Detailed Management Accounting Report: Zylla Company Analysis

VerifiedAdded on 2020/07/23

|18

|4423

|39

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within Zylla Company, a manufacturing firm. It defines management accounting, explores different types of management accounting systems like cost accounting, inventory management, job costing, and price optimization, and their respective requirements. The report delves into various methods of management accounting reporting, including accounts receivable ageing, stock management, segmental reports, operating budget reports, and job costing reports. It demonstrates cost calculation using marginal and absorption costing techniques to prepare income statements, including the relevant workings. Furthermore, the report explains the advantages and disadvantages of different planning tools used in budgetary control, specifically zero-based budgeting. Finally, it outlines how organizations can use management accounting to respond to financial problems, offering insights into financial planning, revaluation accounting, and fund flow statements.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Define management accounting and give requirements of different types of .................1

management accounting.........................................................................................................1

1.2 Methods used in management accounting reporting........................................................3

1.3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costing.............................................................................................4

APPENDIX......................................................................................................................................6

Working Note 1......................................................................................................................6

Working Note 2.....................................................................................................................6

Working Note 3......................................................................................................................7

1.4 Explain the advantages and disadvantages of different types of planning tools used in..7

budgetary control....................................................................................................................7

1.5 Outline the ways in which organisations could use management accounting to respond to

financial problems................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Define management accounting and give requirements of different types of .................1

management accounting.........................................................................................................1

1.2 Methods used in management accounting reporting........................................................3

1.3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costing.............................................................................................4

APPENDIX......................................................................................................................................6

Working Note 1......................................................................................................................6

Working Note 2.....................................................................................................................6

Working Note 3......................................................................................................................7

1.4 Explain the advantages and disadvantages of different types of planning tools used in..7

budgetary control....................................................................................................................7

1.5 Outline the ways in which organisations could use management accounting to respond to

financial problems................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is the vital part of the organisation. It helps to evaluate and

analysed the internal factors of the organisation in that way which increases their ability to

perform well. Management accounting is widely used tool by the organisation. The enclosed

report deals with Zylla Company which is a manufacturing firm which is highly proficient in its

working. Management accounting is used to evaluate the performance of the company so that it

can satisfy the customers (Bryer, 2013). It also helps to measure the performance of the

organisation by using different tools and methods so that it can perform well. The techniques

used are revaluation accounting and fund flow statements. It helps to measure the effectiveness

of the organisation. It also forecasts the performance by matching the actual results with the

budgeted one and take any corrective action if deviations are found. It helps to improve the

overall efficiency of the organisation.

TASK 1

1.1 Define management accounting and give requirements of different types of

management accounting.

Management accounting means to prepare the management reports and accounts to

provide information to the managers so that they mat be abler to taken quick and timely

decisions for the betterment of the company. It provides accurate and timely information about

the financial statements and statistical data to provide the manager for enhanced decision making

on the important matters of the organisation Zylla company also uses management accounting so

that it can achieve its goals within the limited resources. Management accounting is used for

internal reporting only not for external users.

The different types of management accounting and their requirement in organisation is as

follows:

1. Cost accounting system-

Cost accounting system is used which aims to capture and control the costs of the

company so that it can reduce the expenses of different production activities and can achieve

more production within the company and can generate more revenue from it resulting in the

achievement of its goals. It aims to control the fixed expenditure and depreciation. Cost

Management accounting is the vital part of the organisation. It helps to evaluate and

analysed the internal factors of the organisation in that way which increases their ability to

perform well. Management accounting is widely used tool by the organisation. The enclosed

report deals with Zylla Company which is a manufacturing firm which is highly proficient in its

working. Management accounting is used to evaluate the performance of the company so that it

can satisfy the customers (Bryer, 2013). It also helps to measure the performance of the

organisation by using different tools and methods so that it can perform well. The techniques

used are revaluation accounting and fund flow statements. It helps to measure the effectiveness

of the organisation. It also forecasts the performance by matching the actual results with the

budgeted one and take any corrective action if deviations are found. It helps to improve the

overall efficiency of the organisation.

TASK 1

1.1 Define management accounting and give requirements of different types of

management accounting.

Management accounting means to prepare the management reports and accounts to

provide information to the managers so that they mat be abler to taken quick and timely

decisions for the betterment of the company. It provides accurate and timely information about

the financial statements and statistical data to provide the manager for enhanced decision making

on the important matters of the organisation Zylla company also uses management accounting so

that it can achieve its goals within the limited resources. Management accounting is used for

internal reporting only not for external users.

The different types of management accounting and their requirement in organisation is as

follows:

1. Cost accounting system-

Cost accounting system is used which aims to capture and control the costs of the

company so that it can reduce the expenses of different production activities and can achieve

more production within the company and can generate more revenue from it resulting in the

achievement of its goals. It aims to control the fixed expenditure and depreciation. Cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting will first measure and record the expenses individually and then will match with the

input results with the output so that financial performance can be aided in effectual manner. Cost

accounting is most suitable for controlling the budget and setting up the cost control program to

improve the net margin of the company in effective way (Hald and Thrane, 2016).

There are different expenses involved in the organisation. Zylla company refers to

managerial reports which are maintained and provided by the management accounting in

efficient manner which provide as a tool for management to take timely and accurate decisions

for the betterment of the organisation. The costs consist of direct costs, operating costs, fixed

costs, variable costs. Direct costs means that cost which is associated with the production of a

particular product. Operating costs means the costs which are incurred on day to day operations

of the company. Fixed costs are irrelevant to the production of the product. Whether company is

generating profit or loss, it doesn't matter to fixed cost. Fixed costs has to be incurred in the

company like payment of rent of the organisation premises etc. Variable costs are tied up in the

level of production. This expenses are affected when organisation is generating profit or not.

2. Inventory management system-

Inventory management system means organisation will use the inventory in that manner

which satisfies the requirement of the production unit. It is useful for the company as it manages

the inventory in effective way. It provides purchase orders, sales orders which is required so that

inventory is managed. For the company, it is required to manage inventory as it is valuable and

precious asset which needs to be preserved so that it may not deteriorates the benefits from it.

Moreover, more than required inventory leads to additional cost and spoilage as well.

3. Job costing-

It involves cost associated with the specific job. It is useful for the company as it provide

information for direct materials, direct labour and overhead costs. It is required for the company

as it controls the costs of various jobs involved in the organisation. Labour costs and overhead

costs are assessed which are related to each jobs and moreover it may be reduced so that the

profits of firm are maximised too much extent.

4. Price Optimisation-

input results with the output so that financial performance can be aided in effectual manner. Cost

accounting is most suitable for controlling the budget and setting up the cost control program to

improve the net margin of the company in effective way (Hald and Thrane, 2016).

There are different expenses involved in the organisation. Zylla company refers to

managerial reports which are maintained and provided by the management accounting in

efficient manner which provide as a tool for management to take timely and accurate decisions

for the betterment of the organisation. The costs consist of direct costs, operating costs, fixed

costs, variable costs. Direct costs means that cost which is associated with the production of a

particular product. Operating costs means the costs which are incurred on day to day operations

of the company. Fixed costs are irrelevant to the production of the product. Whether company is

generating profit or loss, it doesn't matter to fixed cost. Fixed costs has to be incurred in the

company like payment of rent of the organisation premises etc. Variable costs are tied up in the

level of production. This expenses are affected when organisation is generating profit or not.

2. Inventory management system-

Inventory management system means organisation will use the inventory in that manner

which satisfies the requirement of the production unit. It is useful for the company as it manages

the inventory in effective way. It provides purchase orders, sales orders which is required so that

inventory is managed. For the company, it is required to manage inventory as it is valuable and

precious asset which needs to be preserved so that it may not deteriorates the benefits from it.

Moreover, more than required inventory leads to additional cost and spoilage as well.

3. Job costing-

It involves cost associated with the specific job. It is useful for the company as it provide

information for direct materials, direct labour and overhead costs. It is required for the company

as it controls the costs of various jobs involved in the organisation. Labour costs and overhead

costs are assessed which are related to each jobs and moreover it may be reduced so that the

profits of firm are maximised too much extent.

4. Price Optimisation-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the required for providing information that uses mathematical problems that calculate

how demand and price of the product varies at different levels (Joshi and Li, 2016). It therefore

combines the data with information on expenses and inventory levels to recommend the prices

which will yield more revenue to the company in effectual manner. Moreover, it is useful for the

company when it quotes the price of products in that way by which customers will prefer to buy

it at that price level.

1.2 Methods used in management accounting reporting

1. Accounts receivables ageing:

Accounts ageing report is the report that lists down all the unpaid customer invoices and

credit memos which are unused by date ranges (Soheilirad and Sofian, 2016). The ageing report

is the primary tool for management to track down the unpaid invoices from the customers which

are overdue for the payment. This report is also used for the purpose for the collection and credit

functions which is used by the management to list down all the unpaid payments which are

overdue from the customers.

2. Stock management:

Stock management report helps to maintain the level of inventory in the organisation.

Zylla company also uses the stock management report to keep track on the stock which is

required to be call for the inventory if needed. It lists down the closing and opening inventory to

show the costs required to be measure for calculating the expenditure. Stock management is the

ordering, storing and controlling the inventory in the organisation so that it enables business to

free up the capital for other uses in the organisation.

3. Segmental report:

Segmental report is the reporting of the company of the operating segments which

undertakes in it. Segment reporting is required for public entities and not for the privately held.

Segment reporting is used for giving and providing information to the creditors and investors

regarding the financial information and overall position of the company. It also used to provide

information regarding the operations of the company to the investors and creditors which they

can use in making decisions. An operating segment engages in business activities from which it

how demand and price of the product varies at different levels (Joshi and Li, 2016). It therefore

combines the data with information on expenses and inventory levels to recommend the prices

which will yield more revenue to the company in effectual manner. Moreover, it is useful for the

company when it quotes the price of products in that way by which customers will prefer to buy

it at that price level.

1.2 Methods used in management accounting reporting

1. Accounts receivables ageing:

Accounts ageing report is the report that lists down all the unpaid customer invoices and

credit memos which are unused by date ranges (Soheilirad and Sofian, 2016). The ageing report

is the primary tool for management to track down the unpaid invoices from the customers which

are overdue for the payment. This report is also used for the purpose for the collection and credit

functions which is used by the management to list down all the unpaid payments which are

overdue from the customers.

2. Stock management:

Stock management report helps to maintain the level of inventory in the organisation.

Zylla company also uses the stock management report to keep track on the stock which is

required to be call for the inventory if needed. It lists down the closing and opening inventory to

show the costs required to be measure for calculating the expenditure. Stock management is the

ordering, storing and controlling the inventory in the organisation so that it enables business to

free up the capital for other uses in the organisation.

3. Segmental report:

Segmental report is the reporting of the company of the operating segments which

undertakes in it. Segment reporting is required for public entities and not for the privately held.

Segment reporting is used for giving and providing information to the creditors and investors

regarding the financial information and overall position of the company. It also used to provide

information regarding the operations of the company to the investors and creditors which they

can use in making decisions. An operating segment engages in business activities from which it

may earn revenue and expenses and whose results are continuous reviewed by the chief

operating decision maker for resource allocation decisions in the organisation.

4. Operating budget report:

Operating budget report portrays company expected expenses and incomes to forecast the

budget in effective manner. It estimates the incomes and expenses in consideration with the

performance of the company on quarterly or annual basis. It is required to estimate the historical

data and analysing the different market variables (Nuhu and et.al., 2017). An operation report

takes into account the current trends in the sector, historical sales performance of the company. It

also undertakes products expected to be launched by the company and various competitive forces

in the market. Firms create operating budget to keep the track on the costs of the company and

estimation of the profit margin.

5. Job costing report:

Job costing report involves the cost associated with the accumulation of the costs of

labour, cost of materials, and overhead costs for a specific job in the organisation. It tracks down

the expenditure involved in performing the job (Zimmerman and Yahya-Zadeh, 2011). It is the

primary tool for measuring the individuals' performance to track on the expenses and helps to

reduce the costs of the other job. Job costing is the process of accumulating the costs involved in

performing the job. It allocates the cost for labour , materials as well as overhead for tracking the

job. This report is essential for the management to make decisions for the company (The job

costing system, 2015.).

Evaluate of how management accounting systems and management accounting reporting

integrates in organisation

Management accounting system is integrated with management accounting reporting

providing the valuable information to the managers of the company. It is critically used in the

organisation by the managers so that they can make decisions with reference of the reports which

are required for internal stability of the organisation in better and effective way. It controls the

cost of the various operations which reports provide. As a result, they make quick and timely

decisions.

operating decision maker for resource allocation decisions in the organisation.

4. Operating budget report:

Operating budget report portrays company expected expenses and incomes to forecast the

budget in effective manner. It estimates the incomes and expenses in consideration with the

performance of the company on quarterly or annual basis. It is required to estimate the historical

data and analysing the different market variables (Nuhu and et.al., 2017). An operation report

takes into account the current trends in the sector, historical sales performance of the company. It

also undertakes products expected to be launched by the company and various competitive forces

in the market. Firms create operating budget to keep the track on the costs of the company and

estimation of the profit margin.

5. Job costing report:

Job costing report involves the cost associated with the accumulation of the costs of

labour, cost of materials, and overhead costs for a specific job in the organisation. It tracks down

the expenditure involved in performing the job (Zimmerman and Yahya-Zadeh, 2011). It is the

primary tool for measuring the individuals' performance to track on the expenses and helps to

reduce the costs of the other job. Job costing is the process of accumulating the costs involved in

performing the job. It allocates the cost for labour , materials as well as overhead for tracking the

job. This report is essential for the management to make decisions for the company (The job

costing system, 2015.).

Evaluate of how management accounting systems and management accounting reporting

integrates in organisation

Management accounting system is integrated with management accounting reporting

providing the valuable information to the managers of the company. It is critically used in the

organisation by the managers so that they can make decisions with reference of the reports which

are required for internal stability of the organisation in better and effective way. It controls the

cost of the various operations which reports provide. As a result, they make quick and timely

decisions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costing

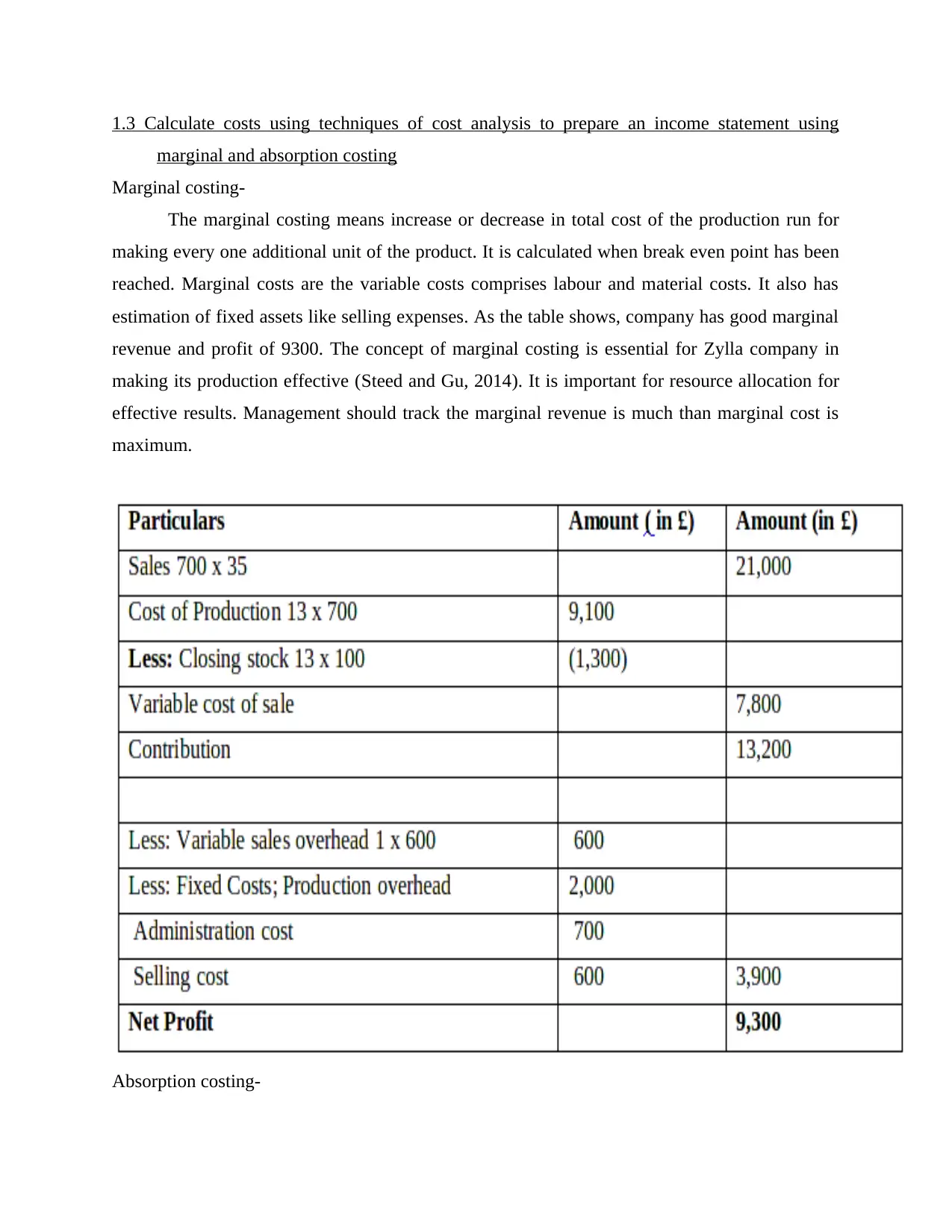

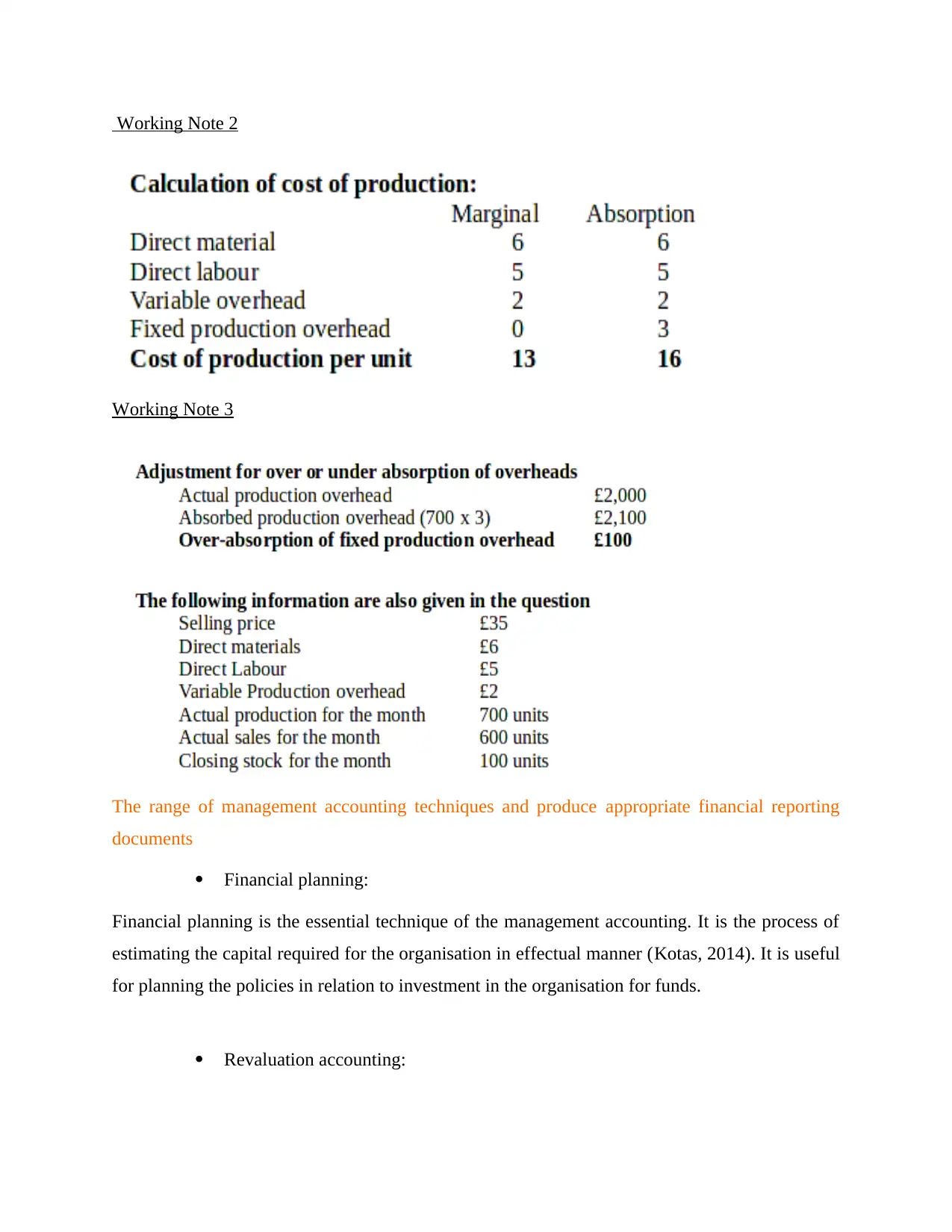

Marginal costing-

The marginal costing means increase or decrease in total cost of the production run for

making every one additional unit of the product. It is calculated when break even point has been

reached. Marginal costs are the variable costs comprises labour and material costs. It also has

estimation of fixed assets like selling expenses. As the table shows, company has good marginal

revenue and profit of 9300. The concept of marginal costing is essential for Zylla company in

making its production effective (Steed and Gu, 2014). It is important for resource allocation for

effective results. Management should track the marginal revenue is much than marginal cost is

maximum.

Absorption costing-

marginal and absorption costing

Marginal costing-

The marginal costing means increase or decrease in total cost of the production run for

making every one additional unit of the product. It is calculated when break even point has been

reached. Marginal costs are the variable costs comprises labour and material costs. It also has

estimation of fixed assets like selling expenses. As the table shows, company has good marginal

revenue and profit of 9300. The concept of marginal costing is essential for Zylla company in

making its production effective (Steed and Gu, 2014). It is important for resource allocation for

effective results. Management should track the marginal revenue is much than marginal cost is

maximum.

Absorption costing-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

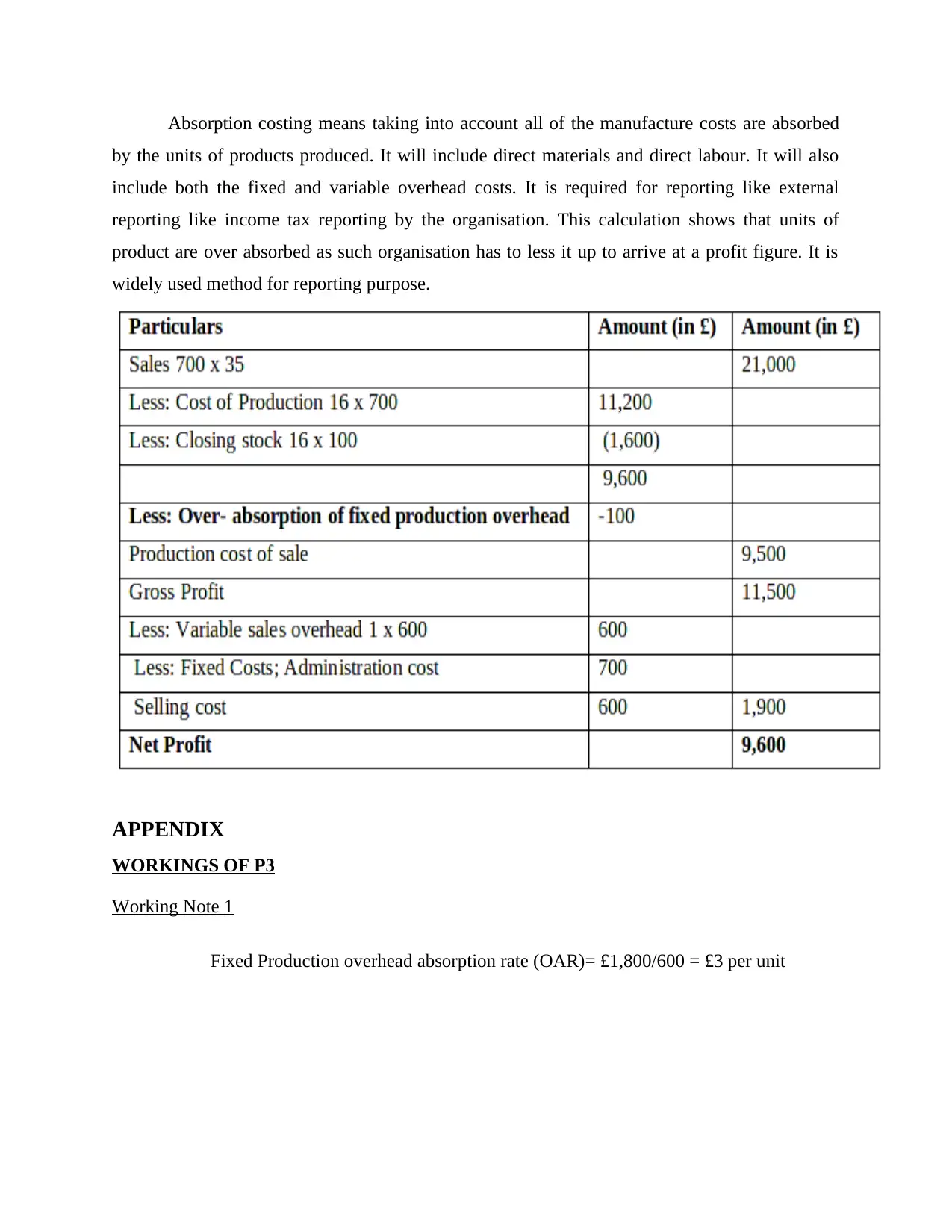

Absorption costing means taking into account all of the manufacture costs are absorbed

by the units of products produced. It will include direct materials and direct labour. It will also

include both the fixed and variable overhead costs. It is required for reporting like external

reporting like income tax reporting by the organisation. This calculation shows that units of

product are over absorbed as such organisation has to less it up to arrive at a profit figure. It is

widely used method for reporting purpose.

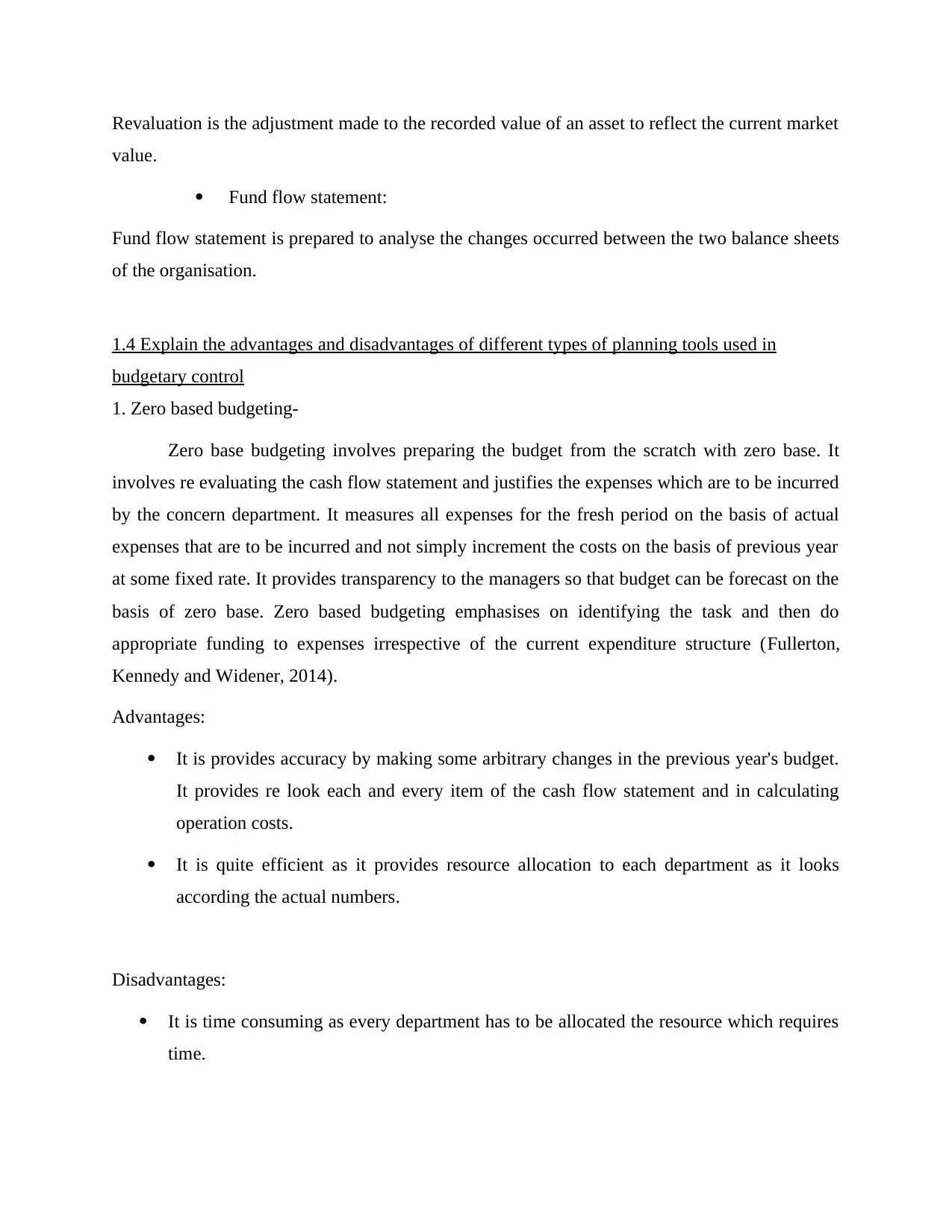

APPENDIX

WORKINGS OF P3

Working Note 1

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

by the units of products produced. It will include direct materials and direct labour. It will also

include both the fixed and variable overhead costs. It is required for reporting like external

reporting like income tax reporting by the organisation. This calculation shows that units of

product are over absorbed as such organisation has to less it up to arrive at a profit figure. It is

widely used method for reporting purpose.

APPENDIX

WORKINGS OF P3

Working Note 1

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

Working Note 2

Working Note 3

The range of management accounting techniques and produce appropriate financial reporting

documents

Financial planning:

Financial planning is the essential technique of the management accounting. It is the process of

estimating the capital required for the organisation in effectual manner (Kotas, 2014). It is useful

for planning the policies in relation to investment in the organisation for funds.

Revaluation accounting:

Working Note 3

The range of management accounting techniques and produce appropriate financial reporting

documents

Financial planning:

Financial planning is the essential technique of the management accounting. It is the process of

estimating the capital required for the organisation in effectual manner (Kotas, 2014). It is useful

for planning the policies in relation to investment in the organisation for funds.

Revaluation accounting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Revaluation is the adjustment made to the recorded value of an asset to reflect the current market

value.

Fund flow statement:

Fund flow statement is prepared to analyse the changes occurred between the two balance sheets

of the organisation.

1.4 Explain the advantages and disadvantages of different types of planning tools used in

budgetary control

1. Zero based budgeting-

Zero base budgeting involves preparing the budget from the scratch with zero base. It

involves re evaluating the cash flow statement and justifies the expenses which are to be incurred

by the concern department. It measures all expenses for the fresh period on the basis of actual

expenses that are to be incurred and not simply increment the costs on the basis of previous year

at some fixed rate. It provides transparency to the managers so that budget can be forecast on the

basis of zero base. Zero based budgeting emphasises on identifying the task and then do

appropriate funding to expenses irrespective of the current expenditure structure (Fullerton,

Kennedy and Widener, 2014).

Advantages:

It is provides accuracy by making some arbitrary changes in the previous year's budget.

It provides re look each and every item of the cash flow statement and in calculating

operation costs.

It is quite efficient as it provides resource allocation to each department as it looks

according the actual numbers.

Disadvantages:

It is time consuming as every department has to be allocated the resource which requires

time.

value.

Fund flow statement:

Fund flow statement is prepared to analyse the changes occurred between the two balance sheets

of the organisation.

1.4 Explain the advantages and disadvantages of different types of planning tools used in

budgetary control

1. Zero based budgeting-

Zero base budgeting involves preparing the budget from the scratch with zero base. It

involves re evaluating the cash flow statement and justifies the expenses which are to be incurred

by the concern department. It measures all expenses for the fresh period on the basis of actual

expenses that are to be incurred and not simply increment the costs on the basis of previous year

at some fixed rate. It provides transparency to the managers so that budget can be forecast on the

basis of zero base. Zero based budgeting emphasises on identifying the task and then do

appropriate funding to expenses irrespective of the current expenditure structure (Fullerton,

Kennedy and Widener, 2014).

Advantages:

It is provides accuracy by making some arbitrary changes in the previous year's budget.

It provides re look each and every item of the cash flow statement and in calculating

operation costs.

It is quite efficient as it provides resource allocation to each department as it looks

according the actual numbers.

Disadvantages:

It is time consuming as every department has to be allocated the resource which requires

time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is complex procedure as every line item and every expense has to be explained which

requires training to managers.

2. Fixed budgeting-

Fixed budgeting is the budget which remains constant. It remains fixed like other factor

such as sales volume. A fixed budget is based on the anticipated level of output and revenue at

start of the accounting period (Grabner and Moers, 2013). It is typically based on data that is

collected and analysed before accounting period begins.

Advantages:

Fixed budgeting is easy to implement and follow. It does not need to be continuously

updated throughout the accounting period.

It provides strong insight into company's costs and revenue when a variance analysis is

performed in the organisation (Miriam, C., 2011. The Advantages of Using a Fixed

Budget).

It also provides company to see where it may be overestimating or underestimating the

expenses and revenues so that it can make changes.

Disadvantages:

It lacks flexibility because it is fixed in nature. If company establishes budget based on

sales volume and that volume increases, it cannot alter changes to increase the budget for

it.

As fixed budget is based on historical data, newer businesses find it difficult to

implement it in the organisation.

Fixed budget is based on historical figures. So, it cannot experience fluctuations in the

budgets. It is useful only for company having high predicability of sales and costs.

3. Incremental budgeting-

requires training to managers.

2. Fixed budgeting-

Fixed budgeting is the budget which remains constant. It remains fixed like other factor

such as sales volume. A fixed budget is based on the anticipated level of output and revenue at

start of the accounting period (Grabner and Moers, 2013). It is typically based on data that is

collected and analysed before accounting period begins.

Advantages:

Fixed budgeting is easy to implement and follow. It does not need to be continuously

updated throughout the accounting period.

It provides strong insight into company's costs and revenue when a variance analysis is

performed in the organisation (Miriam, C., 2011. The Advantages of Using a Fixed

Budget).

It also provides company to see where it may be overestimating or underestimating the

expenses and revenues so that it can make changes.

Disadvantages:

It lacks flexibility because it is fixed in nature. If company establishes budget based on

sales volume and that volume increases, it cannot alter changes to increase the budget for

it.

As fixed budget is based on historical data, newer businesses find it difficult to

implement it in the organisation.

Fixed budget is based on historical figures. So, it cannot experience fluctuations in the

budgets. It is useful only for company having high predicability of sales and costs.

3. Incremental budgeting-

Incremental budgeting is used to prepare the budgets using the previous year data or the

actual performance as a basis for incremental amount which is added for the new period for the

effectiveness of the organisation (Baldvinsdottir, Mitchell and Nørreklit, 2010). The resources

are based on allocation from the previous allocations.

Advantages:

The incremental budget is quite stable and gradual in nature. It does not fluctuate

regularly which helps the firm in effectual manner.

The system is relative easy to operate and easy to understand as it only increments the

value from the previous period data.

It is easy for managers to operate their concern department. So, that it provide efficiency

in the organisation to make optimised budgets in timely manner.

Disadvantages:

There is no innovative ideas in the organisation as it is based on the incremental basis

which is done on the past data.

Incremental budgeting is not based on the principle of reducing expenditure. This is the

drawback as no effort is made to reduce the costs and as such resources are not properly

utilised.

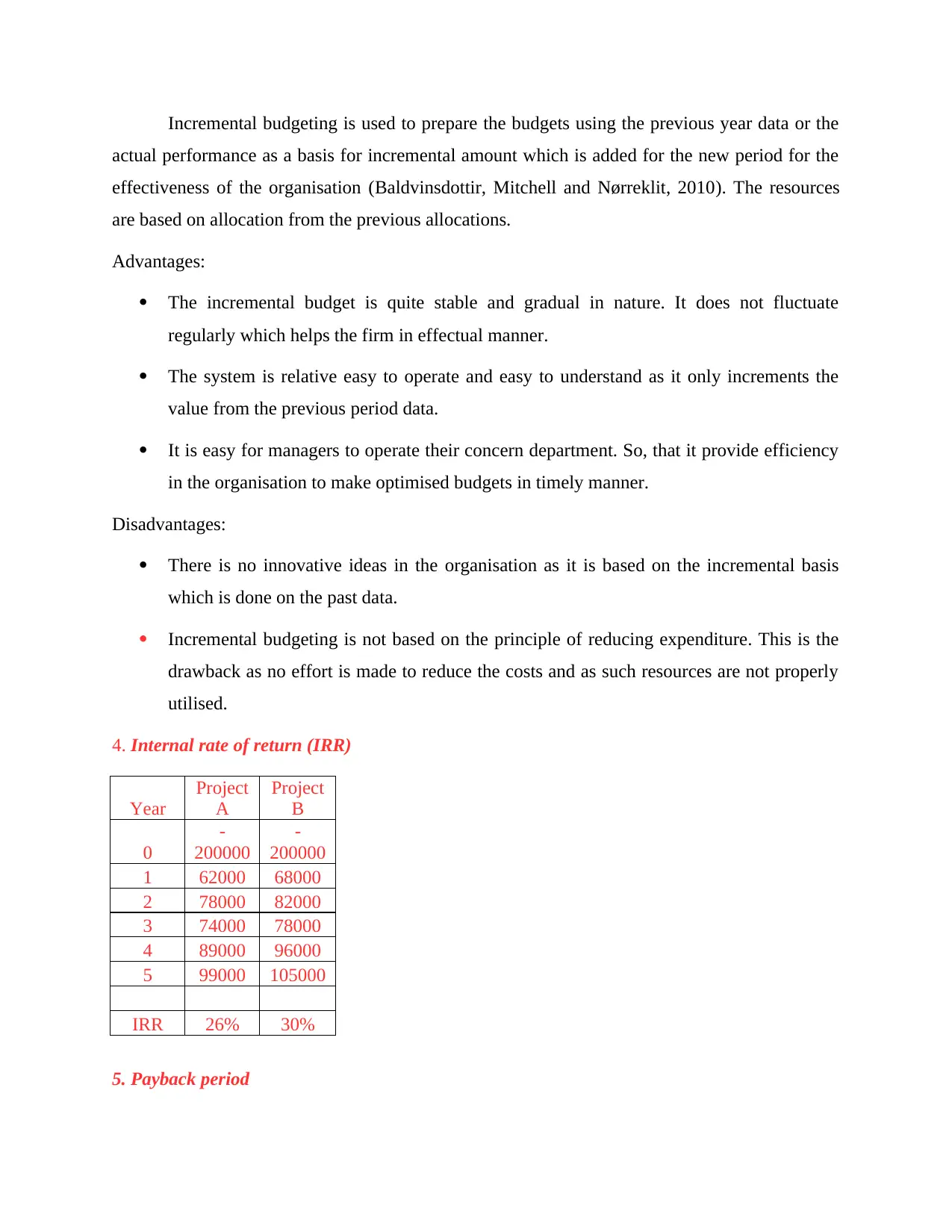

4. Internal rate of return (IRR)

Year

Project

A

Project

B

0

-

200000

-

200000

1 62000 68000

2 78000 82000

3 74000 78000

4 89000 96000

5 99000 105000

IRR 26% 30%

5. Payback period

actual performance as a basis for incremental amount which is added for the new period for the

effectiveness of the organisation (Baldvinsdottir, Mitchell and Nørreklit, 2010). The resources

are based on allocation from the previous allocations.

Advantages:

The incremental budget is quite stable and gradual in nature. It does not fluctuate

regularly which helps the firm in effectual manner.

The system is relative easy to operate and easy to understand as it only increments the

value from the previous period data.

It is easy for managers to operate their concern department. So, that it provide efficiency

in the organisation to make optimised budgets in timely manner.

Disadvantages:

There is no innovative ideas in the organisation as it is based on the incremental basis

which is done on the past data.

Incremental budgeting is not based on the principle of reducing expenditure. This is the

drawback as no effort is made to reduce the costs and as such resources are not properly

utilised.

4. Internal rate of return (IRR)

Year

Project

A

Project

B

0

-

200000

-

200000

1 62000 68000

2 78000 82000

3 74000 78000

4 89000 96000

5 99000 105000

IRR 26% 30%

5. Payback period

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.