ACCT20073: Company Accounting Assessment Task 2 - Part B

VerifiedAdded on 2023/03/17

|7

|898

|89

Report

AI Summary

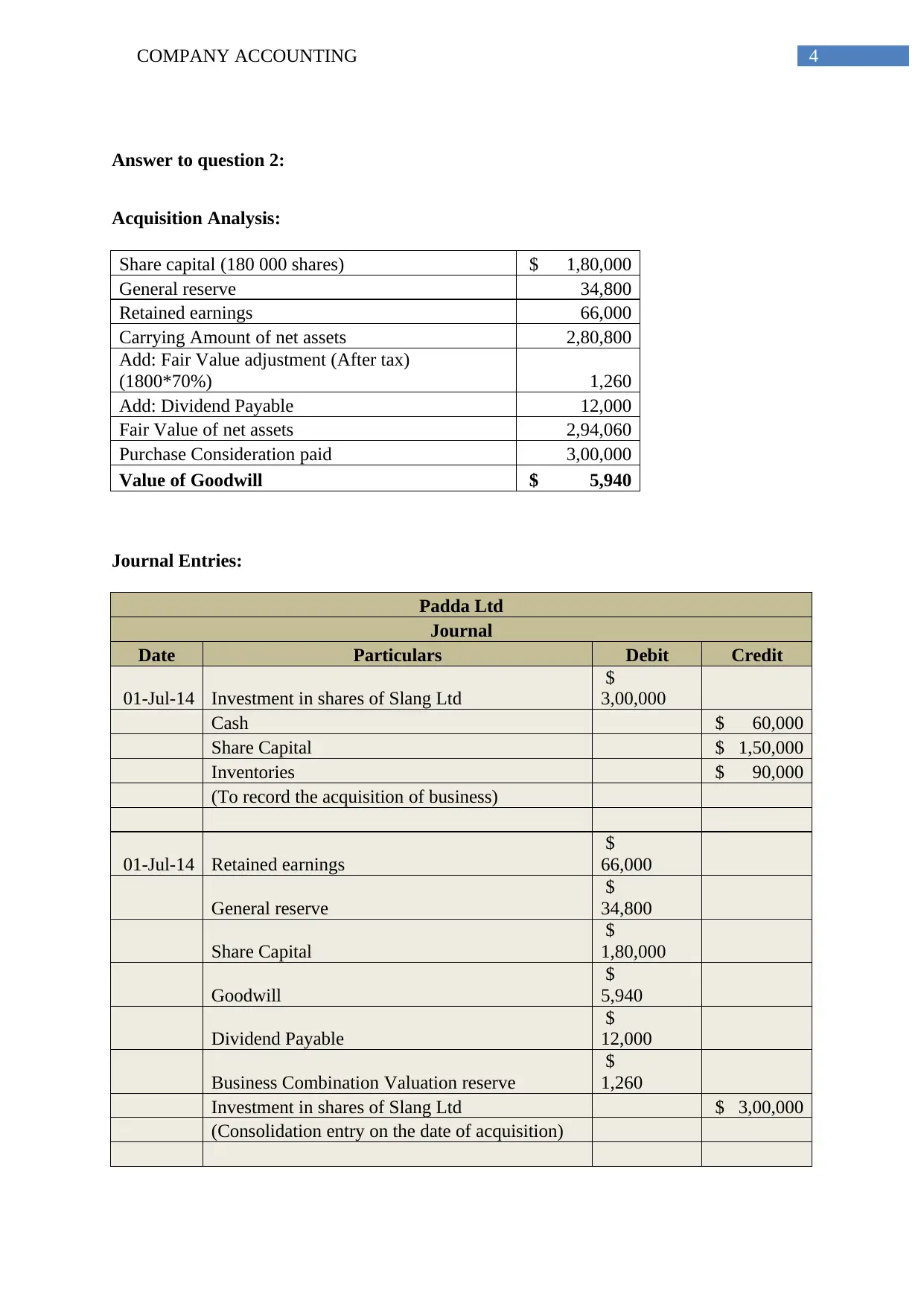

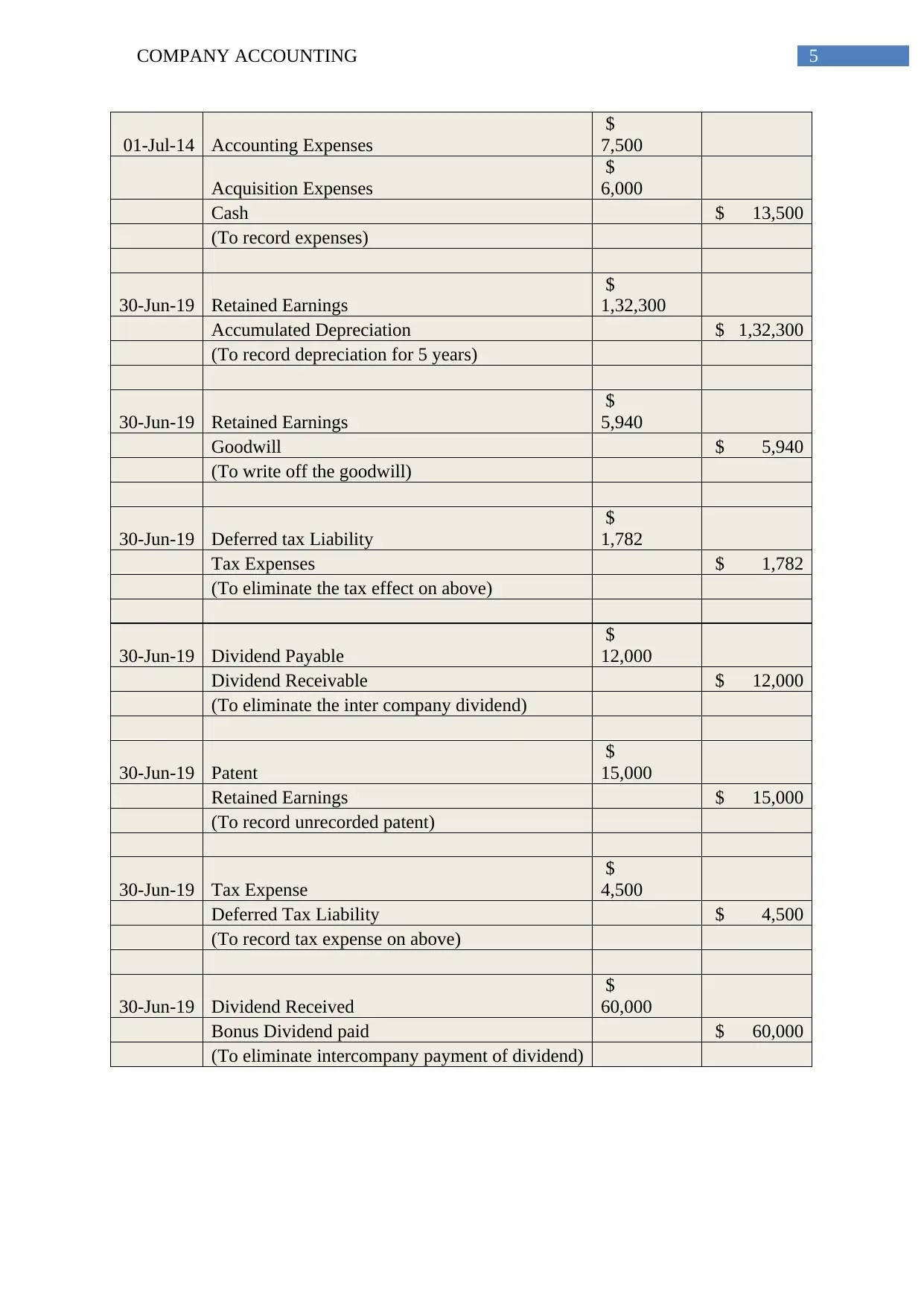

This report provides a comprehensive analysis of company accounting principles, specifically focusing on the concepts of goodwill and its accounting treatment. The report begins with a memorandum explaining the nature of goodwill, differentiating between inherent and purchased goodwill, and detailing how each should be recorded and amortized in the books of accounts. Following this, the report presents an acquisition analysis, including the calculation of goodwill based on the purchase consideration and the fair value of net assets. It then provides a series of journal entries to illustrate the recording of the acquisition, consolidation entries, and other accounting adjustments such as depreciation, goodwill write-off, and tax implications. The report also includes consolidation entries, the elimination of intercompany transactions, and the recording of unrecorded assets. Finally, the report includes a bibliography of relevant accounting literature.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.