Management Accounting Report: Systems, Costs, and Budgeting at Agmet

VerifiedAdded on 2021/01/03

|15

|5447

|268

Report

AI Summary

This report provides a comprehensive analysis of Agmet Ltd's management accounting practices. It begins with an introduction to management accounting and its various types, including cost accounting, price optimization, inventory management, and job costing systems. The report then delves into management accounting reporting, covering performance reporting, inventory management reporting, job cost reporting, and account receivable reporting. The core of the report focuses on cost calculation techniques, specifically marginal costing and absorption costing, providing detailed calculations. Furthermore, the report examines budgetary control, outlining different planning tools and their advantages and disadvantages. The report also explores how management accounting systems respond to financial problems and contribute to an organization's sustainable success. The report concludes with a summary of the key findings and recommendations for Agmet Ltd's financial management strategies.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Management accounting reporting and its types..................................................................2

M1: Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................4

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2: Various types of accounting techniques and financial reporting documents......................6

TASK 3............................................................................................................................................7

P4: Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control.....................................................................................7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Management accounting reporting and its types..................................................................2

M1: Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................4

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2: Various types of accounting techniques and financial reporting documents......................6

TASK 3............................................................................................................................................7

P4: Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control.....................................................................................7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a process of providing all the internal data to stakeholders of

the company. It helps in preparing several managements reports which determine the amount of

cash, incomes, expenses, outstanding payments and accrued gains etc. of the company.

Management accounting assist in evaluating accurate financial data to the management which is

necessary for company's operations. Agmet Ltd is a leading recycler and manufacturer which is

located in Reading, UK. It provides innovative and high quality chemicals products to customers.

In this report, company follows essential management accounting systems and reporting

methods which helps in creating accurate reports. Company determine cost and net profit of its

product using appropriate techniques. Its also analysis various budgetary control planning

techniques and identify accounting systems to respond to financial problems.

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting is an approach of identification, measurement, collection,

interpretation and communication of financial data that is used by management in planning,

controlling it's operations. The aim of management accounting is to aid company in making

effective qualitative decisions. Management accounting system refer to internal system which a

company uses to measure and evaluate it's processes or activities. Agmet Ltd uses several

management accounting system which help in determining it's accurate information to internal

and external stakeholders. These systems assist in making plans and policies which increase

company's performance and profitability. Cost accounting, price optimisation, inventory

management and job costing systems are the different types of management accounting that

Agmet Ltd follow (Agrawal and Cooper, 2017). These systems are described below:

Cost Accounting System: This system refers to accumulated cost of raw material that a

manufacturer use in its production activities. These material processed through several

production stages like raw material, work in progress, finished goods in a particular time period.

So, this system is an essential for Agmet Ltd to evaluate accurate cost of its product that is

important for efficient delivery to manufacturing plants. Company measures and details the cost

of product i.e. chemicals separately then compare actual outcomes with standard and input

results with outputs. By this comparison managers of Agmet Ltd get actual data that helps in

1

Management accounting is a process of providing all the internal data to stakeholders of

the company. It helps in preparing several managements reports which determine the amount of

cash, incomes, expenses, outstanding payments and accrued gains etc. of the company.

Management accounting assist in evaluating accurate financial data to the management which is

necessary for company's operations. Agmet Ltd is a leading recycler and manufacturer which is

located in Reading, UK. It provides innovative and high quality chemicals products to customers.

In this report, company follows essential management accounting systems and reporting

methods which helps in creating accurate reports. Company determine cost and net profit of its

product using appropriate techniques. Its also analysis various budgetary control planning

techniques and identify accounting systems to respond to financial problems.

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting is an approach of identification, measurement, collection,

interpretation and communication of financial data that is used by management in planning,

controlling it's operations. The aim of management accounting is to aid company in making

effective qualitative decisions. Management accounting system refer to internal system which a

company uses to measure and evaluate it's processes or activities. Agmet Ltd uses several

management accounting system which help in determining it's accurate information to internal

and external stakeholders. These systems assist in making plans and policies which increase

company's performance and profitability. Cost accounting, price optimisation, inventory

management and job costing systems are the different types of management accounting that

Agmet Ltd follow (Agrawal and Cooper, 2017). These systems are described below:

Cost Accounting System: This system refers to accumulated cost of raw material that a

manufacturer use in its production activities. These material processed through several

production stages like raw material, work in progress, finished goods in a particular time period.

So, this system is an essential for Agmet Ltd to evaluate accurate cost of its product that is

important for efficient delivery to manufacturing plants. Company measures and details the cost

of product i.e. chemicals separately then compare actual outcomes with standard and input

results with outputs. By this comparison managers of Agmet Ltd get actual data that helps in

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

evaluating its cost accounting strategies. With the aid of this strategies manager track the inside

cost of product for a particular project and record cost of each activities at all levels of

production.

Price Optimisation System: This system helps in determining the proper price of

product or services. This system works as calculating the demand of product at different price

levels. Price optimisation system help organisation in determining their initial pricing i.e. product

secure base for long run, promotional pricing like setting temporary prices of product to increase

its sales and discounting pricing such as selling product according to trends. Agmet Ltd uses this

system as a pricing strategy for finding that optimum price of product which a customer is

willing to pay. The basis requirement of using this system to analyse the perception of customer

regarding the product offer by the company.(Anderson and Dekker, 2014).

Inventory Management System: This system used to track inflow and outflow of

inventory at different stages of production. It also helps in managing overall information of

inventory in process, warehouse or it market. FIFO, LIFO and weighted average are the methods

of inventory valuation. Agmet Ltd use inventory management system for monitoring,

controlling, directing the flow of product in the operations. It also identify chemicals stock in

process and its availability in the storage. This minimizes the risk of improper inventory

management in the company by controlling and managing the product demand in future.

Job cost System: This system identify the manufacturing costs of product at various job

levels. In this system accountant can track each job by maintaining information which is often

related to company's operations. This system is used in situation where every job is different and

is performed according to the customer's specification. Agmet Ltd is dealing in manufacturing

chemicals and supply it's products to clients. Therefore company deal in two different jobs and

follow process costing system to determine the costs and revenues of its product used in different

levels of job. This system helps in evaluating its actual cost and performance involved in each

jobs i.e. manufacturing and distributing.

P2. Management accounting reporting and its types

Management accounting reporting is an important method of collecting information

through company's accounting records. This details helps in preparing effective management

accounting reports. These reports display fair information that are useful for its managers and

stakeholders. Reports are very clear and easy to understand for stakeholders such as customer

2

cost of product for a particular project and record cost of each activities at all levels of

production.

Price Optimisation System: This system helps in determining the proper price of

product or services. This system works as calculating the demand of product at different price

levels. Price optimisation system help organisation in determining their initial pricing i.e. product

secure base for long run, promotional pricing like setting temporary prices of product to increase

its sales and discounting pricing such as selling product according to trends. Agmet Ltd uses this

system as a pricing strategy for finding that optimum price of product which a customer is

willing to pay. The basis requirement of using this system to analyse the perception of customer

regarding the product offer by the company.(Anderson and Dekker, 2014).

Inventory Management System: This system used to track inflow and outflow of

inventory at different stages of production. It also helps in managing overall information of

inventory in process, warehouse or it market. FIFO, LIFO and weighted average are the methods

of inventory valuation. Agmet Ltd use inventory management system for monitoring,

controlling, directing the flow of product in the operations. It also identify chemicals stock in

process and its availability in the storage. This minimizes the risk of improper inventory

management in the company by controlling and managing the product demand in future.

Job cost System: This system identify the manufacturing costs of product at various job

levels. In this system accountant can track each job by maintaining information which is often

related to company's operations. This system is used in situation where every job is different and

is performed according to the customer's specification. Agmet Ltd is dealing in manufacturing

chemicals and supply it's products to clients. Therefore company deal in two different jobs and

follow process costing system to determine the costs and revenues of its product used in different

levels of job. This system helps in evaluating its actual cost and performance involved in each

jobs i.e. manufacturing and distributing.

P2. Management accounting reporting and its types

Management accounting reporting is an important method of collecting information

through company's accounting records. This details helps in preparing effective management

accounting reports. These reports display fair information that are useful for its managers and

stakeholders. Reports are very clear and easy to understand for stakeholders such as customer

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and investors. Agmet Ltd prepares several types of management accounting reports like

performance, inventory management, job costing and account receivable reports for determining

and maintaining its financial position in future also (Bennett and James, 2017). The different

types of management accounting reporting are explained below:

Performance Reporting: This reporting method used to evaluate regular performance of

the company on the basis of collection and distribution of project data, communication of

information or progresses to stakeholders. This reporting system includes a summary of past

performance, modification in reporting period, any risks in present status etc. Agmet Ltd use

performance reporting method for comparing its actual performance with past. It also evaluate

the variation in production and distribution of its current performance with standard.

Performance reporting aid in future growth of company within various departments. On the basis

of this reporting, company define certain rules and regulations for managers at various level.

These rules helps in determining errors and resolve it on time which is important for improving

company's performance.

Inventory Management Reporting: This reporting technique refers to status, analyse

and integration of inventory at different level of production and distribution. This report includes

analysing and reviewing information about the inventory. Agmet Ltd use inventory management

reporting to determine chemicals status by location, time period etc. It also analyse report to

evaluate product demand, profitability, turnover etc. and review the variance between product

information and accounting information. This reports give accurate information about company's

inventory which helps manager in dealing with over or out of stock situations. It also helps in

creating effective reports (Bennett and James, 2017).

Job Cost reporting: This reporting method shows a lists of each job in which company

works and the total cost incurred on the job in the previous period. Job costs like material, labour

cost, overhead etc. which can be directly related to a job are appears in this report. Agmet Ltd

use job cost reporting for identifying issues such as excess of expenses in manufacturing process

relevant to current job. It ignores this issues in future by minimizing excesses of spending which

helps in generating revenues.

Account Receivable Reporting: This report shows due amount on customers that a

company recovers within a specific time period. This report consist of both summarized and

detailed list of customer's previous and present due invoices, debit memos, cash amounts and on

3

performance, inventory management, job costing and account receivable reports for determining

and maintaining its financial position in future also (Bennett and James, 2017). The different

types of management accounting reporting are explained below:

Performance Reporting: This reporting method used to evaluate regular performance of

the company on the basis of collection and distribution of project data, communication of

information or progresses to stakeholders. This reporting system includes a summary of past

performance, modification in reporting period, any risks in present status etc. Agmet Ltd use

performance reporting method for comparing its actual performance with past. It also evaluate

the variation in production and distribution of its current performance with standard.

Performance reporting aid in future growth of company within various departments. On the basis

of this reporting, company define certain rules and regulations for managers at various level.

These rules helps in determining errors and resolve it on time which is important for improving

company's performance.

Inventory Management Reporting: This reporting technique refers to status, analyse

and integration of inventory at different level of production and distribution. This report includes

analysing and reviewing information about the inventory. Agmet Ltd use inventory management

reporting to determine chemicals status by location, time period etc. It also analyse report to

evaluate product demand, profitability, turnover etc. and review the variance between product

information and accounting information. This reports give accurate information about company's

inventory which helps manager in dealing with over or out of stock situations. It also helps in

creating effective reports (Bennett and James, 2017).

Job Cost reporting: This reporting method shows a lists of each job in which company

works and the total cost incurred on the job in the previous period. Job costs like material, labour

cost, overhead etc. which can be directly related to a job are appears in this report. Agmet Ltd

use job cost reporting for identifying issues such as excess of expenses in manufacturing process

relevant to current job. It ignores this issues in future by minimizing excesses of spending which

helps in generating revenues.

Account Receivable Reporting: This report shows due amount on customers that a

company recovers within a specific time period. This report consist of both summarized and

detailed list of customer's previous and present due invoices, debit memos, cash amounts and on

3

account credits etc. This report is also known as aging report because it determine the age of

certain items. Agmet Ltd use account receivable reporting method that assist in identifying the

list of unpaid customers invoice, average collection period and credit customers. With the help of

this report company will try to recover its due amount frequently and minimize the list of

creditors. It also maximize its average collection period which helps company to increase

chemicals sells (Ding, Dekker and Groot, 2013).

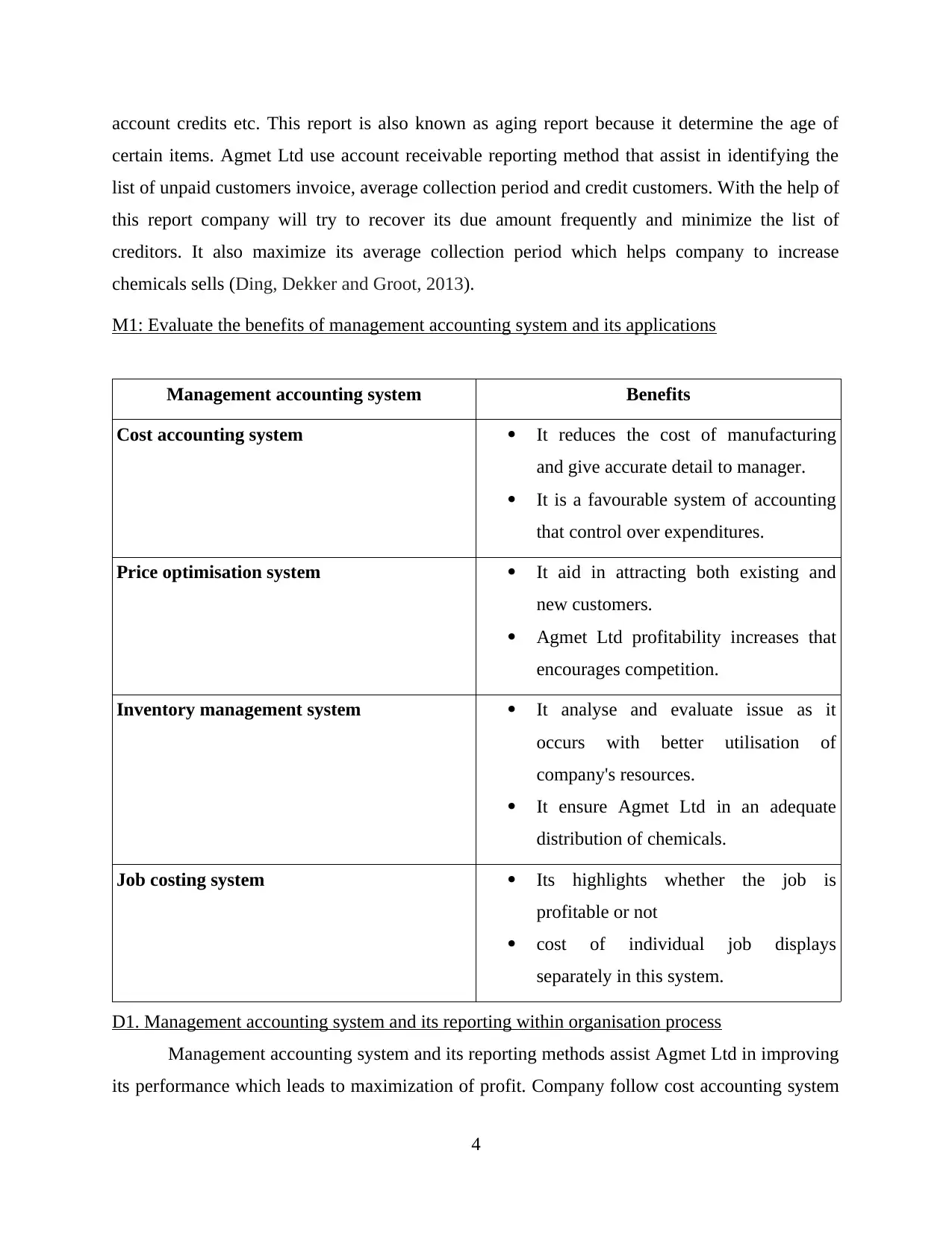

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It reduces the cost of manufacturing

and give accurate detail to manager.

It is a favourable system of accounting

that control over expenditures.

Price optimisation system It aid in attracting both existing and

new customers.

Agmet Ltd profitability increases that

encourages competition.

Inventory management system It analyse and evaluate issue as it

occurs with better utilisation of

company's resources.

It ensure Agmet Ltd in an adequate

distribution of chemicals.

Job costing system Its highlights whether the job is

profitable or not

cost of individual job displays

separately in this system.

D1. Management accounting system and its reporting within organisation process

Management accounting system and its reporting methods assist Agmet Ltd in improving

its performance which leads to maximization of profit. Company follow cost accounting system

4

certain items. Agmet Ltd use account receivable reporting method that assist in identifying the

list of unpaid customers invoice, average collection period and credit customers. With the help of

this report company will try to recover its due amount frequently and minimize the list of

creditors. It also maximize its average collection period which helps company to increase

chemicals sells (Ding, Dekker and Groot, 2013).

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It reduces the cost of manufacturing

and give accurate detail to manager.

It is a favourable system of accounting

that control over expenditures.

Price optimisation system It aid in attracting both existing and

new customers.

Agmet Ltd profitability increases that

encourages competition.

Inventory management system It analyse and evaluate issue as it

occurs with better utilisation of

company's resources.

It ensure Agmet Ltd in an adequate

distribution of chemicals.

Job costing system Its highlights whether the job is

profitable or not

cost of individual job displays

separately in this system.

D1. Management accounting system and its reporting within organisation process

Management accounting system and its reporting methods assist Agmet Ltd in improving

its performance which leads to maximization of profit. Company follow cost accounting system

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for determining exact cost of product at the time of manufacturing. It set a price strategies under

prime optimisation system in order to target more customers by increasing its product demand.

Agmet Ltd follow inventory management system and reporting to balance its inflow and outflow

of inventory. Its also works under two job like manufacturer and distributors of chemicals so,

they follow process job costing system for identifying individual job costs and revenues.

Account receivable reporting helps in determining average collection period. Above these

systems helps Agmet Ltd in preparing their reporting techniques more effective.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is monetary value which is used in creating a product, need in running an

organisation or execute its operations. It is an amount that buyer pays to seller for buying a

particular product. Agmet Ltd want to set a right cost for its product which is increasing

customer's purchasing power. Here right cost refers to that cost which is bearable by both

company and customers (Dalla Via, 2012).

Marginal costing: It is a cost of additional unit which is added to the production. Agmet

Ltd use marginal costing technique for determining variable cost that charge to extra level of

production. It assist in profit planning, cost control and managerial decision making.

Absorption costing: This method is used to absorbed all the cost which are incurred in

the production when same product is sold. This technique is used by Agmet Ltd in determining

the budgeted cost which involved in manufacturing process.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 320

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

5

prime optimisation system in order to target more customers by increasing its product demand.

Agmet Ltd follow inventory management system and reporting to balance its inflow and outflow

of inventory. Its also works under two job like manufacturer and distributors of chemicals so,

they follow process job costing system for identifying individual job costs and revenues.

Account receivable reporting helps in determining average collection period. Above these

systems helps Agmet Ltd in preparing their reporting techniques more effective.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is monetary value which is used in creating a product, need in running an

organisation or execute its operations. It is an amount that buyer pays to seller for buying a

particular product. Agmet Ltd want to set a right cost for its product which is increasing

customer's purchasing power. Here right cost refers to that cost which is bearable by both

company and customers (Dalla Via, 2012).

Marginal costing: It is a cost of additional unit which is added to the production. Agmet

Ltd use marginal costing technique for determining variable cost that charge to extra level of

production. It assist in profit planning, cost control and managerial decision making.

Absorption costing: This method is used to absorbed all the cost which are incurred in

the production when same product is sold. This technique is used by Agmet Ltd in determining

the budgeted cost which involved in manufacturing process.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 320

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

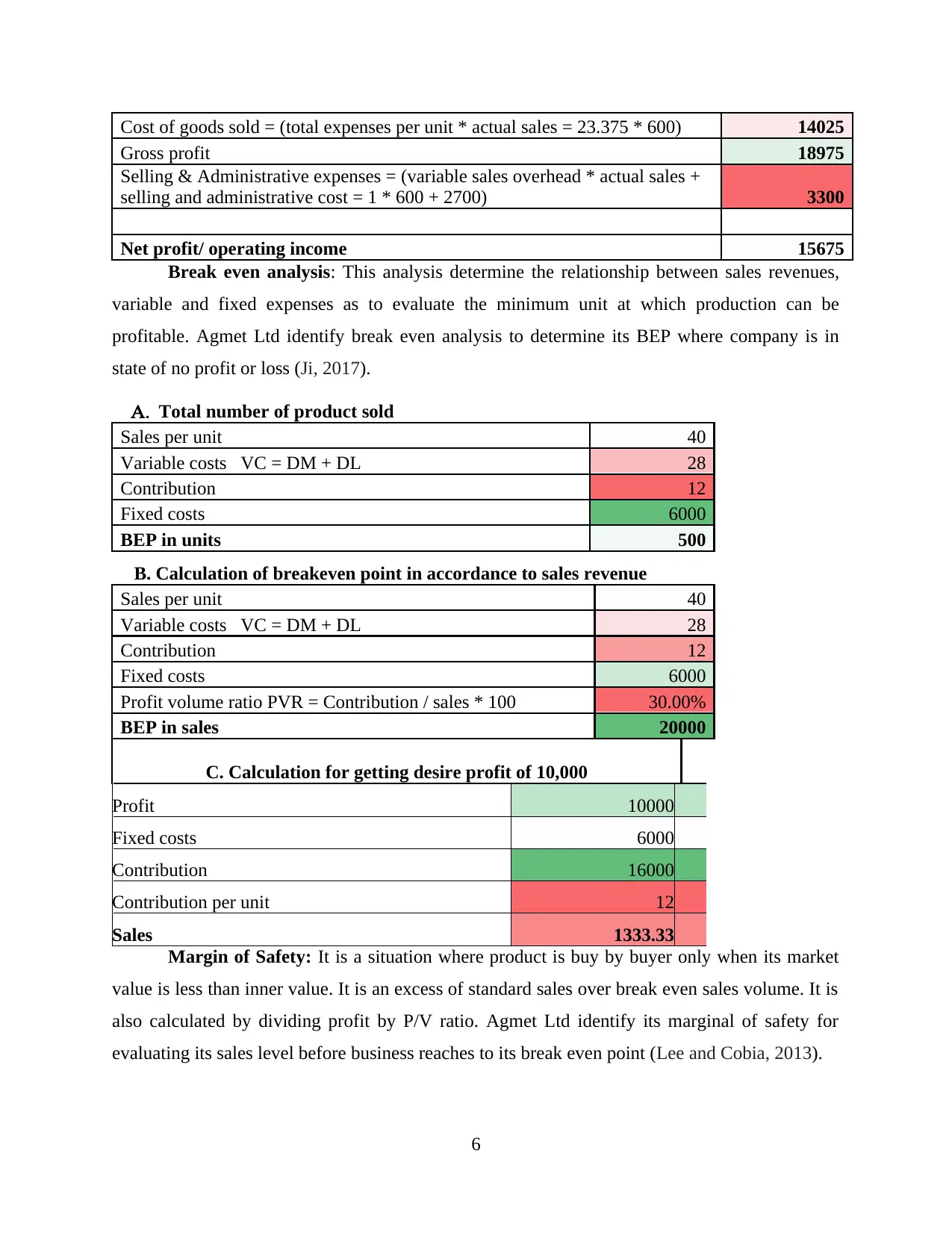

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: This analysis determine the relationship between sales revenues,

variable and fixed expenses as to evaluate the minimum unit at which production can be

profitable. Agmet Ltd identify break even analysis to determine its BEP where company is in

state of no profit or loss (Ji, 2017).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is a situation where product is buy by buyer only when its market

value is less than inner value. It is an excess of standard sales over break even sales volume. It is

also calculated by dividing profit by P/V ratio. Agmet Ltd identify its marginal of safety for

evaluating its sales level before business reaches to its break even point (Lee and Cobia, 2013).

6

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: This analysis determine the relationship between sales revenues,

variable and fixed expenses as to evaluate the minimum unit at which production can be

profitable. Agmet Ltd identify break even analysis to determine its BEP where company is in

state of no profit or loss (Ji, 2017).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is a situation where product is buy by buyer only when its market

value is less than inner value. It is an excess of standard sales over break even sales volume. It is

also calculated by dividing profit by P/V ratio. Agmet Ltd identify its marginal of safety for

evaluating its sales level before business reaches to its break even point (Lee and Cobia, 2013).

6

M2: Various types of accounting techniques and financial reporting documents

Techniques of managerial accounting are used by Agmet Ltd for short and long project

decision making and it also help to record operational measurement in a company. Concepts like

standard costing are used for controlling cost and it shows the difference between actual and

expected cost, marginal costing is use to find additional cost spent over production of additional

unit of output and historical costing that provide past data for each type of cost so that

comparison may be easy and will benefit in cost control.

D2: Data interpretation

Resulted from the above calculation it is easy to say that marginal costing method will

provide more benefit to Agmet Ltd as compared to an other method. As, profit generated from

marginal costing approach is about £17500 and from absorption costing method it is £15675. It is

clear from the result that marginal costing approach give £1825 amount more as a result.

Acording to break even analysis, if Agmet Ltd sell 500units at £40 per unit it will be generating

sales revenue of £20000 to reach break even. If company wants to earn desired profit of £10000

they have to swll 1333.33 units. Similarly, if company is willing to sell 800 units the margin of

safety is 37.5%.

TASK 3

P4: Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control.

Budgetary control: This system of management refer to how well their manager uilize

past or present result to monitor and control its existing cost and operation in an accounting

peorid to maximise their future profit. Agmet Ltd is a producer and distributor of various

chemical, so their management must set predefined financial and performance goals with

budgets, compare those actual result, and adjust performance of their company if needed. If

management of Agmet Ltd is able to have a proper budgetary control then it will be advantage

company in many ways like proper co-ordination, important tool to measure performance,

maximisation of profit, economic growth, help to reduce production cost etc. (Maskell, Baggaley

and Grasso, 2016).

Management of Agmet Ltd take following steps in budgetary control process. First, they

set performance budget/goals that management wants to achieve like production or sales goals.

7

Techniques of managerial accounting are used by Agmet Ltd for short and long project

decision making and it also help to record operational measurement in a company. Concepts like

standard costing are used for controlling cost and it shows the difference between actual and

expected cost, marginal costing is use to find additional cost spent over production of additional

unit of output and historical costing that provide past data for each type of cost so that

comparison may be easy and will benefit in cost control.

D2: Data interpretation

Resulted from the above calculation it is easy to say that marginal costing method will

provide more benefit to Agmet Ltd as compared to an other method. As, profit generated from

marginal costing approach is about £17500 and from absorption costing method it is £15675. It is

clear from the result that marginal costing approach give £1825 amount more as a result.

Acording to break even analysis, if Agmet Ltd sell 500units at £40 per unit it will be generating

sales revenue of £20000 to reach break even. If company wants to earn desired profit of £10000

they have to swll 1333.33 units. Similarly, if company is willing to sell 800 units the margin of

safety is 37.5%.

TASK 3

P4: Budgetary control and different types of planning tool and their advantages and

disadvantages used in budgetary control.

Budgetary control: This system of management refer to how well their manager uilize

past or present result to monitor and control its existing cost and operation in an accounting

peorid to maximise their future profit. Agmet Ltd is a producer and distributor of various

chemical, so their management must set predefined financial and performance goals with

budgets, compare those actual result, and adjust performance of their company if needed. If

management of Agmet Ltd is able to have a proper budgetary control then it will be advantage

company in many ways like proper co-ordination, important tool to measure performance,

maximisation of profit, economic growth, help to reduce production cost etc. (Maskell, Baggaley

and Grasso, 2016).

Management of Agmet Ltd take following steps in budgetary control process. First, they

set performance budget/goals that management wants to achieve like production or sales goals.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Second they compare and interpret the actual performance result with the budgeted goals. Third,

after comparison if there is any need manages of company needs to improve their, under

performing operation and give more strength to the favourable one. These reposts help

management to focus more on unfavourable operation and improve them as soon as possible to

gain more profit. At the last, manager of Agmet Ltd take final steps at the end of an accounting

period, they start making plans for the next year. So in budgetary control company uses three

planning tools that are explained below:

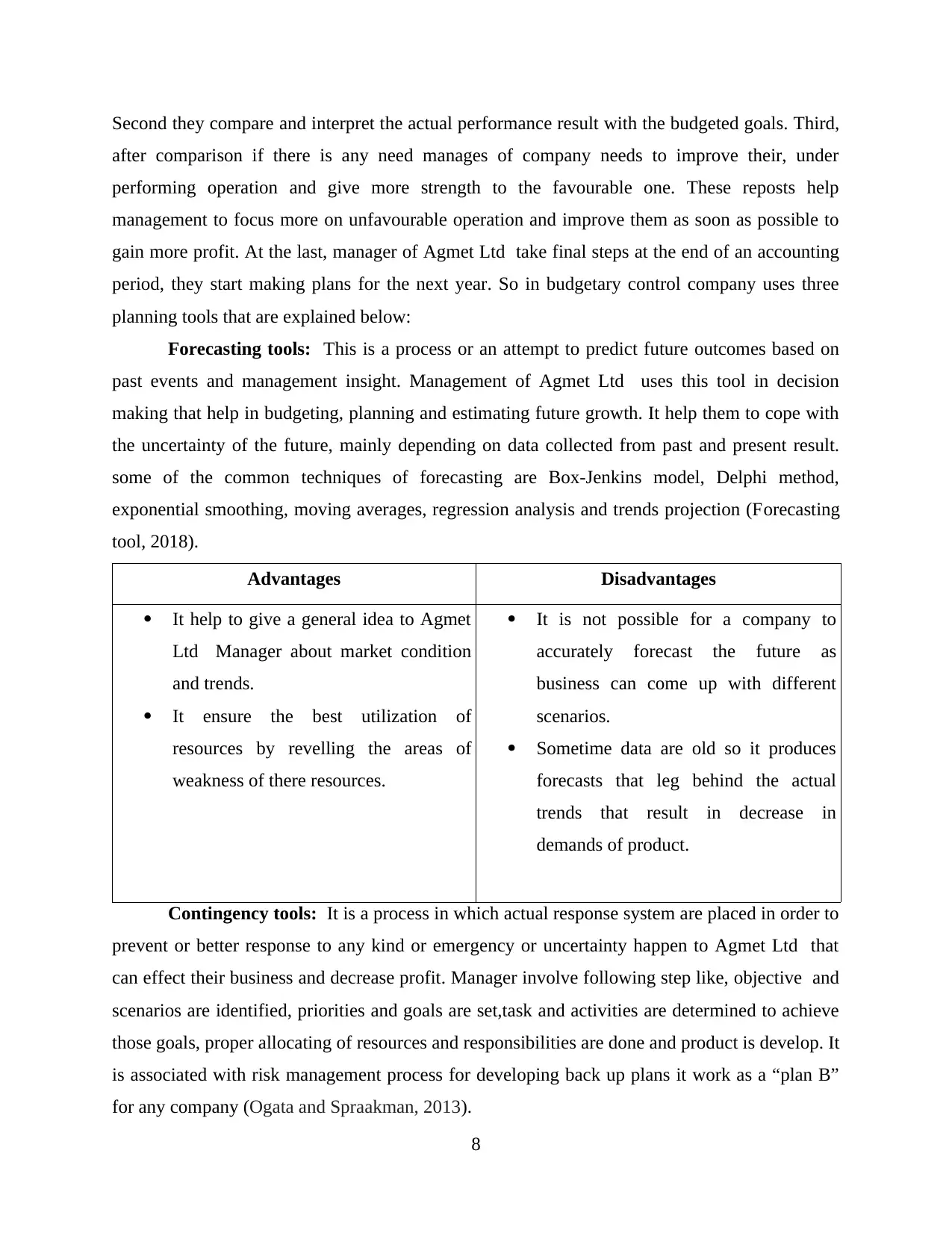

Forecasting tools: This is a process or an attempt to predict future outcomes based on

past events and management insight. Management of Agmet Ltd uses this tool in decision

making that help in budgeting, planning and estimating future growth. It help them to cope with

the uncertainty of the future, mainly depending on data collected from past and present result.

some of the common techniques of forecasting are Box-Jenkins model, Delphi method,

exponential smoothing, moving averages, regression analysis and trends projection (Forecasting

tool, 2018).

Advantages Disadvantages

It help to give a general idea to Agmet

Ltd Manager about market condition

and trends.

It ensure the best utilization of

resources by revelling the areas of

weakness of there resources.

It is not possible for a company to

accurately forecast the future as

business can come up with different

scenarios.

Sometime data are old so it produces

forecasts that leg behind the actual

trends that result in decrease in

demands of product.

Contingency tools: It is a process in which actual response system are placed in order to

prevent or better response to any kind or emergency or uncertainty happen to Agmet Ltd that

can effect their business and decrease profit. Manager involve following step like, objective and

scenarios are identified, priorities and goals are set,task and activities are determined to achieve

those goals, proper allocating of resources and responsibilities are done and product is develop. It

is associated with risk management process for developing back up plans it work as a “plan B”

for any company (Ogata and Spraakman, 2013).

8

after comparison if there is any need manages of company needs to improve their, under

performing operation and give more strength to the favourable one. These reposts help

management to focus more on unfavourable operation and improve them as soon as possible to

gain more profit. At the last, manager of Agmet Ltd take final steps at the end of an accounting

period, they start making plans for the next year. So in budgetary control company uses three

planning tools that are explained below:

Forecasting tools: This is a process or an attempt to predict future outcomes based on

past events and management insight. Management of Agmet Ltd uses this tool in decision

making that help in budgeting, planning and estimating future growth. It help them to cope with

the uncertainty of the future, mainly depending on data collected from past and present result.

some of the common techniques of forecasting are Box-Jenkins model, Delphi method,

exponential smoothing, moving averages, regression analysis and trends projection (Forecasting

tool, 2018).

Advantages Disadvantages

It help to give a general idea to Agmet

Ltd Manager about market condition

and trends.

It ensure the best utilization of

resources by revelling the areas of

weakness of there resources.

It is not possible for a company to

accurately forecast the future as

business can come up with different

scenarios.

Sometime data are old so it produces

forecasts that leg behind the actual

trends that result in decrease in

demands of product.

Contingency tools: It is a process in which actual response system are placed in order to

prevent or better response to any kind or emergency or uncertainty happen to Agmet Ltd that

can effect their business and decrease profit. Manager involve following step like, objective and

scenarios are identified, priorities and goals are set,task and activities are determined to achieve

those goals, proper allocating of resources and responsibilities are done and product is develop. It

is associated with risk management process for developing back up plans it work as a “plan B”

for any company (Ogata and Spraakman, 2013).

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

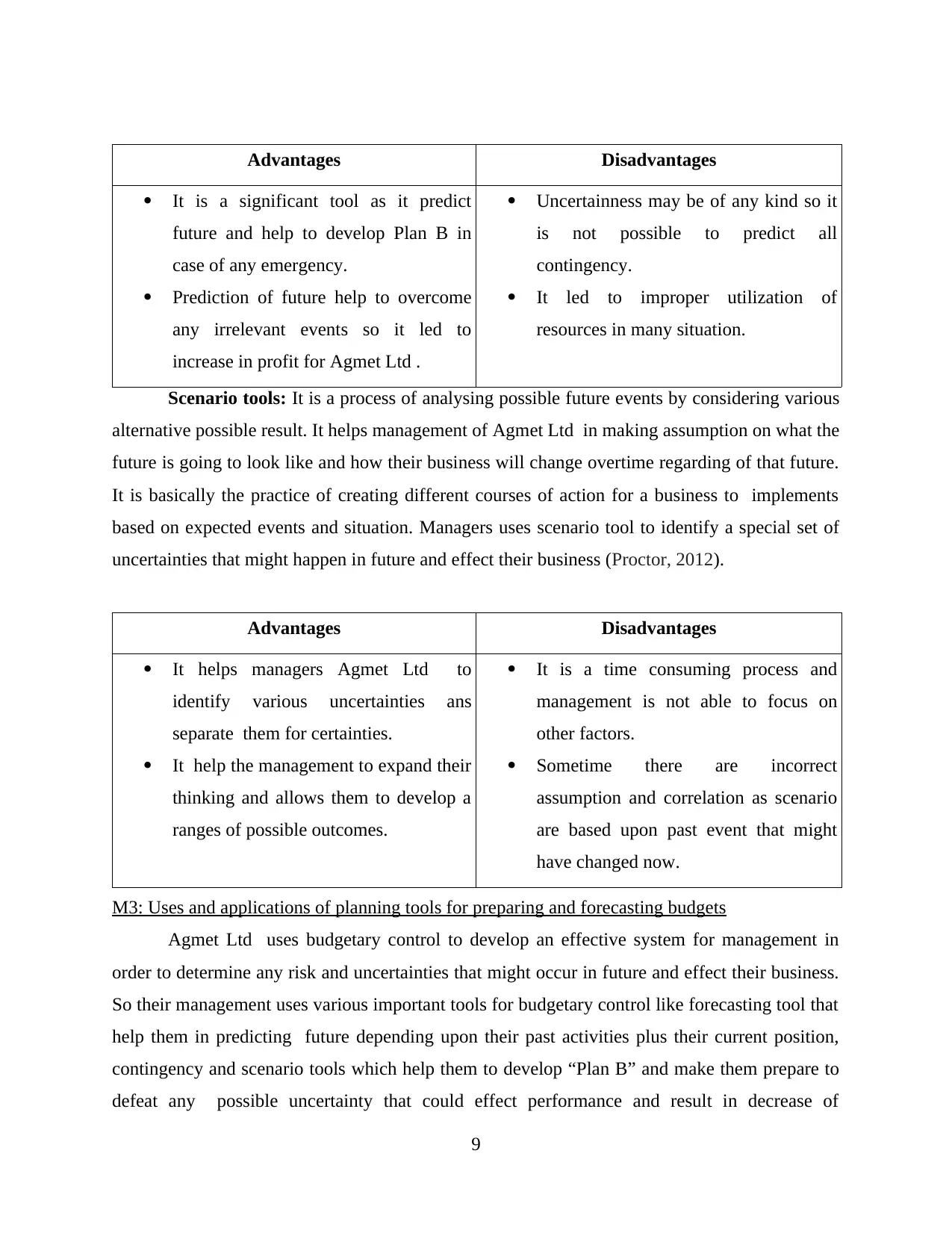

Advantages Disadvantages

It is a significant tool as it predict

future and help to develop Plan B in

case of any emergency.

Prediction of future help to overcome

any irrelevant events so it led to

increase in profit for Agmet Ltd .

Uncertainness may be of any kind so it

is not possible to predict all

contingency.

It led to improper utilization of

resources in many situation.

Scenario tools: It is a process of analysing possible future events by considering various

alternative possible result. It helps management of Agmet Ltd in making assumption on what the

future is going to look like and how their business will change overtime regarding of that future.

It is basically the practice of creating different courses of action for a business to implements

based on expected events and situation. Managers uses scenario tool to identify a special set of

uncertainties that might happen in future and effect their business (Proctor, 2012).

Advantages Disadvantages

It helps managers Agmet Ltd to

identify various uncertainties ans

separate them for certainties.

It help the management to expand their

thinking and allows them to develop a

ranges of possible outcomes.

It is a time consuming process and

management is not able to focus on

other factors.

Sometime there are incorrect

assumption and correlation as scenario

are based upon past event that might

have changed now.

M3: Uses and applications of planning tools for preparing and forecasting budgets

Agmet Ltd uses budgetary control to develop an effective system for management in

order to determine any risk and uncertainties that might occur in future and effect their business.

So their management uses various important tools for budgetary control like forecasting tool that

help them in predicting future depending upon their past activities plus their current position,

contingency and scenario tools which help them to develop “Plan B” and make them prepare to

defeat any possible uncertainty that could effect performance and result in decrease of

9

It is a significant tool as it predict

future and help to develop Plan B in

case of any emergency.

Prediction of future help to overcome

any irrelevant events so it led to

increase in profit for Agmet Ltd .

Uncertainness may be of any kind so it

is not possible to predict all

contingency.

It led to improper utilization of

resources in many situation.

Scenario tools: It is a process of analysing possible future events by considering various

alternative possible result. It helps management of Agmet Ltd in making assumption on what the

future is going to look like and how their business will change overtime regarding of that future.

It is basically the practice of creating different courses of action for a business to implements

based on expected events and situation. Managers uses scenario tool to identify a special set of

uncertainties that might happen in future and effect their business (Proctor, 2012).

Advantages Disadvantages

It helps managers Agmet Ltd to

identify various uncertainties ans

separate them for certainties.

It help the management to expand their

thinking and allows them to develop a

ranges of possible outcomes.

It is a time consuming process and

management is not able to focus on

other factors.

Sometime there are incorrect

assumption and correlation as scenario

are based upon past event that might

have changed now.

M3: Uses and applications of planning tools for preparing and forecasting budgets

Agmet Ltd uses budgetary control to develop an effective system for management in

order to determine any risk and uncertainties that might occur in future and effect their business.

So their management uses various important tools for budgetary control like forecasting tool that

help them in predicting future depending upon their past activities plus their current position,

contingency and scenario tools which help them to develop “Plan B” and make them prepare to

defeat any possible uncertainty that could effect performance and result in decrease of

9

profitability of the company. Planning is a must for any company to grow and proper uses of

these tools in planning help Agmet Ltd to predict future and overcome uncertain events.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems may be defined, a situation where company is not in a condition to

pay its outstanding bills, provides salaries to their employees or sells off its assets to raise fund to

run their business. Agmet Ltd also faces problem of financing due to following factors like lack

of money management, more number of credit customer, late recovery of funds etc. therefore

Manger of Agmet Ltd must have a unique approach to resolve its financial problem and follow

proper guideline in utilizing their resources and available fund (Schaltegger and Burritt, 2017).

Lack of budgeting and money management skills: management of Agmet Ltd faces

problem of funds and money to run their business because the lack the skill how to manage their

existing resources and funds.

Sales are good but profit are low: Major factor for Agmet Ltd financial problem is not

generating high profit. As a result company is making sufficient sales but not maximising their

income because there are various hidden cost which were not recognise by the management.

Improper book keeping habits: small business like Agmet Ltd are usually bad record

keeper , they do not have a proper record of all their expenses and income.

Paying bills late: late payment of outstanding bills may led to financial problem in

Agmet Ltd as there liability keeps on increasing and effect their profit.

More spending on promotion and coupons: regular promotion in order to increase sales

for their product Agmet Ltd spend huge amount on their profit that led to a financial problem.

These problem of finance must be properly examine and solved by Agmet Ltd

management, that will increase their marketplace. To solve these problem following tools are

adopted by Agmet Ltd :

Key Performance Indicators (KPI):- Agmet Ltd uses this tool to resolve its financial

problem, as it help the management to set predefined quantitative measure and examine there

performance in a period of time. It is also referred as key success indicator that help a company

to compare its financial position and performance against other companies within the same

industry. These may differ from organisation to organisation based on business priorities. KPI

10

these tools in planning help Agmet Ltd to predict future and overcome uncertain events.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems may be defined, a situation where company is not in a condition to

pay its outstanding bills, provides salaries to their employees or sells off its assets to raise fund to

run their business. Agmet Ltd also faces problem of financing due to following factors like lack

of money management, more number of credit customer, late recovery of funds etc. therefore

Manger of Agmet Ltd must have a unique approach to resolve its financial problem and follow

proper guideline in utilizing their resources and available fund (Schaltegger and Burritt, 2017).

Lack of budgeting and money management skills: management of Agmet Ltd faces

problem of funds and money to run their business because the lack the skill how to manage their

existing resources and funds.

Sales are good but profit are low: Major factor for Agmet Ltd financial problem is not

generating high profit. As a result company is making sufficient sales but not maximising their

income because there are various hidden cost which were not recognise by the management.

Improper book keeping habits: small business like Agmet Ltd are usually bad record

keeper , they do not have a proper record of all their expenses and income.

Paying bills late: late payment of outstanding bills may led to financial problem in

Agmet Ltd as there liability keeps on increasing and effect their profit.

More spending on promotion and coupons: regular promotion in order to increase sales

for their product Agmet Ltd spend huge amount on their profit that led to a financial problem.

These problem of finance must be properly examine and solved by Agmet Ltd

management, that will increase their marketplace. To solve these problem following tools are

adopted by Agmet Ltd :

Key Performance Indicators (KPI):- Agmet Ltd uses this tool to resolve its financial

problem, as it help the management to set predefined quantitative measure and examine there

performance in a period of time. It is also referred as key success indicator that help a company

to compare its financial position and performance against other companies within the same

industry. These may differ from organisation to organisation based on business priorities. KPI

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.