Dealing with Accounting Adjustments: Biological Assets & Inventory

VerifiedAdded on 2023/06/11

|9

|1849

|307

Report

AI Summary

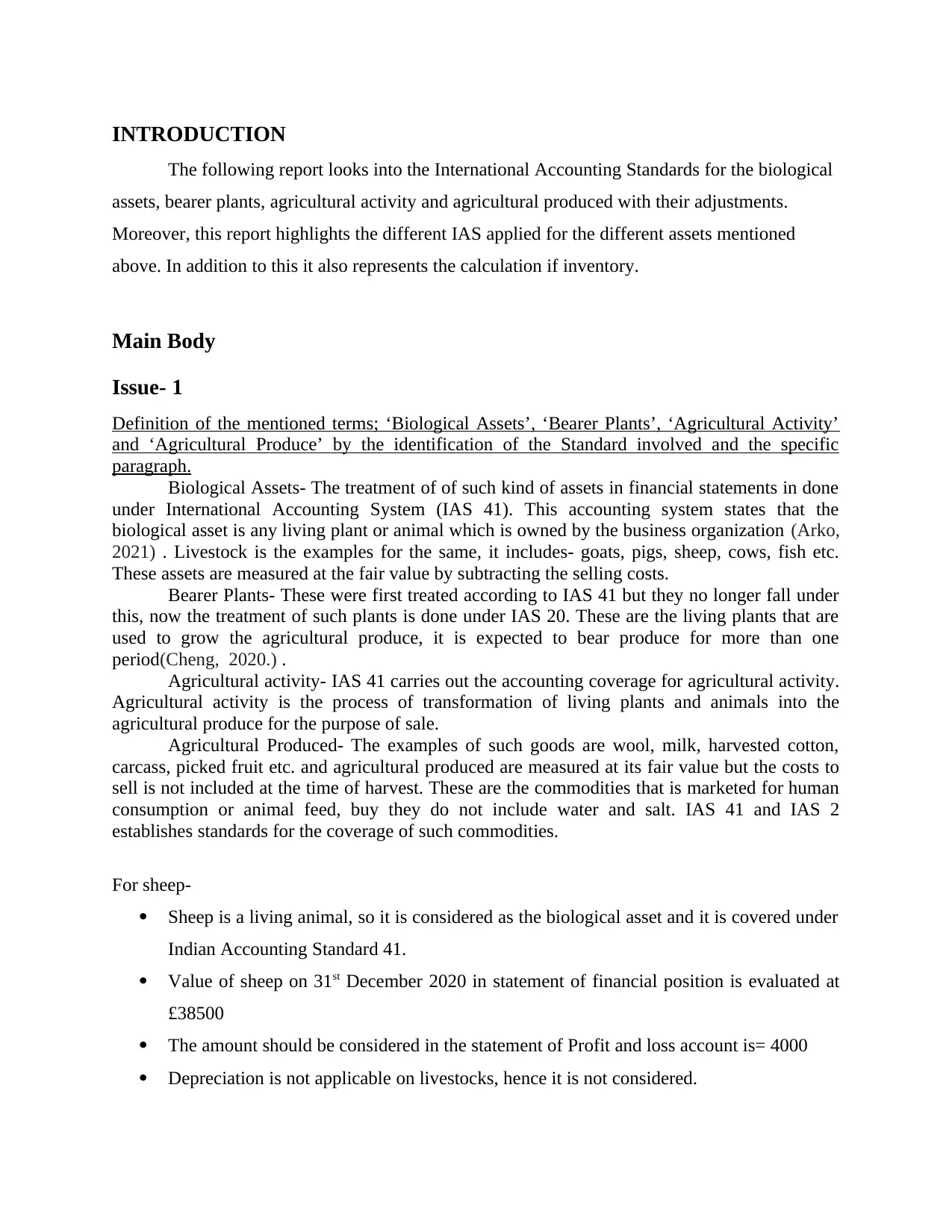

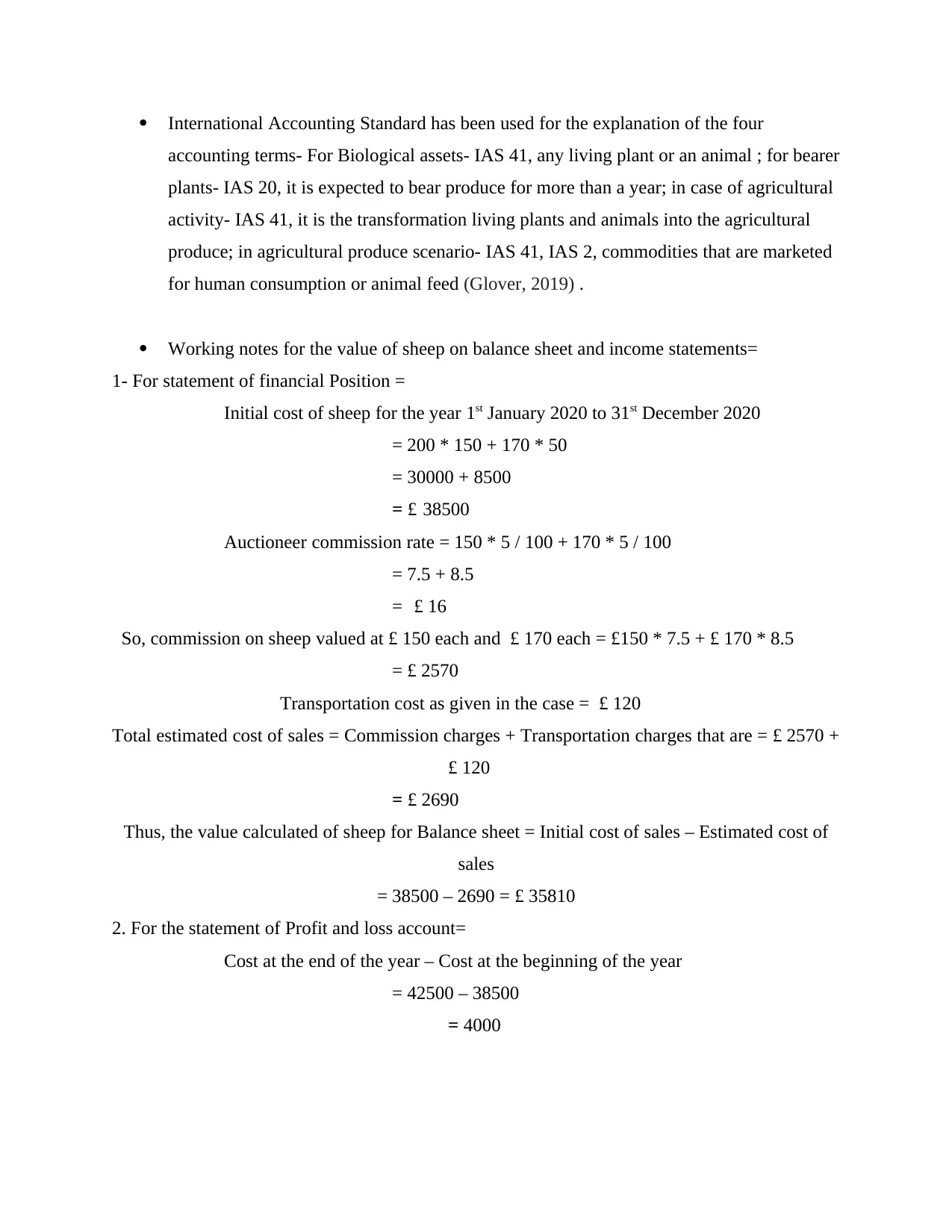

This report provides a detailed analysis of accounting adjustments related to International Accounting Standards (IAS), specifically focusing on biological assets, bearer plants, agricultural activity, and agricultural produce. It identifies and explains the relevant IAS standards, including IAS 41 for biological assets and agricultural activity, IAS 16 for property, plant, and equipment (land), and IAS 2 for inventory. The report includes calculations for determining the value of sheep as biological assets, the valuation of land, and the accounting treatment of grapevines, considering factors like initial cost, fair value changes, and depreciation. Furthermore, it addresses the valuation of agricultural produce such as wool, milk, and wine, emphasizing the lower of cost or net realizable value method for inventory. The report concludes by summarizing the application of different IAS standards in accounting for these various asset types, providing clarity on their treatment in financial statements. Desklib offers a wide range of solved assignments and past papers for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.