Corporate Accounting Analysis of Wesfarmers and Woolworths (HI5020)

VerifiedAdded on 2023/06/04

|19

|4203

|289

Report

AI Summary

This report presents a thorough accounting analysis of two Australian Securities Exchange (ASX)-listed companies, Wesfarmers Limited and Woolworths Group Limited, focusing on their financial performance. The analysis encompasses key financial aspects such as owner's equity, cash flow statements (including operating, investing, and financing activities), and other comprehensive income statements. The report examines the companies' issued capital, reserves, and retained earnings to assess their equity positions. It also delves into the cash flow statements, evaluating operating, investing, and financing activities over a period of time. Furthermore, the report discusses the accounting for corporate income tax, providing a comprehensive overview of the companies' financial health and decision-making processes. The report is structured to meet the requirements of a corporate accounting assignment, offering insights into the financial strategies and performance of these prominent Australian retailers.

Running head: ACCOUNTING

Accounting

Name of the student:

Name of the University:

Authors note:

Accounting

Name of the student:

Name of the University:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Executive Summary:

In the report is based on the analysis that considers the equity position that comprises of the

company’s cash flows, and other relevant statement of income. This is related to the basic

requirement of managing of the income tax for the corporate income that has lead to the

evaluation of the suitable that is based on the effective decision making on the methods right

investment of making the two companies namely Wesfarmers Limited and Woolworths Group

Limited. The various types of current assessment can be evaluated on the apparent solvent

position that would relate to both companies. On reviewing the balance sheet statement of the

company the4 companies shares reserves have declined on majority for calculating all the shares

equity of the company.

Executive Summary:

In the report is based on the analysis that considers the equity position that comprises of the

company’s cash flows, and other relevant statement of income. This is related to the basic

requirement of managing of the income tax for the corporate income that has lead to the

evaluation of the suitable that is based on the effective decision making on the methods right

investment of making the two companies namely Wesfarmers Limited and Woolworths Group

Limited. The various types of current assessment can be evaluated on the apparent solvent

position that would relate to both companies. On reviewing the balance sheet statement of the

company the4 companies shares reserves have declined on majority for calculating all the shares

equity of the company.

2ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Owner’s Equity................................................................................................................................4

Requirement (i)............................................................................................................................4

Requirement (ii)...........................................................................................................................5

Cash Flow Statement.......................................................................................................................5

Requirement (iii)..........................................................................................................................6

Operating cash Flow........................................................................................................................6

Investing cash flows........................................................................................................................6

Financing cash flows.......................................................................................................................7

Requirement (iv)..........................................................................................................................8

Requirement (v)...........................................................................................................................9

The other comprehensive income statement....................................................................................9

Requirement (vi)..........................................................................................................................9

Requirement (viii)......................................................................................................................10

Requirement (viii)......................................................................................................................10

Requirement (ix)........................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Owner’s Equity................................................................................................................................4

Requirement (i)............................................................................................................................4

Requirement (ii)...........................................................................................................................5

Cash Flow Statement.......................................................................................................................5

Requirement (iii)..........................................................................................................................6

Operating cash Flow........................................................................................................................6

Investing cash flows........................................................................................................................6

Financing cash flows.......................................................................................................................7

Requirement (iv)..........................................................................................................................8

Requirement (v)...........................................................................................................................9

The other comprehensive income statement....................................................................................9

Requirement (vi)..........................................................................................................................9

Requirement (viii)......................................................................................................................10

Requirement (viii)......................................................................................................................10

Requirement (ix)........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

Accounting for Corporate Income Tax..........................................................................................12

Requirement (x).........................................................................................................................12

Requirement (xi)........................................................................................................................12

Requirement (xii).......................................................................................................................13

Requirement (xiii)......................................................................................................................13

Requirement (xiv)......................................................................................................................14

Requirement (xv).......................................................................................................................14

Requirement (xvi)......................................................................................................................15

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Accounting for Corporate Income Tax..........................................................................................12

Requirement (x).........................................................................................................................12

Requirement (xi)........................................................................................................................12

Requirement (xii).......................................................................................................................13

Requirement (xiii)......................................................................................................................13

Requirement (xiv)......................................................................................................................14

Requirement (xv).......................................................................................................................14

Requirement (xvi)......................................................................................................................15

Conclusion.....................................................................................................................................15

References......................................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

Introduction

In this present scenario, it is normal practice for the shareholders to critically analyze

position of the equity, cash flow and some other relevant statement of income based on the

concept of corporate accounting income tax for undertaking some vital decisions of investment.

Specifically, for meeting the specific purposes of this report, the company Woolworth Group

Limited and the Wesfarmers have rightly taken into some considerations that comprises of the

two magnificent retailers who are operating within the super markets of Australia. The

mentioned aspects in this report is specifically discussed with the lights on the two organizations

there are selected using the specific methods that can be followed for bringing the disclosures of

all the items that are to be mentioned in the statement of finance.

Owner’s Equity

Requirement (i):

The statement of balance sheet of the company mainly consists of three major categories in

which main focus is given on equity part under this particular segment. The companies

Wesfarmers and Woolworth cannot be considered an exception context of equity. To be precise

enough, the capital that is issued treated by the business organization as equity. It has been

estimated that the issued capital of Woolworths has gone up significantly from the amount of $

5,252.20 million in the year 2016 and was evaluated in the year 2017 be around $ 5,615 million.

The same had happened for Wesfarmers where amount has been increased from $ 21,937 million

Introduction

In this present scenario, it is normal practice for the shareholders to critically analyze

position of the equity, cash flow and some other relevant statement of income based on the

concept of corporate accounting income tax for undertaking some vital decisions of investment.

Specifically, for meeting the specific purposes of this report, the company Woolworth Group

Limited and the Wesfarmers have rightly taken into some considerations that comprises of the

two magnificent retailers who are operating within the super markets of Australia. The

mentioned aspects in this report is specifically discussed with the lights on the two organizations

there are selected using the specific methods that can be followed for bringing the disclosures of

all the items that are to be mentioned in the statement of finance.

Owner’s Equity

Requirement (i):

The statement of balance sheet of the company mainly consists of three major categories in

which main focus is given on equity part under this particular segment. The companies

Wesfarmers and Woolworth cannot be considered an exception context of equity. To be precise

enough, the capital that is issued treated by the business organization as equity. It has been

estimated that the issued capital of Woolworths has gone up significantly from the amount of $

5,252.20 million in the year 2016 and was evaluated in the year 2017 be around $ 5,615 million.

The same had happened for Wesfarmers where amount has been increased from $ 21,937 million

5ACCOUNTING

in the year 2016 and in 2017, the amount reached $22,268. The amount was due, and the

management of the company for both the organization had gone for minimizing the funding for

debt (Dagwellet al 2015). From Woolworth and Wesfarmers that has been identified that the

company Woolworth has experienced an increase in the reserve rate from about $ 166 million in

the year 2016that amounts to $ 190 million by 2017 (Langfield-Smithet al 2017).

The equity shares occurs due to the repurchase and do not require a payment of dividend along

with the voting rights. It has been ascertained from the statement of the Wesfarmers a declination

in the reserved shares of the amount $ 28 million in the year 2016 which has been decreased by 2

million in the next accounting period of 2017. Hence there are no such specific shares that are

inherent for the case of Woolworths. It can be increased as retained earnings to be observed as

the profit base in the whole year (Al‐Hadiet al 2017).

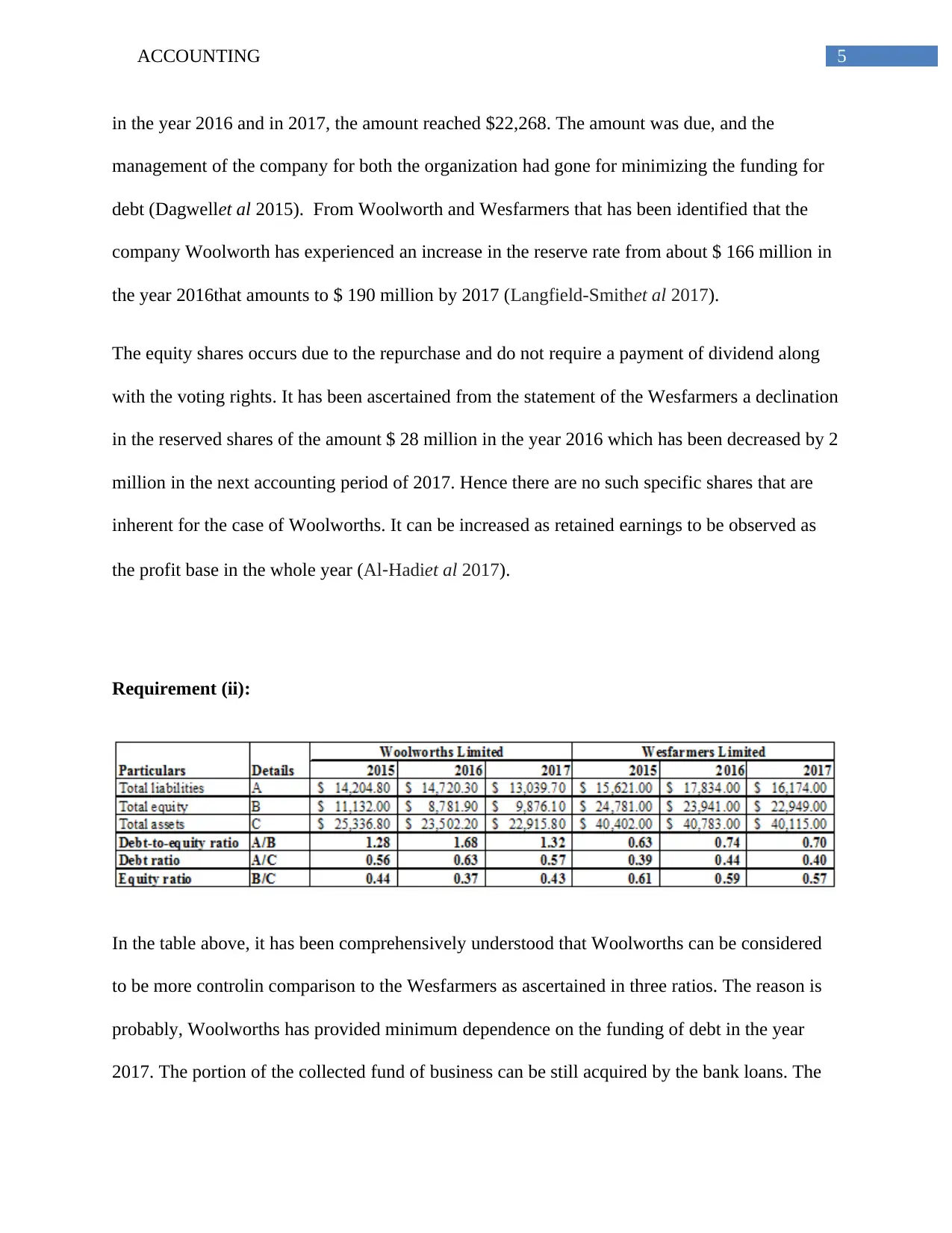

Requirement (ii):

In the table above, it has been comprehensively understood that Woolworths can be considered

to be more controlin comparison to the Wesfarmers as ascertained in three ratios. The reason is

probably, Woolworths has provided minimum dependence on the funding of debt in the year

2017. The portion of the collected fund of business can be still acquired by the bank loans. The

in the year 2016 and in 2017, the amount reached $22,268. The amount was due, and the

management of the company for both the organization had gone for minimizing the funding for

debt (Dagwellet al 2015). From Woolworth and Wesfarmers that has been identified that the

company Woolworth has experienced an increase in the reserve rate from about $ 166 million in

the year 2016that amounts to $ 190 million by 2017 (Langfield-Smithet al 2017).

The equity shares occurs due to the repurchase and do not require a payment of dividend along

with the voting rights. It has been ascertained from the statement of the Wesfarmers a declination

in the reserved shares of the amount $ 28 million in the year 2016 which has been decreased by 2

million in the next accounting period of 2017. Hence there are no such specific shares that are

inherent for the case of Woolworths. It can be increased as retained earnings to be observed as

the profit base in the whole year (Al‐Hadiet al 2017).

Requirement (ii):

In the table above, it has been comprehensively understood that Woolworths can be considered

to be more controlin comparison to the Wesfarmers as ascertained in three ratios. The reason is

probably, Woolworths has provided minimum dependence on the funding of debt in the year

2017. The portion of the collected fund of business can be still acquired by the bank loans. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

situation is just opposite with Wesfarmers as it raised a considerable portion for its equity shares

fund through market operation. It can be clearly estimated that, the solvent position terms when

considered by Wesfarmers can be compared with a much favorable position on bringing

comparison to the retail sector of Australian market considering Woolworths (Schaltegger et al

2017).

Cash Flow Statement:

Requirement (iii)

The items which have the considerable importance are listed within the statement of cash flow of

Woolworth and Wesfarmers that are briefly evaluated

Operating cash Flow:

The path mainly consists significantly of four items, that includes the payments made to the

suppliers and employee structure, the receipts received from the customers, the interest payments

and the cost that is borrowed from others. The amount tamed is mainly denoted by the receipts

from the business customers according to which the sales are generally made on the credit basis.

Furthermore, the payments made to the suppliers during both organizations have mutually

increased due to the product line extension for fulfilling certain changes of preferences among

the ultimate customers. The other side, signifies the payments of interest from among those

amounts that and business organization needs to incur for some loans from Bank that can be

taken for conducting the daily operations in business. For both the business concern, the interest

situation is just opposite with Wesfarmers as it raised a considerable portion for its equity shares

fund through market operation. It can be clearly estimated that, the solvent position terms when

considered by Wesfarmers can be compared with a much favorable position on bringing

comparison to the retail sector of Australian market considering Woolworths (Schaltegger et al

2017).

Cash Flow Statement:

Requirement (iii)

The items which have the considerable importance are listed within the statement of cash flow of

Woolworth and Wesfarmers that are briefly evaluated

Operating cash Flow:

The path mainly consists significantly of four items, that includes the payments made to the

suppliers and employee structure, the receipts received from the customers, the interest payments

and the cost that is borrowed from others. The amount tamed is mainly denoted by the receipts

from the business customers according to which the sales are generally made on the credit basis.

Furthermore, the payments made to the suppliers during both organizations have mutually

increased due to the product line extension for fulfilling certain changes of preferences among

the ultimate customers. The other side, signifies the payments of interest from among those

amounts that and business organization needs to incur for some loans from Bank that can be

taken for conducting the daily operations in business. For both the business concern, the interest

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

payments gradually declined over a period of time I have reduced their interdependence on fund

raising true collection of debts (Epstein 2018).

Investing cash flows:

The items that are considered under the section basically includes payments that comprises of the

plant, equipments and properties that are considered add some specific amount that are meant for

acquiring and purchasing the necessary items that are essential for carrying out business

proceedings. On the conversing note, that includes those assets that help in generating income to

be on the advantages position for organization. The assets mainly comprises of the equipment

proceedings along with the plant and the property. The information has been gathered that

according to the company Wesfarmers Limited, fees in the investment rate for the year 2017 this

has increased passage of time because of some assets portions. In such an situation, the

Woolworths a considerable processing amount needs to be gathered from the arrangement the

company associates jointly. The amount gathered for the investment of about $ 47 millions along

with the attainment of redemption loan notes of about $ 54 million (Carnegie and O’Connell

2014).

Financing cash flows:

The most important divisions within the activities of financing generally includes mission of

repayment and equity proceeds. The proceeds are made with the dividends of equity and the

borrowings that are offered to the shareholders of Wesfarmers Limited. The procedure of

payments gradually declined over a period of time I have reduced their interdependence on fund

raising true collection of debts (Epstein 2018).

Investing cash flows:

The items that are considered under the section basically includes payments that comprises of the

plant, equipments and properties that are considered add some specific amount that are meant for

acquiring and purchasing the necessary items that are essential for carrying out business

proceedings. On the conversing note, that includes those assets that help in generating income to

be on the advantages position for organization. The assets mainly comprises of the equipment

proceedings along with the plant and the property. The information has been gathered that

according to the company Wesfarmers Limited, fees in the investment rate for the year 2017 this

has increased passage of time because of some assets portions. In such an situation, the

Woolworths a considerable processing amount needs to be gathered from the arrangement the

company associates jointly. The amount gathered for the investment of about $ 47 millions along

with the attainment of redemption loan notes of about $ 54 million (Carnegie and O’Connell

2014).

Financing cash flows:

The most important divisions within the activities of financing generally includes mission of

repayment and equity proceeds. The proceeds are made with the dividends of equity and the

borrowings that are offered to the shareholders of Wesfarmers Limited. The procedure of

8ACCOUNTING

borrowing mainly indicates that the net amount the companies lender to its segment of borrowers

under some conditions that are quite relevant sorry nice eating loan agreements. On considering

the situation of the company Woolworth Limited, there has been a drop in the amount of

borrowings extension of the loan terms there are made to the company debtors. There is also an

increased the amount of offerings made to the bank for repayment of loans as well as the equity

dividend clearly indicates that there is a offer to the companies equity shareholders from the

annual cash flow. On considering the case analysis of Wesfarmers, dividend payment has been

decreased gate 2017 and has got focused on increasing the rate of retained earning (Quet al

2018).

Requirement (iv):

As it has been gathered from the annual report, the company Woolworth and Wesfarmers

Limited has three segments of cash flow that also includes the operational investment along with

the activities of finance. The table shows an comparative analysis of the main identified groups

and the categories that can be considered within the statement of cash flow on considering the

previous three years of business (Sivathaasan 2016).

borrowing mainly indicates that the net amount the companies lender to its segment of borrowers

under some conditions that are quite relevant sorry nice eating loan agreements. On considering

the situation of the company Woolworth Limited, there has been a drop in the amount of

borrowings extension of the loan terms there are made to the company debtors. There is also an

increased the amount of offerings made to the bank for repayment of loans as well as the equity

dividend clearly indicates that there is a offer to the companies equity shareholders from the

annual cash flow. On considering the case analysis of Wesfarmers, dividend payment has been

decreased gate 2017 and has got focused on increasing the rate of retained earning (Quet al

2018).

Requirement (iv):

As it has been gathered from the annual report, the company Woolworth and Wesfarmers

Limited has three segments of cash flow that also includes the operational investment along with

the activities of finance. The table shows an comparative analysis of the main identified groups

and the categories that can be considered within the statement of cash flow on considering the

previous three years of business (Sivathaasan 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

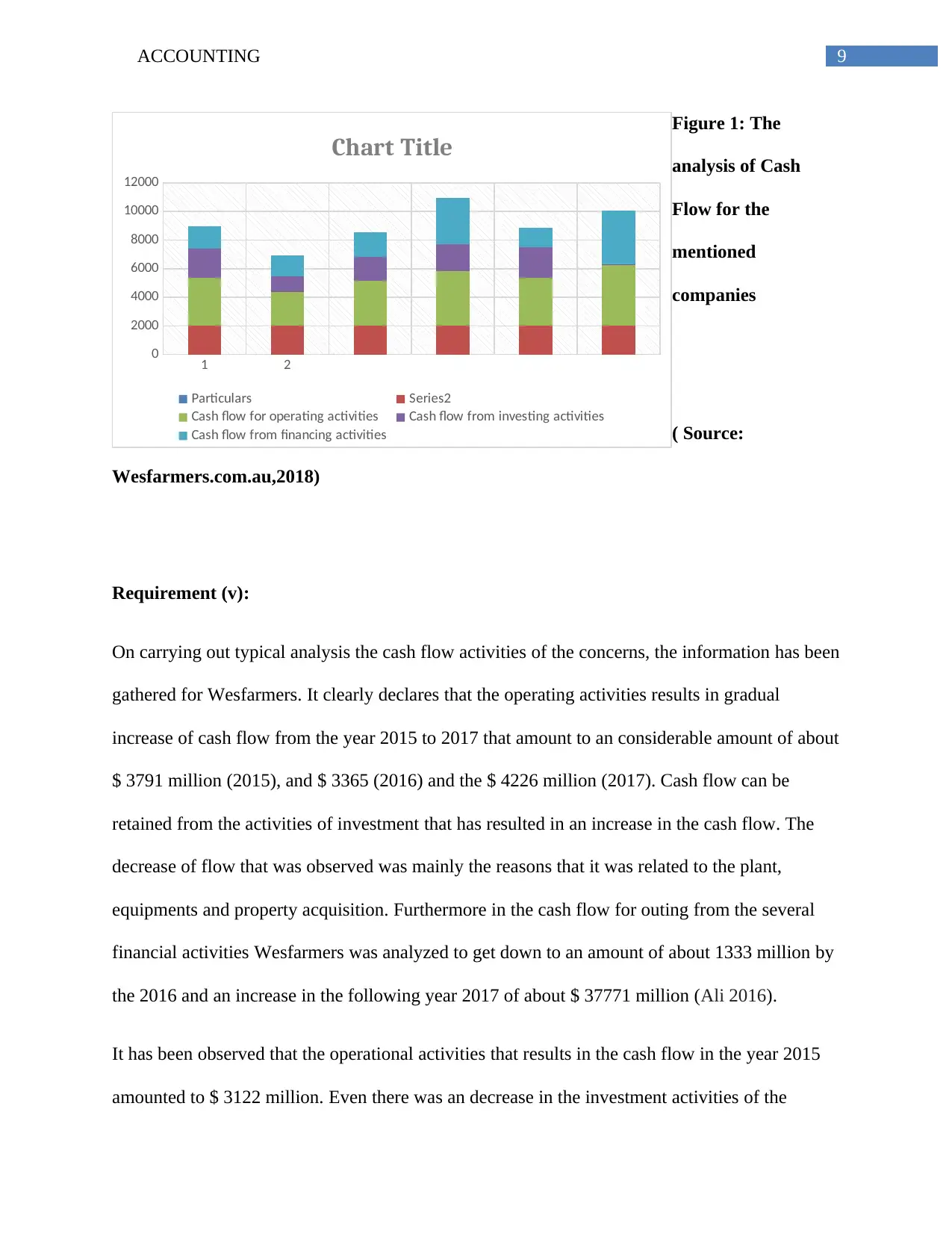

Figure 1: The

analysis of Cash

Flow for the

mentioned

companies

( Source:

Wesfarmers.com.au,2018)

Requirement (v):

On carrying out typical analysis the cash flow activities of the concerns, the information has been

gathered for Wesfarmers. It clearly declares that the operating activities results in gradual

increase of cash flow from the year 2015 to 2017 that amount to an considerable amount of about

$ 3791 million (2015), and $ 3365 (2016) and the $ 4226 million (2017). Cash flow can be

retained from the activities of investment that has resulted in an increase in the cash flow. The

decrease of flow that was observed was mainly the reasons that it was related to the plant,

equipments and property acquisition. Furthermore in the cash flow for outing from the several

financial activities Wesfarmers was analyzed to get down to an amount of about 1333 million by

the 2016 and an increase in the following year 2017 of about $ 37771 million (Ali 2016).

It has been observed that the operational activities that results in the cash flow in the year 2015

amounted to $ 3122 million. Even there was an decrease in the investment activities of the

1 2

0

2000

4000

6000

8000

10000

12000

Chart Title

Particulars Series2

Cash flow for operating activities Cash flow from investing activities

Cash flow from financing activities

Figure 1: The

analysis of Cash

Flow for the

mentioned

companies

( Source:

Wesfarmers.com.au,2018)

Requirement (v):

On carrying out typical analysis the cash flow activities of the concerns, the information has been

gathered for Wesfarmers. It clearly declares that the operating activities results in gradual

increase of cash flow from the year 2015 to 2017 that amount to an considerable amount of about

$ 3791 million (2015), and $ 3365 (2016) and the $ 4226 million (2017). Cash flow can be

retained from the activities of investment that has resulted in an increase in the cash flow. The

decrease of flow that was observed was mainly the reasons that it was related to the plant,

equipments and property acquisition. Furthermore in the cash flow for outing from the several

financial activities Wesfarmers was analyzed to get down to an amount of about 1333 million by

the 2016 and an increase in the following year 2017 of about $ 37771 million (Ali 2016).

It has been observed that the operational activities that results in the cash flow in the year 2015

amounted to $ 3122 million. Even there was an decrease in the investment activities of the

1 2

0

2000

4000

6000

8000

10000

12000

Chart Title

Particulars Series2

Cash flow for operating activities Cash flow from investing activities

Cash flow from financing activities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

business concern. The main reasons that lies behind clearing all the loans by the year 2016 is

because of all the activities of investment. The financial activities results in the increase in the

cash flow that gradually increases from 2015 to the early span of 2017 on putting upon a

comparatively analysis to the business concern Wesfarmers Limited (Miglaniet al 2015).

The other comprehensive income statement:

Requirement (vi):

The major and mandatory aspects that have been reported with some of the specifications for the

comprehensive statement of income of the business concerns Woolworths Limited and

Wesfarmers generally includes the retained earnings, cash flow hedges reserve and the retained

earning along with translation reserve of the foreign currencies (Carnegie 2014).

Requirement (viii):

The foreign currencies are employed for initiation of certain subsidiaries for the parent company

for reporting the currencies. This can be considered as a major part for facilitating the

consolidation of the financial statements of the Wesfarmers for the currencies that are functional

for the several cross-border business organizations that needs to be ascertained initially (Bryce et

al 2015). Additionally, the foreign companies at the same time re-measured along with the

reporting currencies within the working of the parent organization. It ultimately indicates the

parts of retained that can be evaluated by calculation of the payment of dividend that is enabled

the shareholders. This also is investment within the company capital projects that are meant for

business concern. The main reasons that lies behind clearing all the loans by the year 2016 is

because of all the activities of investment. The financial activities results in the increase in the

cash flow that gradually increases from 2015 to the early span of 2017 on putting upon a

comparatively analysis to the business concern Wesfarmers Limited (Miglaniet al 2015).

The other comprehensive income statement:

Requirement (vi):

The major and mandatory aspects that have been reported with some of the specifications for the

comprehensive statement of income of the business concerns Woolworths Limited and

Wesfarmers generally includes the retained earnings, cash flow hedges reserve and the retained

earning along with translation reserve of the foreign currencies (Carnegie 2014).

Requirement (viii):

The foreign currencies are employed for initiation of certain subsidiaries for the parent company

for reporting the currencies. This can be considered as a major part for facilitating the

consolidation of the financial statements of the Wesfarmers for the currencies that are functional

for the several cross-border business organizations that needs to be ascertained initially (Bryce et

al 2015). Additionally, the foreign companies at the same time re-measured along with the

reporting currencies within the working of the parent organization. It ultimately indicates the

parts of retained that can be evaluated by calculation of the payment of dividend that is enabled

the shareholders. This also is investment within the company capital projects that are meant for

11ACCOUNTING

bringing the development in the future years. On analyzing the case of Woolworths Limited, the

hedge reserve that can be used for the benefit of the company has been subjected to decrease and

finally get rid of certain exposure. It also results in changes in the liability in the financial assets

from the changes in cash flow. This is the result of some particular changes within the risk

factors like the floating rate debt and the interest rates (Watson 2015).

Requirement (viii):

On analyzing the statement of comprehensive income has been observed various kinds of

diversified views that the company has been subjected to a net profit. Over the early years, there

has been certain change in the profit that has been observed as a major channel operation that can

be considered volatile. It results in transfer within the equity of shareholders. To be on the note

of comparative analysis, the employee base of Wesfarmers can go for employing certain income

statement considerably on the details of the numerical associated along with the other types of

items that are mentioned. In case of the company Woolworth Limited, the income

comprehensively is observed within the income statement for offering comprehensiveness along

with certain perceptions that are not concurrent enough for all kinds of business operation and all

kind of activities that may not be adequately reported among the statement of income (Tucker

and Schaltegger 2016).

Requirement (ix):

It can be clearly observed from the income statement comprehensively that it is likely to get the

potential recognition of the items important. The reason is facilitating the right manner in which

the company dealings and the issues related to investment can be conducted with the ability to

bringing the development in the future years. On analyzing the case of Woolworths Limited, the

hedge reserve that can be used for the benefit of the company has been subjected to decrease and

finally get rid of certain exposure. It also results in changes in the liability in the financial assets

from the changes in cash flow. This is the result of some particular changes within the risk

factors like the floating rate debt and the interest rates (Watson 2015).

Requirement (viii):

On analyzing the statement of comprehensive income has been observed various kinds of

diversified views that the company has been subjected to a net profit. Over the early years, there

has been certain change in the profit that has been observed as a major channel operation that can

be considered volatile. It results in transfer within the equity of shareholders. To be on the note

of comparative analysis, the employee base of Wesfarmers can go for employing certain income

statement considerably on the details of the numerical associated along with the other types of

items that are mentioned. In case of the company Woolworth Limited, the income

comprehensively is observed within the income statement for offering comprehensiveness along

with certain perceptions that are not concurrent enough for all kinds of business operation and all

kind of activities that may not be adequately reported among the statement of income (Tucker

and Schaltegger 2016).

Requirement (ix):

It can be clearly observed from the income statement comprehensively that it is likely to get the

potential recognition of the items important. The reason is facilitating the right manner in which

the company dealings and the issues related to investment can be conducted with the ability to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.