Analysis of Financial Accounting Concepts: Cochlear Limited Report

VerifiedAdded on 2022/10/19

|9

|3437

|15

Report

AI Summary

This report provides a detailed analysis of advanced financial accounting concepts, specifically within the context of Cochlear Limited. It begins by identifying and describing key accounting concepts as defined by the Australian Accounting Standard Board (AASB), including financial statements, reporting entities, elements of financial statements, recognition and derecognition, measurement, presentation, and disclosure. The report then delves into the measurement issues, contrasting historical cost and fair value measurement bases, and discussing their relevance and application. Furthermore, the report examines the fundamental qualitative characteristics of financial information, emphasizing relevance and faithful representation, and their importance in making financial information useful for decision-making. Throughout the report, the analysis is grounded in the 2018 Annual Report of Cochlear Limited, illustrating how these concepts are applied in practice. The report concludes by summarizing the key findings and their implications for effective financial accounting.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Advanced Financial Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction...................................................................................................................2

Identification and Description of Accounting Concepts................................................2

Discussion on Issues of Measurement.........................................................................3

Fundamental Qualitative Characteristics......................................................................4

Conclusion....................................................................................................................7

References...................................................................................................................8

Table of Contents

Introduction...................................................................................................................2

Identification and Description of Accounting Concepts................................................2

Discussion on Issues of Measurement.........................................................................3

Fundamental Qualitative Characteristics......................................................................4

Conclusion....................................................................................................................7

References...................................................................................................................8

2ADVANCED FINANCIAL ACCOUNTING

Introduction

The managements of the companies are needed to take into consideration of

certain accounting concepts in the process of financial accounting and these

concepts are crucial for the business success. In Australia, the companies are

needed to comply with different requirements of the Accounting Conceptual

Framework of the Australian Accounting Standard Board (AASB) for the purpose of

financial reporting (Cheng et al.2014). This aspect helps the companies in

addressing the measurement related issue within the organizations. The AASB

conceptual framework states that the companies are needed to put major emphasis

on both the fundamental qualitative characteristics of financial statements for the

effective measurement as well as accounting treatments of the organizational assets

and liabilities (Simnett and Huggins 2015). Consideration of these aspects leads to

the development of effective financial accounting systems within the organizations.

There are three parts of the report. The first part of the report discusses about

different accounting concepts and relates them with the chosen company. The

second part of the report addresses the measurement issues of AASB in respect to

the selected company. The last part of the report discusses about the fundamental

qualitative characteristics of financial information of the chosen company. For the

purpose of the report, Cochlear Limited is taken into consideration.

Identification and Description of Accounting Concepts

It can be seen from the above that the Australian companies are required to

comply with the accounting conceptual framework of the AASB for the purpose of

financial accounting. In this process, the companies are needed to adopt the

accounting concepts provided in the conceptual framework of AASB (aasb.gov.au

2019). It can be seen from the conceptual framework of AASB that there are certain

accounting concepts that the companies are needed to adopt for the purpose of

financial reporting. These concepts are Financial statements and reporting entities,

Elements of financial statements, Recognition and Derecognition, Measurement,

Presentation and disclosure and Concepts of capital and capital management

(aasb.gov.au 2019). These concepts are discussed below in general and in relation

to Cochlear Limited.

Financial Statements and Reporting Entities – This accounting concept deals with

the role of financial statements and the concept of reporting entity. It states that the

main objective of financial statements is to provide information on the company’s

assets, liabilities, equity, income and expenses (Barth 2013). As per the 2018 Annual

Report of Cochlear Limited, the company has provide the financial statements such

as income statement, balance sheet and others that provide this information. Going

concern is considered as another major accounting concept which states that the

reporting entity is going concern and will continue for foreseeable future. According

to the 2018 Annual Report of Cochlear Limited, the main objective of the capital

management of the company is safeguarding their ability to continue as a going

concern (aasb.gov.au 2019).

Elements of Financial Statement – The main components of this accounting

concepts are definition of assets, liabilities, equity, income and expenses. According

to AASB conceptual framework, asset can be considered as a present resource of a

company as a result of past events. Liability can be considered as a present

obligation of an entity for transferring an economic resource due to past events

(Weil, Schipper and Francis 2013). After that, equity is considered as a residual

Introduction

The managements of the companies are needed to take into consideration of

certain accounting concepts in the process of financial accounting and these

concepts are crucial for the business success. In Australia, the companies are

needed to comply with different requirements of the Accounting Conceptual

Framework of the Australian Accounting Standard Board (AASB) for the purpose of

financial reporting (Cheng et al.2014). This aspect helps the companies in

addressing the measurement related issue within the organizations. The AASB

conceptual framework states that the companies are needed to put major emphasis

on both the fundamental qualitative characteristics of financial statements for the

effective measurement as well as accounting treatments of the organizational assets

and liabilities (Simnett and Huggins 2015). Consideration of these aspects leads to

the development of effective financial accounting systems within the organizations.

There are three parts of the report. The first part of the report discusses about

different accounting concepts and relates them with the chosen company. The

second part of the report addresses the measurement issues of AASB in respect to

the selected company. The last part of the report discusses about the fundamental

qualitative characteristics of financial information of the chosen company. For the

purpose of the report, Cochlear Limited is taken into consideration.

Identification and Description of Accounting Concepts

It can be seen from the above that the Australian companies are required to

comply with the accounting conceptual framework of the AASB for the purpose of

financial accounting. In this process, the companies are needed to adopt the

accounting concepts provided in the conceptual framework of AASB (aasb.gov.au

2019). It can be seen from the conceptual framework of AASB that there are certain

accounting concepts that the companies are needed to adopt for the purpose of

financial reporting. These concepts are Financial statements and reporting entities,

Elements of financial statements, Recognition and Derecognition, Measurement,

Presentation and disclosure and Concepts of capital and capital management

(aasb.gov.au 2019). These concepts are discussed below in general and in relation

to Cochlear Limited.

Financial Statements and Reporting Entities – This accounting concept deals with

the role of financial statements and the concept of reporting entity. It states that the

main objective of financial statements is to provide information on the company’s

assets, liabilities, equity, income and expenses (Barth 2013). As per the 2018 Annual

Report of Cochlear Limited, the company has provide the financial statements such

as income statement, balance sheet and others that provide this information. Going

concern is considered as another major accounting concept which states that the

reporting entity is going concern and will continue for foreseeable future. According

to the 2018 Annual Report of Cochlear Limited, the main objective of the capital

management of the company is safeguarding their ability to continue as a going

concern (aasb.gov.au 2019).

Elements of Financial Statement – The main components of this accounting

concepts are definition of assets, liabilities, equity, income and expenses. According

to AASB conceptual framework, asset can be considered as a present resource of a

company as a result of past events. Liability can be considered as a present

obligation of an entity for transferring an economic resource due to past events

(Weil, Schipper and Francis 2013). After that, equity is considered as a residual

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

interest in the asset after the deduction of all of its liabilities. Income can be

considered as the increase in assets or decrease in liabilities which leads to the

increase in equity. On the other hand, expenses are considered as increase in

liabilities or decrease in asses that leads to the decrease in equity. It can be seen

from the 2018 Annual Report of Cochlear Limited that the company has reported

their assets, liabilities, equity, income and expenses in their financial statements.

Recognition and Derecognition – Recognition and derecogntion are considered as

two specific accounting concept as per the accounting conceptual framework of the

AASB. Recognition is considered as the process to capture and item that satisfies

the definition of an element with the aim to include that element in the statement of

financial position and income statement (Măciucă, Hlaciuc and Ursache 2015). At

the same time, derecognition is considered as the process of removing a part or the

whole part of a pre-recognized asset or liability from the statement of financial

position of a company. It can be seen from the 2018 Annual Report of Cochlear

Limited that the company has used this concept in the process of their financial

reporting with the proper recognition of their assets and liabilities.

Measurement – The concept of measurement is considered as one of the most

crucial concepts for the companies. According to the AASB conceptual framework,

there are two types of measurement which are historical cost and current value. As

per the AASB conceptual framework, the historical cost measurement base helps in

providing monetary value about the assets, liabilities, income and expenses with the

information derived from the transaction or event (Ryan et al. 2014). It also states

that current value includes both fair value measurement and value in use. As per the

annual report of Cochlear Limited, the company has used both the historical cost and

fair value measurement for measuring their different assets and liabilities.

Presentation and Disclosure – According to the AASB conceptual framework,

presentation and disclosure can be considered as the communication tools for

providing information about the recognized assets, liabilities, equity, income and

expenses (aasb.gov.au 2019). Thus, the companies are needed to ensure effective

presentation as well as disclosure of all information of their financial substances. It

can be seen from the 2018 Annual Report of Cochlear Limited that the company has

effectively presented as well as disclosed all relevant information of their assets,

liabilities, equity, income and expenses (Luke 2016).

Discussion on Issues of Measurement

Measurement of considered as a crucial concept in financial reporting of the

companies. According to the AASB conceptual framework, the presence of two

measurement bases can be seen; they are historical cost measurement and fair

value measurement (aasb.gov.au 2019). As per AASB conceptual framework, fair

value can be considered as the price that an entity receive for selling an asset or

paying or transferring a liability in an orderly transaction between the market

participants at the date of measurement (Hodder, Hopkins and Schipper 2014). In

this context, it needs to be mentioned that the fair value measurement reflects the

actual market price of the assets and liabilities at the current date. On the other

hand, historical cost measurement base shows the values of the assets and liabilities

at ta date of acquisition or transaction (Linsmeier 2013). Thus, it can be seen that

there is difference between fair value measurement and historical cost measurement

bases.

The presence of a major debate can be seen regarding the measurement

concept and the debate can be seen between fair value measurement and historical

interest in the asset after the deduction of all of its liabilities. Income can be

considered as the increase in assets or decrease in liabilities which leads to the

increase in equity. On the other hand, expenses are considered as increase in

liabilities or decrease in asses that leads to the decrease in equity. It can be seen

from the 2018 Annual Report of Cochlear Limited that the company has reported

their assets, liabilities, equity, income and expenses in their financial statements.

Recognition and Derecognition – Recognition and derecogntion are considered as

two specific accounting concept as per the accounting conceptual framework of the

AASB. Recognition is considered as the process to capture and item that satisfies

the definition of an element with the aim to include that element in the statement of

financial position and income statement (Măciucă, Hlaciuc and Ursache 2015). At

the same time, derecognition is considered as the process of removing a part or the

whole part of a pre-recognized asset or liability from the statement of financial

position of a company. It can be seen from the 2018 Annual Report of Cochlear

Limited that the company has used this concept in the process of their financial

reporting with the proper recognition of their assets and liabilities.

Measurement – The concept of measurement is considered as one of the most

crucial concepts for the companies. According to the AASB conceptual framework,

there are two types of measurement which are historical cost and current value. As

per the AASB conceptual framework, the historical cost measurement base helps in

providing monetary value about the assets, liabilities, income and expenses with the

information derived from the transaction or event (Ryan et al. 2014). It also states

that current value includes both fair value measurement and value in use. As per the

annual report of Cochlear Limited, the company has used both the historical cost and

fair value measurement for measuring their different assets and liabilities.

Presentation and Disclosure – According to the AASB conceptual framework,

presentation and disclosure can be considered as the communication tools for

providing information about the recognized assets, liabilities, equity, income and

expenses (aasb.gov.au 2019). Thus, the companies are needed to ensure effective

presentation as well as disclosure of all information of their financial substances. It

can be seen from the 2018 Annual Report of Cochlear Limited that the company has

effectively presented as well as disclosed all relevant information of their assets,

liabilities, equity, income and expenses (Luke 2016).

Discussion on Issues of Measurement

Measurement of considered as a crucial concept in financial reporting of the

companies. According to the AASB conceptual framework, the presence of two

measurement bases can be seen; they are historical cost measurement and fair

value measurement (aasb.gov.au 2019). As per AASB conceptual framework, fair

value can be considered as the price that an entity receive for selling an asset or

paying or transferring a liability in an orderly transaction between the market

participants at the date of measurement (Hodder, Hopkins and Schipper 2014). In

this context, it needs to be mentioned that the fair value measurement reflects the

actual market price of the assets and liabilities at the current date. On the other

hand, historical cost measurement base shows the values of the assets and liabilities

at ta date of acquisition or transaction (Linsmeier 2013). Thus, it can be seen that

there is difference between fair value measurement and historical cost measurement

bases.

The presence of a major debate can be seen regarding the measurement

concept and the debate can be seen between fair value measurement and historical

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

cost measurement (Blankespoor et al. 2013). As per the proponents of the fair value

accounting, this is a more relevant measure because it captures aspects like market

trend, depreciation and others and thus, it makes the values of the assets and

liabilities more current as well as relevant. However, the measure of historical cost

accounting is considered as a more conservative idea which is also perceived as

reliable. Fair value accounting was vastly used in the 19th and early 20th centuries.

However, at the time of the economic collapse of US in 1920’s, the fair value

accounting was majorly blamed in the presence of its tendency to overstate the

value of the assets. It needs to be mentioned that this is an ever continuing debate.

However, AASB has provided the companies with the permission to use these

measurement bases on the basis of the nature of their businesses and needs

(Magnan, Menini and Parbonetti 2015).

It can be seen from the 2018 Annual Report of Cochlear Limited that the

company has used both the historical cost accounting as well as fair value

accounting based on their business needs. As per Note 1.2 (b), the company has

prepared their consolidated financial statements on the basis of historical cost

accounting and they have used fair value accounting measurement base for the

measurement of derivative financial instruments and the investments available for

sales (cochlear.com 2019).

According to the 2018 Annual Report, the company has measured their

inventory at the lower of cost and net realizable value (cochlear.com 2019). At the

same time, the company has measured the value of property, plant and equipment

at the cost price after the deduction of the aspects like accumulated depreciation and

impairment losses. The same aspect can be seen in the case of Goodwill since the

company has measured their goodwill at cost value after the deduction of any

accumulated impairment losses (cochlear.com 2019).

At the same time, Cochlear Limited has measured their investments at fair

value by adding directly attributed transaction costs. After that, the company has

done the initial recognition of the net debts at fair value after the deduction of

attributable transaction costs (cochlear.com 2019). In addition, the company has

recognized the forward exchange contracts initially at fair value and their

measurement is also done based on fair value accounting. It needs to be mentioned

that Cochlear Limited uses the three tier fair value model for the valuation of the

selected assets and liabilities (cochlear.com 2019).

Thus, it can be seen from the above discussion that the management of

Cochlear Limited has addressed the issue of measurement through the adoption of

both the measurement bases for their selected assets and liabilities. The

management of Cochlear Limited has adopted these methods based on their

business needs.

Fundamental Qualitative Characteristics

In case the financial information is to be useful, it is required that they must be

relevant as well as faithfully represented. The presence of two fundamental

qualitative characteristics of financial information can be seen; they are Reliance and

Faithful Representation (aasb.gov.au 2019). It needs to be mentioned that both of

these characteristics are useful in order to make the financial information useful.

These are discussed below.

Relevance – It needs to be mentioned it is possible to make positive difference in

the decision-making process of the users in case the information is relevant.

Information become relevant when they have both confirmatory value and predictive

cost measurement (Blankespoor et al. 2013). As per the proponents of the fair value

accounting, this is a more relevant measure because it captures aspects like market

trend, depreciation and others and thus, it makes the values of the assets and

liabilities more current as well as relevant. However, the measure of historical cost

accounting is considered as a more conservative idea which is also perceived as

reliable. Fair value accounting was vastly used in the 19th and early 20th centuries.

However, at the time of the economic collapse of US in 1920’s, the fair value

accounting was majorly blamed in the presence of its tendency to overstate the

value of the assets. It needs to be mentioned that this is an ever continuing debate.

However, AASB has provided the companies with the permission to use these

measurement bases on the basis of the nature of their businesses and needs

(Magnan, Menini and Parbonetti 2015).

It can be seen from the 2018 Annual Report of Cochlear Limited that the

company has used both the historical cost accounting as well as fair value

accounting based on their business needs. As per Note 1.2 (b), the company has

prepared their consolidated financial statements on the basis of historical cost

accounting and they have used fair value accounting measurement base for the

measurement of derivative financial instruments and the investments available for

sales (cochlear.com 2019).

According to the 2018 Annual Report, the company has measured their

inventory at the lower of cost and net realizable value (cochlear.com 2019). At the

same time, the company has measured the value of property, plant and equipment

at the cost price after the deduction of the aspects like accumulated depreciation and

impairment losses. The same aspect can be seen in the case of Goodwill since the

company has measured their goodwill at cost value after the deduction of any

accumulated impairment losses (cochlear.com 2019).

At the same time, Cochlear Limited has measured their investments at fair

value by adding directly attributed transaction costs. After that, the company has

done the initial recognition of the net debts at fair value after the deduction of

attributable transaction costs (cochlear.com 2019). In addition, the company has

recognized the forward exchange contracts initially at fair value and their

measurement is also done based on fair value accounting. It needs to be mentioned

that Cochlear Limited uses the three tier fair value model for the valuation of the

selected assets and liabilities (cochlear.com 2019).

Thus, it can be seen from the above discussion that the management of

Cochlear Limited has addressed the issue of measurement through the adoption of

both the measurement bases for their selected assets and liabilities. The

management of Cochlear Limited has adopted these methods based on their

business needs.

Fundamental Qualitative Characteristics

In case the financial information is to be useful, it is required that they must be

relevant as well as faithfully represented. The presence of two fundamental

qualitative characteristics of financial information can be seen; they are Reliance and

Faithful Representation (aasb.gov.au 2019). It needs to be mentioned that both of

these characteristics are useful in order to make the financial information useful.

These are discussed below.

Relevance – It needs to be mentioned it is possible to make positive difference in

the decision-making process of the users in case the information is relevant.

Information become relevant when they have both confirmatory value and predictive

5ADVANCED FINANCIAL ACCOUNTING

value. Confirmatory value increases the usefulness of the information through

providing feedback about the previous judgements (Herath and Albarqi 2017). On

the other hand, predictive value makes the information useful by making the

decision-makers able in predicting the future outcome of the companies. Materiality

and measurement uncertainty is considered as other crucial aspects in this for

increasing the usefulness of the information (Cohen and Karatzimas 2017).

Faithful Representation – It is needed for the managements of the companies to

ensure the faithful representation of the financial information along with representing

the relevant phenomena in order to make the information useful for the decision-

makers. There are three crucial elements that need to be there for ensuring faithful

representation of financial information; they are complete, neutral and free from

errors. An economic phenomena with complete, neutral and error free description is

paramount to the users of the financial statements to make effusive investment and

other decisions (Biondi and Lapsley 2014).

The investors are needed to follow certain steps for ensuring whether the

company has presented these two characteristics of financial information. First, it is

needed to consider an essential economic phenomena about the company. Second,

it is needed to identify the types of information that would be most relevant in case it

is available and it can be faithful represented. Third, it is needed to determine

whether the financial statements contain this information and they can be faithfully

represented. These steps satisfy the process to satisfy these two characteristic of

financial information.

It can be seen from the 2018 Annual Report of Cochlear Limited that the

company has satisfied these two fundamental qualitative characteristics of financial

information. Specific examples are provided below.

It needs to be mentioned that three major aspects of the financial statements

of the companies are assets, non-current assets and liabilities. It can be seen from

the 2018 Annual Report of Cochlear Limited that the company has faithfully

presented the most relevant information on these aspects in their financial

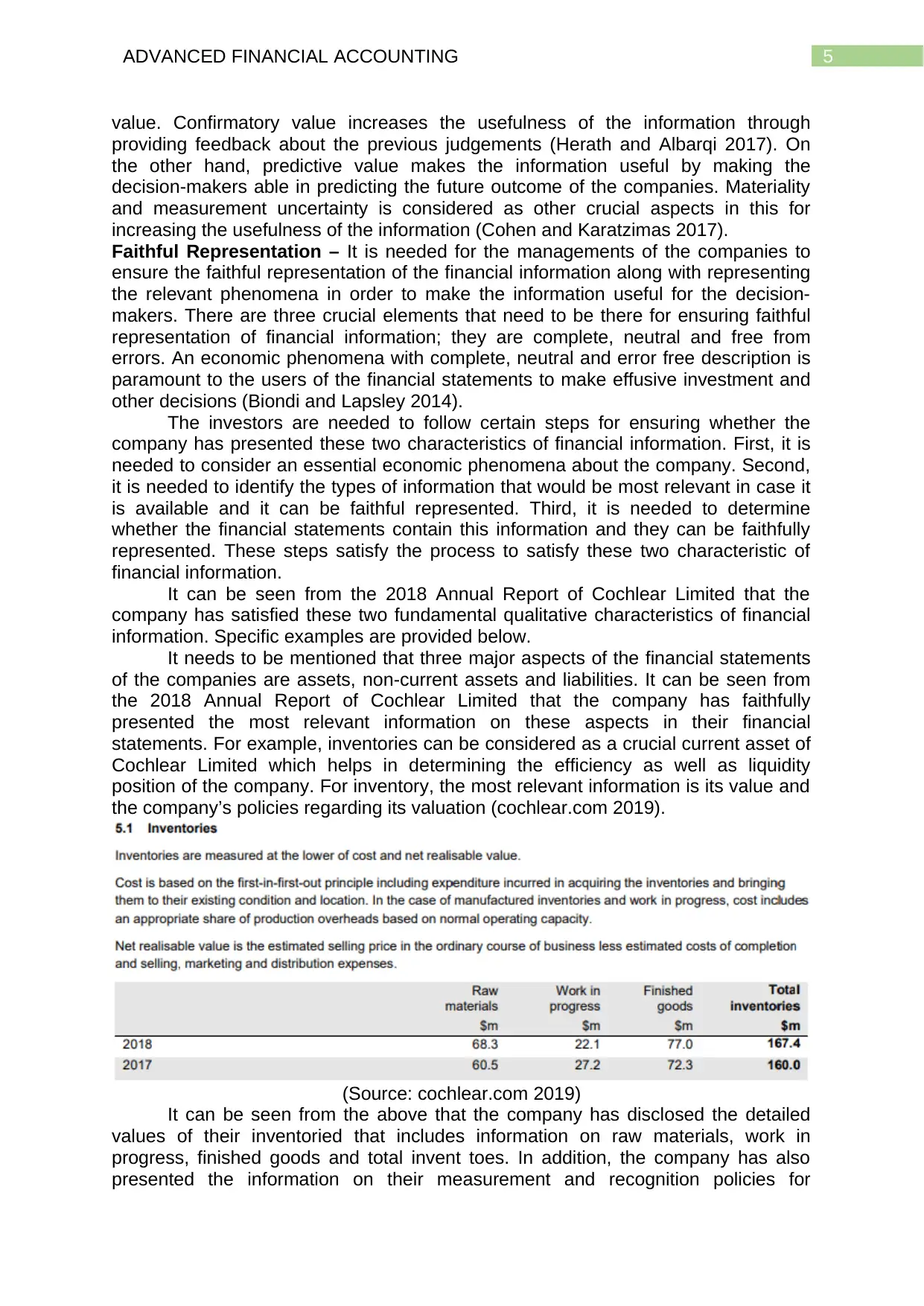

statements. For example, inventories can be considered as a crucial current asset of

Cochlear Limited which helps in determining the efficiency as well as liquidity

position of the company. For inventory, the most relevant information is its value and

the company’s policies regarding its valuation (cochlear.com 2019).

(Source: cochlear.com 2019)

It can be seen from the above that the company has disclosed the detailed

values of their inventoried that includes information on raw materials, work in

progress, finished goods and total invent toes. In addition, the company has also

presented the information on their measurement and recognition policies for

value. Confirmatory value increases the usefulness of the information through

providing feedback about the previous judgements (Herath and Albarqi 2017). On

the other hand, predictive value makes the information useful by making the

decision-makers able in predicting the future outcome of the companies. Materiality

and measurement uncertainty is considered as other crucial aspects in this for

increasing the usefulness of the information (Cohen and Karatzimas 2017).

Faithful Representation – It is needed for the managements of the companies to

ensure the faithful representation of the financial information along with representing

the relevant phenomena in order to make the information useful for the decision-

makers. There are three crucial elements that need to be there for ensuring faithful

representation of financial information; they are complete, neutral and free from

errors. An economic phenomena with complete, neutral and error free description is

paramount to the users of the financial statements to make effusive investment and

other decisions (Biondi and Lapsley 2014).

The investors are needed to follow certain steps for ensuring whether the

company has presented these two characteristics of financial information. First, it is

needed to consider an essential economic phenomena about the company. Second,

it is needed to identify the types of information that would be most relevant in case it

is available and it can be faithful represented. Third, it is needed to determine

whether the financial statements contain this information and they can be faithfully

represented. These steps satisfy the process to satisfy these two characteristic of

financial information.

It can be seen from the 2018 Annual Report of Cochlear Limited that the

company has satisfied these two fundamental qualitative characteristics of financial

information. Specific examples are provided below.

It needs to be mentioned that three major aspects of the financial statements

of the companies are assets, non-current assets and liabilities. It can be seen from

the 2018 Annual Report of Cochlear Limited that the company has faithfully

presented the most relevant information on these aspects in their financial

statements. For example, inventories can be considered as a crucial current asset of

Cochlear Limited which helps in determining the efficiency as well as liquidity

position of the company. For inventory, the most relevant information is its value and

the company’s policies regarding its valuation (cochlear.com 2019).

(Source: cochlear.com 2019)

It can be seen from the above that the company has disclosed the detailed

values of their inventoried that includes information on raw materials, work in

progress, finished goods and total invent toes. In addition, the company has also

presented the information on their measurement and recognition policies for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

inventories (cochlear.com 2019). This information ensures the presence of relevance

and faithful representation of this asset.

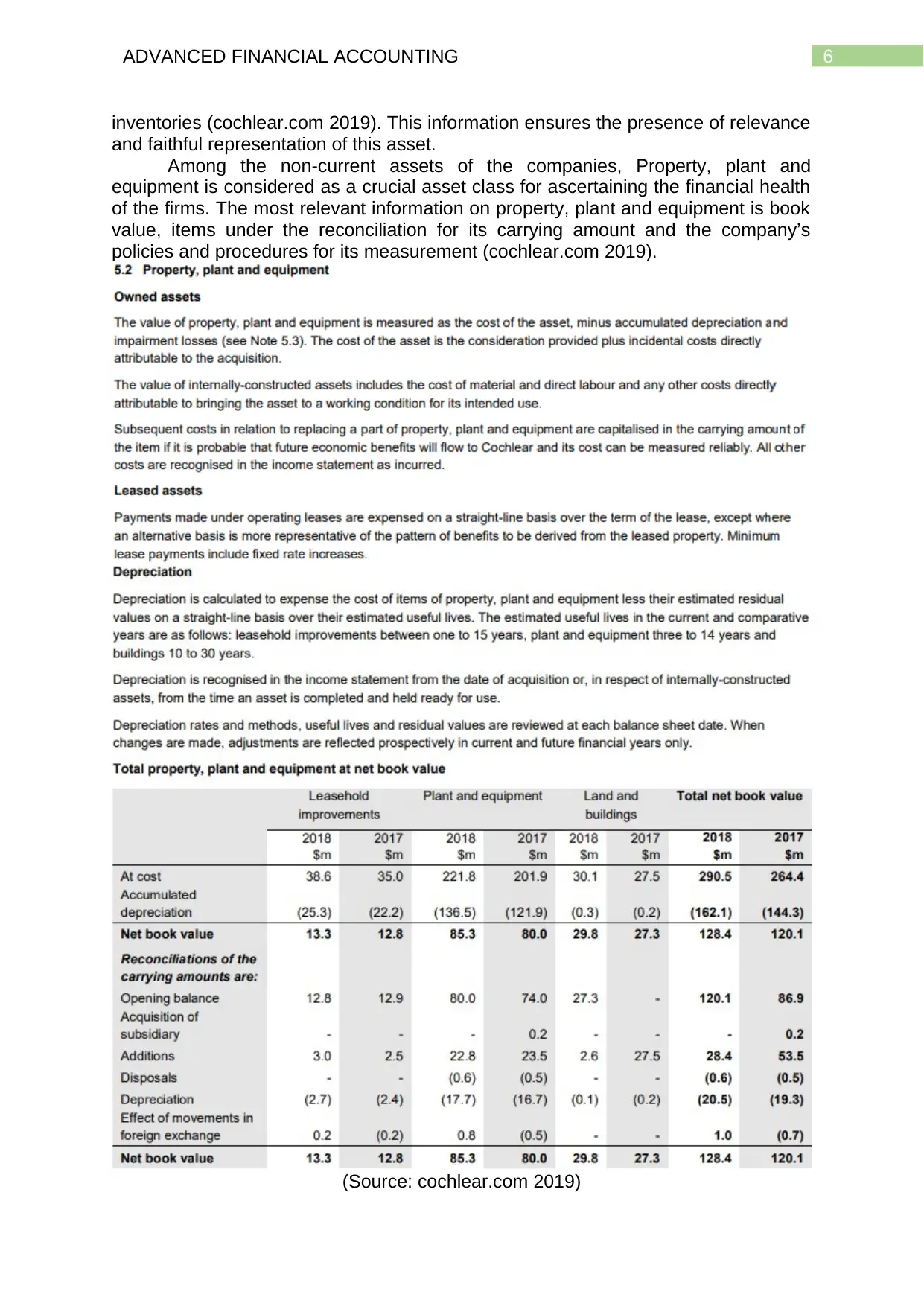

Among the non-current assets of the companies, Property, plant and

equipment is considered as a crucial asset class for ascertaining the financial health

of the firms. The most relevant information on property, plant and equipment is book

value, items under the reconciliation for its carrying amount and the company’s

policies and procedures for its measurement (cochlear.com 2019).

(Source: cochlear.com 2019)

inventories (cochlear.com 2019). This information ensures the presence of relevance

and faithful representation of this asset.

Among the non-current assets of the companies, Property, plant and

equipment is considered as a crucial asset class for ascertaining the financial health

of the firms. The most relevant information on property, plant and equipment is book

value, items under the reconciliation for its carrying amount and the company’s

policies and procedures for its measurement (cochlear.com 2019).

(Source: cochlear.com 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

It can be seen from the above that the company has disclosed all the relevant

information on this class of non-current assets in faithful manner where the

information related to net book value, reconciliation amounts of carrying value,

measurement methods, depreciation method, impairment and others (cochlear.com

2019).

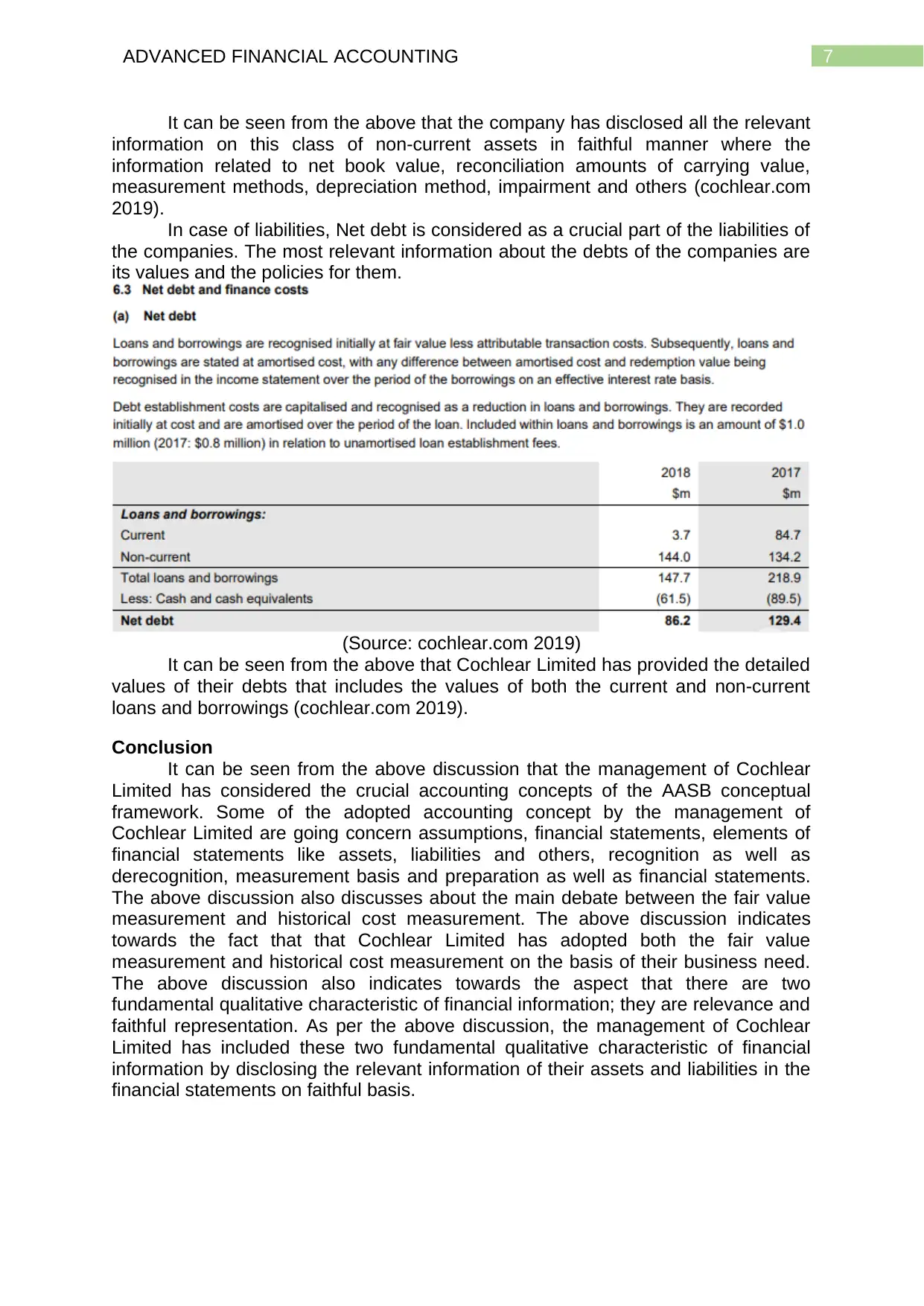

In case of liabilities, Net debt is considered as a crucial part of the liabilities of

the companies. The most relevant information about the debts of the companies are

its values and the policies for them.

(Source: cochlear.com 2019)

It can be seen from the above that Cochlear Limited has provided the detailed

values of their debts that includes the values of both the current and non-current

loans and borrowings (cochlear.com 2019).

Conclusion

It can be seen from the above discussion that the management of Cochlear

Limited has considered the crucial accounting concepts of the AASB conceptual

framework. Some of the adopted accounting concept by the management of

Cochlear Limited are going concern assumptions, financial statements, elements of

financial statements like assets, liabilities and others, recognition as well as

derecognition, measurement basis and preparation as well as financial statements.

The above discussion also discusses about the main debate between the fair value

measurement and historical cost measurement. The above discussion indicates

towards the fact that that Cochlear Limited has adopted both the fair value

measurement and historical cost measurement on the basis of their business need.

The above discussion also indicates towards the aspect that there are two

fundamental qualitative characteristic of financial information; they are relevance and

faithful representation. As per the above discussion, the management of Cochlear

Limited has included these two fundamental qualitative characteristic of financial

information by disclosing the relevant information of their assets and liabilities in the

financial statements on faithful basis.

It can be seen from the above that the company has disclosed all the relevant

information on this class of non-current assets in faithful manner where the

information related to net book value, reconciliation amounts of carrying value,

measurement methods, depreciation method, impairment and others (cochlear.com

2019).

In case of liabilities, Net debt is considered as a crucial part of the liabilities of

the companies. The most relevant information about the debts of the companies are

its values and the policies for them.

(Source: cochlear.com 2019)

It can be seen from the above that Cochlear Limited has provided the detailed

values of their debts that includes the values of both the current and non-current

loans and borrowings (cochlear.com 2019).

Conclusion

It can be seen from the above discussion that the management of Cochlear

Limited has considered the crucial accounting concepts of the AASB conceptual

framework. Some of the adopted accounting concept by the management of

Cochlear Limited are going concern assumptions, financial statements, elements of

financial statements like assets, liabilities and others, recognition as well as

derecognition, measurement basis and preparation as well as financial statements.

The above discussion also discusses about the main debate between the fair value

measurement and historical cost measurement. The above discussion indicates

towards the fact that that Cochlear Limited has adopted both the fair value

measurement and historical cost measurement on the basis of their business need.

The above discussion also indicates towards the aspect that there are two

fundamental qualitative characteristic of financial information; they are relevance and

faithful representation. As per the above discussion, the management of Cochlear

Limited has included these two fundamental qualitative characteristic of financial

information by disclosing the relevant information of their assets and liabilities in the

financial statements on faithful basis.

8ADVANCED FINANCIAL ACCOUNTING

References

Aasb.gov.au. 2019. Conceptual Framework for Financial Reporting. [online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-

15.pdf [Accessed 25 May 2019].

Barth, M.E., 2013. Measurement in financial reporting: The need for

concepts. Accounting Horizons, 28(2), pp.331-352.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the

heritage assets problem. Qualitative Research in Accounting & Management, 11(2),

pp.146-164.

Blankespoor, E., Linsmeier, T.J., Petroni, K.R. and Shakespeare, C., 2013. Fair

value accounting for financial instruments: Does it improve the association between

bank leverage and credit risk?. The Accounting Review, 88(4), pp.1143-1177.

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The

international integrated reporting framework: key issues and future research

opportunities. Journal of International Financial Management & Accounting, 25(1),

pp.90-119.

Cochlear.com. 2019. 2018 COCHLEAR LIMITED Annual Report. [online] Available

at:

https://www.cochlear.com/43d56bcc-d510-4a20-ab70-6208fa5af77e/en_annualrepor

t2018_cochlear2018annualreport_5.69mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

43d56bcc-d510-4a20-ab70-6208fa5af77e-mkRS5RK [Accessed 25 May 2019].

Cohen, S. and Karatzimas, S., 2017. Accounting information quality and decision-

usefulness of governmental financial reporting: Moving from cash to modified

cash. Meditari Accountancy Research, 25(1), pp.95-113.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature

review. International Business Management and Commerce, 2(2).

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Linsmeier, T.J., 2013. A Standard setter’s framework for selecting between fair value

and historical cost measurement attributes: a basis for discussion of “Does fair value

accounting for nonfinancial assets pass the market test?”. Review of Accounting

Studies, 18(3), pp.776-782.

Luke, B., 2016. Measuring and reporting on social performance: from numbers and

narratives to a useful reporting framework for social enterprises. Social and

Environmental Accountability Journal, 36(2), pp.103-123.

Măciucă, G., Hlaciuc, E. and Ursache, A., 2015. The role of prudence in financial

reporting: IFRS versus Directive 34. Procedia Economics and Finance, 32, pp.738-

744.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information

or confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-

591.

Ryan, C., Mack, J., Tooley, S. and Irvine, H., 2014. Do not‐for‐profits need their own

conceptual framework?. Financial Accountability & Management, 30(4), pp.383-402.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can

research add value?. Sustainability Accounting, Management and Policy

Journal, 6(1), pp.29-53.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction

to concepts, methods and uses. Cengage Learning.

References

Aasb.gov.au. 2019. Conceptual Framework for Financial Reporting. [online]

Available at: https://www.aasb.gov.au/admin/file/content105/c9/ACCED264_06-

15.pdf [Accessed 25 May 2019].

Barth, M.E., 2013. Measurement in financial reporting: The need for

concepts. Accounting Horizons, 28(2), pp.331-352.

Biondi, L. and Lapsley, I., 2014. Accounting, transparency and governance: the

heritage assets problem. Qualitative Research in Accounting & Management, 11(2),

pp.146-164.

Blankespoor, E., Linsmeier, T.J., Petroni, K.R. and Shakespeare, C., 2013. Fair

value accounting for financial instruments: Does it improve the association between

bank leverage and credit risk?. The Accounting Review, 88(4), pp.1143-1177.

Cheng, M., Green, W., Conradie, P., Konishi, N. and Romi, A., 2014. The

international integrated reporting framework: key issues and future research

opportunities. Journal of International Financial Management & Accounting, 25(1),

pp.90-119.

Cochlear.com. 2019. 2018 COCHLEAR LIMITED Annual Report. [online] Available

at:

https://www.cochlear.com/43d56bcc-d510-4a20-ab70-6208fa5af77e/en_annualrepor

t2018_cochlear2018annualreport_5.69mb.pdf?

MOD=AJPERES&CONVERT_TO=url&CACHEID=ROOTWORKSPACE-

43d56bcc-d510-4a20-ab70-6208fa5af77e-mkRS5RK [Accessed 25 May 2019].

Cohen, S. and Karatzimas, S., 2017. Accounting information quality and decision-

usefulness of governmental financial reporting: Moving from cash to modified

cash. Meditari Accountancy Research, 25(1), pp.95-113.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature

review. International Business Management and Commerce, 2(2).

Hodder, L., Hopkins, P. and Schipper, K., 2014. Fair value measurement in financial

reporting. Foundations and Trends® in Accounting, 8(3-4), pp.143-270.

Linsmeier, T.J., 2013. A Standard setter’s framework for selecting between fair value

and historical cost measurement attributes: a basis for discussion of “Does fair value

accounting for nonfinancial assets pass the market test?”. Review of Accounting

Studies, 18(3), pp.776-782.

Luke, B., 2016. Measuring and reporting on social performance: from numbers and

narratives to a useful reporting framework for social enterprises. Social and

Environmental Accountability Journal, 36(2), pp.103-123.

Măciucă, G., Hlaciuc, E. and Ursache, A., 2015. The role of prudence in financial

reporting: IFRS versus Directive 34. Procedia Economics and Finance, 32, pp.738-

744.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information

or confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-

591.

Ryan, C., Mack, J., Tooley, S. and Irvine, H., 2014. Do not‐for‐profits need their own

conceptual framework?. Financial Accountability & Management, 30(4), pp.383-402.

Simnett, R. and Huggins, A.L., 2015. Integrated reporting and assurance: where can

research add value?. Sustainability Accounting, Management and Policy

Journal, 6(1), pp.29-53.

Weil, R.L., Schipper, K. and Francis, J., 2013. Financial accounting: an introduction

to concepts, methods and uses. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.