Management Accounting Report: Techniques and Analysis for Unicorn Ltd

VerifiedAdded on 2020/01/16

|17

|5577

|160

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Unicorn Limited, a small-scale retailer. It explores various aspects, including the evaluation of management accounting needs, different reporting methods, and the benefits of various management accounting systems like traditional, lean, and throughput accounting. The report delves into specific techniques for developing income statements, such as marginal and absorption costing, and analyzes budgetary planning advantages and disadvantages. Furthermore, it examines the integration of accounting systems within an organization and compares the adoption of management accounting to address financial problems, offering insights into how management accounting can contribute to financial success. The report covers topics from cost accounting to inventory management and provides a detailed overview of financial planning and analysis within the context of a real-world business.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..................................................................................................................2

TASK 1............................................................................................................................................3

P1 Evaluation and Analysis of needs of management accounting........................................3

P2 Different methods used for management accounting reporting........................................5

M1 Benefits of different management accounting system.....................................................6

D1 Integration of systems and accounting in process of organization...................................7

TASK 2............................................................................................................................................7

P3 Analysis of techniques for development of income statement..........................................7

M2 Applying a range of management accounting techniques...............................................9

D2 Development of report and interpretation of data..........................................................10

TASK 3..........................................................................................................................................10

P4 Explanation of the advantages and disadvantages of the varied kinds of budgetary planning

..............................................................................................................................................10

M3 Analysis of the usage of varied planning tools and implementation for budget forecasting

..............................................................................................................................................12

D3 Evaluating the tools of planning for solution of financial problems..............................13

TASK 4..........................................................................................................................................13

P5 Compare the adoption of management accounting system to respond financial problems13

M4 Responding financial problem through management accounting to bring success.......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION..................................................................................................................2

TASK 1............................................................................................................................................3

P1 Evaluation and Analysis of needs of management accounting........................................3

P2 Different methods used for management accounting reporting........................................5

M1 Benefits of different management accounting system.....................................................6

D1 Integration of systems and accounting in process of organization...................................7

TASK 2............................................................................................................................................7

P3 Analysis of techniques for development of income statement..........................................7

M2 Applying a range of management accounting techniques...............................................9

D2 Development of report and interpretation of data..........................................................10

TASK 3..........................................................................................................................................10

P4 Explanation of the advantages and disadvantages of the varied kinds of budgetary planning

..............................................................................................................................................10

M3 Analysis of the usage of varied planning tools and implementation for budget forecasting

..............................................................................................................................................12

D3 Evaluating the tools of planning for solution of financial problems..............................13

TASK 4..........................................................................................................................................13

P5 Compare the adoption of management accounting system to respond financial problems13

M4 Responding financial problem through management accounting to bring success.......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

2

INTRODUCTION

Management accounting is considered as a significant process of analysing of data and

recording enteries of financial statements and reflects the reports which are used for

understanding the growth and improvement of organization. Thus, management accounting is

plays a key role within firm and therefore, it helps management of firm to make effective

decision making through using information provided in accounts. Currently businesses aims to

track their performance and thus goes beyond cost based information of historic general ledge

system provided by traditional financial accounting information (Christ and et.al., 2017).

Through creating a good management accounting it helps in involving the responsibility to

manage wide variety of critical management accounting information through using management

accounting system and management accounting techniques i.e. analysis of profitability through

volume of cost, manufacturing cost absorption and charging cost of variables in order to make

effective decision making.

Further, management accounting is also prepared by the businesses in regard to keep

monthly or weekly reports of businesses regarding their financial performance. Hence,

management accountant of any firm obtains the responsibility to follow all the rules and

regulations as per the accounting standard so that they do not hinder the system. Carrying out

management accounting within business it helps in obtaining information related to business and

then take managerial decisions upon them (Deegan, 2013). Present study has been undertaken

upon small business enterprise i.e. Unicorn Limited which is a small scale retailer. It employs

less than 50 workers and also it has annual net turnover not exceeding Pound 500,000. Here,

different tools are being used for carrying out management accounting reporting and thus

advantages and disadvantages of different planning tools which could be utilized for budgetary

control.

TASK 1

P1 Evaluation and Analysis of needs of management accounting

It is the process of preparing and analysing the statements as well as reports related to

financial information and thus later could be used by decision makers of firm. It provides useful

data or information related to finance so that managers could use the same in regard to carry out

regular short term decisions (DRURY, 2013). Management accounting is different concept than

3

Management accounting is considered as a significant process of analysing of data and

recording enteries of financial statements and reflects the reports which are used for

understanding the growth and improvement of organization. Thus, management accounting is

plays a key role within firm and therefore, it helps management of firm to make effective

decision making through using information provided in accounts. Currently businesses aims to

track their performance and thus goes beyond cost based information of historic general ledge

system provided by traditional financial accounting information (Christ and et.al., 2017).

Through creating a good management accounting it helps in involving the responsibility to

manage wide variety of critical management accounting information through using management

accounting system and management accounting techniques i.e. analysis of profitability through

volume of cost, manufacturing cost absorption and charging cost of variables in order to make

effective decision making.

Further, management accounting is also prepared by the businesses in regard to keep

monthly or weekly reports of businesses regarding their financial performance. Hence,

management accountant of any firm obtains the responsibility to follow all the rules and

regulations as per the accounting standard so that they do not hinder the system. Carrying out

management accounting within business it helps in obtaining information related to business and

then take managerial decisions upon them (Deegan, 2013). Present study has been undertaken

upon small business enterprise i.e. Unicorn Limited which is a small scale retailer. It employs

less than 50 workers and also it has annual net turnover not exceeding Pound 500,000. Here,

different tools are being used for carrying out management accounting reporting and thus

advantages and disadvantages of different planning tools which could be utilized for budgetary

control.

TASK 1

P1 Evaluation and Analysis of needs of management accounting

It is the process of preparing and analysing the statements as well as reports related to

financial information and thus later could be used by decision makers of firm. It provides useful

data or information related to finance so that managers could use the same in regard to carry out

regular short term decisions (DRURY, 2013). Management accounting is different concept than

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial accounting in which managers generates monthly or weekly reports in relation to

Unicorn Limited. Preparing such report by the management accountant involves the information

in relation to cash available, sales revenue generated, amount of order in hand, accounts payable,

outstanding debts, inventory and raw material. Moreover, it also involves trend chart, variance

and other statistics. Also, it has been stated that financial and accounting of cost are considered

as the basis of management accounting. There are various kinds of systems of management

accounting are mentioned below: Traditional method - Such method has been used by different accountants and thus

considered as the traditional approach which is used by businesses. In order to carry out

calculation it involves direct cost, labour and overhead. Further, carrying out the

traditional cost accounting it involves cost driver which results in occurring of cost such

as direct material, labour and machine hours (Fullerton, Kennedy and Widener, 2013). Lean accounting- Further, it is another type of management accounting and thus

considered as new concept which is generally being utilized for different alterations

which are being made within accounting, controlling and carrying out different

management procedure and thus measuring business carried out by Unicorn Ltd.

However, accountant here requires focusing upon lean manufacturing and carrying out

lean thinking to obtain better information and outcomes (Zimmerman and Yahya-Zadeh,

2011). Throughput accounting- In such type of accounting it comprises determination of

constraints in the system of production within firm. However, such concept is based upon

the principle and approach of simplified management system. Therefore, in regard to

improve profitability, Unicorn uses such system and also helps them to make effective

decision making (Marginal and absorption costing. 2016).

Transfer pricing- Further, it involves the price within movement of products or services

is being done and thus helps Unicorn to calculate cost as well as expenses in transferring

of products or services (Christ and et.al., 2017).

Following are the different examples linked with management accounting system that are

described underneath-

Cost accounting system- It is considered as the tool that helps in utilising the business

towards making crucial estimation that involves cost of products in regard to identify the

4

Unicorn Limited. Preparing such report by the management accountant involves the information

in relation to cash available, sales revenue generated, amount of order in hand, accounts payable,

outstanding debts, inventory and raw material. Moreover, it also involves trend chart, variance

and other statistics. Also, it has been stated that financial and accounting of cost are considered

as the basis of management accounting. There are various kinds of systems of management

accounting are mentioned below: Traditional method - Such method has been used by different accountants and thus

considered as the traditional approach which is used by businesses. In order to carry out

calculation it involves direct cost, labour and overhead. Further, carrying out the

traditional cost accounting it involves cost driver which results in occurring of cost such

as direct material, labour and machine hours (Fullerton, Kennedy and Widener, 2013). Lean accounting- Further, it is another type of management accounting and thus

considered as new concept which is generally being utilized for different alterations

which are being made within accounting, controlling and carrying out different

management procedure and thus measuring business carried out by Unicorn Ltd.

However, accountant here requires focusing upon lean manufacturing and carrying out

lean thinking to obtain better information and outcomes (Zimmerman and Yahya-Zadeh,

2011). Throughput accounting- In such type of accounting it comprises determination of

constraints in the system of production within firm. However, such concept is based upon

the principle and approach of simplified management system. Therefore, in regard to

improve profitability, Unicorn uses such system and also helps them to make effective

decision making (Marginal and absorption costing. 2016).

Transfer pricing- Further, it involves the price within movement of products or services

is being done and thus helps Unicorn to calculate cost as well as expenses in transferring

of products or services (Christ and et.al., 2017).

Following are the different examples linked with management accounting system that are

described underneath-

Cost accounting system- It is considered as the tool that helps in utilising the business

towards making crucial estimation that involves cost of products in regard to identify the

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability, inventory and product sold etc. However, estimating the appropriate product

cost is stated as significant value for obtaining profitable business functions.

Job costing system- Further, such system helps in comprising assigning the

manufacturing costs to the individual product or batches of products. However, it is being

used at the time of manufacturing products in appropriate manner that varies from one

another.

Batch costing system- It is another method that is cost related method and thus helps in

developing the product which is computed in terms of batch instead of individual item

that involves comparison of costs of several sized batches which is produced within

different conditions.

Inventory management system- It helps in carrying out supervision of non capitalized

asset and stock items. However, it is considered as the component of supply chain

management that helps in supervising the inflow of products from manufacturers to

warehouses and thus end to sales places.

Price optimization system- Such method is used in regard to calculate the mathematical

analysis by business in regard to determine the price of products so that customers could

be attracted towards firm.

P2 Different methods used for management accounting reporting

Following are the different methods which is being used for management accounting

reporting such as-

Financial planning- Carrying out financial planning helps in offering direction to carry

out business activity. However, if business possess sound financial planning it helps them

to enhance its profit condition (Deegan, 2013).

Financial statement analysis- Further, Unicorn Ltd carries out financial statement

analysis and thus involves profit and loss account and balance sheet so that business can

enhance its financial position in market. However, such analysis could be done on yearly

basis (DRURY, 2013).

Cost accounting- Such method is being used in regard to carry out management

accounting reporting and thus obtain information related to cost. Also, it helps in

revealing the information related to cost of products, process, department and obtains the

best information. It assesses that the actual cost borne by company is being compared

5

cost is stated as significant value for obtaining profitable business functions.

Job costing system- Further, such system helps in comprising assigning the

manufacturing costs to the individual product or batches of products. However, it is being

used at the time of manufacturing products in appropriate manner that varies from one

another.

Batch costing system- It is another method that is cost related method and thus helps in

developing the product which is computed in terms of batch instead of individual item

that involves comparison of costs of several sized batches which is produced within

different conditions.

Inventory management system- It helps in carrying out supervision of non capitalized

asset and stock items. However, it is considered as the component of supply chain

management that helps in supervising the inflow of products from manufacturers to

warehouses and thus end to sales places.

Price optimization system- Such method is used in regard to calculate the mathematical

analysis by business in regard to determine the price of products so that customers could

be attracted towards firm.

P2 Different methods used for management accounting reporting

Following are the different methods which is being used for management accounting

reporting such as-

Financial planning- Carrying out financial planning helps in offering direction to carry

out business activity. However, if business possess sound financial planning it helps them

to enhance its profit condition (Deegan, 2013).

Financial statement analysis- Further, Unicorn Ltd carries out financial statement

analysis and thus involves profit and loss account and balance sheet so that business can

enhance its financial position in market. However, such analysis could be done on yearly

basis (DRURY, 2013).

Cost accounting- Such method is being used in regard to carry out management

accounting reporting and thus obtain information related to cost. Also, it helps in

revealing the information related to cost of products, process, department and obtains the

best information. It assesses that the actual cost borne by company is being compared

5

with the budgeted information. Later, deviation is being identified in regard to improve

business performance (Fullerton, Kennedy and Widener, 2013).

It involves different examples that are related with management account reports which

are as follows-

Job cost reports- It is one of the effective accounting report that help in tracking the costs

and revenues with the help of hob and help in standardizing reporting related to

profitability in regard to job.

Sales reports- Such report helps in comprising data regarding all the sales that is being

made by firm considering the particular period.

Accounts receivables reports- It is considered as the money that the business possess the

right to receive as it offers clients with appropriate products or services.

Inventory management reports- Such report helps in comprising detail regarding the

available stock with the firm, the amount sold and requirement of stock for firm.

M1 Benefits of different management accounting system

Management accounting is the new concept which is also known as managerial accounting.

It determines various aspects that beneficial for assess cost and outcomes of the company at

workplace. Business owner of Unicorn Limited use management accounting system due to

following benefits:

Reduce expenses: In order to perform functions and operations, management accounting

system creates various benefits. In this aspect, the company review the cost of economic

resources and other operations of company. It assists to create better understand running

cost within the company (Banerjee and Das, 2017).

Cash flow enhancement: Budget is considered as major part which is determined under

systems of accounting. Business owner of the relevant business entity use it for future

business expenditure. Budget is based on historical financial information (Bhimani and

et.al., 2013).

Increase financial returns: Owner of the company Unicorn Limited also uses

management accounting to assess financial returns. Management accounts prepare

financial statement to forecast relating to consumer demand and potential sales which

creates impact on consumer price changes (Chenhall and Moers, 2015).

6

business performance (Fullerton, Kennedy and Widener, 2013).

It involves different examples that are related with management account reports which

are as follows-

Job cost reports- It is one of the effective accounting report that help in tracking the costs

and revenues with the help of hob and help in standardizing reporting related to

profitability in regard to job.

Sales reports- Such report helps in comprising data regarding all the sales that is being

made by firm considering the particular period.

Accounts receivables reports- It is considered as the money that the business possess the

right to receive as it offers clients with appropriate products or services.

Inventory management reports- Such report helps in comprising detail regarding the

available stock with the firm, the amount sold and requirement of stock for firm.

M1 Benefits of different management accounting system

Management accounting is the new concept which is also known as managerial accounting.

It determines various aspects that beneficial for assess cost and outcomes of the company at

workplace. Business owner of Unicorn Limited use management accounting system due to

following benefits:

Reduce expenses: In order to perform functions and operations, management accounting

system creates various benefits. In this aspect, the company review the cost of economic

resources and other operations of company. It assists to create better understand running

cost within the company (Banerjee and Das, 2017).

Cash flow enhancement: Budget is considered as major part which is determined under

systems of accounting. Business owner of the relevant business entity use it for future

business expenditure. Budget is based on historical financial information (Bhimani and

et.al., 2013).

Increase financial returns: Owner of the company Unicorn Limited also uses

management accounting to assess financial returns. Management accounts prepare

financial statement to forecast relating to consumer demand and potential sales which

creates impact on consumer price changes (Chenhall and Moers, 2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D1 Integration of systems and accounting in process of organization.

Management accounting is related with value creators that assist to make effective results

and performances at workplace. It is also considered with management accounting that strategic

planning of the company. As per the view of (Christ and et.al., 2017) management accounting is

based on performance based actions. In this aspect, management accounting looks with matter

related to the performances' enhancement. It assists to make excellent with profit margin and

enhance profitability for achieve competitive outcomes. Risk managing also takes at workplace

to measure risk decisions. On the other hand (Hecht, 2016) stated that management accounting is

concerned with planning and output that assist to make operational status. It assists to keep

records for ascertain progress and outcomes of Unicorn Limited. They possess that management

accounting is delivering effective functions and operations that requires for creates various

advantages. As results, objectives and goals can be maintained at workplace easily through

determines effective results and performances.

TASK 2

P3 Analysis of techniques for development of income statement

Interpretation of cost price is recognised as the crucial part which helps in carrying out

managerial accounting practices. Thus, it is carried out because of inaccurate cost identified

within business and thus it affects the business in a negative way. However, management of

Unicorn is getting affected in terms of making pricing decisions so that ultimately customer

dissatisfaction would be raised (Horngren and et.al., 2010). Following are different techniques

which could be used in regard to carry out cost determination i.e. marginal costing, absorption

costing etc.

Marginal costing- Such method is being used in regard to charge variable cost to per unit

of products manufactured by Unicorn and thus it is essential for them to compute the total

cost and then fixed it so that they could be charged in full against the contribution to

reflect the net return. Also, total fixed cost needs to be considered as periodical cost and

do not allocate the same to find total production (Kaplan and Atkinson, 2015). However,

it is considered as of great significance in regard to determine the total expenses which is

faced by Unicorn and incur additional unit of production.

Advantages-

7

Management accounting is related with value creators that assist to make effective results

and performances at workplace. It is also considered with management accounting that strategic

planning of the company. As per the view of (Christ and et.al., 2017) management accounting is

based on performance based actions. In this aspect, management accounting looks with matter

related to the performances' enhancement. It assists to make excellent with profit margin and

enhance profitability for achieve competitive outcomes. Risk managing also takes at workplace

to measure risk decisions. On the other hand (Hecht, 2016) stated that management accounting is

concerned with planning and output that assist to make operational status. It assists to keep

records for ascertain progress and outcomes of Unicorn Limited. They possess that management

accounting is delivering effective functions and operations that requires for creates various

advantages. As results, objectives and goals can be maintained at workplace easily through

determines effective results and performances.

TASK 2

P3 Analysis of techniques for development of income statement

Interpretation of cost price is recognised as the crucial part which helps in carrying out

managerial accounting practices. Thus, it is carried out because of inaccurate cost identified

within business and thus it affects the business in a negative way. However, management of

Unicorn is getting affected in terms of making pricing decisions so that ultimately customer

dissatisfaction would be raised (Horngren and et.al., 2010). Following are different techniques

which could be used in regard to carry out cost determination i.e. marginal costing, absorption

costing etc.

Marginal costing- Such method is being used in regard to charge variable cost to per unit

of products manufactured by Unicorn and thus it is essential for them to compute the total

cost and then fixed it so that they could be charged in full against the contribution to

reflect the net return. Also, total fixed cost needs to be considered as periodical cost and

do not allocate the same to find total production (Kaplan and Atkinson, 2015). However,

it is considered as of great significance in regard to determine the total expenses which is

faced by Unicorn and incur additional unit of production.

Advantages-

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing is being carried out in terms of valuing inventory which is considering

through carrying out closing inventory items.

It also helps in making required adjustments for under or over absorption of overheads to

control cost of products (Quattrone, 2016).

Moreover, it is the best way through which firm is required to determine the total cost

and profitable upon a specific job.

Demerits

Marginal costing is not useful in making pricing decisions within firm.

Also, it is not helpful in controlling the cost of products produced by firm.

Difference between marginal and absorption costing

Marginal costing method helps in valuing inventory at variable production cost while

absorption cost measures helps in inventory value at full costing. Thus, carrying out

under variable costing inventory valuation is understated (Saladrigues and Tena, 2017).

Further, with high inventory absorption cost also helps in delivering large return while at

a low rate of selling inventory, it provides less revenue to marginal costing.

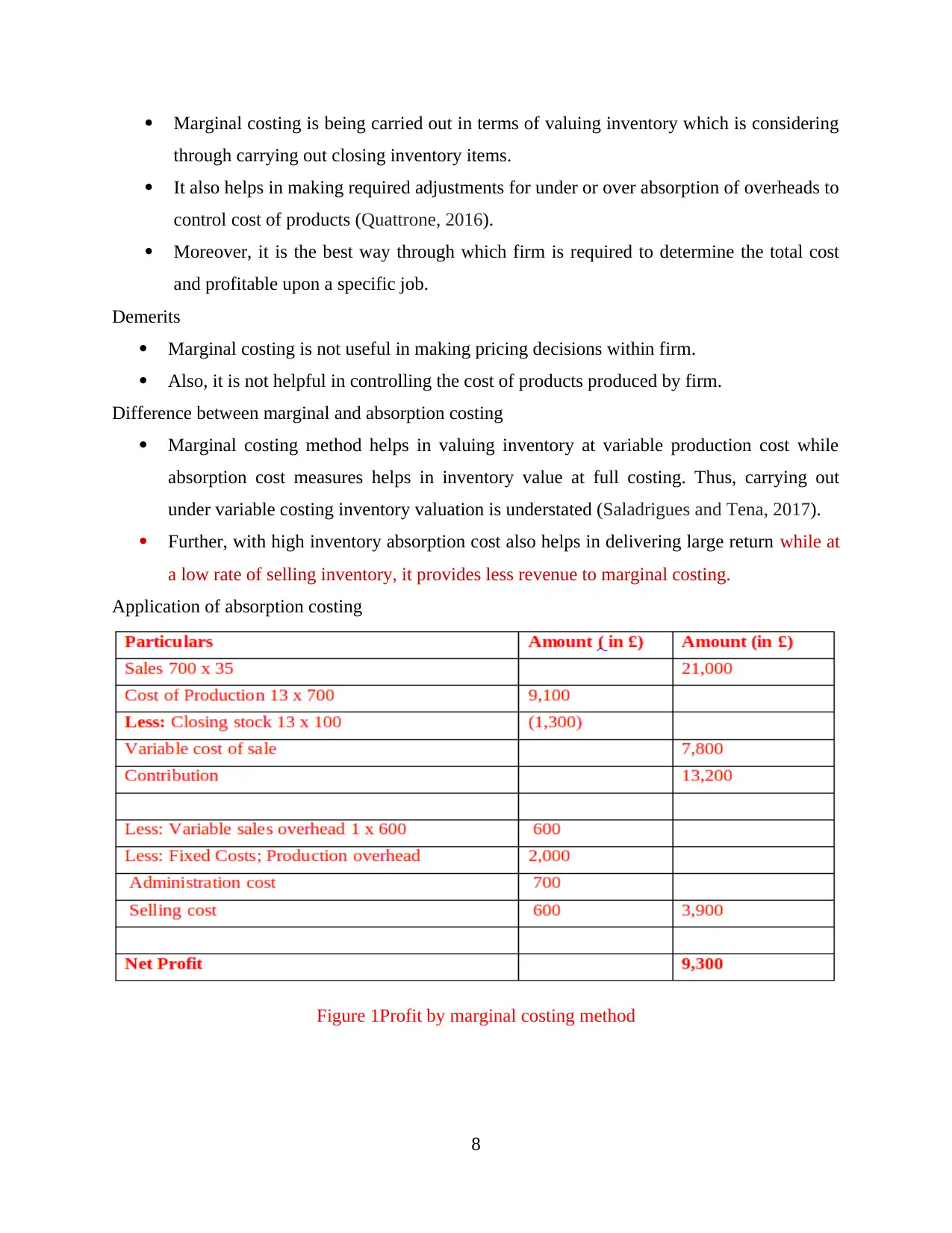

Application of absorption costing

Figure 1Profit by marginal costing method

8

through carrying out closing inventory items.

It also helps in making required adjustments for under or over absorption of overheads to

control cost of products (Quattrone, 2016).

Moreover, it is the best way through which firm is required to determine the total cost

and profitable upon a specific job.

Demerits

Marginal costing is not useful in making pricing decisions within firm.

Also, it is not helpful in controlling the cost of products produced by firm.

Difference between marginal and absorption costing

Marginal costing method helps in valuing inventory at variable production cost while

absorption cost measures helps in inventory value at full costing. Thus, carrying out

under variable costing inventory valuation is understated (Saladrigues and Tena, 2017).

Further, with high inventory absorption cost also helps in delivering large return while at

a low rate of selling inventory, it provides less revenue to marginal costing.

Application of absorption costing

Figure 1Profit by marginal costing method

8

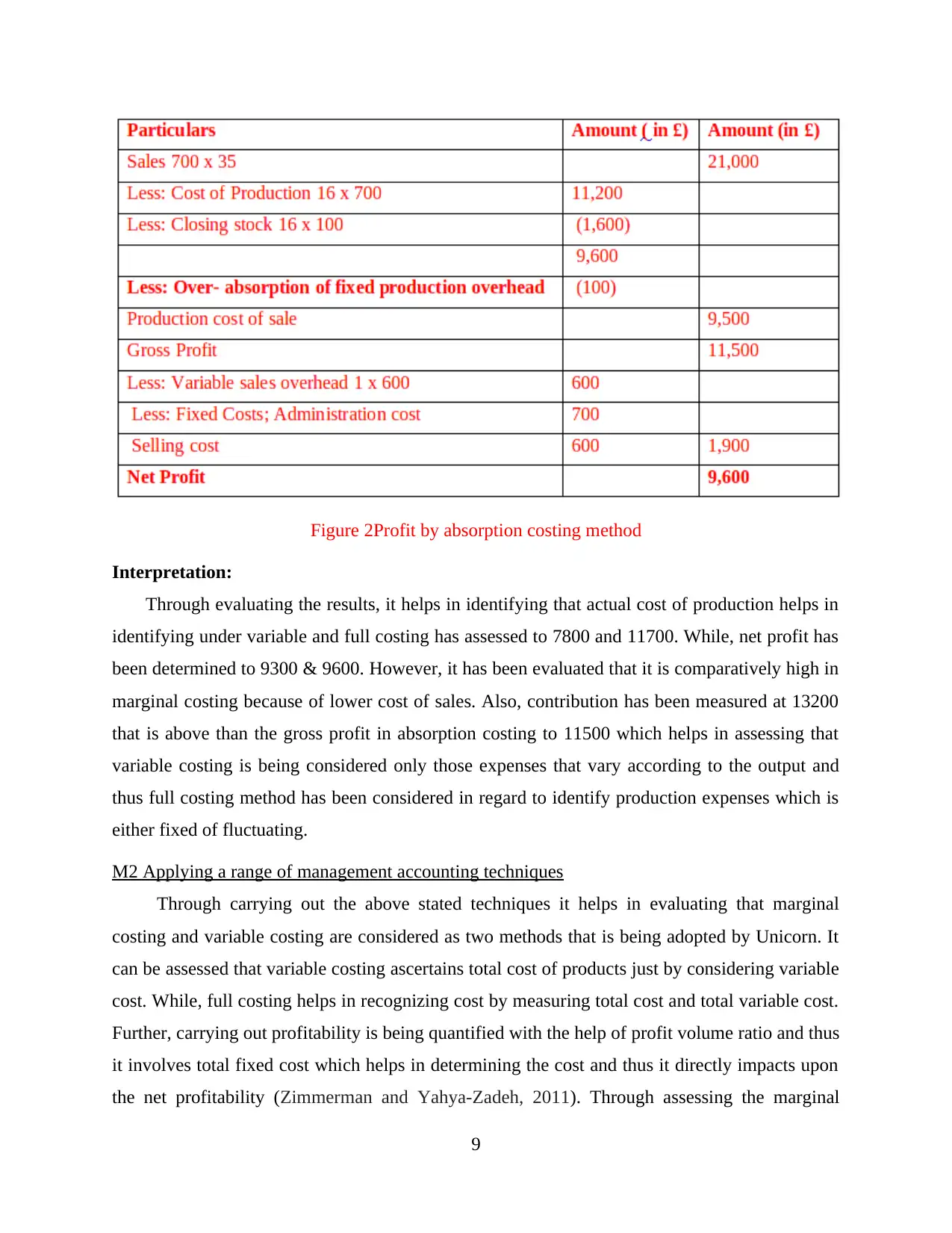

Figure 2Profit by absorption costing method

Interpretation:

Through evaluating the results, it helps in identifying that actual cost of production helps in

identifying under variable and full costing has assessed to 7800 and 11700. While, net profit has

been determined to 9300 & 9600. However, it has been evaluated that it is comparatively high in

marginal costing because of lower cost of sales. Also, contribution has been measured at 13200

that is above than the gross profit in absorption costing to 11500 which helps in assessing that

variable costing is being considered only those expenses that vary according to the output and

thus full costing method has been considered in regard to identify production expenses which is

either fixed of fluctuating.

M2 Applying a range of management accounting techniques

Through carrying out the above stated techniques it helps in evaluating that marginal

costing and variable costing are considered as two methods that is being adopted by Unicorn. It

can be assessed that variable costing ascertains total cost of products just by considering variable

cost. While, full costing helps in recognizing cost by measuring total cost and total variable cost.

Further, carrying out profitability is being quantified with the help of profit volume ratio and thus

it involves total fixed cost which helps in determining the cost and thus it directly impacts upon

the net profitability (Zimmerman and Yahya-Zadeh, 2011). Through assessing the marginal

9

Interpretation:

Through evaluating the results, it helps in identifying that actual cost of production helps in

identifying under variable and full costing has assessed to 7800 and 11700. While, net profit has

been determined to 9300 & 9600. However, it has been evaluated that it is comparatively high in

marginal costing because of lower cost of sales. Also, contribution has been measured at 13200

that is above than the gross profit in absorption costing to 11500 which helps in assessing that

variable costing is being considered only those expenses that vary according to the output and

thus full costing method has been considered in regard to identify production expenses which is

either fixed of fluctuating.

M2 Applying a range of management accounting techniques

Through carrying out the above stated techniques it helps in evaluating that marginal

costing and variable costing are considered as two methods that is being adopted by Unicorn. It

can be assessed that variable costing ascertains total cost of products just by considering variable

cost. While, full costing helps in recognizing cost by measuring total cost and total variable cost.

Further, carrying out profitability is being quantified with the help of profit volume ratio and thus

it involves total fixed cost which helps in determining the cost and thus it directly impacts upon

the net profitability (Zimmerman and Yahya-Zadeh, 2011). Through assessing the marginal

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

costing it helps in measuring profit through contributing per unit and thus identifying the return

in terms of net profit of per unit. Hence, it can be evaluated that out of these techniques marginal

costing is considered as suitable because it helps in measuring contribution and overall net profit

and thus managers need to carry out short term managerial planning.

D2 Development of report and interpretation of data

To: Unicorn’s Board of directors

Date: 1st April 2017

Subject: Determination of cost.

It can be evaluated that after calculating cost through using both the techniques it can be stated

that Unicorn helps in making marginal costing, actual profitability is quantified up to a high level

i.e. 11300. While, full costing method is valued at 9585.71 which is being considered as

comparatively low. Further, in the first it has been identified that expenses have been carried out

that they vary as per the changes in production or output within Unicorn. Moreover, it has been

assessed that both fixed and fluctuating cost of production has been evaluated and thus it helps in

identifying desired results (Gullifer and Payne, 2015). Hence, it results in identifying that low

profitability has been identified. Because of this closing inventory has been valued which is

reported very differently and under both this methods variable costing method has been valued

i.e. 1300. While, full costing has been evaluated that it is 1585.71 which is high. However, main

reason behind this is that full costing method has been taken into consideration and thus fixed

production overheads i.e. 2000 has not been involved within the cost of production and thus

identify that marginal cost results in computing manufacturing cost of products at Unicorn i.e.

11100 and 7800. While, less cost is the main reason for high contribution i.e. 12600.

TASK 3

P4 Explanation of the advantages and disadvantages of the varied kinds of budgetary planning

Budgetary control is regarded as the procedure in which Unicorn management is required to

develop the budget for the future duration of time by means of projection as well as comparing it

actual performance for the purpose of detecting the variances to take corrective measures without

making any delay. There is presence of several methods and tools that are important for the

preparation of budget in the years to come (Agrawal and Cooper, 2015). These are enumerated in

the manner stated as under:

10

in terms of net profit of per unit. Hence, it can be evaluated that out of these techniques marginal

costing is considered as suitable because it helps in measuring contribution and overall net profit

and thus managers need to carry out short term managerial planning.

D2 Development of report and interpretation of data

To: Unicorn’s Board of directors

Date: 1st April 2017

Subject: Determination of cost.

It can be evaluated that after calculating cost through using both the techniques it can be stated

that Unicorn helps in making marginal costing, actual profitability is quantified up to a high level

i.e. 11300. While, full costing method is valued at 9585.71 which is being considered as

comparatively low. Further, in the first it has been identified that expenses have been carried out

that they vary as per the changes in production or output within Unicorn. Moreover, it has been

assessed that both fixed and fluctuating cost of production has been evaluated and thus it helps in

identifying desired results (Gullifer and Payne, 2015). Hence, it results in identifying that low

profitability has been identified. Because of this closing inventory has been valued which is

reported very differently and under both this methods variable costing method has been valued

i.e. 1300. While, full costing has been evaluated that it is 1585.71 which is high. However, main

reason behind this is that full costing method has been taken into consideration and thus fixed

production overheads i.e. 2000 has not been involved within the cost of production and thus

identify that marginal cost results in computing manufacturing cost of products at Unicorn i.e.

11100 and 7800. While, less cost is the main reason for high contribution i.e. 12600.

TASK 3

P4 Explanation of the advantages and disadvantages of the varied kinds of budgetary planning

Budgetary control is regarded as the procedure in which Unicorn management is required to

develop the budget for the future duration of time by means of projection as well as comparing it

actual performance for the purpose of detecting the variances to take corrective measures without

making any delay. There is presence of several methods and tools that are important for the

preparation of budget in the years to come (Agrawal and Cooper, 2015). These are enumerated in

the manner stated as under:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental budgeting: This tool is on the basis of making smaller alterations in the prevailing

budgets in order to make preparation of new budget for the prospective year. This is considered

as effective way in terms that each year, incremental amounts are being added to the budget of

previous year as well as makes sure that funding is required on day to day basis. On the other

hand it encourages expenses as well as do not offer any kind of incentive to the managers for

cost curtailment (Marginal and absorption costing. 2016).

Advantages: It possesses merit in terms that it is simpler to be created. Along with this it makes

sure smaller or little deviations. Along with this it maintains equality in all the Unicorn

departments.

Disadvantages: It has disadvantage in terms that it encourages unnecessary spending. Along

with this there is no incentive for the control of cost. Further perpetual resource allocation system

is its major demerit (Romano, 2015).

Zero based budgeting

The manager of Unicorn can make development of budget considering into account zero as base.

Further it includes analysis of requirements as well as attached cost of each function along with

suitable justification by market research. It offers real figures regarding the potential operations

as managers assess the external market situations and after that forecast the future. Thus,

unnecessary actions are removed that encourage saving (Banerjee and Das, 2017).

Advantages: The main merit of such is that there are real figures with the judgement. Along with

this it assists in suitable planning. Further it lays emphasis on cost curtailment.

Disadvantages: It has major demerit in terms that it is time consuming. It has need for high

funding. Along with this it has demerit that is manager needs to be highly skilled in order to

assess trends within the market as well as challenges for the preparation of budget.

Fixed Budgeting: It is considered as the financial plans that do not differ in accordance with the

actual volume of production of Unicorn (Bhimani and et.al., 2013).

Advantages: The major merit it has is that it assists in measuring as well as examining the

performance. Further it assist in strategic decisions and plan related with growth. In addition to

this it keeps the cost at minimum level for the greater returns.

Disadvantages: The demerit it has is that it does not offer any kind of assistance for comparing

the outcomes in case the standard as well as actual output varies. Along with this it cannot be

altered in accordance with the actual level of activity.

11

budgets in order to make preparation of new budget for the prospective year. This is considered

as effective way in terms that each year, incremental amounts are being added to the budget of

previous year as well as makes sure that funding is required on day to day basis. On the other

hand it encourages expenses as well as do not offer any kind of incentive to the managers for

cost curtailment (Marginal and absorption costing. 2016).

Advantages: It possesses merit in terms that it is simpler to be created. Along with this it makes

sure smaller or little deviations. Along with this it maintains equality in all the Unicorn

departments.

Disadvantages: It has disadvantage in terms that it encourages unnecessary spending. Along

with this there is no incentive for the control of cost. Further perpetual resource allocation system

is its major demerit (Romano, 2015).

Zero based budgeting

The manager of Unicorn can make development of budget considering into account zero as base.

Further it includes analysis of requirements as well as attached cost of each function along with

suitable justification by market research. It offers real figures regarding the potential operations

as managers assess the external market situations and after that forecast the future. Thus,

unnecessary actions are removed that encourage saving (Banerjee and Das, 2017).

Advantages: The main merit of such is that there are real figures with the judgement. Along with

this it assists in suitable planning. Further it lays emphasis on cost curtailment.

Disadvantages: It has major demerit in terms that it is time consuming. It has need for high

funding. Along with this it has demerit that is manager needs to be highly skilled in order to

assess trends within the market as well as challenges for the preparation of budget.

Fixed Budgeting: It is considered as the financial plans that do not differ in accordance with the

actual volume of production of Unicorn (Bhimani and et.al., 2013).

Advantages: The major merit it has is that it assists in measuring as well as examining the

performance. Further it assist in strategic decisions and plan related with growth. In addition to

this it keeps the cost at minimum level for the greater returns.

Disadvantages: The demerit it has is that it does not offer any kind of assistance for comparing

the outcomes in case the standard as well as actual output varies. Along with this it cannot be

altered in accordance with the actual level of activity.

11

Flexible budgeting: In comparison with fixed, such kind of budgeting plan pays greater attention

to more than one production output (Chenhall and Moers, 2015).

Advantages: It assists in making adjustment of target as per the actual volume production of

Unicorn. In addition to this it offers assistance for optimum allocation of funds in accordance

with need. Along with this it makes adjustments in relation with market volatility that is inflation

and other.

Disadvantages: It needs to continuously monitor for tracking the changes within the external

environment that is time consuming process. Along with this there is an issue in determining the

data that results in arising complexities within the construction of budget (Christ and et.al.,

2017).

Activity based budgeting: In the modern era activity based budgeting is being utilized by the firm

for the preparation of the budgets. In accordance with the method Unicorn makes construction of

budget wherein each activity that bears cost in daily functionality is being reported. The essential

aspect of such is that income is being allocated to the associated activity cost.

Advantage: It is considered as the most suitable tool as it makes allocation of the revenue that is

being produced for each activity to its associated expenses. Further it lays emphasis on

controlling of overheads by means of taking distinctive measures of cost control.

Disadvantage: However demerit associated with such is that it needs managerial training for

training of individual in order to use the methods. Moreover it requires extensive managerial

skills as well as knowledge to possess in-depth understanding in relation with planning of budget

(Hecht, 2016).

M3 Analysis of the usage of varied planning tools and implementation for budget forecasting

Out of the above discussed tools of planning, it is being suggested to Unicorn to make use of

Zero based budgeting that demonstrate real projected figures regarding the future time. I=Under

this budget is required to be developed for greater than one activity volume. This means it is

flexible in nature for the sake of adjusting budgeted outcomes as per the actual production

volume in order to compare actual performance of firm with target set. In accordance with such

departmental manager of Unicorn can make comparison of operational effectiveness in

successful manner (Horngren and et.al., 2010). Identification of causes in relation with the

failure assists in bringing out the positive alterations as well as streamlining functionality of

regular basis for attaining success.

12

to more than one production output (Chenhall and Moers, 2015).

Advantages: It assists in making adjustment of target as per the actual volume production of

Unicorn. In addition to this it offers assistance for optimum allocation of funds in accordance

with need. Along with this it makes adjustments in relation with market volatility that is inflation

and other.

Disadvantages: It needs to continuously monitor for tracking the changes within the external

environment that is time consuming process. Along with this there is an issue in determining the

data that results in arising complexities within the construction of budget (Christ and et.al.,

2017).

Activity based budgeting: In the modern era activity based budgeting is being utilized by the firm

for the preparation of the budgets. In accordance with the method Unicorn makes construction of

budget wherein each activity that bears cost in daily functionality is being reported. The essential

aspect of such is that income is being allocated to the associated activity cost.

Advantage: It is considered as the most suitable tool as it makes allocation of the revenue that is

being produced for each activity to its associated expenses. Further it lays emphasis on

controlling of overheads by means of taking distinctive measures of cost control.

Disadvantage: However demerit associated with such is that it needs managerial training for

training of individual in order to use the methods. Moreover it requires extensive managerial

skills as well as knowledge to possess in-depth understanding in relation with planning of budget

(Hecht, 2016).

M3 Analysis of the usage of varied planning tools and implementation for budget forecasting

Out of the above discussed tools of planning, it is being suggested to Unicorn to make use of

Zero based budgeting that demonstrate real projected figures regarding the future time. I=Under

this budget is required to be developed for greater than one activity volume. This means it is

flexible in nature for the sake of adjusting budgeted outcomes as per the actual production

volume in order to compare actual performance of firm with target set. In accordance with such

departmental manager of Unicorn can make comparison of operational effectiveness in

successful manner (Horngren and et.al., 2010). Identification of causes in relation with the

failure assists in bringing out the positive alterations as well as streamlining functionality of

regular basis for attaining success.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.