Accounting 7111AFE - Topic 2: Adjusting Process Homework Solution

VerifiedAdded on 2022/10/11

|4

|939

|15

Homework Assignment

AI Summary

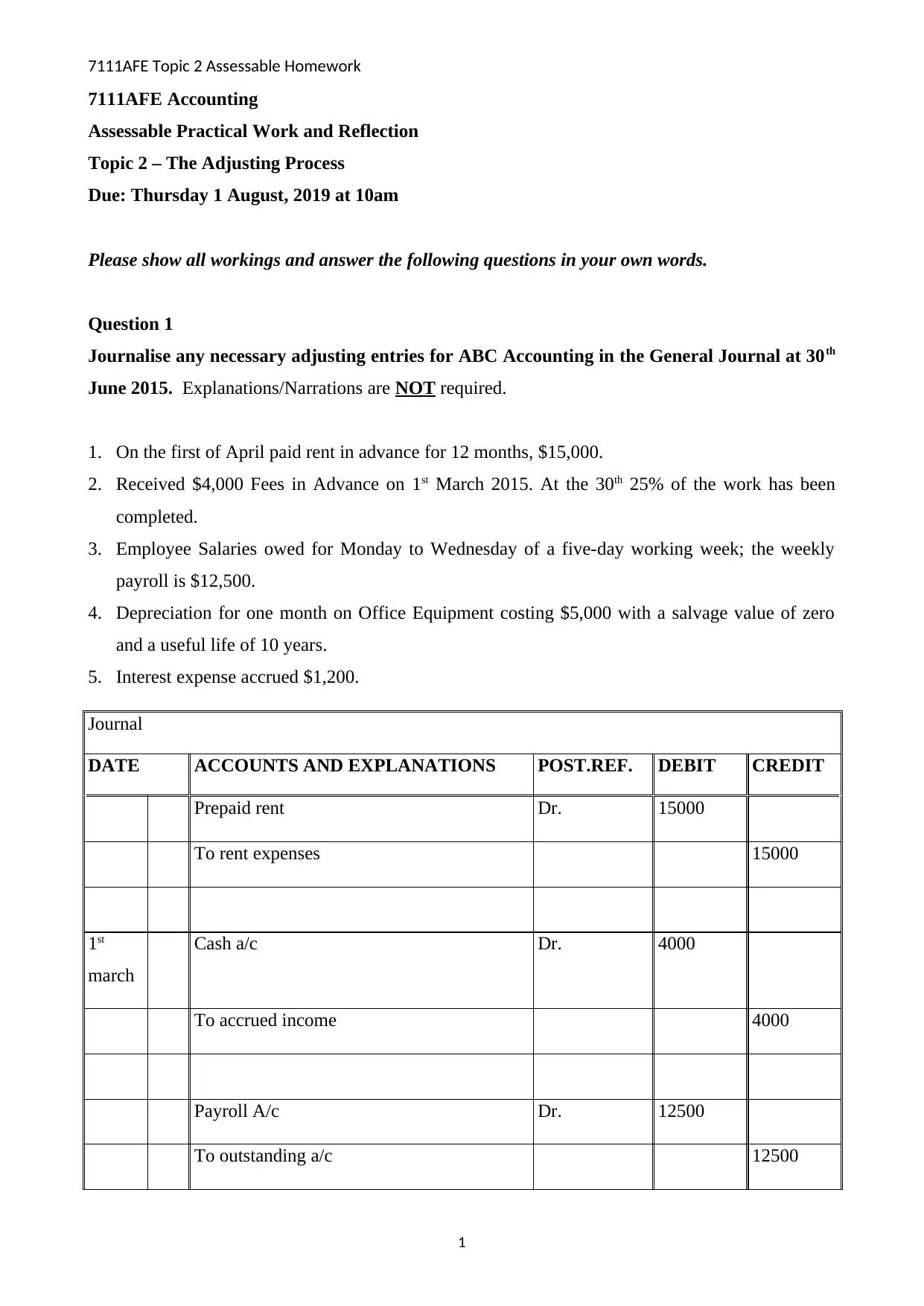

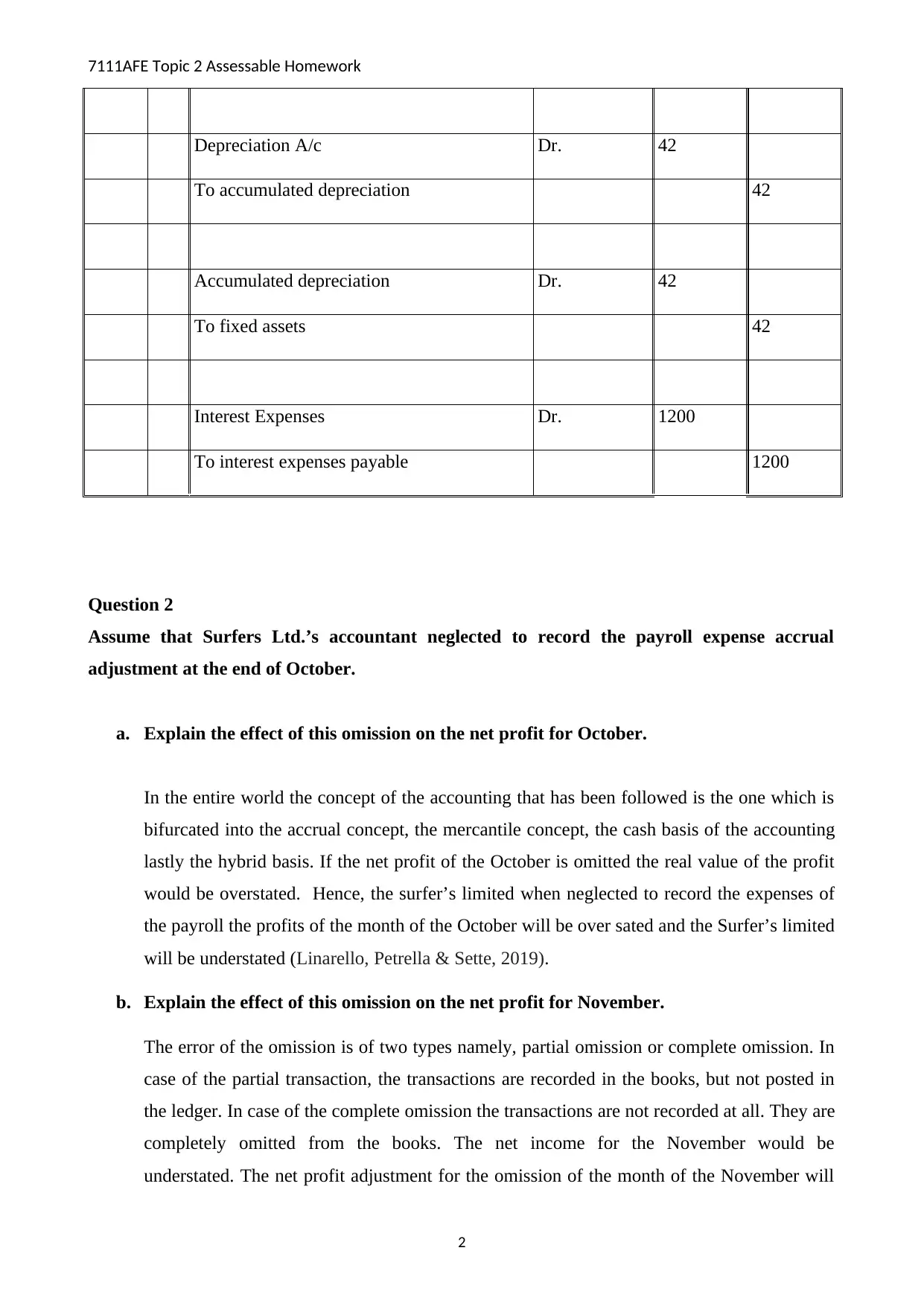

This document presents a complete solution to an accounting homework assignment focused on the adjusting process. The solution begins with journalizing adjusting entries for ABC Accounting, covering prepaid rent, fees in advance, employee salaries, depreciation, and accrued interest. It then analyzes the impact of omitting a payroll expense accrual adjustment on net profit for both October and November, explaining why the accrual adjustment is crucial for accurate financial reporting. Furthermore, the solution provides reasons why a company's cash generation might exceed its recorded profit, considering factors like the timing of cash flows relative to revenue recognition and the impact of asset sales. The assignment demonstrates a solid understanding of accrual accounting principles and the importance of accurate financial statement preparation.

1 out of 4

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.