Financial Analysis Report: Company Performance Evaluation

VerifiedAdded on 2023/06/06

|5

|667

|318

Report

AI Summary

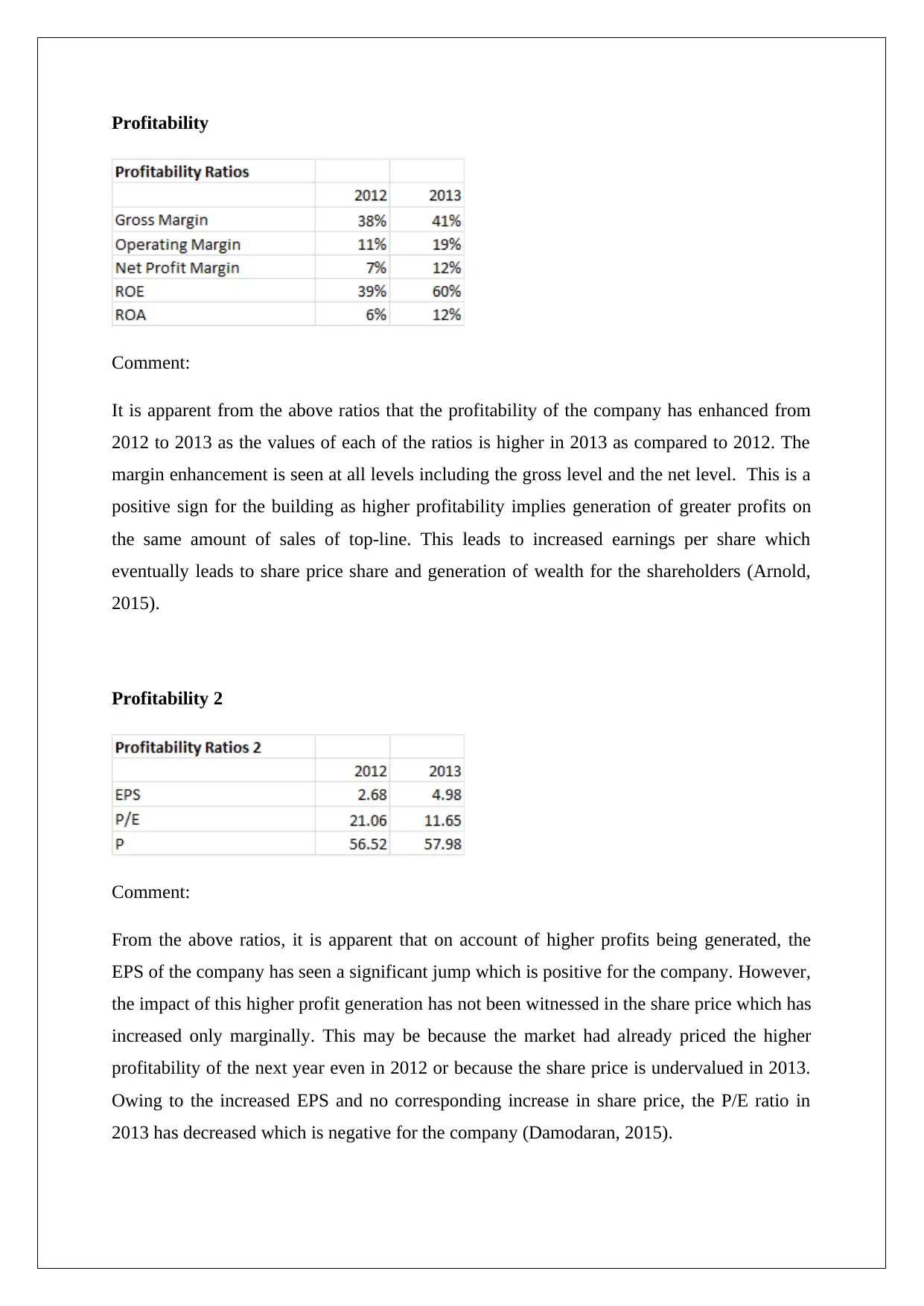

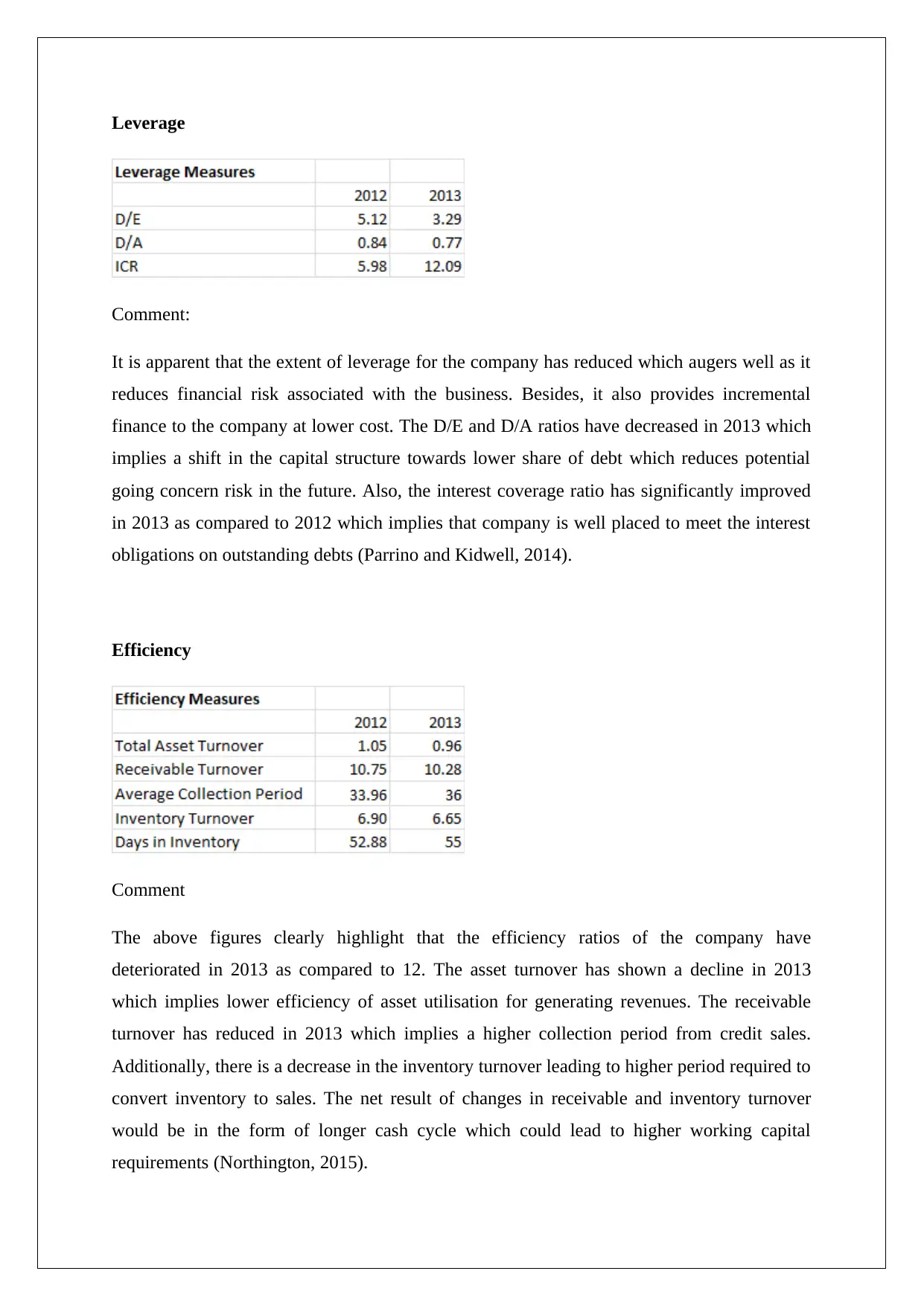

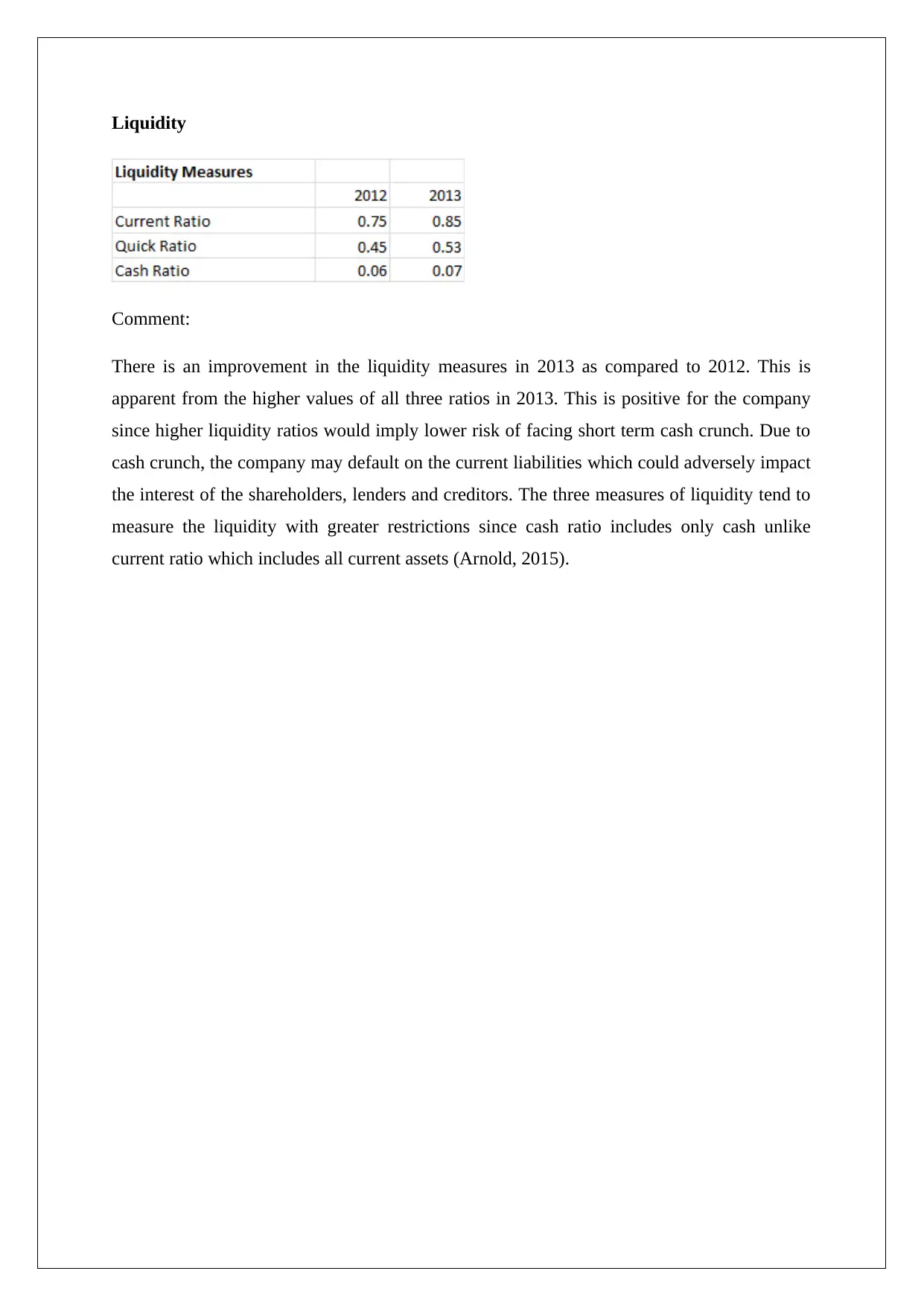

This report presents a financial analysis of a company, evaluating its performance across several key areas. The analysis begins with an assessment of profitability, comparing ratios from 2012 to 2013 to highlight improvements in gross and net margins, and discussing the impact on earnings per share and share price. The report then examines leverage, noting a reduction in the company's debt-to-equity and debt-to-assets ratios, which indicates decreased financial risk and improved interest coverage. Efficiency is analyzed, revealing a decline in asset turnover, receivable turnover, and inventory turnover, which suggests lower efficiency in asset utilization and longer collection and conversion periods. Finally, the report assesses liquidity, indicating an improvement in liquidity measures in 2013 compared to 2012, reducing the risk of short-term cash crunches. The analysis references key financial management texts and provides a comprehensive overview of the company's financial health and performance trends.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.