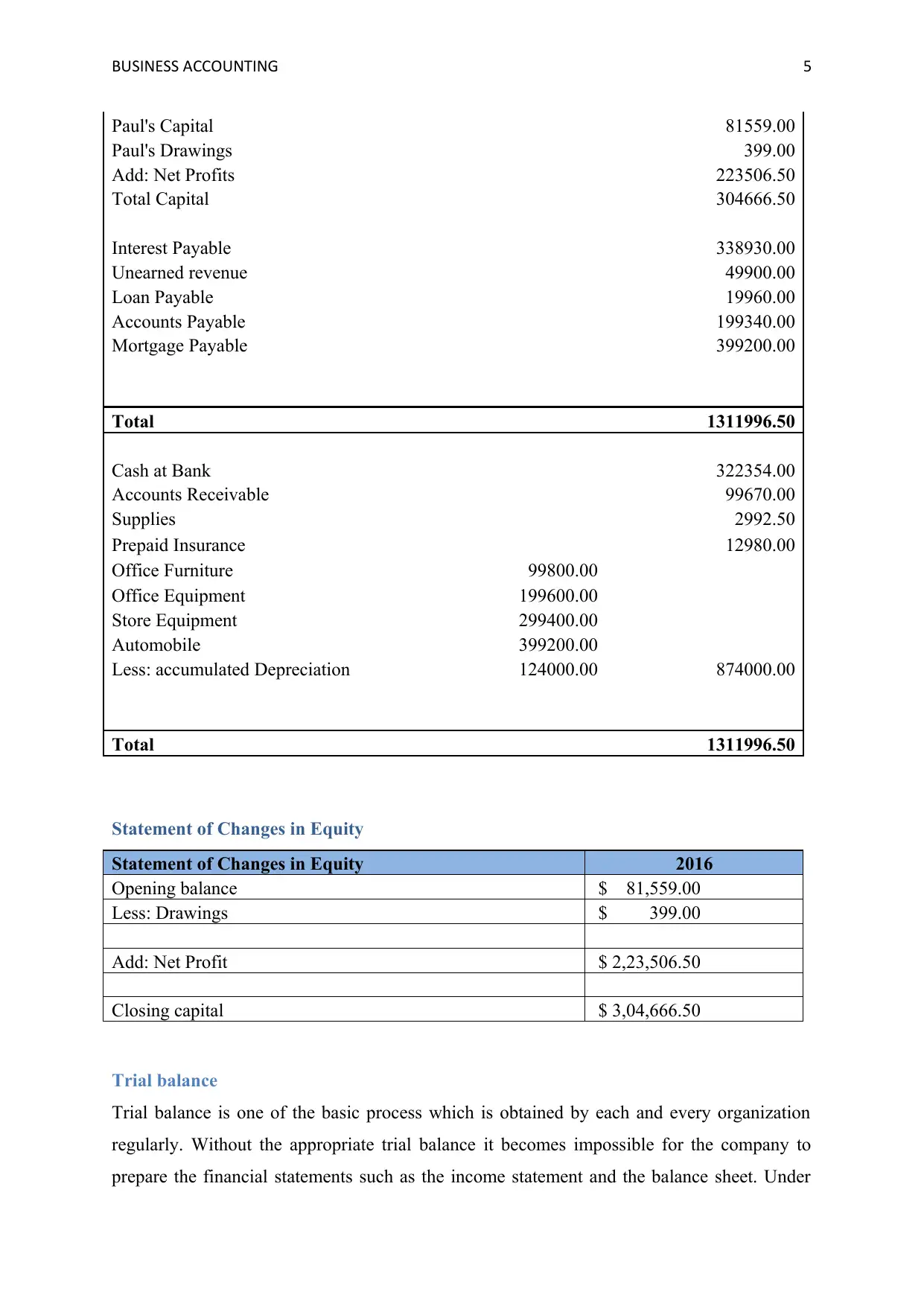

BUSINESS ACCOUNTING 5

Paul's Capital 81559.00

Paul's Drawings 399.00

Add: Net Profits 223506.50

Total Capital 304666.50

Interest Payable 338930.00

Unearned revenue 49900.00

Loan Payable 19960.00

Accounts Payable 199340.00

Mortgage Payable 399200.00

Total 1311996.50

Cash at Bank 322354.00

Accounts Receivable 99670.00

Supplies 2992.50

Prepaid Insurance 12980.00

Office Furniture 99800.00

Office Equipment 199600.00

Store Equipment 299400.00

Automobile 399200.00

Less: accumulated Depreciation 124000.00 874000.00

Total 1311996.50

Statement of Changes in Equity

Statement of Changes in Equity 2016

Opening balance $ 81,559.00

Less: Drawings $ 399.00

Add: Net Profit $ 2,23,506.50

Closing capital $ 3,04,666.50

Trial balance

Trial balance is one of the basic process which is obtained by each and every organization

regularly. Without the appropriate trial balance it becomes impossible for the company to

prepare the financial statements such as the income statement and the balance sheet. Under

Paul's Capital 81559.00

Paul's Drawings 399.00

Add: Net Profits 223506.50

Total Capital 304666.50

Interest Payable 338930.00

Unearned revenue 49900.00

Loan Payable 19960.00

Accounts Payable 199340.00

Mortgage Payable 399200.00

Total 1311996.50

Cash at Bank 322354.00

Accounts Receivable 99670.00

Supplies 2992.50

Prepaid Insurance 12980.00

Office Furniture 99800.00

Office Equipment 199600.00

Store Equipment 299400.00

Automobile 399200.00

Less: accumulated Depreciation 124000.00 874000.00

Total 1311996.50

Statement of Changes in Equity

Statement of Changes in Equity 2016

Opening balance $ 81,559.00

Less: Drawings $ 399.00

Add: Net Profit $ 2,23,506.50

Closing capital $ 3,04,666.50

Trial balance

Trial balance is one of the basic process which is obtained by each and every organization

regularly. Without the appropriate trial balance it becomes impossible for the company to

prepare the financial statements such as the income statement and the balance sheet. Under

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 6

the trial balance there are two columns namely the debit as well as the credit. The debit

column depicts all the assets and the expenses incurred, whereas the credit column shows the

amount of the revenue earned and the liabilities incurred in operating a business. The

magnificence of the trail balance lies in the arrangement between the debit and the credit side.

Toward the finish of the chronicle of the considerable number of exchanges from general

records the equalization is equivalent in both the sides. Prior in the manual framework the

preliminary equalization was set up by the bookkeeper or the clerk so as to discover the

fluctuations and the jumble of the sums, which currently has been unravelled through the

usage of the different software available in the market such as SAP, oracle , tally, for

example, Tally. Once the trial balance is established it certainly does not mean it will be free

from errors and there could be certain adjustments that are required to be adjusted while

preparing the final trial (Akçay, 2018).

Reason for Creation

The trial balance acts as the basic ingredient in determining the performance of the business,

henceforth the creation of the trail balance is equally necessary and worthy. At times the

situation can be such that the figure is posted into the wrong account, or the numbers are

reversed by mistake for example the adverting expense was originally $9876 but it has been

written as $9768. These mistakes were of such minor nature that they were being neglected

by the accountants. Hence the trial balance was introduced in the concept of the preparation

of the financial statements (Salmon and Wild, 2016).

Preliminary trial balance is a basic and important instrument which in the end distinguishes

such sort of blunders and the individual in charge of the mix-up can likewise be discovered

effectively in the association with the help of the trial balance. There is a considerable

rundown of the general population who uses the trial balance, for example, ,management

itself in preparation of the financial statements, the creditors in knowing whether the proper

recording of the entries are made in case of the inventory purchased on the credit, the

shareholder for making the strategic decision making. The preliminary trail balance has the

novel component that is serves the total prerequisite and gives an inside and out investigation

of the firm or the organization. The standard of the twofold passage framework can be made

sense of utilizing the preliminary parity.

Adjustment Journal Entry is passed utilizing the division of all the pay adjusts. The diary

section is fundamentally passed to cause an alteration of the incomes and the use from the

the trial balance there are two columns namely the debit as well as the credit. The debit

column depicts all the assets and the expenses incurred, whereas the credit column shows the

amount of the revenue earned and the liabilities incurred in operating a business. The

magnificence of the trail balance lies in the arrangement between the debit and the credit side.

Toward the finish of the chronicle of the considerable number of exchanges from general

records the equalization is equivalent in both the sides. Prior in the manual framework the

preliminary equalization was set up by the bookkeeper or the clerk so as to discover the

fluctuations and the jumble of the sums, which currently has been unravelled through the

usage of the different software available in the market such as SAP, oracle , tally, for

example, Tally. Once the trial balance is established it certainly does not mean it will be free

from errors and there could be certain adjustments that are required to be adjusted while

preparing the final trial (Akçay, 2018).

Reason for Creation

The trial balance acts as the basic ingredient in determining the performance of the business,

henceforth the creation of the trail balance is equally necessary and worthy. At times the

situation can be such that the figure is posted into the wrong account, or the numbers are

reversed by mistake for example the adverting expense was originally $9876 but it has been

written as $9768. These mistakes were of such minor nature that they were being neglected

by the accountants. Hence the trial balance was introduced in the concept of the preparation

of the financial statements (Salmon and Wild, 2016).

Preliminary trial balance is a basic and important instrument which in the end distinguishes

such sort of blunders and the individual in charge of the mix-up can likewise be discovered

effectively in the association with the help of the trial balance. There is a considerable

rundown of the general population who uses the trial balance, for example, ,management

itself in preparation of the financial statements, the creditors in knowing whether the proper

recording of the entries are made in case of the inventory purchased on the credit, the

shareholder for making the strategic decision making. The preliminary trail balance has the

novel component that is serves the total prerequisite and gives an inside and out investigation

of the firm or the organization. The standard of the twofold passage framework can be made

sense of utilizing the preliminary parity.

Adjustment Journal Entry is passed utilizing the division of all the pay adjusts. The diary

section is fundamentally passed to cause an alteration of the incomes and the use from the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS ACCOUNTING 7

beginning since them to have happened. These entries can likewise be named as a monetary

announcing that redresses the misstep which have made in the earlier years when the trial

balance was prepared. The Adjusting Journal Entries is utilized to adjust and make the offset

with the accumulation idea. The Adjusting Journal Entries is passed just before the

arrangement of the budget reports to move the sum into the fiscal summaries and mirror the

unmistakable and the straightforward picture. To deal with the proper accounting treatment

the altering of the entries is vital and a greater picture is reflected so as to take a gander at the

monetary changes of the firm (Accounitng Tools, 2018).

Reason for recording

Once the trial balance is prepared yet there are certain entries which the accountants fail to

record either intentionally to show the increased profit or unintentionally where the work load

is heavy. In both the scenarios the company must engage the accountant to pass the adjusting

journal entries to make the trial balance equal and worthy without any skip of even the

smallest transaction. That’s where the concept of the adjusting entries was introduced. The

adjusting entries are the way for the proper accounting treatment which organization must

follow and moreover the company have an advantage of the preparation of the trial balance

with the help of the recording of the adjusting entries. This can provide the advantage over

the competitors as they can have a rough idea by looking at their financial statements whether

the entries have been adjusted or not (Accounitng Tools, 2018).

Altering entries are recorded for the kind of the bookkeeping exchange, for example, to

record the devaluation and amortization of the period, to record a guarantee hold, when the

sales reserve account is made, or when any collected costs like prepaid insurance or rent or

advertising costs are recorded. Further, to address the month to month income figure the

adjusting entries play a crucial role in recording with the goal that the associations can get a

lucid image of their books of records. The best possible and the total learning of the adjusting

entries section help in knowing the eventual fate of the administrations. Accordingly these

journal entries help in picking the plans so business could get for the long haul advantage

(Blakely., 2018).

Purpose of writing an adjusted trial balance

The trial balance when have the certain entries to get adjust within a new trial balance is

prepared with the intention to correctly post all the transactions. This new trial balance is

known as the adjusted trail balance. The Adjusted trail balance can be prepared only after the

beginning since them to have happened. These entries can likewise be named as a monetary

announcing that redresses the misstep which have made in the earlier years when the trial

balance was prepared. The Adjusting Journal Entries is utilized to adjust and make the offset

with the accumulation idea. The Adjusting Journal Entries is passed just before the

arrangement of the budget reports to move the sum into the fiscal summaries and mirror the

unmistakable and the straightforward picture. To deal with the proper accounting treatment

the altering of the entries is vital and a greater picture is reflected so as to take a gander at the

monetary changes of the firm (Accounitng Tools, 2018).

Reason for recording

Once the trial balance is prepared yet there are certain entries which the accountants fail to

record either intentionally to show the increased profit or unintentionally where the work load

is heavy. In both the scenarios the company must engage the accountant to pass the adjusting

journal entries to make the trial balance equal and worthy without any skip of even the

smallest transaction. That’s where the concept of the adjusting entries was introduced. The

adjusting entries are the way for the proper accounting treatment which organization must

follow and moreover the company have an advantage of the preparation of the trial balance

with the help of the recording of the adjusting entries. This can provide the advantage over

the competitors as they can have a rough idea by looking at their financial statements whether

the entries have been adjusted or not (Accounitng Tools, 2018).

Altering entries are recorded for the kind of the bookkeeping exchange, for example, to

record the devaluation and amortization of the period, to record a guarantee hold, when the

sales reserve account is made, or when any collected costs like prepaid insurance or rent or

advertising costs are recorded. Further, to address the month to month income figure the

adjusting entries play a crucial role in recording with the goal that the associations can get a

lucid image of their books of records. The best possible and the total learning of the adjusting

entries section help in knowing the eventual fate of the administrations. Accordingly these

journal entries help in picking the plans so business could get for the long haul advantage

(Blakely., 2018).

Purpose of writing an adjusted trial balance

The trial balance when have the certain entries to get adjust within a new trial balance is

prepared with the intention to correctly post all the transactions. This new trial balance is

known as the adjusted trail balance. The Adjusted trail balance can be prepared only after the

BUSINESS ACCOUNTING 8

adjusting entries are made. Further the verification of the debit as well as the credit side can

be done in the best possible manner with the help of the adjusted trial balance (Bailin and

Battersby, 2016).

Adjusted trial balance is portrayed toward the finish of the accounting cycle. Setting up a fair

fundamental preliminary equalization will help in structure up the budget reports for a

specific term and before setting up adjusted starter preliminary adjusts the yearly changes are

necessary. The other clarification behind setting up the decent fundamental Trial Balance is

for ensuring that adjustments to the transaction have been recorded successfully. As indicated

by the last stage through the summary of the reports of the organization execution is the

significant standpoint according to the banks, financial specialists, reviewers and investors. In

the event that there is any fluctuation in the financial reports than it won't be acknowledged

by the clients of the announcements and for the purpose of the decision making (Banks,

2016).

Difference between the adjustment entries and closing journal entries

Closing entries are the entries that are recorded to close the books of the accounts whereas the

adjusting entries are those entries that are recoded to rectify the balances that have not taken

into account for the particular year and which should have been taken. The only difference

between the both the entries is the time frame of the recording and the purpose of the

recording (Dekker, 2016).

In the event of the adjusting entries, it is recorded toward the finish of the budgetary year

however before the arrangement of the monetary reports and these records are kept up as a

proof with the end goal of the association itself. Additionally the exceptional fiscal reports

will be useful for the organization and the clients of the equivalent. For example the

recording of the prepaid insurance rent that has been accounted for the current year is

recorded successfully (Bah and Fang, 2016).

Closing entries are recorded on the last day of the financial year but before the financial

statements are presented to its users. Most of the times the reports include the closing entries

recording as these entries help in creating the zero variance between the revenue and the

expenses incurred by the organization. This can also be understood with the simple fact that

the after the profit or loss is made in the company, the company will start with the new

figures, leaving the old ones in the previous years. Also there will some account which will

be carried forward as well (Accounting capital, 2019).

adjusting entries are made. Further the verification of the debit as well as the credit side can

be done in the best possible manner with the help of the adjusted trial balance (Bailin and

Battersby, 2016).

Adjusted trial balance is portrayed toward the finish of the accounting cycle. Setting up a fair

fundamental preliminary equalization will help in structure up the budget reports for a

specific term and before setting up adjusted starter preliminary adjusts the yearly changes are

necessary. The other clarification behind setting up the decent fundamental Trial Balance is

for ensuring that adjustments to the transaction have been recorded successfully. As indicated

by the last stage through the summary of the reports of the organization execution is the

significant standpoint according to the banks, financial specialists, reviewers and investors. In

the event that there is any fluctuation in the financial reports than it won't be acknowledged

by the clients of the announcements and for the purpose of the decision making (Banks,

2016).

Difference between the adjustment entries and closing journal entries

Closing entries are the entries that are recorded to close the books of the accounts whereas the

adjusting entries are those entries that are recoded to rectify the balances that have not taken

into account for the particular year and which should have been taken. The only difference

between the both the entries is the time frame of the recording and the purpose of the

recording (Dekker, 2016).

In the event of the adjusting entries, it is recorded toward the finish of the budgetary year

however before the arrangement of the monetary reports and these records are kept up as a

proof with the end goal of the association itself. Additionally the exceptional fiscal reports

will be useful for the organization and the clients of the equivalent. For example the

recording of the prepaid insurance rent that has been accounted for the current year is

recorded successfully (Bah and Fang, 2016).

Closing entries are recorded on the last day of the financial year but before the financial

statements are presented to its users. Most of the times the reports include the closing entries

recording as these entries help in creating the zero variance between the revenue and the

expenses incurred by the organization. This can also be understood with the simple fact that

the after the profit or loss is made in the company, the company will start with the new

figures, leaving the old ones in the previous years. Also there will some account which will

be carried forward as well (Accounting capital, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS ACCOUNTING 9

References

Accounitng Tools, 2018. Purpose of the trial balance [Online] Available from

https://www.accountingtools.com/articles/what-is-the-purpose-of-a-trial-balance.html

[Accessed on 31st may 2019]

Accounting capital, 2019. What are Closing Entries? [Online] Available from

https://www.accountingcapital.com/journal-entries/what-are-closing-entries/ [Accessed on

31st may 2019]

Akçay, S., 2018. A COMPARATIVE EVALUATION ON THE GENERAL ACCOUNTING

SYSTEMS OF TURKEY AND KAZAKHSTAN. CHANGING ORGANIZATIONS, p.87.

Bah, E.H. and Fang, L., 2016. Entry costs, financial frictions, and cross-country differences

in income and TFP. Macroeconomic Dynamics, 20(4), pp.884-908.

Bailin, S. and Battersby, M., 2016. Reason in the balance: An inquiry approach to critical

thinking. Hackett Publishing.

Banks, E., 2016. Dictionary of Finance, Investment and Banking. Springer.

Blakely., R. 2018. What Are Adjusting Entries? [Online] Available from

https://www.patriotsoftware.com/accounting/training/blog/adjusting-entries/ [Accessed on

31st may 2019]

Dekker, S., 2016. Just culture: Balancing safety and accountability. CRC Press.

Proformative, 2016. Trial Balance [Online] Available from

https://www.proformative.com/questions/adjusted-trial-balance [Accessed on 31st may 2019]

Salmon, J. and Wild, C., 2016. First Steps in SAP S/4HANA Finance.

References

Accounitng Tools, 2018. Purpose of the trial balance [Online] Available from

https://www.accountingtools.com/articles/what-is-the-purpose-of-a-trial-balance.html

[Accessed on 31st may 2019]

Accounting capital, 2019. What are Closing Entries? [Online] Available from

https://www.accountingcapital.com/journal-entries/what-are-closing-entries/ [Accessed on

31st may 2019]

Akçay, S., 2018. A COMPARATIVE EVALUATION ON THE GENERAL ACCOUNTING

SYSTEMS OF TURKEY AND KAZAKHSTAN. CHANGING ORGANIZATIONS, p.87.

Bah, E.H. and Fang, L., 2016. Entry costs, financial frictions, and cross-country differences

in income and TFP. Macroeconomic Dynamics, 20(4), pp.884-908.

Bailin, S. and Battersby, M., 2016. Reason in the balance: An inquiry approach to critical

thinking. Hackett Publishing.

Banks, E., 2016. Dictionary of Finance, Investment and Banking. Springer.

Blakely., R. 2018. What Are Adjusting Entries? [Online] Available from

https://www.patriotsoftware.com/accounting/training/blog/adjusting-entries/ [Accessed on

31st may 2019]

Dekker, S., 2016. Just culture: Balancing safety and accountability. CRC Press.

Proformative, 2016. Trial Balance [Online] Available from

https://www.proformative.com/questions/adjusted-trial-balance [Accessed on 31st may 2019]

Salmon, J. and Wild, C., 2016. First Steps in SAP S/4HANA Finance.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.