Management Accounting Report: Costing, Planning, and Reporting

VerifiedAdded on 2020/02/12

|18

|5615

|80

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring various concepts and methods used in financial analysis and decision-making. It begins by defining management accounting and explaining the rationale behind different accounting systems, including cost accounting, job order costing, process costing, and throughput accounting. The report then delves into the methods used for preparing reports, such as financial planning, financial statement analysis, cost accounting, standard costing, marginal costing, and budgetary reports. Furthermore, it includes detailed calculations and interpretations of income statements under both absorption and marginal costing methods, highlighting the differences in profit calculation. Finally, the report discusses the merits and demerits of various planning tools used in management accounting and identifies financial problems in management accounting systems, providing a holistic view of the subject.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

MANAGEMENT ACCOUNTING.................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and the reasons for usage of various management

accounting systems......................................................................................................................3

P2: Explain the methods that are practiced for preparing reports................................................5

P3 Calculation of cost by using absorption and marginal costing methods................................7

P4 Merits and demerits of various planning tools that are used in the management accounting

......................................................................................................................................................9

P5Financial Problems in Management accounting System:......................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

MANAGEMENT ACCOUNTING.................................................................................................1

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and the reasons for usage of various management

accounting systems......................................................................................................................3

P2: Explain the methods that are practiced for preparing reports................................................5

P3 Calculation of cost by using absorption and marginal costing methods................................7

P4 Merits and demerits of various planning tools that are used in the management accounting

......................................................................................................................................................9

P5Financial Problems in Management accounting System:......................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is the domain that help business firms in identifying the areas

where firm is not performing well and need to make improvement. There are number of tools

and techniques of the management accounting that are used to measure the firm performance. In

the current report, management accounting systems are explained in detail and along with this by

using absorption and marginal costing method income statement is prepared. In middle part of

the report, different planning tools of management accounting are explained in detail. Along with

this, different method of management accounting reporting are also explained in the report. In

this way, entire research work is done in the present study.

TASK 1

P1 Explain management accounting and the reasons for usage of various management

accounting systems

Management accounting is known as provision from which varied sort of decisions are

made by the managers that are financial or non-financial in nature. The scope of management

accounting is very vast because it encompass number of areas like decision making, preparation

of plan and developing performance management system. Apart from this, management

accounting ensured that financial reporting will be better in the business firm and there will be

effective control in the business which helps managers in devising proper organization strategy.

It can be said that there are number of areas in which management accounting help managers in

making decisions that are related to business (Zimmerman and Yahya-Zadeh, 2011). In respect

to the above mentioned areas there are different tools and methods that are used by the managers

to make decisions. Some of the important tools of management accounting are variance analysis

and budgeting etc. It is very important to keep track record of the business performance. In this

regard variance analysis is used by the managers. By using variance analysis method time to time

deviation that comes in the firm performance is identified. It can be observed that performance

may be good or bad and same is identified by using variance analysis method. Budget is the one

of the important method that is used to measure performance. It is very important for the firms to

make strategic use of resources. This can be done in the business by preparing and implementing

proper plan in the business. If there will be plan then in planned manner resources can be

allocated among different business activities and by doing so cost can be minimized in the

Management accounting is the domain that help business firms in identifying the areas

where firm is not performing well and need to make improvement. There are number of tools

and techniques of the management accounting that are used to measure the firm performance. In

the current report, management accounting systems are explained in detail and along with this by

using absorption and marginal costing method income statement is prepared. In middle part of

the report, different planning tools of management accounting are explained in detail. Along with

this, different method of management accounting reporting are also explained in the report. In

this way, entire research work is done in the present study.

TASK 1

P1 Explain management accounting and the reasons for usage of various management

accounting systems

Management accounting is known as provision from which varied sort of decisions are

made by the managers that are financial or non-financial in nature. The scope of management

accounting is very vast because it encompass number of areas like decision making, preparation

of plan and developing performance management system. Apart from this, management

accounting ensured that financial reporting will be better in the business firm and there will be

effective control in the business which helps managers in devising proper organization strategy.

It can be said that there are number of areas in which management accounting help managers in

making decisions that are related to business (Zimmerman and Yahya-Zadeh, 2011). In respect

to the above mentioned areas there are different tools and methods that are used by the managers

to make decisions. Some of the important tools of management accounting are variance analysis

and budgeting etc. It is very important to keep track record of the business performance. In this

regard variance analysis is used by the managers. By using variance analysis method time to time

deviation that comes in the firm performance is identified. It can be observed that performance

may be good or bad and same is identified by using variance analysis method. Budget is the one

of the important method that is used to measure performance. It is very important for the firms to

make strategic use of resources. This can be done in the business by preparing and implementing

proper plan in the business. If there will be plan then in planned manner resources can be

allocated among different business activities and by doing so cost can be minimized in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business. Thus, it can be said that there is huge importance of the management accounting for the

managers because by using same on the multiple areas in single time period managers can focus

to improve performance

Accounting system refers to the process or procedure that is followed to record varied

items in the accounting records. There are different sort of operations that are performed by the

firms on different levels. There are some firms that are producing single product or multiple

product. Accordingly, one need to use appropriate accounting system in order to ensure that

costing will be done in the systematic way (Macintosh and Quattrone, 2010). Apart from this, in

some firms small procedure is followed to produce goods. Contrary to this, in case of some firms

long procedure is followed to manufacture product at the workplace. Thus, it can be said that in

the cases of small process costing and recording of expenses is easy task. Apart from this, in case

of long procedure costing is very different task. Thus, same management accounting system

cannot be prepared by all sort of firms. . There are different sort of management accounting

systems that are used to record expenses in the business. Requirements of these management

accounting systems are as follows. Cost accounting system: This is system that is used by the large size business firms for

computing cost of the product. Under the cost accounting system all expenses are clubbed

together to find its overall value. For example, during manufacturing process all variable

expenses elements costing is done separately and value of same is added to find out

overall value of the variable expenses in the business. Similarly, in case of fixed cost all

fixed expenses variables values are recorded separately and added to find overall value of

fixed expenses in the business. It can be said that in cost accounting system separate

classification of all sort of expenses is done and this help managers in identifying the

extent to which variable expenses increased at rapid rate in the business. Job order costing: It is a system that is used by most of business firms. This is because

in the job order costing system different product lines that are manufactured are taken in

to consideration (Ward, 2012). Moreover, there are some firms that manufacture products

according to the amount of order received from the clients. Different clients give different

specifications for product manufacturing. Thus, cost of these different orders will also be

different because specification provided by the client are not same. In such kind of cases

job order costing system is used and under this for each product line separate calculation

managers because by using same on the multiple areas in single time period managers can focus

to improve performance

Accounting system refers to the process or procedure that is followed to record varied

items in the accounting records. There are different sort of operations that are performed by the

firms on different levels. There are some firms that are producing single product or multiple

product. Accordingly, one need to use appropriate accounting system in order to ensure that

costing will be done in the systematic way (Macintosh and Quattrone, 2010). Apart from this, in

some firms small procedure is followed to produce goods. Contrary to this, in case of some firms

long procedure is followed to manufacture product at the workplace. Thus, it can be said that in

the cases of small process costing and recording of expenses is easy task. Apart from this, in case

of long procedure costing is very different task. Thus, same management accounting system

cannot be prepared by all sort of firms. . There are different sort of management accounting

systems that are used to record expenses in the business. Requirements of these management

accounting systems are as follows. Cost accounting system: This is system that is used by the large size business firms for

computing cost of the product. Under the cost accounting system all expenses are clubbed

together to find its overall value. For example, during manufacturing process all variable

expenses elements costing is done separately and value of same is added to find out

overall value of the variable expenses in the business. Similarly, in case of fixed cost all

fixed expenses variables values are recorded separately and added to find overall value of

fixed expenses in the business. It can be said that in cost accounting system separate

classification of all sort of expenses is done and this help managers in identifying the

extent to which variable expenses increased at rapid rate in the business. Job order costing: It is a system that is used by most of business firms. This is because

in the job order costing system different product lines that are manufactured are taken in

to consideration (Ward, 2012). Moreover, there are some firms that manufacture products

according to the amount of order received from the clients. Different clients give different

specifications for product manufacturing. Thus, cost of these different orders will also be

different because specification provided by the client are not same. In such kind of cases

job order costing system is used and under this for each product line separate calculation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is done. Separate employees are given responsibility to record expenses in respect to

specific product line. All fixed and variable expenses in respect to product are added to

compute overall value of the product. Process costing system: It is a system that have great significance for the managers.

Under process costing system, cost of each phase of the product manufacturing is

computed separately (Sharma, Lawrence and Lowe, 2010). Means that if there are 5

different stages of production then in that case for each of these 5 stages expenses will be

recorded separately. It can be assumed that process costing is the systematic procedure

of costing because every stage of the process is not same and cost of all of them is

different from each other. If cost of all these procedures will be added then in that case

cost of product is accurately computed. This is the reason due to which most of the

business firms prefer to follow process costing system in the business.

Throughput accounting system: Throughput accounting system is another accounting

system that is used by the most of business firms. It is also known as modern accounting

system and under this main focus is given on the cost control (Gray, Coenenberg and

Gordon, 2013). Number of ways that can be adopted to control cost are identified under

this throughput accounting system. It is the process which was developed by the Israel

businessman and is very effective due to which it become very popular among the

people.

P2: Explain the methods that are practiced for preparing reports

Meaning of Management Accounting: Management accounting is the presentation of accounting

information in order to formulate the policies to be adopted by management and assist its day to

day activities. In other words, to helps the management to perform all its function including

planning, organisation, staffing, directing and controlling.

Important Methods used for management accounting Reporting:

1. Financial Planning: Financial planning focuses on earning the profits in thorough the sale of

products and services. Iceland food Ltd. which is British supermarket Chain Company can make

its financial planning as per its goal and objective.

2. Financial Statement Analysis: The financial analysis refers the evaluation of the financial

statements of the company. (Angelakis, Theriou and Floropoulos, 2010). The analysis reveals

specific product line. All fixed and variable expenses in respect to product are added to

compute overall value of the product. Process costing system: It is a system that have great significance for the managers.

Under process costing system, cost of each phase of the product manufacturing is

computed separately (Sharma, Lawrence and Lowe, 2010). Means that if there are 5

different stages of production then in that case for each of these 5 stages expenses will be

recorded separately. It can be assumed that process costing is the systematic procedure

of costing because every stage of the process is not same and cost of all of them is

different from each other. If cost of all these procedures will be added then in that case

cost of product is accurately computed. This is the reason due to which most of the

business firms prefer to follow process costing system in the business.

Throughput accounting system: Throughput accounting system is another accounting

system that is used by the most of business firms. It is also known as modern accounting

system and under this main focus is given on the cost control (Gray, Coenenberg and

Gordon, 2013). Number of ways that can be adopted to control cost are identified under

this throughput accounting system. It is the process which was developed by the Israel

businessman and is very effective due to which it become very popular among the

people.

P2: Explain the methods that are practiced for preparing reports

Meaning of Management Accounting: Management accounting is the presentation of accounting

information in order to formulate the policies to be adopted by management and assist its day to

day activities. In other words, to helps the management to perform all its function including

planning, organisation, staffing, directing and controlling.

Important Methods used for management accounting Reporting:

1. Financial Planning: Financial planning focuses on earning the profits in thorough the sale of

products and services. Iceland food Ltd. which is British supermarket Chain Company can make

its financial planning as per its goal and objective.

2. Financial Statement Analysis: The financial analysis refers the evaluation of the financial

statements of the company. (Angelakis, Theriou and Floropoulos, 2010). The analysis reveals

the financial position of company. Income statement, balance sheet, cash flow statement are the

primary statements. So for Iceland food Ltd. they needs to regular check their financial statement

and financial results and if result found if not as per expected then they have to take important

measures.

3. Cost Accounting: Under this accounting the cost is recorded under several heads which

enable the management to compare the cost. The basic purpose of cost accounting is to

determine the cost of product or services to be sold and after determining cost, profit is added as

per need and objectives and final sales value is determined. So in keeping short cost accounting

is total cost incurred from purchase of raw material to final stocks ready to be sold in market. So

for Iceland food company Ltd. cost is important to calculate they should consider cost

accounting because they further have to sale goods and food product from manufacturing to

supplying (Burritt and Schaltegger, 2010). So these tool can prevent unnecessary wastage of raw

material to finished goods which can reduce cost of sales.

4. Standard costing: Under this method of costing, the expected cost are recorded in the books

instead of the actual costs. In a regular interval variance between the two is recorded. This

system of costing. So companies like Iceland food Ltd. maintain standard costing to periodically

review variance in actual and standard costing.

5. Marginal Costing: Marginal costing the way of costing in which only variable cost is

considered when recording the cost of product and service. The fixed cost is absent in the cost

accounting and is left to be written off by the profits in the year. So, Iceland Food Ltd. Company

maintain marginal costing to optimise marginal costing as contribution against fixed cost and

profit

6. Budgetary report: Under this technique a budget is prepared by the company. This budget

report is the forecast of expected cost to be incurred in the future.

Accounts receivable aging: In management accounting reporting accounts receivable

aging report is prepared under which track record of accounts receivable is maintained. In

the report duration for which accounts receivable given is determined and default in

receipt of payment is identified. By taking action on time cash flows are received from

accounts receivables.

primary statements. So for Iceland food Ltd. they needs to regular check their financial statement

and financial results and if result found if not as per expected then they have to take important

measures.

3. Cost Accounting: Under this accounting the cost is recorded under several heads which

enable the management to compare the cost. The basic purpose of cost accounting is to

determine the cost of product or services to be sold and after determining cost, profit is added as

per need and objectives and final sales value is determined. So in keeping short cost accounting

is total cost incurred from purchase of raw material to final stocks ready to be sold in market. So

for Iceland food company Ltd. cost is important to calculate they should consider cost

accounting because they further have to sale goods and food product from manufacturing to

supplying (Burritt and Schaltegger, 2010). So these tool can prevent unnecessary wastage of raw

material to finished goods which can reduce cost of sales.

4. Standard costing: Under this method of costing, the expected cost are recorded in the books

instead of the actual costs. In a regular interval variance between the two is recorded. This

system of costing. So companies like Iceland food Ltd. maintain standard costing to periodically

review variance in actual and standard costing.

5. Marginal Costing: Marginal costing the way of costing in which only variable cost is

considered when recording the cost of product and service. The fixed cost is absent in the cost

accounting and is left to be written off by the profits in the year. So, Iceland Food Ltd. Company

maintain marginal costing to optimise marginal costing as contribution against fixed cost and

profit

6. Budgetary report: Under this technique a budget is prepared by the company. This budget

report is the forecast of expected cost to be incurred in the future.

Accounts receivable aging: In management accounting reporting accounts receivable

aging report is prepared under which track record of accounts receivable is maintained. In

the report duration for which accounts receivable given is determined and default in

receipt of payment is identified. By taking action on time cash flows are received from

accounts receivables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost reports: Job cost report is one under which for each job under which specific

product will be produced cost is calculated and on same report is prepared. Job cost

report is one important report that is used at large scale by the firms. Managers through

job cost report get an overview of entire cost of specific job.

Inventory and manufacturing report: In inventory and manufacturing report details

related to inventory that is in stock is available. Apart from this, number of units

produced at workplace is also determined in these reports. It can be said that inventory

and manufacturing report provide a lot of details to managers.

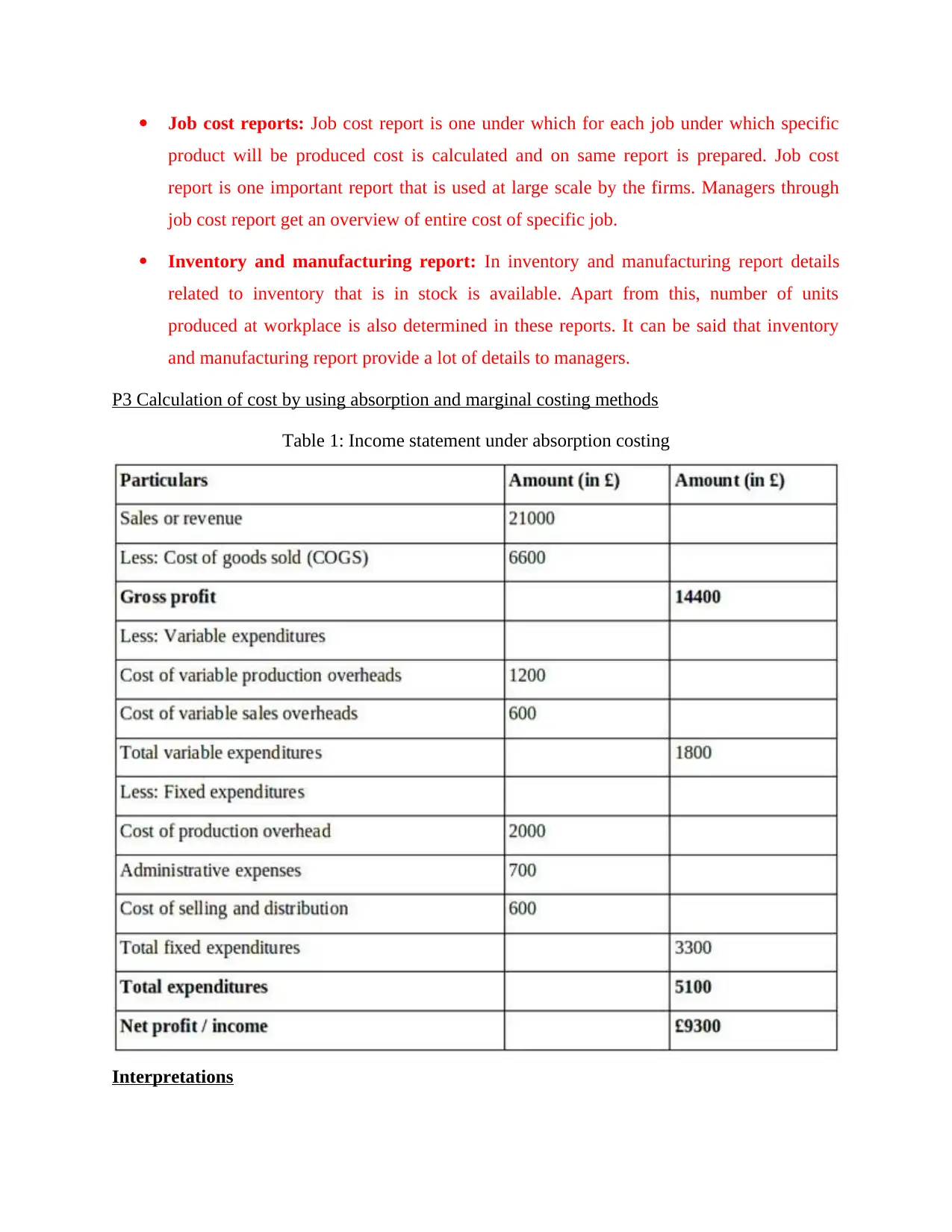

P3 Calculation of cost by using absorption and marginal costing methods

Table 1: Income statement under absorption costing

Interpretations

product will be produced cost is calculated and on same report is prepared. Job cost

report is one important report that is used at large scale by the firms. Managers through

job cost report get an overview of entire cost of specific job.

Inventory and manufacturing report: In inventory and manufacturing report details

related to inventory that is in stock is available. Apart from this, number of units

produced at workplace is also determined in these reports. It can be said that inventory

and manufacturing report provide a lot of details to managers.

P3 Calculation of cost by using absorption and marginal costing methods

Table 1: Income statement under absorption costing

Interpretations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing is the one of the most important method of costing and under this all sort

of expenses that are fixed and variable are taken in to account in order to compute overall cost of

production in the business (Guthrie, Ricceri and Dumay, 2012). It can be observed that in the

table given above varied expenses are taken in to account namely variable production and sales

overhead. Apart from this, fixed expenses are also taken in to account in order to compute net

profit in the business. It can be observed that first of all cost of goods sold is deducted from the

sales value and then from same first of all variables expenses are subtracted and then fixed

expenses are deducted to compute the net profit. In case of absorption costing method net income

is £9300. It must be noted that in the absorption costing method both sort of expenses are taken

in to account and due to this reason less amount of profit is computed in case of absorption

costing method.

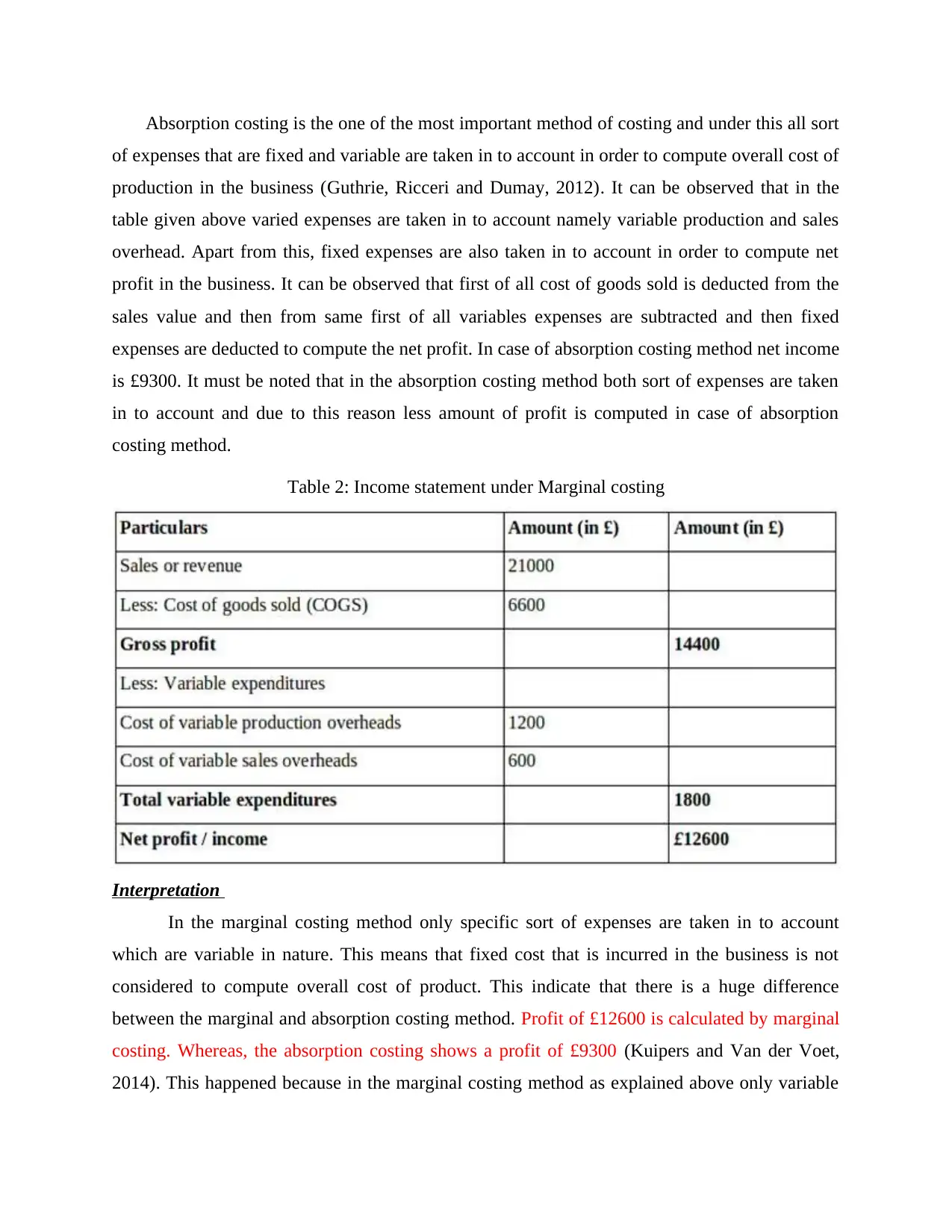

Table 2: Income statement under Marginal costing

Interpretation

In the marginal costing method only specific sort of expenses are taken in to account

which are variable in nature. This means that fixed cost that is incurred in the business is not

considered to compute overall cost of product. This indicate that there is a huge difference

between the marginal and absorption costing method. Profit of £12600 is calculated by marginal

costing. Whereas, the absorption costing shows a profit of £9300 (Kuipers and Van der Voet,

2014). This happened because in the marginal costing method as explained above only variable

of expenses that are fixed and variable are taken in to account in order to compute overall cost of

production in the business (Guthrie, Ricceri and Dumay, 2012). It can be observed that in the

table given above varied expenses are taken in to account namely variable production and sales

overhead. Apart from this, fixed expenses are also taken in to account in order to compute net

profit in the business. It can be observed that first of all cost of goods sold is deducted from the

sales value and then from same first of all variables expenses are subtracted and then fixed

expenses are deducted to compute the net profit. In case of absorption costing method net income

is £9300. It must be noted that in the absorption costing method both sort of expenses are taken

in to account and due to this reason less amount of profit is computed in case of absorption

costing method.

Table 2: Income statement under Marginal costing

Interpretation

In the marginal costing method only specific sort of expenses are taken in to account

which are variable in nature. This means that fixed cost that is incurred in the business is not

considered to compute overall cost of product. This indicate that there is a huge difference

between the marginal and absorption costing method. Profit of £12600 is calculated by marginal

costing. Whereas, the absorption costing shows a profit of £9300 (Kuipers and Van der Voet,

2014). This happened because in the marginal costing method as explained above only variable

expenses are used to calculate the profit amount. In the calculation give above fixed

expenditures, cost of production overhead, administrative expenses and cost of selling and

distribution are not included and due to this reason higher amount of profit comes in existence

which is £12600.

P4 Merits and demerits of various planning tools that are used in the management accounting

Linear programing: Linear programing is the one of the most important method that is used to

take resource allocation related decisions. Resource allocation is the one of the tough task that

managers have to perform in their day to day operations. Management accountant perform

computation and they have an idea the way in which resources like raw material can be allocated

among different products. However, situation get changed consistently and every time it is not

possible for one to make accurate prediction about resource allocation.

Advantages

The main advantage of using linear programing method is that best use of resources is

done in the business (Cadez and Guilding, 2012). Thus, it is ensured that productivity can

be maximized which lead to enhancement of revenue in the business. The other main advantage of linear programing method is that wise decisions are taken

by the managers in terms of use of resources in the business.

Disadvantages

The limitation of linear programing method is that it can be used only when there is a

specific resource that need to be used in the multiple product lines. Thus, there is limited

use of the linear programing method in terms of resource allocation. The other main disadvantage of linear programing is that it is very difficult task to

develop LPP model. In case model will be developed in wrong manner then in that case

wrong results can be produced which will ultimately lead to making wrong decisions.

Simulation: Simulation is the one of the most important method that is used to make prediction

about the extent to which cost can be increase or decrease in the business. There are varied sort

of models that can be developed in the simulation. Development of model depends on the

condition that one wants to simulate. Advantages and disadvantages of simulation are explained

below.

Advantages

expenditures, cost of production overhead, administrative expenses and cost of selling and

distribution are not included and due to this reason higher amount of profit comes in existence

which is £12600.

P4 Merits and demerits of various planning tools that are used in the management accounting

Linear programing: Linear programing is the one of the most important method that is used to

take resource allocation related decisions. Resource allocation is the one of the tough task that

managers have to perform in their day to day operations. Management accountant perform

computation and they have an idea the way in which resources like raw material can be allocated

among different products. However, situation get changed consistently and every time it is not

possible for one to make accurate prediction about resource allocation.

Advantages

The main advantage of using linear programing method is that best use of resources is

done in the business (Cadez and Guilding, 2012). Thus, it is ensured that productivity can

be maximized which lead to enhancement of revenue in the business. The other main advantage of linear programing method is that wise decisions are taken

by the managers in terms of use of resources in the business.

Disadvantages

The limitation of linear programing method is that it can be used only when there is a

specific resource that need to be used in the multiple product lines. Thus, there is limited

use of the linear programing method in terms of resource allocation. The other main disadvantage of linear programing is that it is very difficult task to

develop LPP model. In case model will be developed in wrong manner then in that case

wrong results can be produced which will ultimately lead to making wrong decisions.

Simulation: Simulation is the one of the most important method that is used to make prediction

about the extent to which cost can be increase or decrease in the business. There are varied sort

of models that can be developed in the simulation. Development of model depends on the

condition that one wants to simulate. Advantages and disadvantages of simulation are explained

below.

Advantages

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Main advantage of the simulation is that by using relevant model prediction is made

about the cost and accordingly plan is prepared to ensure that cost will remain in control

and resources will be used in best way in the business (Christ and Burritt, 2013). The other main advantage of simulation is that probable outcome of specific estimation

can be accessed. Thus, one can estimate up to any limit and can identify expected results.

Thus, it can be said that simulation model help one in doing reliable forecast for the

business.

Disadvantage

There are some limitations of the simulation method like one need to prepare a specific

model. Model building is always a very difficult task. There is no specific format that one

can follow to build a simulation model. Thus, there is a probability that one can prepare

wrong or incomplete model to handle the situation. The other main limitation is that management accountant have to estimate the probability

percentage of happening of certain event (Englund and Gerdin, 2011). For example if

management accountant is developing simulation model for costing then in that case one

have to estimate the likelihood that in future demand of raw material will enhanced. The

determined probability may be inaccurate or wrong. If same will happened then in that

case wrong results will be produced by the model and on that basis wrong planning will

be prepared by the managers.

Budget

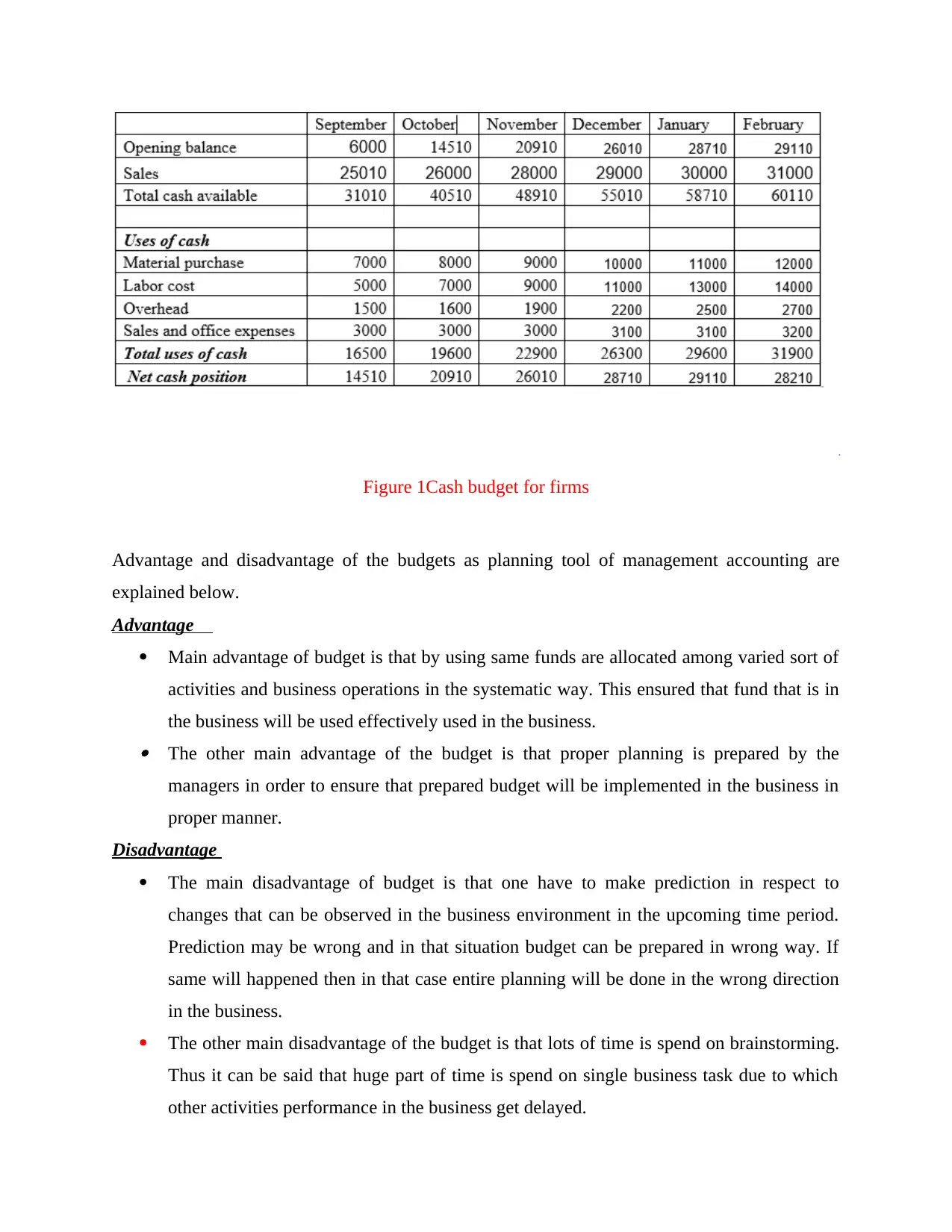

Budget is the one of the important tool that is used by the management accountants. In

the current time period business conditions are unpredictable and even business like Iceland

retail are operating at small scale performance is greatly affected. Thus, it become very important

to prepare proper plan so that effective use of fund can be ensured in the business. There are

different sort of budgets that are prepared by the managers like fixed, flexible and zero based

budgeting (Haiza Muhammad Zawawi and Hoque, 2010). Fixed budget is used by the firm and

under this values of all components of the budget remain stable and remain unchanged. Flexible

budget is totally opposite of the fixed budget and under this values of the budget keeps on

changing consistently. It depends on the firm that which sort of the budget they use in their

business. Zero based budget is another approach under which departments first of all prepare

budget and then same is considered to prepare budget for entire organization.

about the cost and accordingly plan is prepared to ensure that cost will remain in control

and resources will be used in best way in the business (Christ and Burritt, 2013). The other main advantage of simulation is that probable outcome of specific estimation

can be accessed. Thus, one can estimate up to any limit and can identify expected results.

Thus, it can be said that simulation model help one in doing reliable forecast for the

business.

Disadvantage

There are some limitations of the simulation method like one need to prepare a specific

model. Model building is always a very difficult task. There is no specific format that one

can follow to build a simulation model. Thus, there is a probability that one can prepare

wrong or incomplete model to handle the situation. The other main limitation is that management accountant have to estimate the probability

percentage of happening of certain event (Englund and Gerdin, 2011). For example if

management accountant is developing simulation model for costing then in that case one

have to estimate the likelihood that in future demand of raw material will enhanced. The

determined probability may be inaccurate or wrong. If same will happened then in that

case wrong results will be produced by the model and on that basis wrong planning will

be prepared by the managers.

Budget

Budget is the one of the important tool that is used by the management accountants. In

the current time period business conditions are unpredictable and even business like Iceland

retail are operating at small scale performance is greatly affected. Thus, it become very important

to prepare proper plan so that effective use of fund can be ensured in the business. There are

different sort of budgets that are prepared by the managers like fixed, flexible and zero based

budgeting (Haiza Muhammad Zawawi and Hoque, 2010). Fixed budget is used by the firm and

under this values of all components of the budget remain stable and remain unchanged. Flexible

budget is totally opposite of the fixed budget and under this values of the budget keeps on

changing consistently. It depends on the firm that which sort of the budget they use in their

business. Zero based budget is another approach under which departments first of all prepare

budget and then same is considered to prepare budget for entire organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 1Cash budget for firms

Advantage and disadvantage of the budgets as planning tool of management accounting are

explained below.

Advantage

Main advantage of budget is that by using same funds are allocated among varied sort of

activities and business operations in the systematic way. This ensured that fund that is in

the business will be used effectively used in the business. The other main advantage of the budget is that proper planning is prepared by the

managers in order to ensure that prepared budget will be implemented in the business in

proper manner.

Disadvantage

The main disadvantage of budget is that one have to make prediction in respect to

changes that can be observed in the business environment in the upcoming time period.

Prediction may be wrong and in that situation budget can be prepared in wrong way. If

same will happened then in that case entire planning will be done in the wrong direction

in the business.

The other main disadvantage of the budget is that lots of time is spend on brainstorming.

Thus it can be said that huge part of time is spend on single business task due to which

other activities performance in the business get delayed.

Advantage and disadvantage of the budgets as planning tool of management accounting are

explained below.

Advantage

Main advantage of budget is that by using same funds are allocated among varied sort of

activities and business operations in the systematic way. This ensured that fund that is in

the business will be used effectively used in the business. The other main advantage of the budget is that proper planning is prepared by the

managers in order to ensure that prepared budget will be implemented in the business in

proper manner.

Disadvantage

The main disadvantage of budget is that one have to make prediction in respect to

changes that can be observed in the business environment in the upcoming time period.

Prediction may be wrong and in that situation budget can be prepared in wrong way. If

same will happened then in that case entire planning will be done in the wrong direction

in the business.

The other main disadvantage of the budget is that lots of time is spend on brainstorming.

Thus it can be said that huge part of time is spend on single business task due to which

other activities performance in the business get delayed.

There are many alternative methods of budgeting apart from cash budget. Some of these

methods are zero based budget and capital expenditure budget. It depend on which that which of

these budget firm prepared. Usually, budget preparation depends on firm requirements.

There are some behavioral implications of budget as it can be noted that it is a statement

under which estimations are made. These estimations may be different from reality and in that

case firm may need to change its strategy. In case strategy does not change company may face

heavy loss in its business.

Statistical technique: Statistical techniques are the new methods that are used to planning in

respect to management accounting (Lee, 2011). It must be noted that in the management

accounting huge sort of data is gathered. Such data is analyzed by using statistical methods like

regression and one way ANNOVA etc. Some advantages and disadvantages of the statistical

method are explained below.

Advantages The main merit of statistical method is that it reflects the extent to which change comes in

the one variable due to change in another variable. One can identify the relationship

between variable expenses and production. The percentage change that comes in the

dependent variable like variable expense with production of each unit of item can be

identified by using regression model. These tools and methods help one in evaluating

variables in many ways. Thus, better decisions can be made by the managers by using

statistical tools.

Disadvantages Main limitation of the statistical tools is that there are some assumptions of the statistical

methods and on fulfillment of that conditions specific tool can be applied on the data set

(Li and et.al., 2012). If one have wrong knowledge of the statistics then in that case it

may choose wrong method and can take decisions on the basis of unreliable or wrong

output.

Pricing strategies

There are different sort of pricing strategies that are available to the business firms. These

pricing approaches have merits and demerits both. It depend on firm that which of these options

it think is better. Competitor pricing strategy is one under which by considering competitor price,

methods are zero based budget and capital expenditure budget. It depend on which that which of

these budget firm prepared. Usually, budget preparation depends on firm requirements.

There are some behavioral implications of budget as it can be noted that it is a statement

under which estimations are made. These estimations may be different from reality and in that

case firm may need to change its strategy. In case strategy does not change company may face

heavy loss in its business.

Statistical technique: Statistical techniques are the new methods that are used to planning in

respect to management accounting (Lee, 2011). It must be noted that in the management

accounting huge sort of data is gathered. Such data is analyzed by using statistical methods like

regression and one way ANNOVA etc. Some advantages and disadvantages of the statistical

method are explained below.

Advantages The main merit of statistical method is that it reflects the extent to which change comes in

the one variable due to change in another variable. One can identify the relationship

between variable expenses and production. The percentage change that comes in the

dependent variable like variable expense with production of each unit of item can be

identified by using regression model. These tools and methods help one in evaluating

variables in many ways. Thus, better decisions can be made by the managers by using

statistical tools.

Disadvantages Main limitation of the statistical tools is that there are some assumptions of the statistical

methods and on fulfillment of that conditions specific tool can be applied on the data set

(Li and et.al., 2012). If one have wrong knowledge of the statistics then in that case it

may choose wrong method and can take decisions on the basis of unreliable or wrong

output.

Pricing strategies

There are different sort of pricing strategies that are available to the business firms. These

pricing approaches have merits and demerits both. It depend on firm that which of these options

it think is better. Competitor pricing strategy is one under which by considering competitor price,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.