Accounting Analysis of NSW Sydney Transportation Company Report

VerifiedAdded on 2021/04/21

|15

|2207

|31

Report

AI Summary

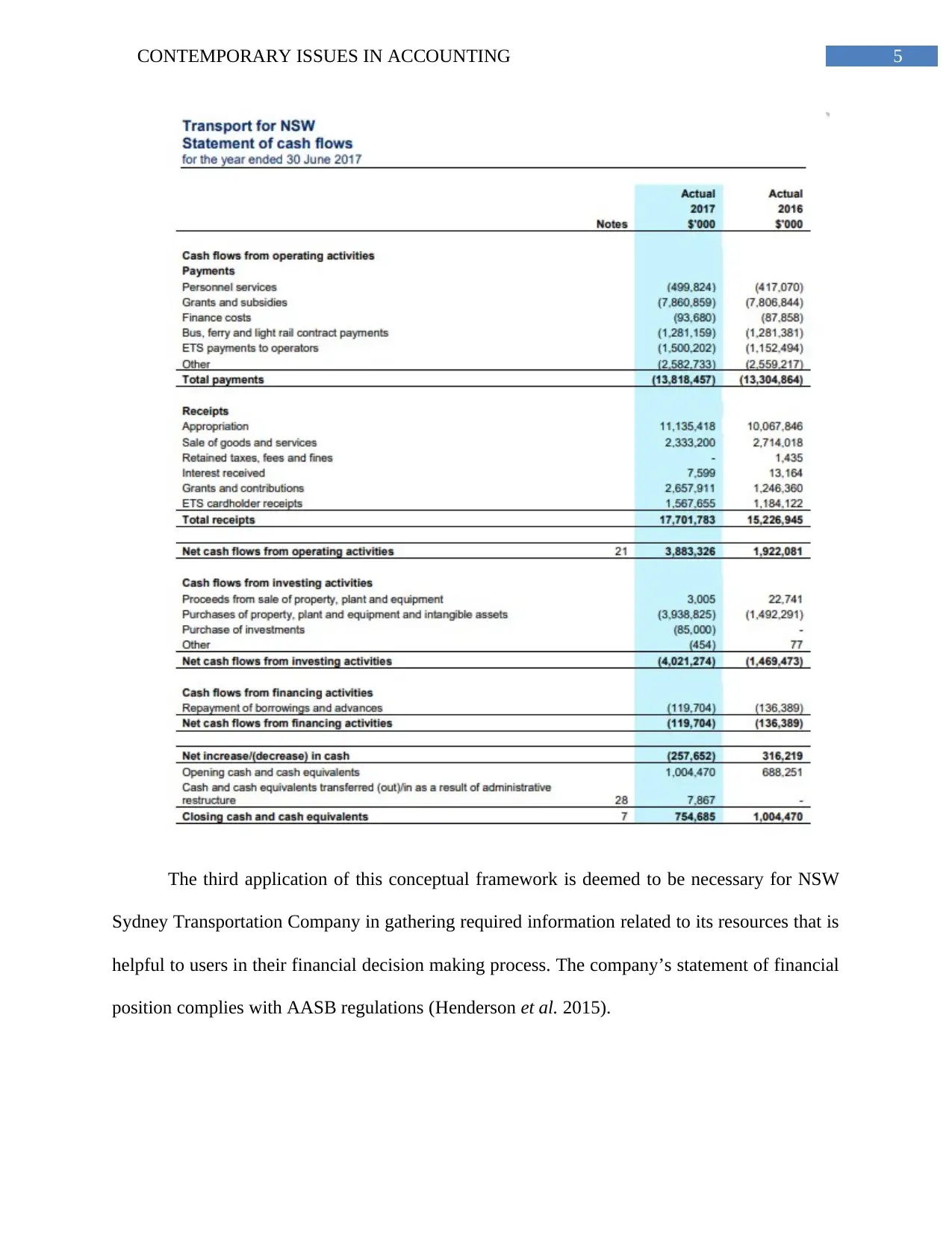

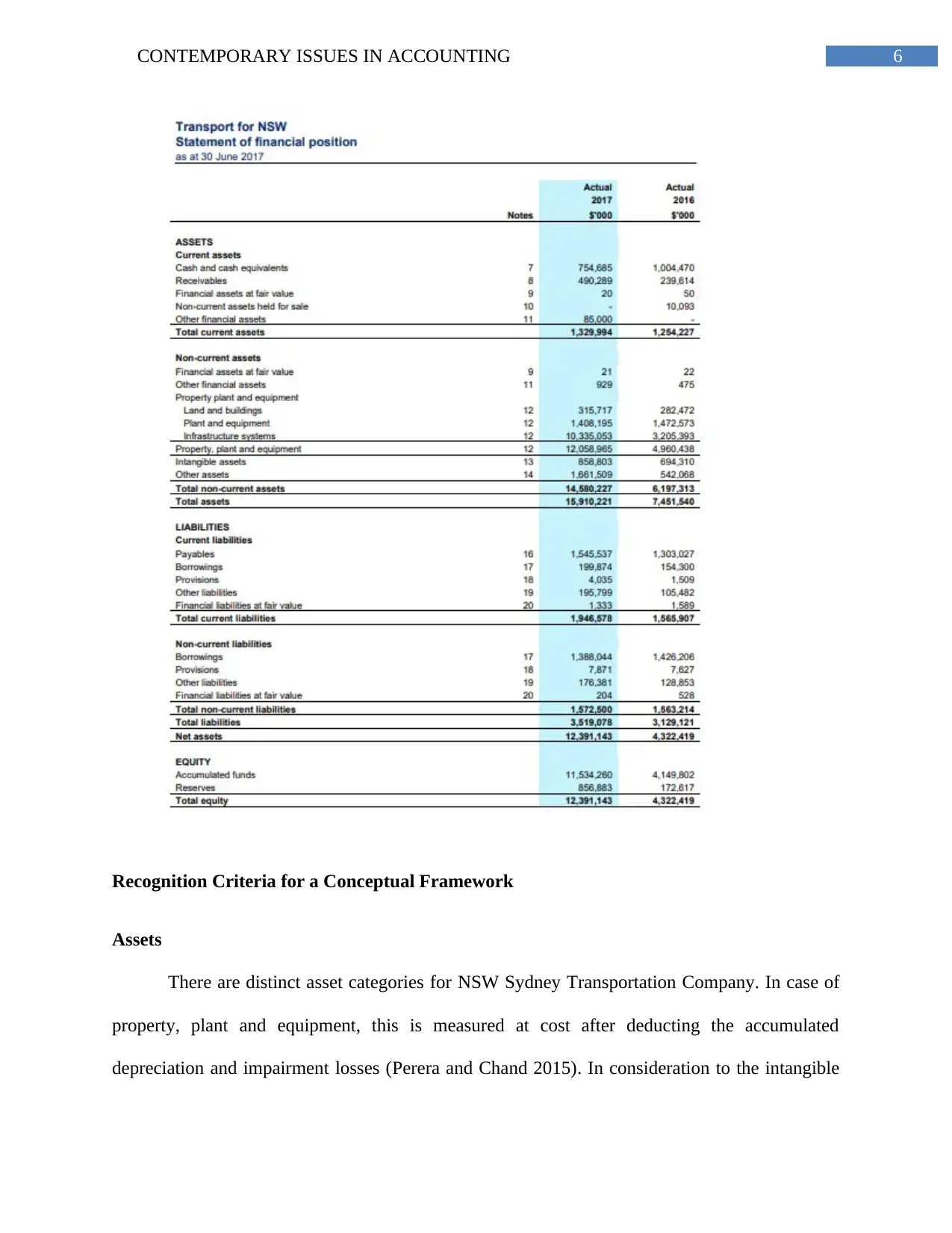

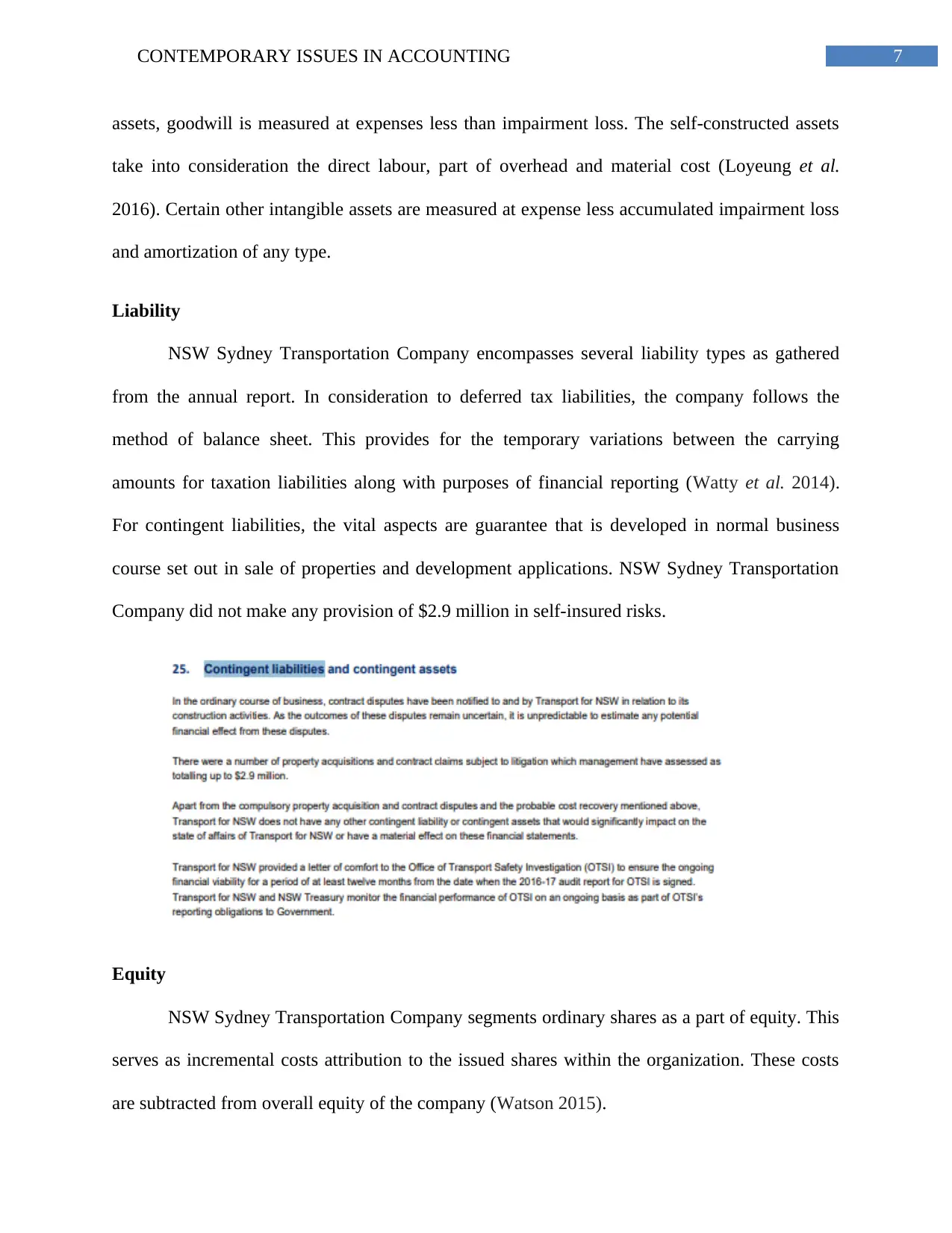

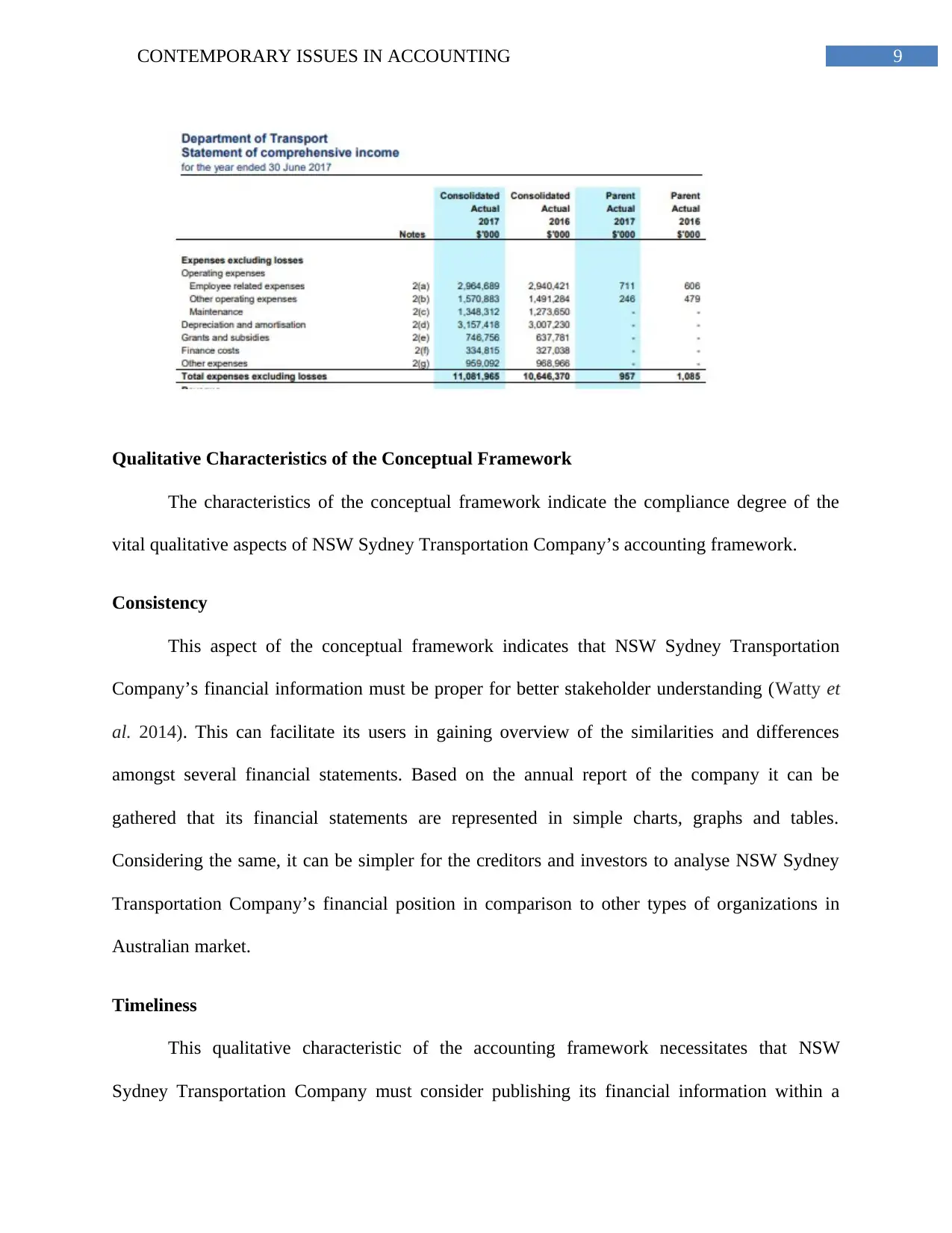

This report examines the contemporary accounting issues encountered by the NSW Sydney Transportation Company, a prominent entity listed on the ASX Top 100. The analysis delves into the company's application of the accounting conceptual framework, specifically focusing on its adherence to the Australian Accounting Standards Board (AASB) and its implications for financial reporting. The report explores key accounting concerns, including the efficient development of financial statements, regulatory compliance, and the maintenance of the conceptual framework. It then critically assesses the company's recognition criteria for assets, liabilities, equity, revenue, and expenses, as well as the qualitative characteristics of the conceptual framework, such as consistency, timeliness, verifiability, understandability, and faithful representation. The report concludes with recommendations for the company to improve the clarity and effectiveness of its financial reporting, including suggestions for presentation and adherence to conceptual principles like offsetting, cohesiveness, and classification. The report references relevant academic sources to support its analysis.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.