Accounting Report: Analyzing ABC Motors Company Limited Annual Report

VerifiedAdded on 2023/03/29

|11

|1780

|224

Report

AI Summary

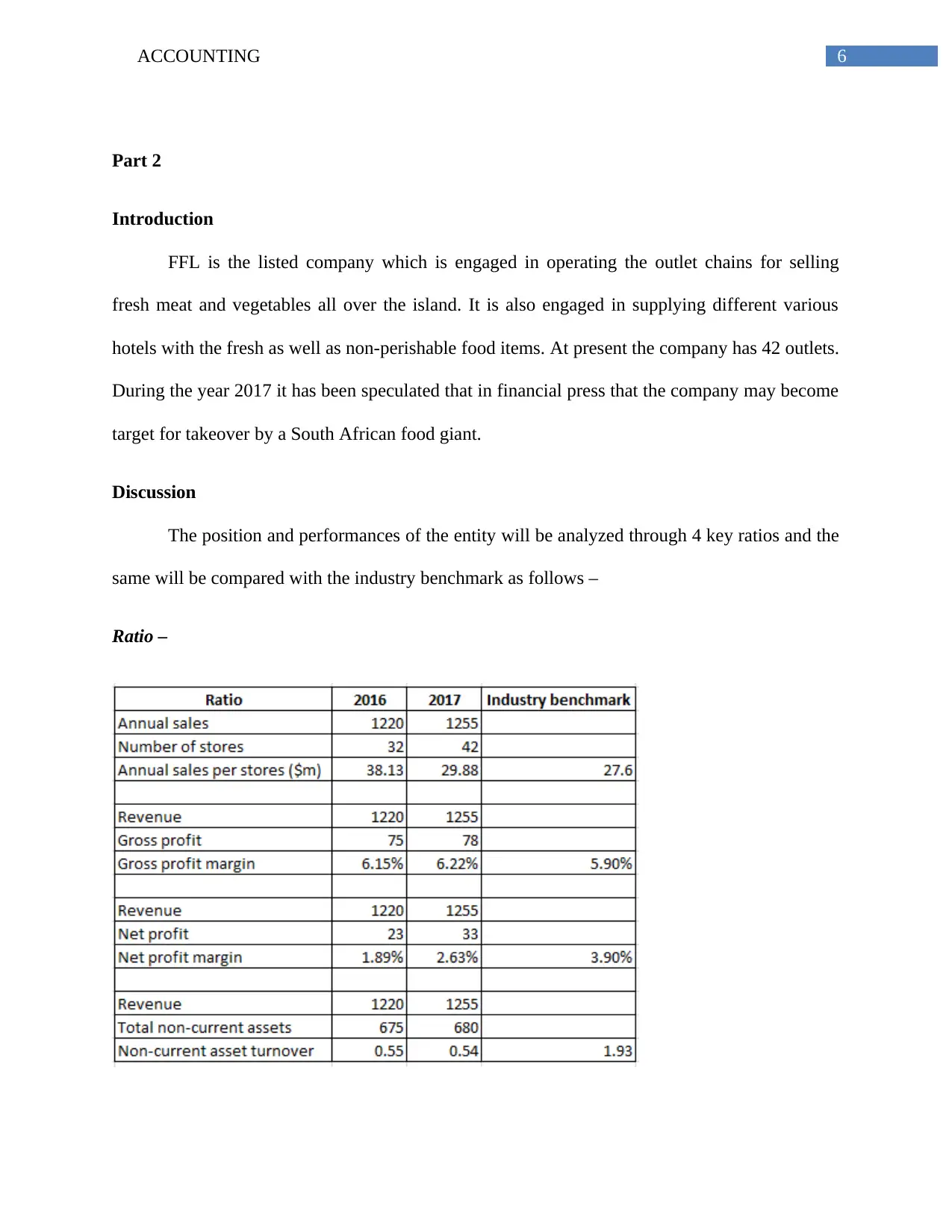

This report analyzes the annual report of ABC Motors Company Limited, a leading automotive entity listed on the Mauritius stock exchange. It identifies the major components of the annual report, including the director's report, company profile, corporate governance report, auditor's report, and financial statements (statement of financial position, statement of profit and loss, statement of changes in equity, and statement of cash flows). The report also identifies potential users of the annual report, such as investors, management, lenders, suppliers, government, employees, customers, and the general public, and elaborates on their specific information needs. Furthermore, the report analyzes Fresh Food Lovers (FFL), a listed company operating outlet chains for fresh meat and vegetables, using key financial ratios such as annual sales per store, gross profit margin, net profit margin, and non-current asset turnover, comparing them with industry benchmarks to assess the company's financial position and performance. The analysis concludes that FFL has generally improved its performance compared to the previous year and performs better than the industry benchmark, making it a potential takeover target.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.