Accounting Homework: Accrual Accounting and Ratio Analysis

VerifiedAdded on 2020/04/21

|11

|2132

|495

Homework Assignment

AI Summary

This accounting assignment delves into the principles of accrual accounting and financial statement analysis. It includes solutions to problems related to prepaid insurance, outstanding bills, and depreciation, demonstrating how these elements are reflected in the balance sheet, profit and loss statement, and cash flow statement. The assignment also provides a comprehensive interpretation of financial ratios, including profitability, liquidity, efficiency, leverage, and shareholder return, based on data from 2011 and 2012. Furthermore, it explores the importance of ratio analysis in evaluating business performance, providing insights into the strengths and weaknesses of a sample company, highlighting trends in sales, return on investment, and the potential impact on future revenue generation.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Authors Note:

Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

Accrual Accounting:..................................................................................................................2

P4.10...........................................................................................................................................2

Statement of Comprehensive Income........................................................................................3

P 4.12..........................................................................................................................................3

Interpretation of Financial Statement and Ratio........................................................................3

P 5.6............................................................................................................................................3

Interpretation of ratios................................................................................................................6

P5.12...........................................................................................................................................6

Reference....................................................................................................................................8

Table of Contents

Accrual Accounting:..................................................................................................................2

P4.10...........................................................................................................................................2

Statement of Comprehensive Income........................................................................................3

P 4.12..........................................................................................................................................3

Interpretation of Financial Statement and Ratio........................................................................3

P 5.6............................................................................................................................................3

Interpretation of ratios................................................................................................................6

P5.12...........................................................................................................................................6

Reference....................................................................................................................................8

2ACCOUNTING

Accrual Accounting:

P4.10

Answer to Question A:

According to the case, the total amount of insurance premium for 24 vehicles will be

$9,600. Now as the business follows accrual accounting system and the insurance premium

period is January-December for each year, thus as per the company’s current financial year,

the company has made a prepaid insurance for a period of 9 months starting from April-

December which will be recorded in the balance sheet as prepaid insurance (Fullerton et al.,

2014).

Answer to Question B:

The usage bills are sent on a quarterly and as the company’s financial period are

January-December, thus the amount for December will be shown in the financial statement of

the company as outstanding bill whereas the bill amount will affect the cash flow statement

after the actual payment that is on the last day of February (Renz 2016).

Answer to Question C:

As the company has purchased the Asset (Computer Network Server) for $12,000 on

30th June, therefore, the depreciation for the same will be applicable from July to March of

the next year i.e. for the period of 9 months. The amount of depreciation which is $1,800 will

be shown in the statement of Profit and loss as an expenses. Similarly in the financial

statement the value of the asset will get reduced by the amount of depreciation as

accumulated depreciation (Otley & Emmanuel, 2013). However there will be no effect of

Accrual Accounting:

P4.10

Answer to Question A:

According to the case, the total amount of insurance premium for 24 vehicles will be

$9,600. Now as the business follows accrual accounting system and the insurance premium

period is January-December for each year, thus as per the company’s current financial year,

the company has made a prepaid insurance for a period of 9 months starting from April-

December which will be recorded in the balance sheet as prepaid insurance (Fullerton et al.,

2014).

Answer to Question B:

The usage bills are sent on a quarterly and as the company’s financial period are

January-December, thus the amount for December will be shown in the financial statement of

the company as outstanding bill whereas the bill amount will affect the cash flow statement

after the actual payment that is on the last day of February (Renz 2016).

Answer to Question C:

As the company has purchased the Asset (Computer Network Server) for $12,000 on

30th June, therefore, the depreciation for the same will be applicable from July to March of

the next year i.e. for the period of 9 months. The amount of depreciation which is $1,800 will

be shown in the statement of Profit and loss as an expenses. Similarly in the financial

statement the value of the asset will get reduced by the amount of depreciation as

accumulated depreciation (Otley & Emmanuel, 2013). However there will be no effect of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

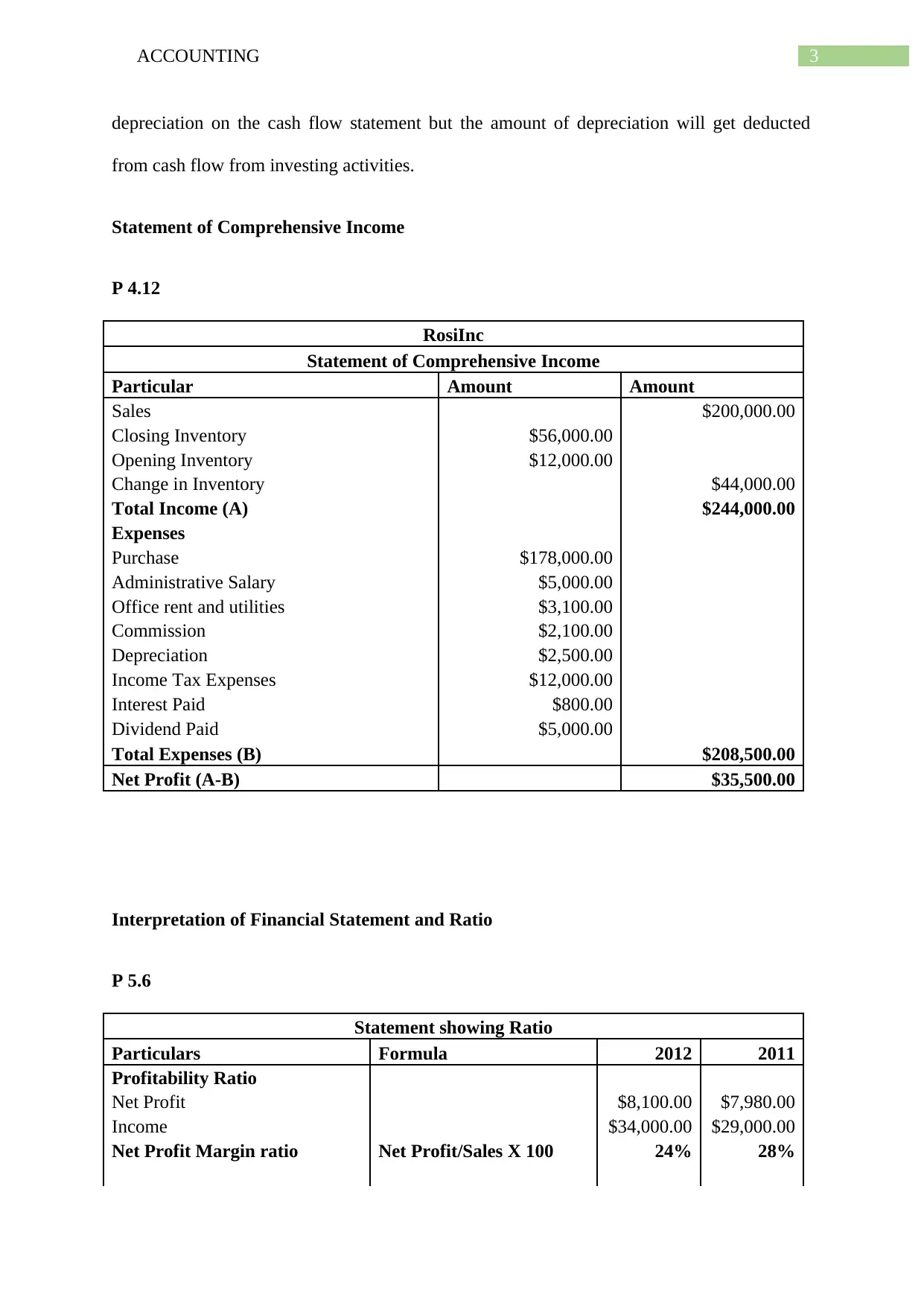

depreciation on the cash flow statement but the amount of depreciation will get deducted

from cash flow from investing activities.

Statement of Comprehensive Income

P 4.12

RosiInc

Statement of Comprehensive Income

Particular Amount Amount

Sales $200,000.00

Closing Inventory $56,000.00

Opening Inventory $12,000.00

Change in Inventory $44,000.00

Total Income (A) $244,000.00

Expenses

Purchase $178,000.00

Administrative Salary $5,000.00

Office rent and utilities $3,100.00

Commission $2,100.00

Depreciation $2,500.00

Income Tax Expenses $12,000.00

Interest Paid $800.00

Dividend Paid $5,000.00

Total Expenses (B) $208,500.00

Net Profit (A-B) $35,500.00

Interpretation of Financial Statement and Ratio

P 5.6

Statement showing Ratio

Particulars Formula 2012 2011

Profitability Ratio

Net Profit $8,100.00 $7,980.00

Income $34,000.00 $29,000.00

Net Profit Margin ratio Net Profit/Sales X 100 24% 28%

depreciation on the cash flow statement but the amount of depreciation will get deducted

from cash flow from investing activities.

Statement of Comprehensive Income

P 4.12

RosiInc

Statement of Comprehensive Income

Particular Amount Amount

Sales $200,000.00

Closing Inventory $56,000.00

Opening Inventory $12,000.00

Change in Inventory $44,000.00

Total Income (A) $244,000.00

Expenses

Purchase $178,000.00

Administrative Salary $5,000.00

Office rent and utilities $3,100.00

Commission $2,100.00

Depreciation $2,500.00

Income Tax Expenses $12,000.00

Interest Paid $800.00

Dividend Paid $5,000.00

Total Expenses (B) $208,500.00

Net Profit (A-B) $35,500.00

Interpretation of Financial Statement and Ratio

P 5.6

Statement showing Ratio

Particulars Formula 2012 2011

Profitability Ratio

Net Profit $8,100.00 $7,980.00

Income $34,000.00 $29,000.00

Net Profit Margin ratio Net Profit/Sales X 100 24% 28%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

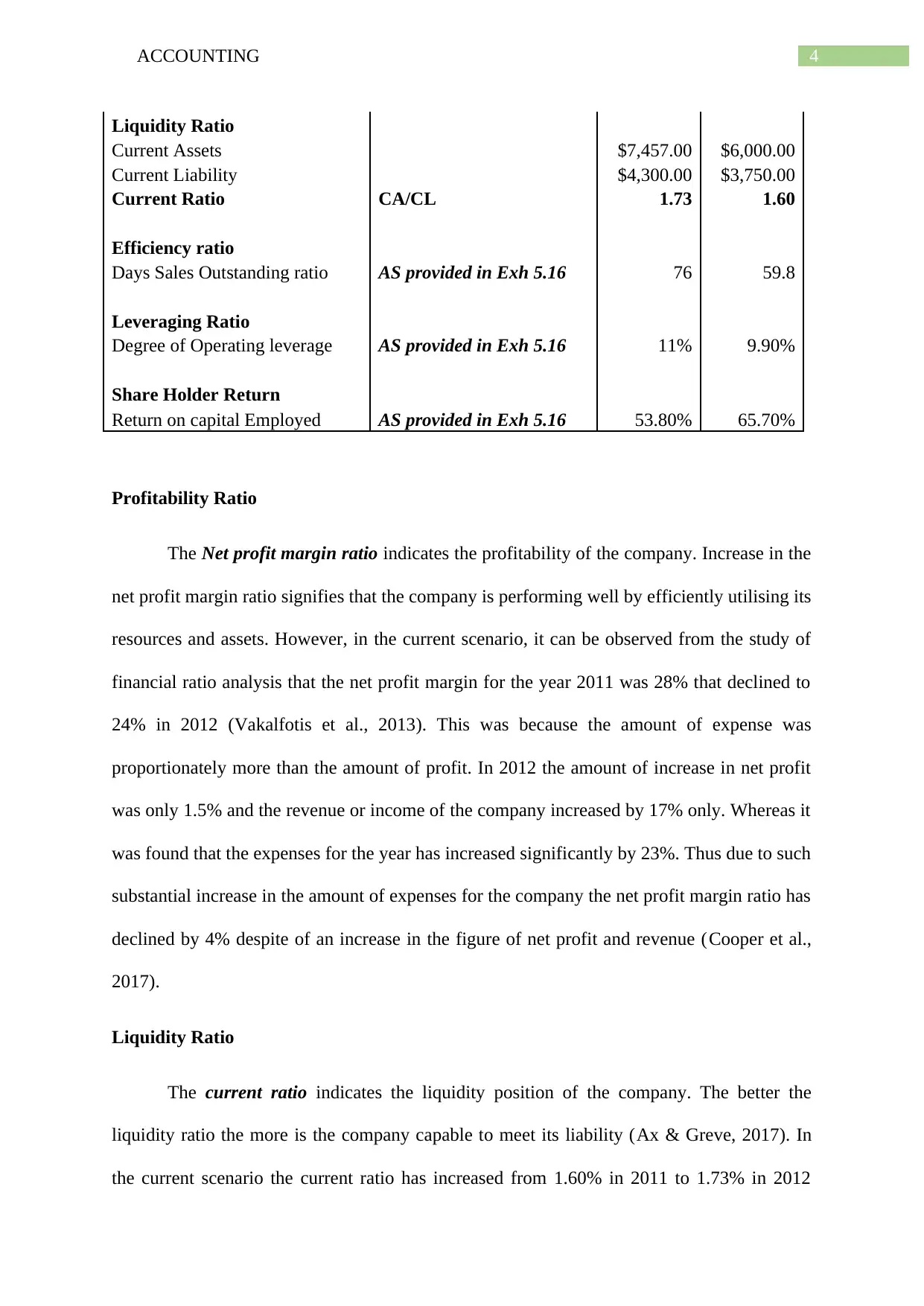

Liquidity Ratio

Current Assets $7,457.00 $6,000.00

Current Liability $4,300.00 $3,750.00

Current Ratio CA/CL 1.73 1.60

Efficiency ratio

Days Sales Outstanding ratio AS provided in Exh 5.16 76 59.8

Leveraging Ratio

Degree of Operating leverage AS provided in Exh 5.16 11% 9.90%

Share Holder Return

Return on capital Employed AS provided in Exh 5.16 53.80% 65.70%

Profitability Ratio

The Net profit margin ratio indicates the profitability of the company. Increase in the

net profit margin ratio signifies that the company is performing well by efficiently utilising its

resources and assets. However, in the current scenario, it can be observed from the study of

financial ratio analysis that the net profit margin for the year 2011 was 28% that declined to

24% in 2012 (Vakalfotis et al., 2013). This was because the amount of expense was

proportionately more than the amount of profit. In 2012 the amount of increase in net profit

was only 1.5% and the revenue or income of the company increased by 17% only. Whereas it

was found that the expenses for the year has increased significantly by 23%. Thus due to such

substantial increase in the amount of expenses for the company the net profit margin ratio has

declined by 4% despite of an increase in the figure of net profit and revenue (Cooper et al.,

2017).

Liquidity Ratio

The current ratio indicates the liquidity position of the company. The better the

liquidity ratio the more is the company capable to meet its liability (Ax & Greve, 2017). In

the current scenario the current ratio has increased from 1.60% in 2011 to 1.73% in 2012

Liquidity Ratio

Current Assets $7,457.00 $6,000.00

Current Liability $4,300.00 $3,750.00

Current Ratio CA/CL 1.73 1.60

Efficiency ratio

Days Sales Outstanding ratio AS provided in Exh 5.16 76 59.8

Leveraging Ratio

Degree of Operating leverage AS provided in Exh 5.16 11% 9.90%

Share Holder Return

Return on capital Employed AS provided in Exh 5.16 53.80% 65.70%

Profitability Ratio

The Net profit margin ratio indicates the profitability of the company. Increase in the

net profit margin ratio signifies that the company is performing well by efficiently utilising its

resources and assets. However, in the current scenario, it can be observed from the study of

financial ratio analysis that the net profit margin for the year 2011 was 28% that declined to

24% in 2012 (Vakalfotis et al., 2013). This was because the amount of expense was

proportionately more than the amount of profit. In 2012 the amount of increase in net profit

was only 1.5% and the revenue or income of the company increased by 17% only. Whereas it

was found that the expenses for the year has increased significantly by 23%. Thus due to such

substantial increase in the amount of expenses for the company the net profit margin ratio has

declined by 4% despite of an increase in the figure of net profit and revenue (Cooper et al.,

2017).

Liquidity Ratio

The current ratio indicates the liquidity position of the company. The better the

liquidity ratio the more is the company capable to meet its liability (Ax & Greve, 2017). In

the current scenario the current ratio has increased from 1.60% in 2011 to 1.73% in 2012

5ACCOUNTING

which means that it has increased by 8.125%. This is a good sign for the company and it

indicates that the company has sufficient liquidity (Messner et al., 2016).

Efficiency Ratio

The Efficiency ratio indicated how efficiently the company is able to utilise its assets

and liabilities internally to produce income. In the present situation, day’s sales outstanding

ratio has increased. This indicates that the collection of the efficiency department of the

company has declined (Tappura et al., 2015).

Leverage Ratio

On analysing the degree of operating leverage is concerned, it can be observed that it

has increased by 11.11% that is from 9.90% in 2011 to 11% in 2012. These suggest that the

company’s fixed cost is higher than its variable cost (Shields, 2015). This is not at all

considerable for the business and require immediate attention in order to bring down the

same.

Shareholders Return

As evident from the above analysis that the Return on Capital Employed has declined

by 18.11%. In 2011 ROCE was 65.70% which became 53.80% in 2012. The primary reason

is the decline in the net profit of the company the ROCE have also decreased drastically over

the period (Figge & Hahn, 2013).

which means that it has increased by 8.125%. This is a good sign for the company and it

indicates that the company has sufficient liquidity (Messner et al., 2016).

Efficiency Ratio

The Efficiency ratio indicated how efficiently the company is able to utilise its assets

and liabilities internally to produce income. In the present situation, day’s sales outstanding

ratio has increased. This indicates that the collection of the efficiency department of the

company has declined (Tappura et al., 2015).

Leverage Ratio

On analysing the degree of operating leverage is concerned, it can be observed that it

has increased by 11.11% that is from 9.90% in 2011 to 11% in 2012. These suggest that the

company’s fixed cost is higher than its variable cost (Shields, 2015). This is not at all

considerable for the business and require immediate attention in order to bring down the

same.

Shareholders Return

As evident from the above analysis that the Return on Capital Employed has declined

by 18.11%. In 2011 ROCE was 65.70% which became 53.80% in 2012. The primary reason

is the decline in the net profit of the company the ROCE have also decreased drastically over

the period (Figge & Hahn, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

Interpretation of ratios

P5.12

Answer to Question A:

When it comes to evaluating the performances of the business, ratio analysis plays an

essential role in it. With the help of various ratio analysis, the profitability, liquidity, solvency

and efficiency of the business can be gauged (Morales & Lambert, 2013). In order to measure

the performance of the business, it is very important to study the trend of those ratio over a

number of years. Through such study it can be understood whether they are improving or

declining over the time. For example, in order to measure the liquidity position of the

business, the current ratio is used. Similarly quick ratio can be used to evaluate the solvency

position. Again using the gross profit ratio, the profitability of the business can be analysed

(Alawattage et al., 2017).

Answer to Question B:

On analysing the ratio of Ratunga Inc. for the past 4 years it can be observed that the

business have shown its strengths in terms of sales, return on investment, profitability,

leverage, asset utilization, wealth of the shareholders, etc (Alawattage et al., 2017 ). This can

be proved by studying several ratios such as the sales ratio in 2009 was 7% which increased

to 10.0% in 2012. This indicates that the sales for the business have increased compared to

the previous year as a result of which there were considerable increase in profit for the

Interpretation of ratios

P5.12

Answer to Question A:

When it comes to evaluating the performances of the business, ratio analysis plays an

essential role in it. With the help of various ratio analysis, the profitability, liquidity, solvency

and efficiency of the business can be gauged (Morales & Lambert, 2013). In order to measure

the performance of the business, it is very important to study the trend of those ratio over a

number of years. Through such study it can be understood whether they are improving or

declining over the time. For example, in order to measure the liquidity position of the

business, the current ratio is used. Similarly quick ratio can be used to evaluate the solvency

position. Again using the gross profit ratio, the profitability of the business can be analysed

(Alawattage et al., 2017).

Answer to Question B:

On analysing the ratio of Ratunga Inc. for the past 4 years it can be observed that the

business have shown its strengths in terms of sales, return on investment, profitability,

leverage, asset utilization, wealth of the shareholders, etc (Alawattage et al., 2017 ). This can

be proved by studying several ratios such as the sales ratio in 2009 was 7% which increased

to 10.0% in 2012. This indicates that the sales for the business have increased compared to

the previous year as a result of which there were considerable increase in profit for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

business as well. As it can be observed from the gross profit ratio, which was 28.0% in 2012

that profit have increased by 9.4% in the year 2012. Also the company was able to provide

fair return on its investments (Fourie et al., 2015). The return on investment for the company

have also increased from 4.1% in 2009 to 5.0% in 2012. This ensures that the company have

utilised its resources in appropriate area in order to earn the desired return. Similarly the

company was also able to generate decent revenue by utilizing its asset due to which the

Asset turnover ratio have also increased. Most importantly, the price/earnings ratio of the

business have increased which signifies that there are higher potential of the company to

generate higher revenue and growth in future (Järvinen 2016).

However, the key weakness of the business as it can be studied from the ratio analysis

is that the return on capital employed for the business is declining over the years and as a

result of which the operating profit is also showing a decent fall (Armitage et al., 2016). In

addition to this the interest cover is also showing negative results over the years. More

importantly from the quick ratio of the business it can be observed that the company is losing

its potential to meet the short term obligation as there were significant fall in its quick ratio

and it is a substantial threat to the business and requires immediate attention (Klychova et al.,

2014).

business as well. As it can be observed from the gross profit ratio, which was 28.0% in 2012

that profit have increased by 9.4% in the year 2012. Also the company was able to provide

fair return on its investments (Fourie et al., 2015). The return on investment for the company

have also increased from 4.1% in 2009 to 5.0% in 2012. This ensures that the company have

utilised its resources in appropriate area in order to earn the desired return. Similarly the

company was also able to generate decent revenue by utilizing its asset due to which the

Asset turnover ratio have also increased. Most importantly, the price/earnings ratio of the

business have increased which signifies that there are higher potential of the company to

generate higher revenue and growth in future (Järvinen 2016).

However, the key weakness of the business as it can be studied from the ratio analysis

is that the return on capital employed for the business is declining over the years and as a

result of which the operating profit is also showing a decent fall (Armitage et al., 2016). In

addition to this the interest cover is also showing negative results over the years. More

importantly from the quick ratio of the business it can be observed that the company is losing

its potential to meet the short term obligation as there were significant fall in its quick ratio

and it is a substantial threat to the business and requires immediate attention (Klychova et al.,

2014).

8ACCOUNTING

Reference

Alawattage, C., Wickramasinghe, D., & Uddin, S. (2017). Theorising management

accounting practices in Less Developed Countries. The Routledge Companion to

Performance Management and Control.

Armitage, H. M., Webb, A., & Glynn, J. (2016). The Use of Management Accounting

Techniques by Small and Medium‐Sized Enterprises: A Field Study of Canadian and

Australian Practice. Accounting Perspectives, 15(1), 31-69.

Ax, C., & Greve, J. (2017). Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34, 59-74.

Cooper, D. J., Ezzamel, M., & Qu, S. Q. (2017). Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research.

Figge, F., & Hahn, T. (2013). Value drivers of corporate eco-efficiency: Management

accounting information for the efficient use of environmental resources. Management

Accounting Research, 24(4), 387-400.

Fourie, M. L., Opperman, L., Scott, D., & Kumar, K. (2015). Municipal finance and

accounting. Van Schaik Publishers.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), 414-428.

Järvinen, J. T. (2016). Role of management accounting in applying new institutional logics:

A comparative case study in the non-profit sector. Accounting, Auditing & Accountability

Journal, 29(5), 861-886.

Reference

Alawattage, C., Wickramasinghe, D., & Uddin, S. (2017). Theorising management

accounting practices in Less Developed Countries. The Routledge Companion to

Performance Management and Control.

Armitage, H. M., Webb, A., & Glynn, J. (2016). The Use of Management Accounting

Techniques by Small and Medium‐Sized Enterprises: A Field Study of Canadian and

Australian Practice. Accounting Perspectives, 15(1), 31-69.

Ax, C., & Greve, J. (2017). Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34, 59-74.

Cooper, D. J., Ezzamel, M., & Qu, S. Q. (2017). Popularizing a management accounting idea:

The case of the balanced scorecard. Contemporary Accounting Research.

Figge, F., & Hahn, T. (2013). Value drivers of corporate eco-efficiency: Management

accounting information for the efficient use of environmental resources. Management

Accounting Research, 24(4), 387-400.

Fourie, M. L., Opperman, L., Scott, D., & Kumar, K. (2015). Municipal finance and

accounting. Van Schaik Publishers.

Fullerton, R. R., Kennedy, F. A., & Widener, S. K. (2014). Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), 414-428.

Järvinen, J. T. (2016). Role of management accounting in applying new institutional logics:

A comparative case study in the non-profit sector. Accounting, Auditing & Accountability

Journal, 29(5), 861-886.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Messner, M., Becker, A., Schäffer, U., & Binder, C. (2016). Struggles for legitimacy and

identity: the development of Germanic management accounting research. Research Gate, 1-

38.

Morales, J., & Lambert, C. (2013). Dirty work and the construction of identity. An

ethnographic study of management accounting practices. Accounting, Organizations and

Society, 38(3), 228-244.

Otley, D., & Emmanuel, K. M. C. (2013). Readings in accounting for management control.

Springer.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Shields, M. D. (2015). Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), 123-132.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A., & Nenonen, N. (2015). A management

accounting perspective on safety. Safety science, 71, 151-159.

Vakalfotis, N., Ballantine, J., & Wall, A. P. (2013). A literature review on the impact of

Enterprise Systems on management accounting.

Klychova, G. S., Faskhutdinova, М. S., & Sadrieva, E. R. (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), 79.

Messner, M., Becker, A., Schäffer, U., & Binder, C. (2016). Struggles for legitimacy and

identity: the development of Germanic management accounting research. Research Gate, 1-

38.

Morales, J., & Lambert, C. (2013). Dirty work and the construction of identity. An

ethnographic study of management accounting practices. Accounting, Organizations and

Society, 38(3), 228-244.

Otley, D., & Emmanuel, K. M. C. (2013). Readings in accounting for management control.

Springer.

Renz, D. O. (2016). The Jossey-Bass handbook of nonprofit leadership and management.

John Wiley & Sons.

Shields, M. D. (2015). Established management accounting knowledge. Journal of

Management Accounting Research, 27(1), 123-132.

Tappura, S., Sievänen, M., Heikkilä, J., Jussila, A., & Nenonen, N. (2015). A management

accounting perspective on safety. Safety science, 71, 151-159.

Vakalfotis, N., Ballantine, J., & Wall, A. P. (2013). A literature review on the impact of

Enterprise Systems on management accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.