Accounting for Managers Report: Platform LLP Financial Analysis

VerifiedAdded on 2019/11/19

|13

|2946

|159

Report

AI Summary

This report provides a comprehensive analysis of accounting for managers, focusing on a retail clothing startup named "Platform" in Dubai, structured as a Limited Liability Partnership (LLP). The report begins with a business description, followed by a justification for selecting the LLP structure, highlighting its advantages in terms of maintenance, liability protection, and taxation. It then explores various financing options available, including equity financing, debentures, and bank loans, and presents projected financial statements, including income statements and balance sheets for the years 2016-2018. The report further analyzes the types of financial statement analysis relevant to the business, such as income statements, balance sheets, and cash flow statements. It also discusses how accounting information aids in management accounting for partners and employees, and financial accounting for investors, banks, regulatory authorities, and customers. Finally, the report examines the benefits of dividend distribution and the implications of not distributing dividends, particularly for employees and the potential for government intervention.

RUNNING HEAD: Accounting for managers

Accounting for managers

Accounting for managers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers 2

Table of Contents

Question 1.............................................................................................................................................3

Business description..........................................................................................................................3

Question 2.............................................................................................................................................3

Reason for selecting LLP:...................................................................................................................3

Question 3.............................................................................................................................................4

Financing options available for Platform:..........................................................................................4

Question 4.............................................................................................................................................6

Projected income statement and balance sheet...............................................................................6

Question 5.............................................................................................................................................8

Type of Financial statement analysis for business:............................................................................8

Question 6.............................................................................................................................................9

Accounting information help in management accounting.................................................................9

Accounting information help in financial accounting:.......................................................................9

Question 7...........................................................................................................................................10

Dividend distributing is beneficial....................................................................................................10

Implications for not distributing Dividend:......................................................................................11

References:..........................................................................................................................................12

Table of Contents

Question 1.............................................................................................................................................3

Business description..........................................................................................................................3

Question 2.............................................................................................................................................3

Reason for selecting LLP:...................................................................................................................3

Question 3.............................................................................................................................................4

Financing options available for Platform:..........................................................................................4

Question 4.............................................................................................................................................6

Projected income statement and balance sheet...............................................................................6

Question 5.............................................................................................................................................8

Type of Financial statement analysis for business:............................................................................8

Question 6.............................................................................................................................................9

Accounting information help in management accounting.................................................................9

Accounting information help in financial accounting:.......................................................................9

Question 7...........................................................................................................................................10

Dividend distributing is beneficial....................................................................................................10

Implications for not distributing Dividend:......................................................................................11

References:..........................................................................................................................................12

Accounting for managers 3

Question 1

Business description

Platform

The platform is a start-up retail clothing establishment which will be selling in market

fashionable, comfortable and many more types of clothing to women’s. The platform will be

located in Dubai, a famous place for tourist attraction and people’s entertainment. The

platform will be initiated as an LLP having 5 members as partners. Platform initial aim will

be to achieve target plan by opening shop in local markets of Dubai (Müller & Thoring,

2012). Their future plans are to bring for women’s of Dubai upcoming fashion from various

countries by research, creating the customized online market and become a fashion brand in

near future. In return, Platform will be expecting people to accept it openly and absorb a

penetrable size in the market.

Platform products will be centralized on women’s and girls. It will be creating the market

area by closely adopting trends in the market as well customer preferences. They will also

make tailor made clothes to meet the special requirements of customers with the main focus

on style. The platform will also adopt reasonable cost policy to attract customers of the lower

budget as well.

Question 2

Reason for selecting LLP:

A. After formation, there is a lesser requirement of maintenance and moreover convenience

in adding new members. In LLP it is easy to sell the business to someone else. It requires

lesser procedural follow-up in comparison to the company. There is a more relaxed structure

in LLP, as minutes procedure like the company is not required for taking board decisions in

Question 1

Business description

Platform

The platform is a start-up retail clothing establishment which will be selling in market

fashionable, comfortable and many more types of clothing to women’s. The platform will be

located in Dubai, a famous place for tourist attraction and people’s entertainment. The

platform will be initiated as an LLP having 5 members as partners. Platform initial aim will

be to achieve target plan by opening shop in local markets of Dubai (Müller & Thoring,

2012). Their future plans are to bring for women’s of Dubai upcoming fashion from various

countries by research, creating the customized online market and become a fashion brand in

near future. In return, Platform will be expecting people to accept it openly and absorb a

penetrable size in the market.

Platform products will be centralized on women’s and girls. It will be creating the market

area by closely adopting trends in the market as well customer preferences. They will also

make tailor made clothes to meet the special requirements of customers with the main focus

on style. The platform will also adopt reasonable cost policy to attract customers of the lower

budget as well.

Question 2

Reason for selecting LLP:

A. After formation, there is a lesser requirement of maintenance and moreover convenience

in adding new members. In LLP it is easy to sell the business to someone else. It requires

lesser procedural follow-up in comparison to the company. There is a more relaxed structure

in LLP, as minutes procedure like the company is not required for taking board decisions in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers 4

LLP. There are also fewer business restrictions on many management related decision if

compared with other business structure.

B. It also helps in protecting personal assets used in business from lawsuits against directed

on business (Firth, Mo & Wong, 2012). A proprietorship and partnership will be risky entities

to start. After some period of time growth and increased market share, LLC can convert their

business to S-Corp as well as C-Corp. in takeover and merger, an LLC can benefit itself by

acquiring sick companies giving the tax benefit to the business.

C. LLC helps in avoiding double taxation and supports in maintaining various categories of

inventory. Double taxation generally happens when in a business company and owners both

are taxed separately but LLC helps in preventing this by taxing same as proprietor. This is

very useful for a start-up business to enter to market.

D. An LLC is an optimal structure for a business as it is easy, fast and simple to form. The

registration process for LLP can also be completed without appointing an attorney. The

charge for filing registration fee in LLP is very less. It is also beneficial for a business to

register as LLP because after registration an LLP would get employee id from IRS which will

help in an opening bank account.

Question 3

Financing options available for Platform:

Equity financing:

Equity can turn out to be beneficial since it enables the organization to put more assets over

into the business, though debt financing confines income by commanding that speculators get

paid back on a customary timetable (Da, Guo & Jagannathan, 2012). This adaptability of

equity financing empowers the organization to develop at a quicker rate as opposed to paying

LLP. There are also fewer business restrictions on many management related decision if

compared with other business structure.

B. It also helps in protecting personal assets used in business from lawsuits against directed

on business (Firth, Mo & Wong, 2012). A proprietorship and partnership will be risky entities

to start. After some period of time growth and increased market share, LLC can convert their

business to S-Corp as well as C-Corp. in takeover and merger, an LLC can benefit itself by

acquiring sick companies giving the tax benefit to the business.

C. LLC helps in avoiding double taxation and supports in maintaining various categories of

inventory. Double taxation generally happens when in a business company and owners both

are taxed separately but LLC helps in preventing this by taxing same as proprietor. This is

very useful for a start-up business to enter to market.

D. An LLC is an optimal structure for a business as it is easy, fast and simple to form. The

registration process for LLP can also be completed without appointing an attorney. The

charge for filing registration fee in LLP is very less. It is also beneficial for a business to

register as LLP because after registration an LLP would get employee id from IRS which will

help in an opening bank account.

Question 3

Financing options available for Platform:

Equity financing:

Equity can turn out to be beneficial since it enables the organization to put more assets over

into the business, though debt financing confines income by commanding that speculators get

paid back on a customary timetable (Da, Guo & Jagannathan, 2012). This adaptability of

equity financing empowers the organization to develop at a quicker rate as opposed to paying

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers 5

money out every month. Most organizations issue equity since they either right now have

constrained income, or they hope to eventually to have restricted income. Financial

specialists more often than not support equity as favoured stock, however sometimes the

regular stock is appropriated.

Debentures issue: Debt financing is a legal form of financing. The bank or financial investor

does not "possess" any part of the business and they don't have any interference in everyday

operations. Investors will out be from business operations if the business is paying its

installments on time (Altunbaş, Kara & Marqués-Ibáñez, 2010). The interests pay obligation

financing is additionally assessed deductible, and advance installments are also known from

month to month.

Bank loan:

The bank gives two sorts of financing to organizations. One is the working capital advance,

and other is funding. Working Capital advance is the credit required to run one full cycle of

income producing operations, and the point of confinement is generally chosen by

hypothecating stocks and debtors (Miles, Yang & Marcheggiano, 2013). The funding from

the bank would include the standard procedure of sharing the strategy for success and the

valuation points of interest, alongside the company budgetary report, based on which the

advance is endorsed. Credits from banks and NBFCs help in purchasing the inventory and

machinery, securing working capital and funds for growth. And not at all like a proprietorship

which has an equity stake of investors and moreover banks do not look for the share of profit

in the business.

money out every month. Most organizations issue equity since they either right now have

constrained income, or they hope to eventually to have restricted income. Financial

specialists more often than not support equity as favoured stock, however sometimes the

regular stock is appropriated.

Debentures issue: Debt financing is a legal form of financing. The bank or financial investor

does not "possess" any part of the business and they don't have any interference in everyday

operations. Investors will out be from business operations if the business is paying its

installments on time (Altunbaş, Kara & Marqués-Ibáñez, 2010). The interests pay obligation

financing is additionally assessed deductible, and advance installments are also known from

month to month.

Bank loan:

The bank gives two sorts of financing to organizations. One is the working capital advance,

and other is funding. Working Capital advance is the credit required to run one full cycle of

income producing operations, and the point of confinement is generally chosen by

hypothecating stocks and debtors (Miles, Yang & Marcheggiano, 2013). The funding from

the bank would include the standard procedure of sharing the strategy for success and the

valuation points of interest, alongside the company budgetary report, based on which the

advance is endorsed. Credits from banks and NBFCs help in purchasing the inventory and

machinery, securing working capital and funds for growth. And not at all like a proprietorship

which has an equity stake of investors and moreover banks do not look for the share of profit

in the business.

Accounting for managers 6

Question 4

Projected income statement and balance sheet

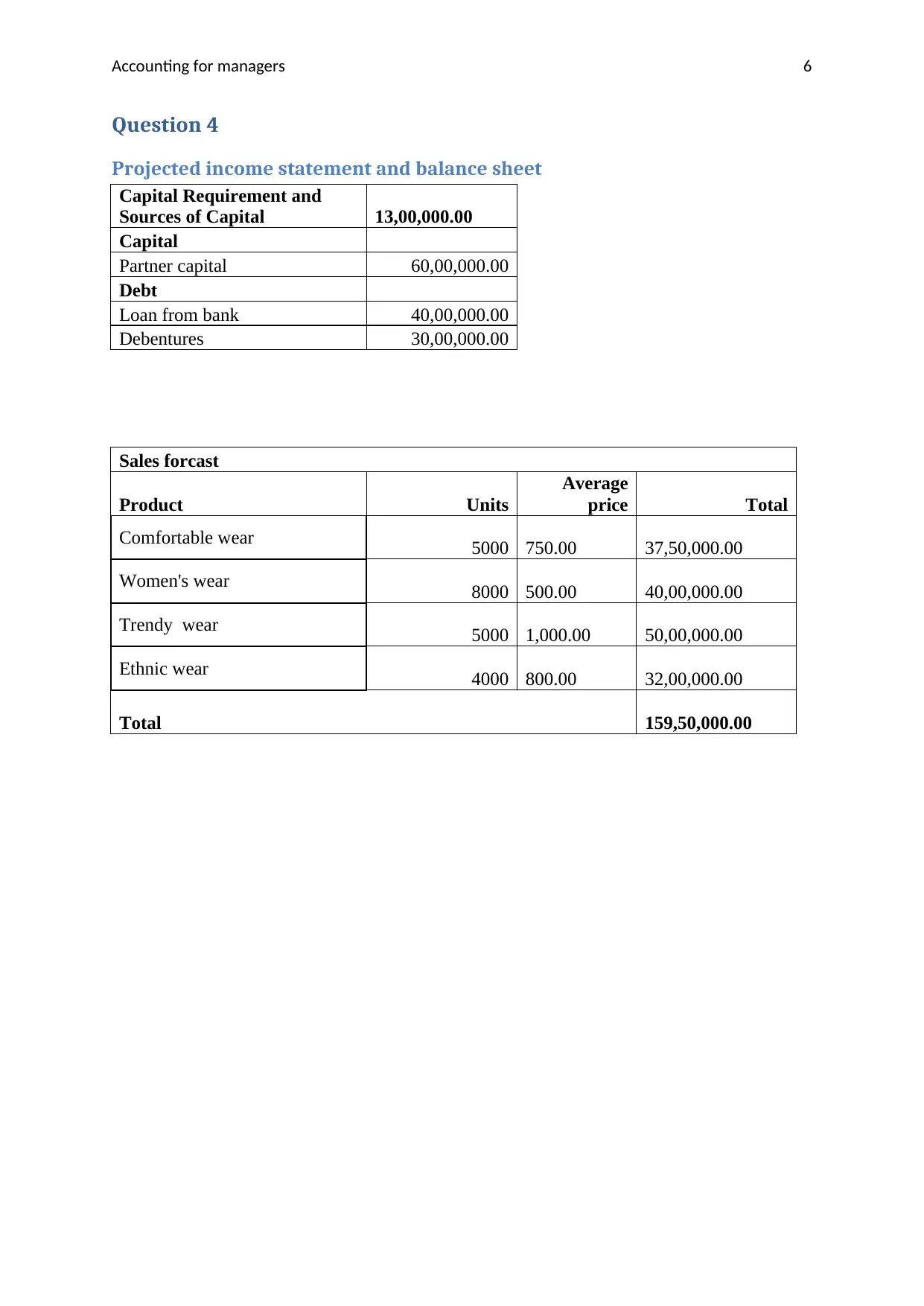

Capital Requirement and

Sources of Capital 13,00,000.00

Capital

Partner capital 60,00,000.00

Debt

Loan from bank 40,00,000.00

Debentures 30,00,000.00

Sales forcast

Product Units

Average

price Total

Comfortable wear 5000 750.00 37,50,000.00

Women's wear 8000 500.00 40,00,000.00

Trendy wear 5000 1,000.00 50,00,000.00

Ethnic wear 4000 800.00 32,00,000.00

Total 159,50,000.00

Question 4

Projected income statement and balance sheet

Capital Requirement and

Sources of Capital 13,00,000.00

Capital

Partner capital 60,00,000.00

Debt

Loan from bank 40,00,000.00

Debentures 30,00,000.00

Sales forcast

Product Units

Average

price Total

Comfortable wear 5000 750.00 37,50,000.00

Women's wear 8000 500.00 40,00,000.00

Trendy wear 5000 1,000.00 50,00,000.00

Ethnic wear 4000 800.00 32,00,000.00

Total 159,50,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers 7

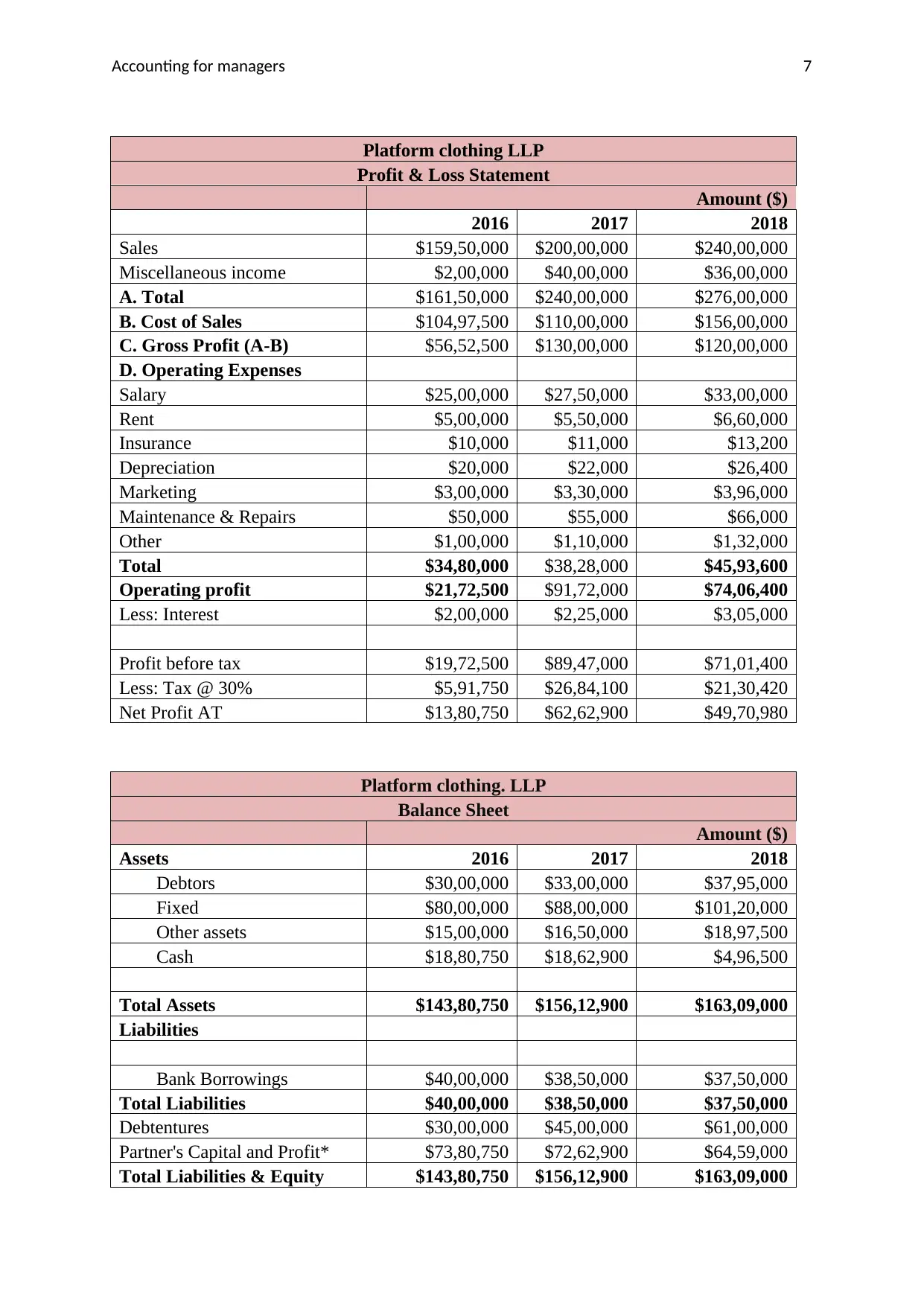

Platform clothing LLP

Profit & Loss Statement

Amount ($)

2016 2017 2018

Sales $159,50,000 $200,00,000 $240,00,000

Miscellaneous income $2,00,000 $40,00,000 $36,00,000

A. Total $161,50,000 $240,00,000 $276,00,000

B. Cost of Sales $104,97,500 $110,00,000 $156,00,000

C. Gross Profit (A-B) $56,52,500 $130,00,000 $120,00,000

D. Operating Expenses

Salary $25,00,000 $27,50,000 $33,00,000

Rent $5,00,000 $5,50,000 $6,60,000

Insurance $10,000 $11,000 $13,200

Depreciation $20,000 $22,000 $26,400

Marketing $3,00,000 $3,30,000 $3,96,000

Maintenance & Repairs $50,000 $55,000 $66,000

Other $1,00,000 $1,10,000 $1,32,000

Total $34,80,000 $38,28,000 $45,93,600

Operating profit $21,72,500 $91,72,000 $74,06,400

Less: Interest $2,00,000 $2,25,000 $3,05,000

Profit before tax $19,72,500 $89,47,000 $71,01,400

Less: Tax @ 30% $5,91,750 $26,84,100 $21,30,420

Net Profit AT $13,80,750 $62,62,900 $49,70,980

Platform clothing. LLP

Balance Sheet

Amount ($)

Assets 2016 2017 2018

Debtors $30,00,000 $33,00,000 $37,95,000

Fixed $80,00,000 $88,00,000 $101,20,000

Other assets $15,00,000 $16,50,000 $18,97,500

Cash $18,80,750 $18,62,900 $4,96,500

Total Assets $143,80,750 $156,12,900 $163,09,000

Liabilities

Bank Borrowings $40,00,000 $38,50,000 $37,50,000

Total Liabilities $40,00,000 $38,50,000 $37,50,000

Debtentures $30,00,000 $45,00,000 $61,00,000

Partner's Capital and Profit* $73,80,750 $72,62,900 $64,59,000

Total Liabilities & Equity $143,80,750 $156,12,900 $163,09,000

Platform clothing LLP

Profit & Loss Statement

Amount ($)

2016 2017 2018

Sales $159,50,000 $200,00,000 $240,00,000

Miscellaneous income $2,00,000 $40,00,000 $36,00,000

A. Total $161,50,000 $240,00,000 $276,00,000

B. Cost of Sales $104,97,500 $110,00,000 $156,00,000

C. Gross Profit (A-B) $56,52,500 $130,00,000 $120,00,000

D. Operating Expenses

Salary $25,00,000 $27,50,000 $33,00,000

Rent $5,00,000 $5,50,000 $6,60,000

Insurance $10,000 $11,000 $13,200

Depreciation $20,000 $22,000 $26,400

Marketing $3,00,000 $3,30,000 $3,96,000

Maintenance & Repairs $50,000 $55,000 $66,000

Other $1,00,000 $1,10,000 $1,32,000

Total $34,80,000 $38,28,000 $45,93,600

Operating profit $21,72,500 $91,72,000 $74,06,400

Less: Interest $2,00,000 $2,25,000 $3,05,000

Profit before tax $19,72,500 $89,47,000 $71,01,400

Less: Tax @ 30% $5,91,750 $26,84,100 $21,30,420

Net Profit AT $13,80,750 $62,62,900 $49,70,980

Platform clothing. LLP

Balance Sheet

Amount ($)

Assets 2016 2017 2018

Debtors $30,00,000 $33,00,000 $37,95,000

Fixed $80,00,000 $88,00,000 $101,20,000

Other assets $15,00,000 $16,50,000 $18,97,500

Cash $18,80,750 $18,62,900 $4,96,500

Total Assets $143,80,750 $156,12,900 $163,09,000

Liabilities

Bank Borrowings $40,00,000 $38,50,000 $37,50,000

Total Liabilities $40,00,000 $38,50,000 $37,50,000

Debtentures $30,00,000 $45,00,000 $61,00,000

Partner's Capital and Profit* $73,80,750 $72,62,900 $64,59,000

Total Liabilities & Equity $143,80,750 $156,12,900 $163,09,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers 8

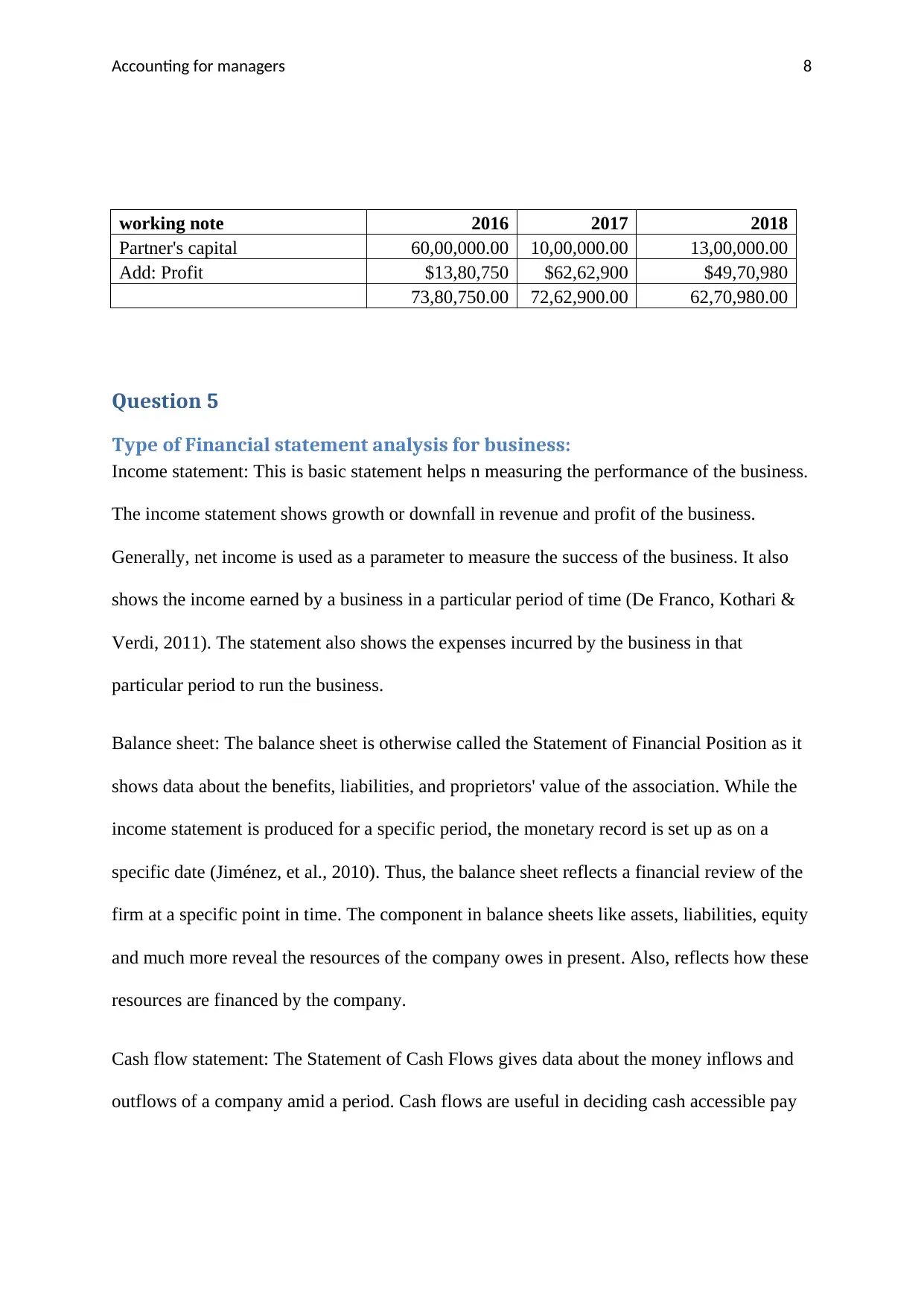

working note 2016 2017 2018

Partner's capital 60,00,000.00 10,00,000.00 13,00,000.00

Add: Profit $13,80,750 $62,62,900 $49,70,980

73,80,750.00 72,62,900.00 62,70,980.00

Question 5

Type of Financial statement analysis for business:

Income statement: This is basic statement helps n measuring the performance of the business.

The income statement shows growth or downfall in revenue and profit of the business.

Generally, net income is used as a parameter to measure the success of the business. It also

shows the income earned by a business in a particular period of time (De Franco, Kothari &

Verdi, 2011). The statement also shows the expenses incurred by the business in that

particular period to run the business.

Balance sheet: The balance sheet is otherwise called the Statement of Financial Position as it

shows data about the benefits, liabilities, and proprietors' value of the association. While the

income statement is produced for a specific period, the monetary record is set up as on a

specific date (Jiménez, et al., 2010). Thus, the balance sheet reflects a financial review of the

firm at a specific point in time. The component in balance sheets like assets, liabilities, equity

and much more reveal the resources of the company owes in present. Also, reflects how these

resources are financed by the company.

Cash flow statement: The Statement of Cash Flows gives data about the money inflows and

outflows of a company amid a period. Cash flows are useful in deciding cash accessible pay

working note 2016 2017 2018

Partner's capital 60,00,000.00 10,00,000.00 13,00,000.00

Add: Profit $13,80,750 $62,62,900 $49,70,980

73,80,750.00 72,62,900.00 62,70,980.00

Question 5

Type of Financial statement analysis for business:

Income statement: This is basic statement helps n measuring the performance of the business.

The income statement shows growth or downfall in revenue and profit of the business.

Generally, net income is used as a parameter to measure the success of the business. It also

shows the income earned by a business in a particular period of time (De Franco, Kothari &

Verdi, 2011). The statement also shows the expenses incurred by the business in that

particular period to run the business.

Balance sheet: The balance sheet is otherwise called the Statement of Financial Position as it

shows data about the benefits, liabilities, and proprietors' value of the association. While the

income statement is produced for a specific period, the monetary record is set up as on a

specific date (Jiménez, et al., 2010). Thus, the balance sheet reflects a financial review of the

firm at a specific point in time. The component in balance sheets like assets, liabilities, equity

and much more reveal the resources of the company owes in present. Also, reflects how these

resources are financed by the company.

Cash flow statement: The Statement of Cash Flows gives data about the money inflows and

outflows of a company amid a period. Cash flows are useful in deciding cash accessible pay

Accounting for managers 9

loan to creditors of the company (Maravas & Pantouvakis, 2012). Normally an increase in

income flow from operating activity shows a healthy income generation for the organization.

Question 6

Accounting information help in management accounting

Management: In assessing how the administration has released its duty regarding securing

and dealing with the organization's assets. Secondly on changing decisions about when to get

or contribute in organization assets. It also helps in decisions regarding extension or

downsizing in organization’s size.

Partners: Partners are more worried about the profits they earn from their capital in the

organization and this aim is satisfied through using accounting information (Macintosh &

Quattrone, 2010). Not exclusively do they need their capital in the safe zone but also keen in

knowing the benefit earned or loss brought about by the business from time to time.

Employees– Employees are curious to know the accounting information elements of their

company with the goal that they know about the general productivity of the organization

which directly affects their compensation and employee stability.

Accounting information help in financial accounting:

Investors: External users are interested in knowing the ROI of the organization. As investors

are not having direct access to business operations of the firm, accounting information helps

them in locating out the money spent by the firm in a different area by managers (Weil,

Schipper & Francis, 2013). It aids them in taking the decision regarding investment amount

they are willing to spend.

Bank: They play an important part in the business organization because they advance a

different kind of loans to business. Accounting information aids them in knowing the credit

loan to creditors of the company (Maravas & Pantouvakis, 2012). Normally an increase in

income flow from operating activity shows a healthy income generation for the organization.

Question 6

Accounting information help in management accounting

Management: In assessing how the administration has released its duty regarding securing

and dealing with the organization's assets. Secondly on changing decisions about when to get

or contribute in organization assets. It also helps in decisions regarding extension or

downsizing in organization’s size.

Partners: Partners are more worried about the profits they earn from their capital in the

organization and this aim is satisfied through using accounting information (Macintosh &

Quattrone, 2010). Not exclusively do they need their capital in the safe zone but also keen in

knowing the benefit earned or loss brought about by the business from time to time.

Employees– Employees are curious to know the accounting information elements of their

company with the goal that they know about the general productivity of the organization

which directly affects their compensation and employee stability.

Accounting information help in financial accounting:

Investors: External users are interested in knowing the ROI of the organization. As investors

are not having direct access to business operations of the firm, accounting information helps

them in locating out the money spent by the firm in a different area by managers (Weil,

Schipper & Francis, 2013). It aids them in taking the decision regarding investment amount

they are willing to spend.

Bank: They play an important part in the business organization because they advance a

different kind of loans to business. Accounting information aids them in knowing the credit

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting for managers 10

worthiness of a firm. Credit is allowed to organization and firm according to the financial

soundness of firm, according to which terms and conditions of the loan are decided.

Regulatory authority: It includes government agencies and regulatory authorities which

determine that accounts of the firm are prepared according to applicable principles, standards,

and rules (Weygandt, et al., 2010). The objective behind these determinations is to save and

protect the stakeholders’ interest of the firm. Tax evaluation is also done with help of

accounting information after analyzing the financials of the organization.

Customers: They are the complex group which incorporating producers at all level of

processing, wholesalers and retailers and the end customers. Sound financial well-being

demonstrates that clients at each level are alright with the constant inflow of stock from the

business. Customers utilize the bookkeeping data for surveying the financial position of its

firms which is necessary for keeping up stable supply in future.

Question 7

Dividend distributing is beneficial

Profit sharing has turned out to be one of another type of motivating forces called total

incentive framework. These incentives forces interface the greater part of the workers of an

organization in pursuing hierarchical objectives (Artz, 2010). A typical confusion of profit

sharing is that it is more suited for smaller organizations where workers would more be able

to effectively observe the association between their proficiency and company commitments.

In fact, profit sharing is as a rule effectively used in big and small organizations, labor

intensive and capital-intensive ventures, large scale manufacturing and employment

circumstances, and businesses with unpredictable profits including with stable benefits. Profit

sharing can remunerate representative performance, status, and thrift, depending upon the

design of the future goals.

worthiness of a firm. Credit is allowed to organization and firm according to the financial

soundness of firm, according to which terms and conditions of the loan are decided.

Regulatory authority: It includes government agencies and regulatory authorities which

determine that accounts of the firm are prepared according to applicable principles, standards,

and rules (Weygandt, et al., 2010). The objective behind these determinations is to save and

protect the stakeholders’ interest of the firm. Tax evaluation is also done with help of

accounting information after analyzing the financials of the organization.

Customers: They are the complex group which incorporating producers at all level of

processing, wholesalers and retailers and the end customers. Sound financial well-being

demonstrates that clients at each level are alright with the constant inflow of stock from the

business. Customers utilize the bookkeeping data for surveying the financial position of its

firms which is necessary for keeping up stable supply in future.

Question 7

Dividend distributing is beneficial

Profit sharing has turned out to be one of another type of motivating forces called total

incentive framework. These incentives forces interface the greater part of the workers of an

organization in pursuing hierarchical objectives (Artz, 2010). A typical confusion of profit

sharing is that it is more suited for smaller organizations where workers would more be able

to effectively observe the association between their proficiency and company commitments.

In fact, profit sharing is as a rule effectively used in big and small organizations, labor

intensive and capital-intensive ventures, large scale manufacturing and employment

circumstances, and businesses with unpredictable profits including with stable benefits. Profit

sharing can remunerate representative performance, status, and thrift, depending upon the

design of the future goals.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting for managers 11

Profit sharing motivates many stakeholders of the organization to invest in the company more

(Poole & Jenkins, 2013). These tendencies show that company does not want to absorb

profits fully rather they are distributing it to shareholder in form of dividends.

Implications for not distributing Dividend

Employees: A major implication is on an employee for not distributing the dividend, as their

investment in the company is not paying them returns. In case of smaller firms, major

fluctuations in dividend distribution by companies affect the saving and income of employees

(Wang, 2012).

Government interventions: If a company is not distributing dividend year to year it will have

many implications by the government and regulatory authority. It will not be having any tax

benefit which is applicable only when firms distribute profit. Government subsidies are also

not granted many times if there are no profit sharing plans of the company.

Investors and creditors: Investors and debtors also will be least interested in granting fund to

the firm, as there is no dividend distribution policy of the company. This indicates that

whatever the company is earning it is retaining it for future or partners are sharing in

themselves leaving no profits for other stakeholders.

Moreover, any investor will be least interested in investing money in business because it is

interpreted generally that if the firm is not distributing profit, then it surely will not be

providing the good return to investors.

Profit sharing motivates many stakeholders of the organization to invest in the company more

(Poole & Jenkins, 2013). These tendencies show that company does not want to absorb

profits fully rather they are distributing it to shareholder in form of dividends.

Implications for not distributing Dividend

Employees: A major implication is on an employee for not distributing the dividend, as their

investment in the company is not paying them returns. In case of smaller firms, major

fluctuations in dividend distribution by companies affect the saving and income of employees

(Wang, 2012).

Government interventions: If a company is not distributing dividend year to year it will have

many implications by the government and regulatory authority. It will not be having any tax

benefit which is applicable only when firms distribute profit. Government subsidies are also

not granted many times if there are no profit sharing plans of the company.

Investors and creditors: Investors and debtors also will be least interested in granting fund to

the firm, as there is no dividend distribution policy of the company. This indicates that

whatever the company is earning it is retaining it for future or partners are sharing in

themselves leaving no profits for other stakeholders.

Moreover, any investor will be least interested in investing money in business because it is

interpreted generally that if the firm is not distributing profit, then it surely will not be

providing the good return to investors.

Accounting for managers 12

References

Artz, B., 2010. Fringe benefits and job satisfaction. International journal of manpower, 31(6),

pp.626-644.

Poole, M. and Jenkins, G., 2013. The impact of economic democracy: Profit-sharing and

employee-shareholding schemes. Routledge..

Miles, D., Yang, J. and Marcheggiano, G., 2013. Optimal bank capital. The Economic

Journal, 123(567), pp.1-37.

Da, Z., Guo, R.J. and Jagannathan, R., 2012. CAPM for estimating the cost of equity capital:

Interpreting the empirical evidence. Journal of Financial Economics, 103(1), pp.204-220.

Altunbaş, Y., Kara, A. and Marqués-Ibáñez, D., 2010. Large debt financing: syndicated loans

versus corporate bonds. The European Journal of Finance, 16(5), pp.437-458.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D., KIESO, D. and Elias, R.Z., 2010. Accounting principles.

Issues in Accounting Education, 25(1), pp.179-180.

Wang, G., Wilson, C., Zhao, X., Zhu, Y., Mohanlal, M., Zheng, H. and Zhao, B.Y., 2012,

April. Serf and turf: crowdturfing for fun and profit. In Proceedings of the 21st international

conference on World Wide Web (pp. 679-688). ACM.

References

Artz, B., 2010. Fringe benefits and job satisfaction. International journal of manpower, 31(6),

pp.626-644.

Poole, M. and Jenkins, G., 2013. The impact of economic democracy: Profit-sharing and

employee-shareholding schemes. Routledge..

Miles, D., Yang, J. and Marcheggiano, G., 2013. Optimal bank capital. The Economic

Journal, 123(567), pp.1-37.

Da, Z., Guo, R.J. and Jagannathan, R., 2012. CAPM for estimating the cost of equity capital:

Interpreting the empirical evidence. Journal of Financial Economics, 103(1), pp.204-220.

Altunbaş, Y., Kara, A. and Marqués-Ibáñez, D., 2010. Large debt financing: syndicated loans

versus corporate bonds. The European Journal of Finance, 16(5), pp.437-458.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction to

concepts, methods and uses. Cengage Learning.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Weygandt, J.J., Kimmel, P.D., KIESO, D. and Elias, R.Z., 2010. Accounting principles.

Issues in Accounting Education, 25(1), pp.179-180.

Wang, G., Wilson, C., Zhao, X., Zhu, Y., Mohanlal, M., Zheng, H. and Zhao, B.Y., 2012,

April. Serf and turf: crowdturfing for fun and profit. In Proceedings of the 21st international

conference on World Wide Web (pp. 679-688). ACM.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.