EMBA Accounting Assignment: Adjusting Entries & Financial Statements

VerifiedAdded on 2022/08/14

|10

|598

|20

Homework Assignment

AI Summary

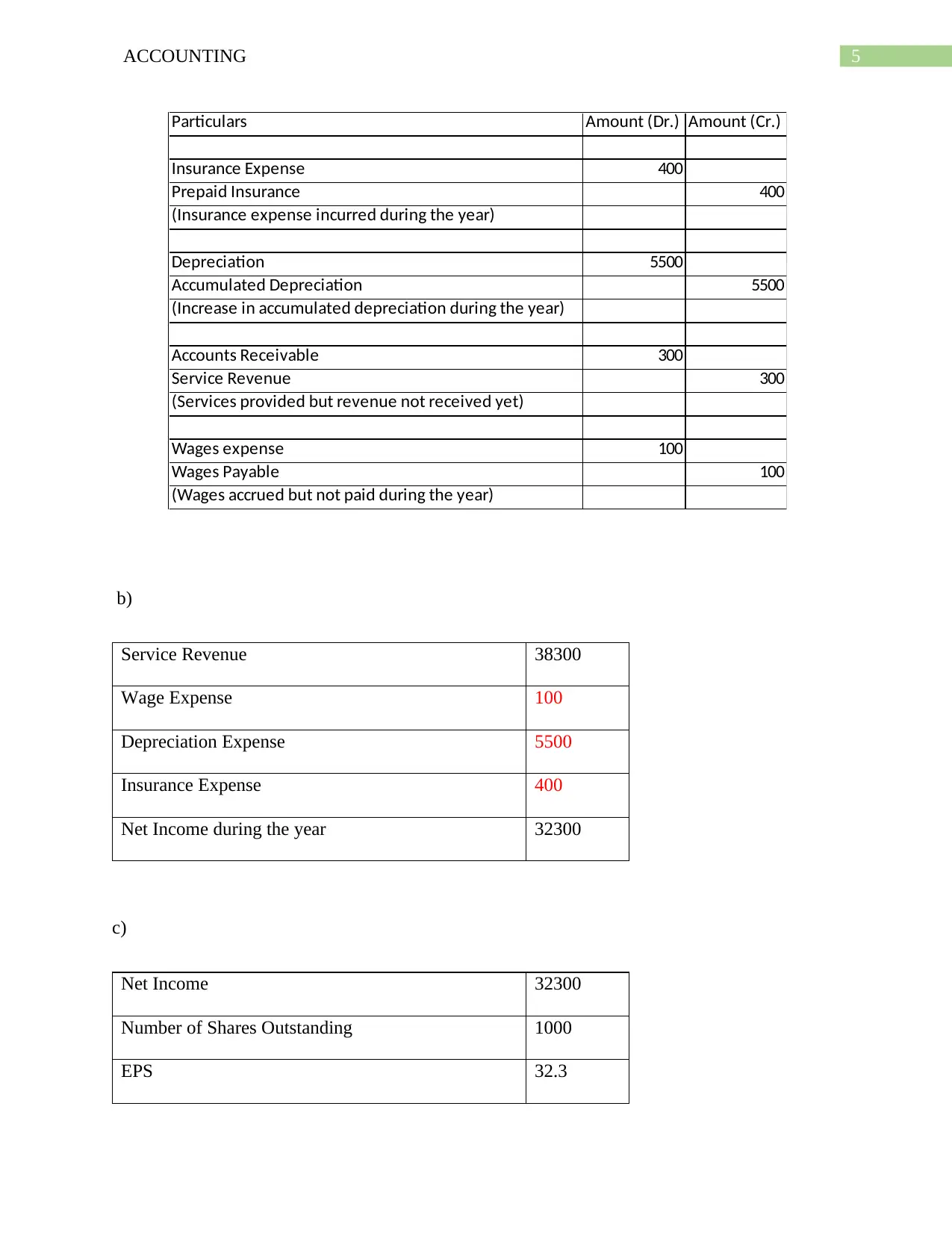

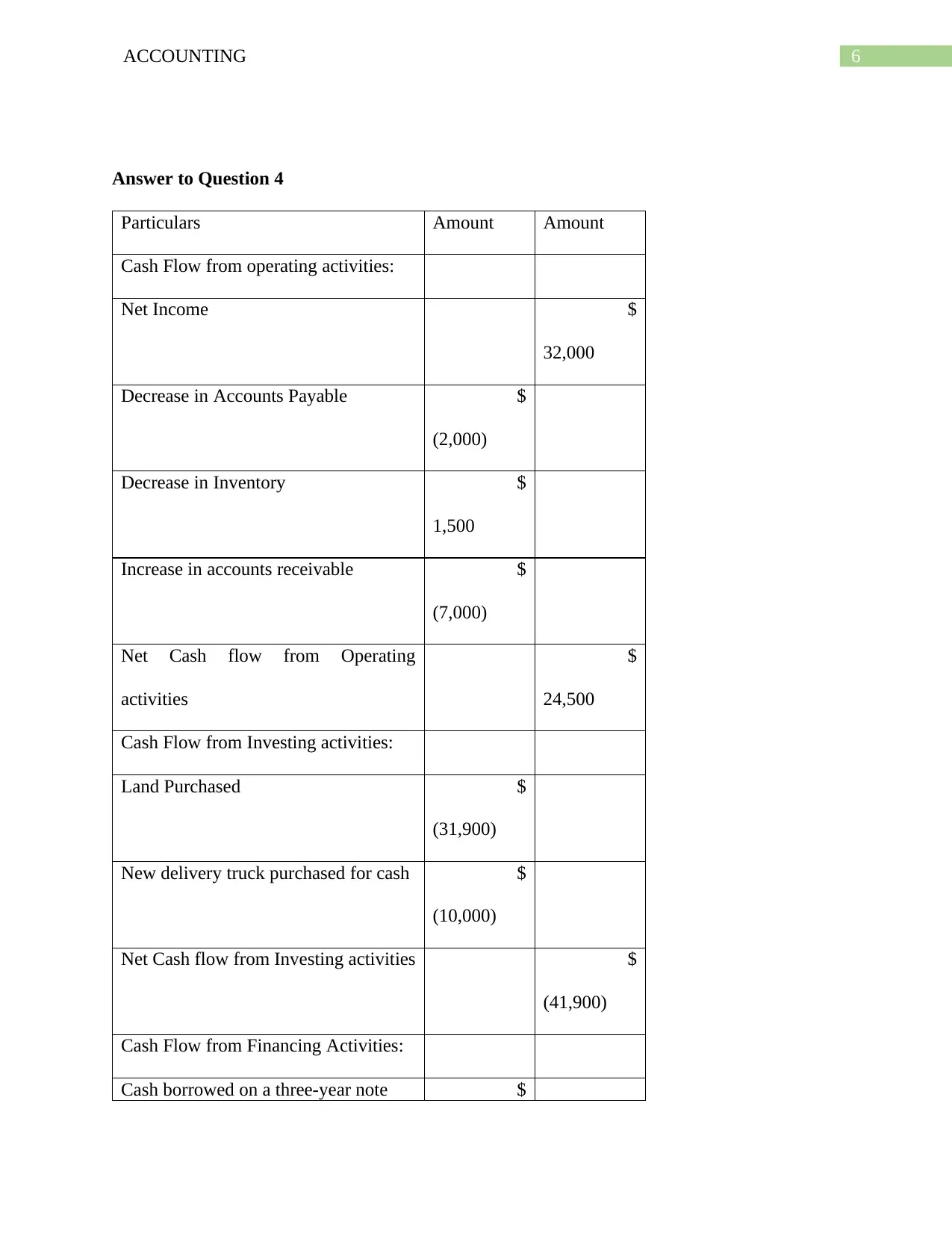

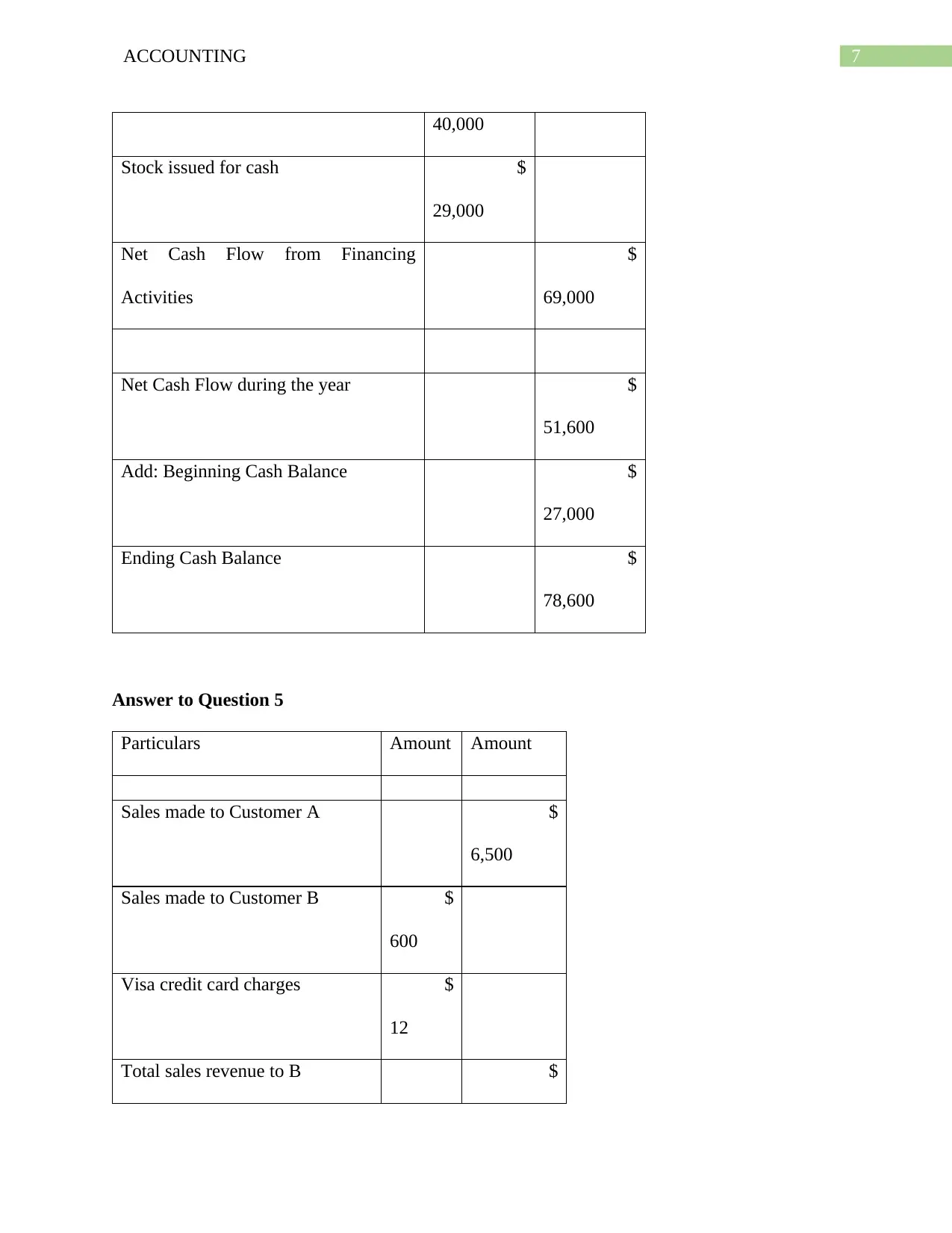

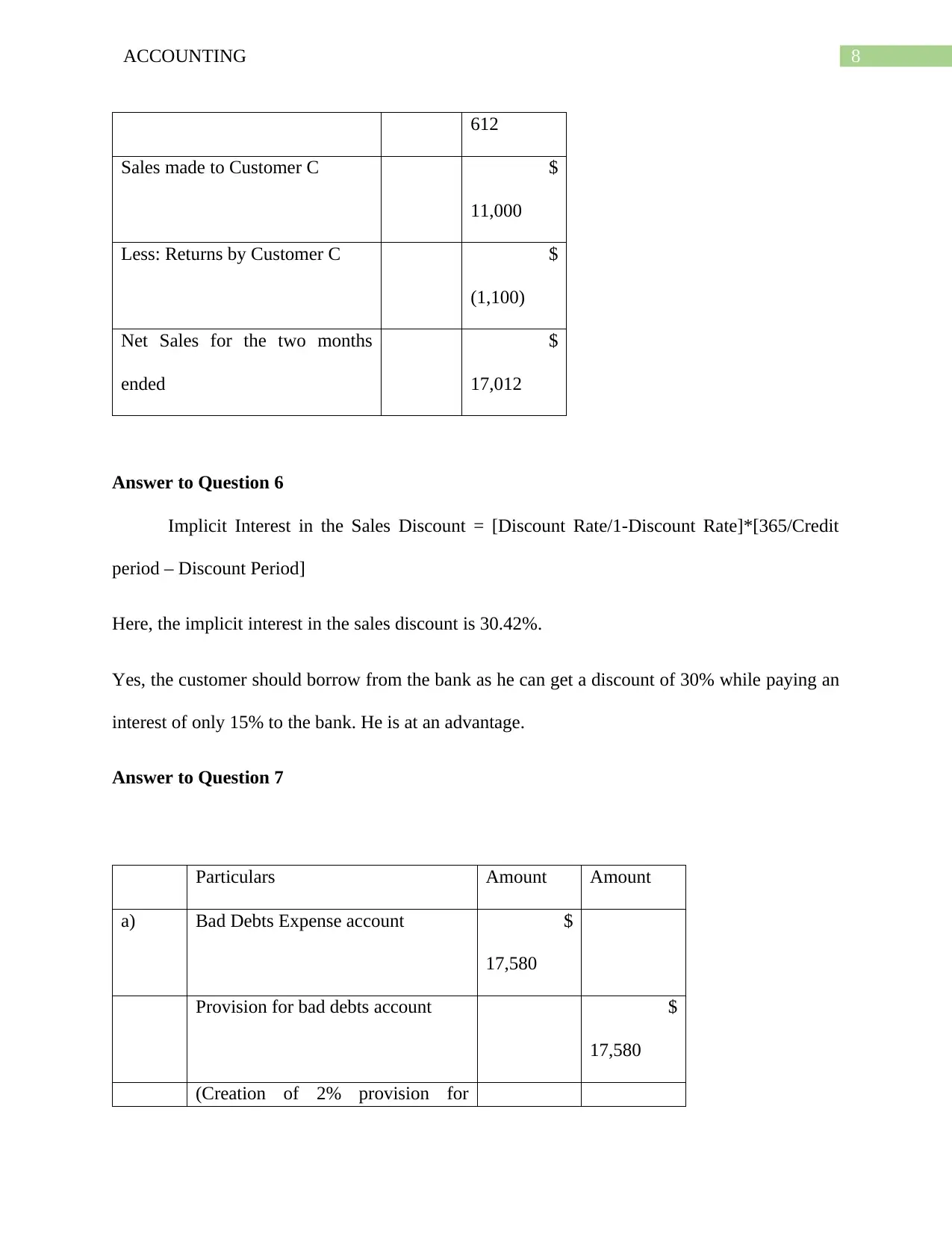

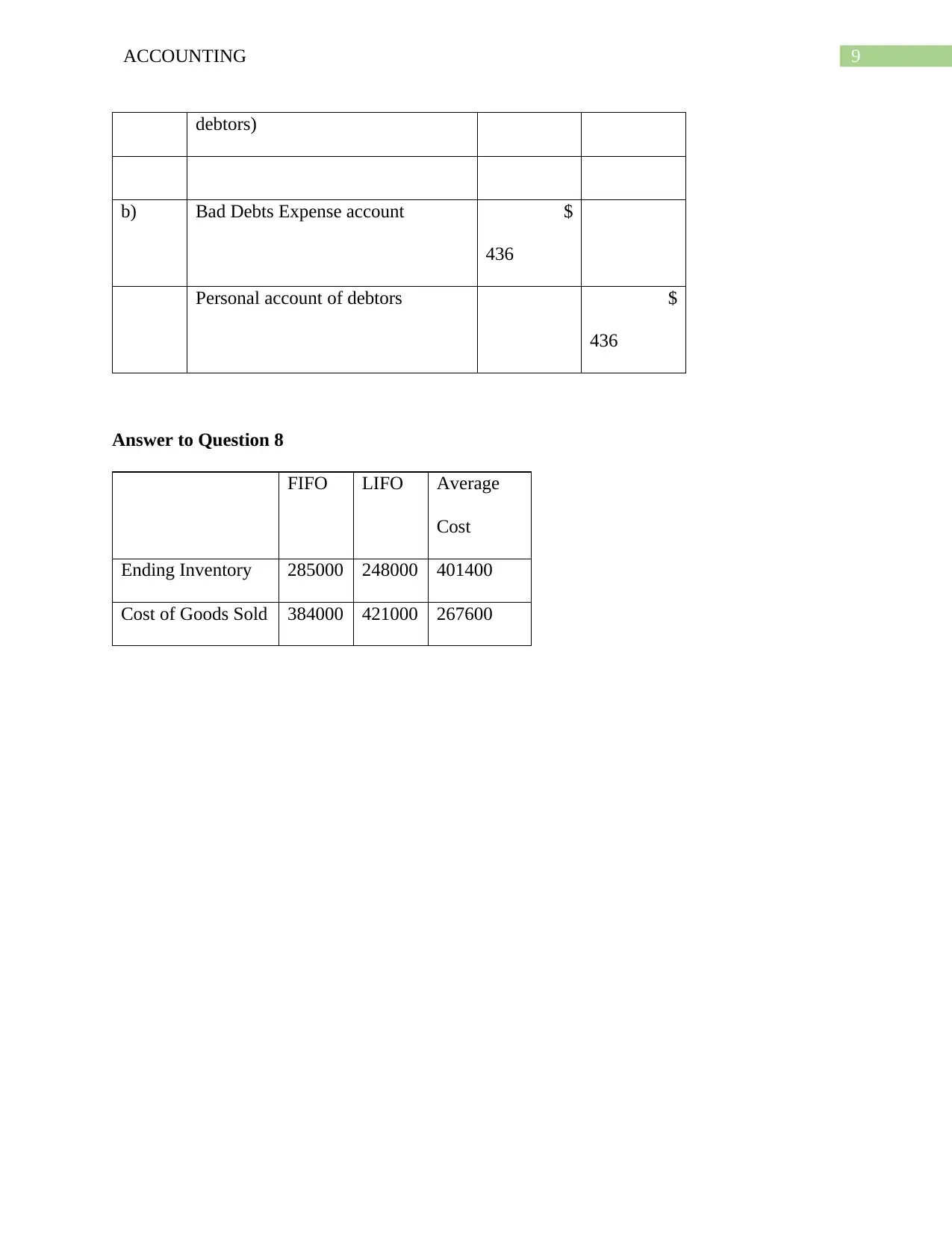

This accounting assignment solution addresses various aspects of adjusting entries, closing processes, and the preparation of financial statements for Markham Industries. It includes detailed calculations and explanations for accrued revenues and expenses, deferred revenues and expenses, depreciation, insurance, and rent. The solution also presents balance sheet and income statement excerpts, earnings per share (EPS) calculation, cash flow statement preparation, sales revenue analysis, implicit interest rate determination in sales discounts, bad debt expense accounting, and inventory valuation using FIFO, LIFO, and average cost methods. The assignment provides a comprehensive overview of key accounting principles and their practical application in financial reporting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.