Accounting Standards and Regulations: Myer's Asset Impairment

VerifiedAdded on 2020/02/24

|10

|1876

|38

Report

AI Summary

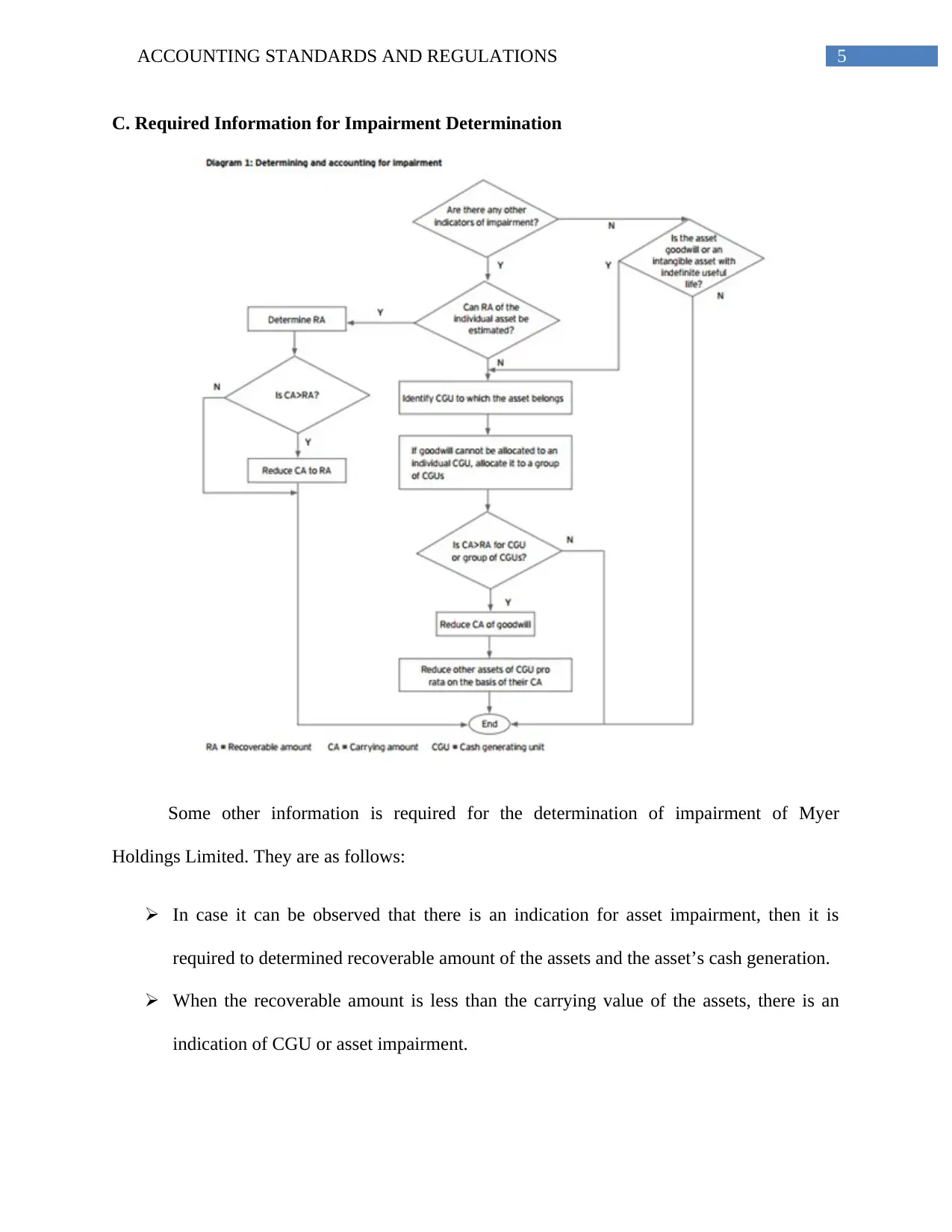

This report provides an in-depth analysis of Myer's asset impairment, adhering to Accounting Standards and Regulations, specifically AASB 136 and IAS 36. The report examines the required evidence for asset impairment testing, focusing on asset flow, asset base, and asset turnover. It outlines the procedures for determining impairment, including the use of a discounted cash flow model with key assumptions such as the pre-tax rate of discount, terminal growth rate, and operational gross profit margin. The report also details the information required for impairment determination, emphasizing the recoverable amount and the treatment of goodwill and intangible assets. Furthermore, it explores the flexibility available to Myer's management in conducting asset impairment tests, highlighting their role in assessing the carrying value of stores and determining future cash flows. The analysis concludes that there is no indication of asset impairment at Myer's stores for the year ended 2016, demonstrating compliance with accounting standards and regulations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.