Analysis of Wave's Final Accounts and ITV's Revenue Recognition

VerifiedAdded on 2023/01/12

|18

|2634

|47

Homework Assignment

AI Summary

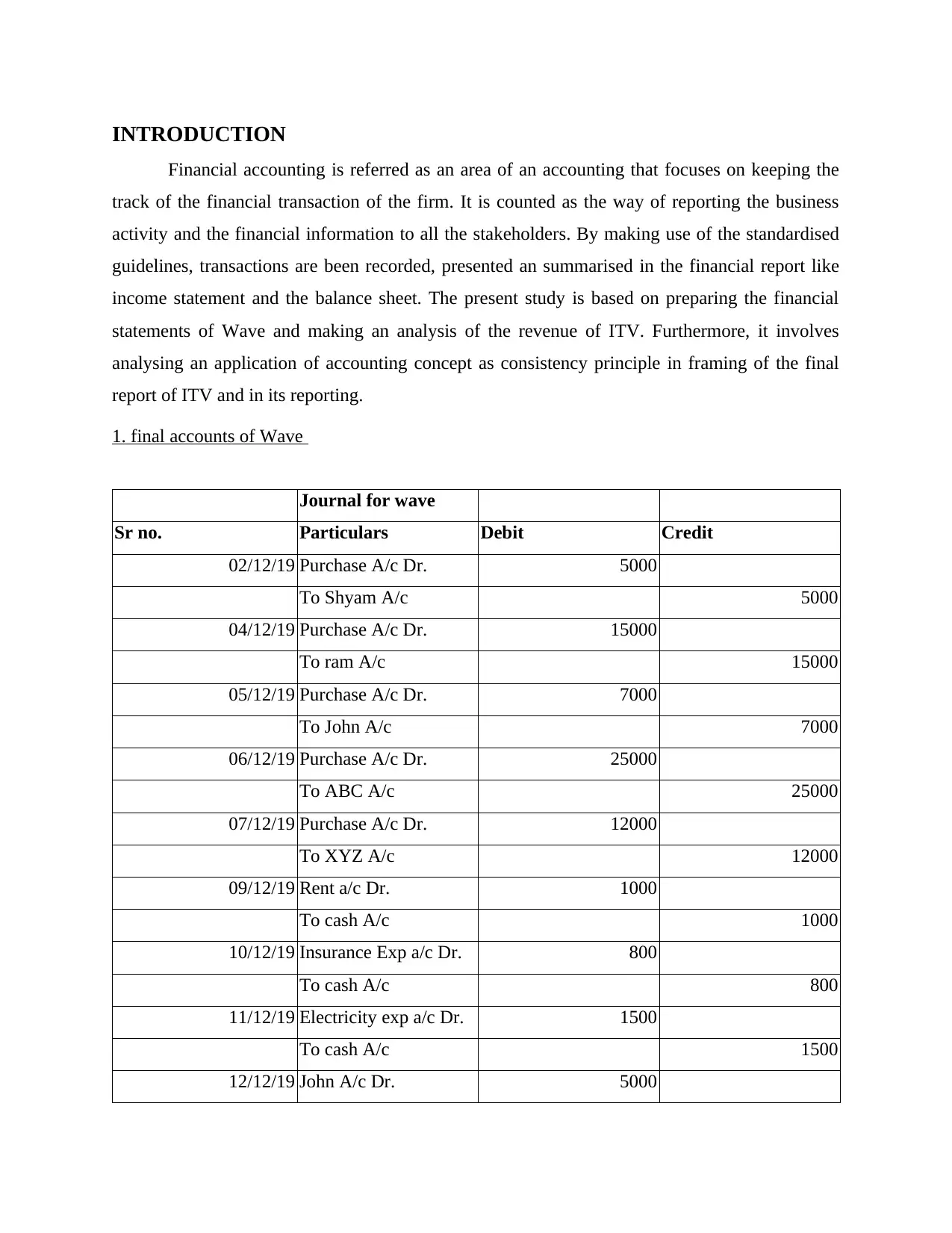

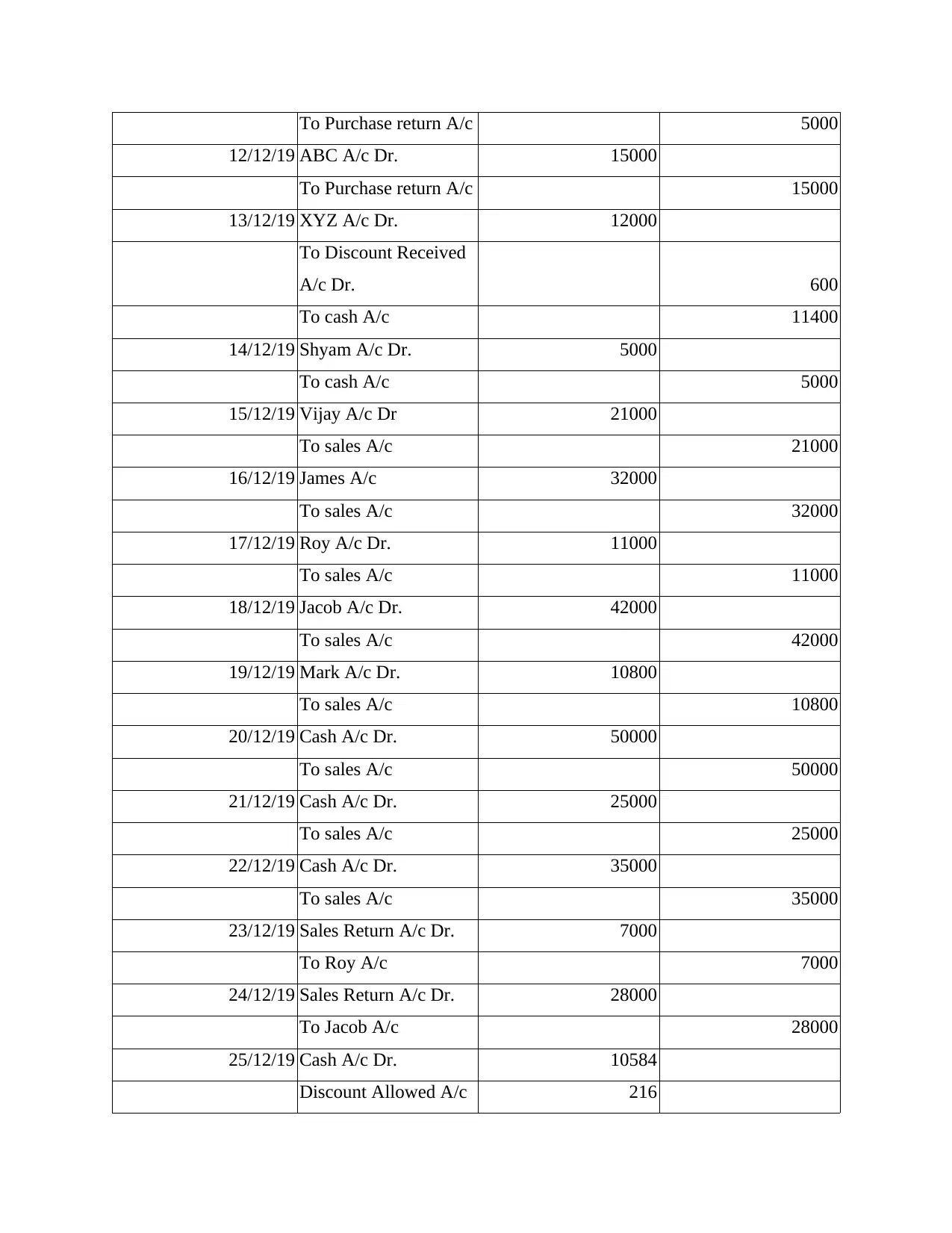

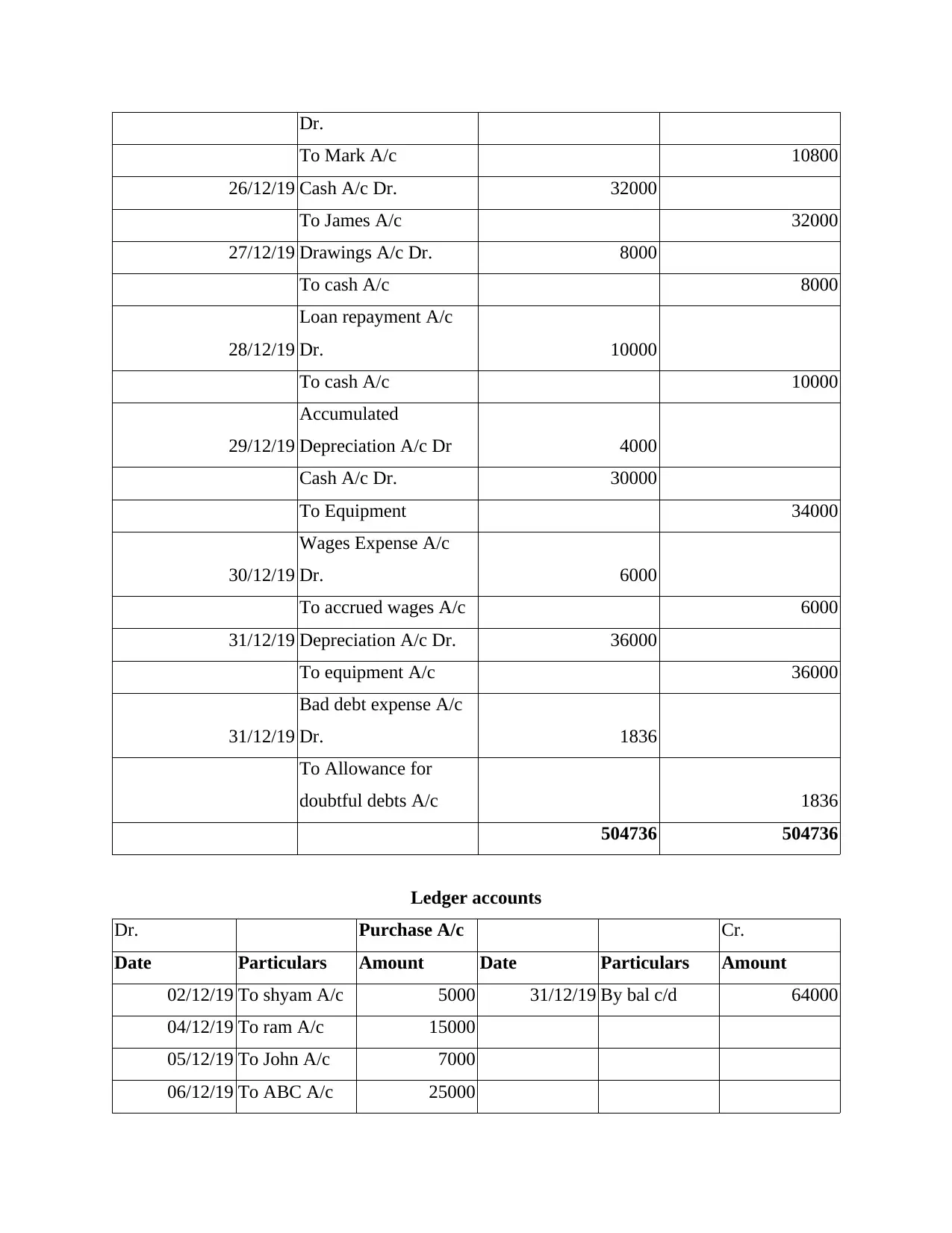

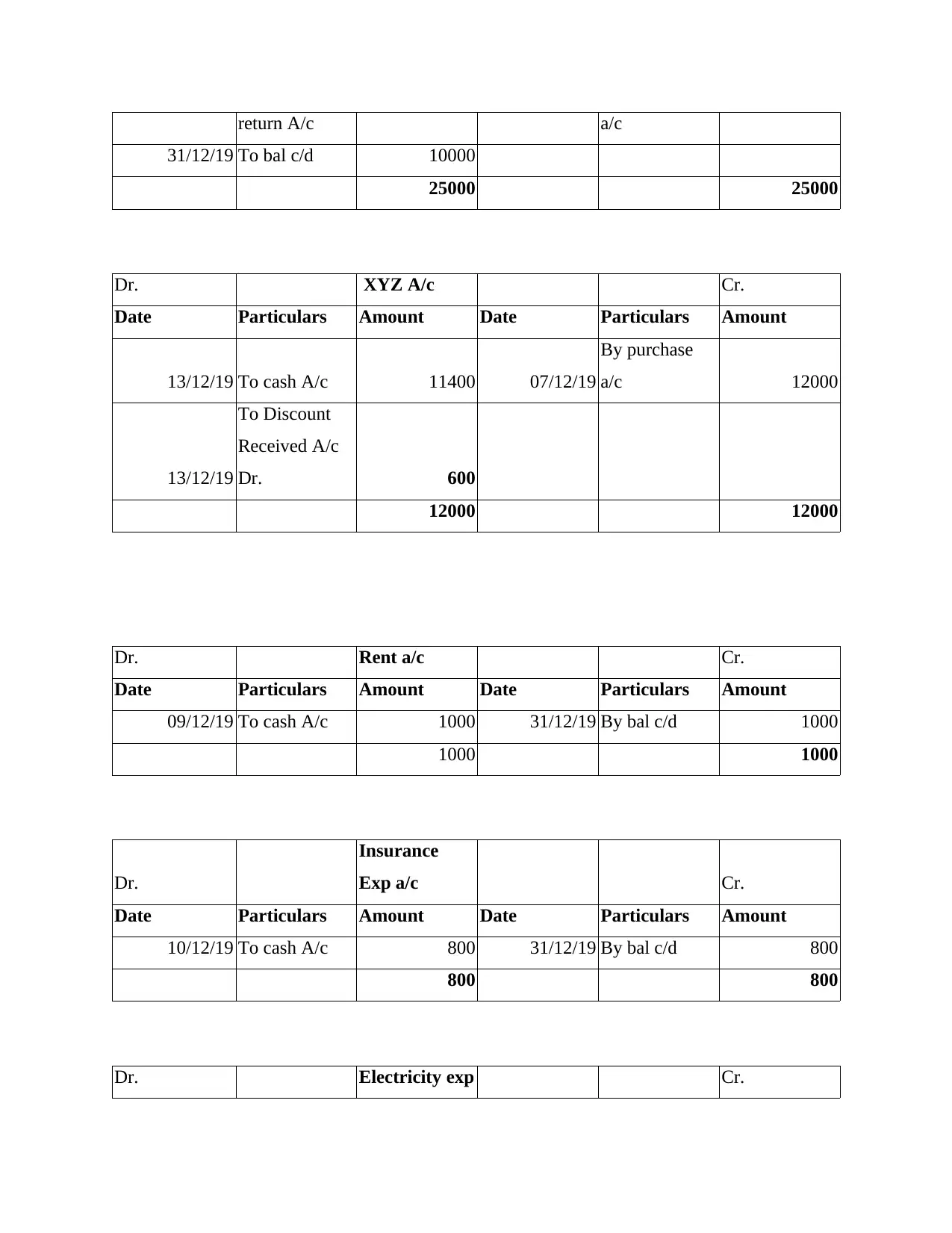

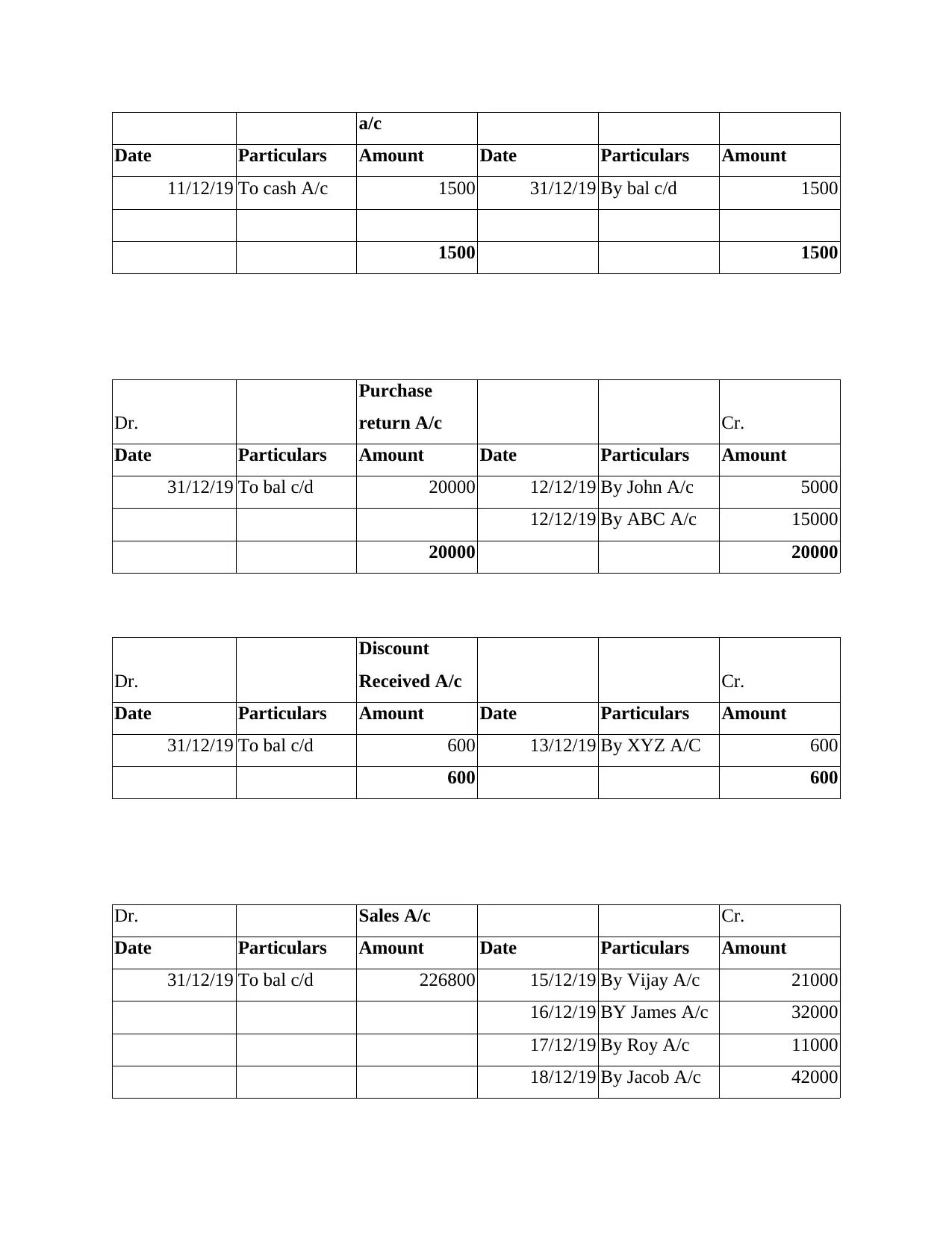

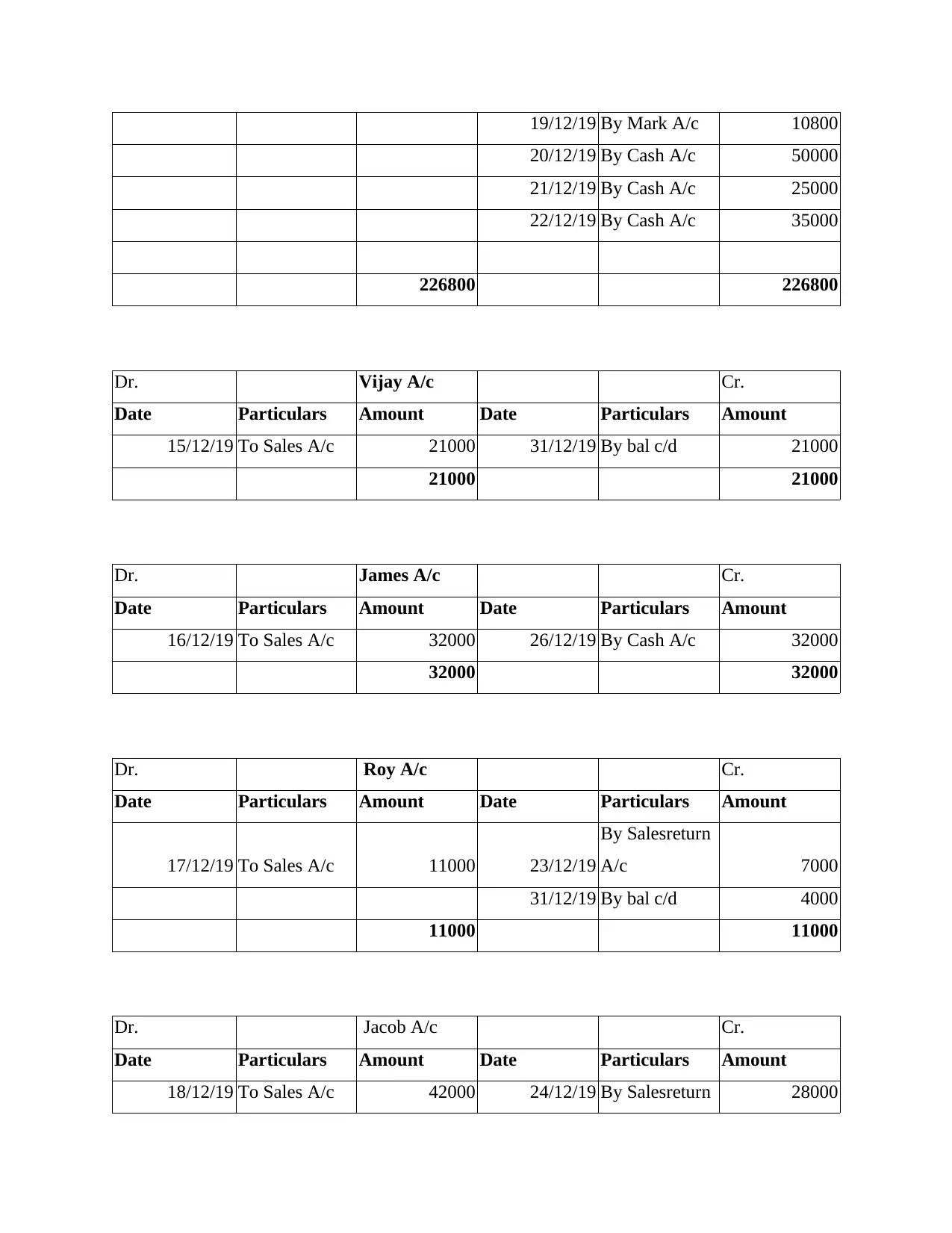

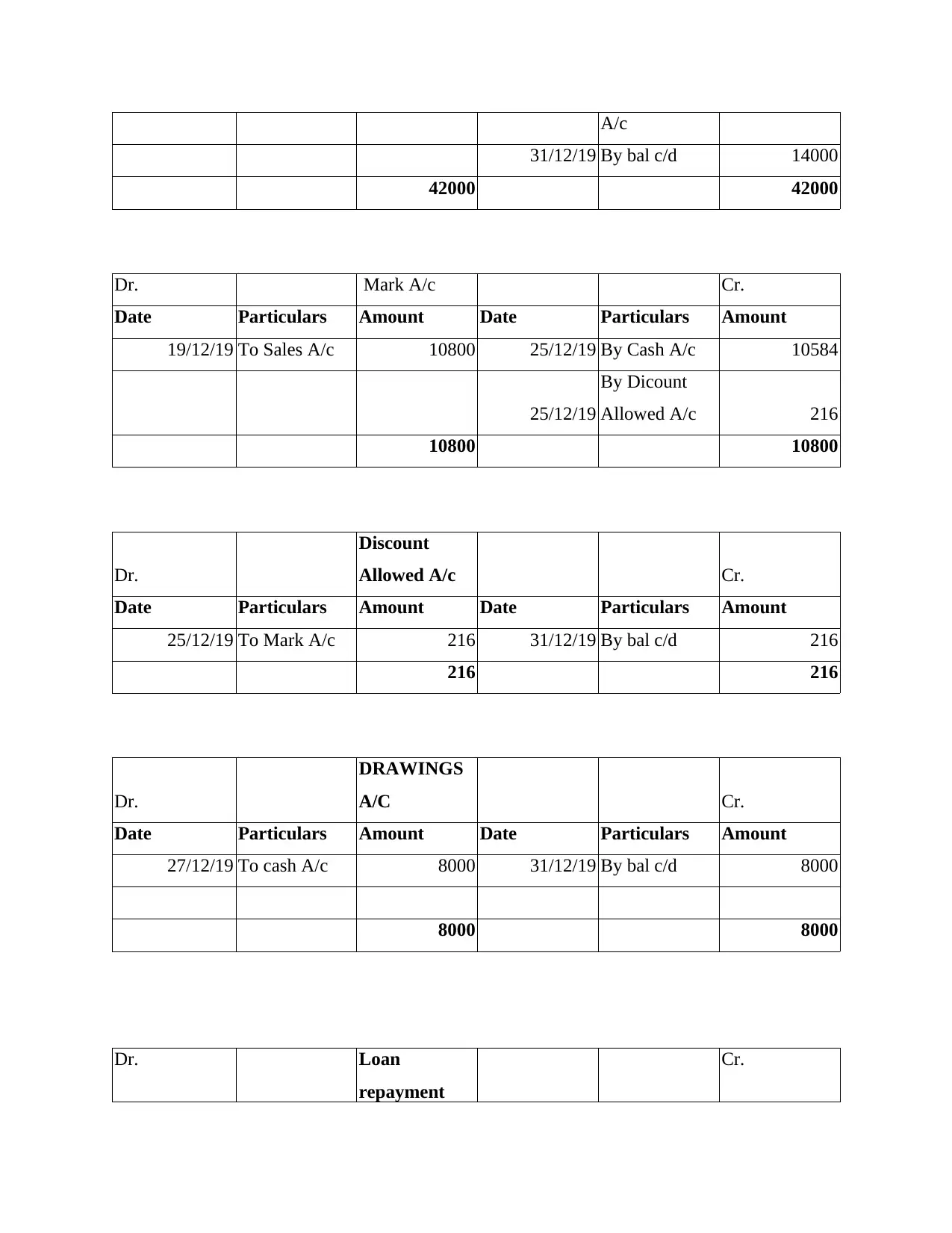

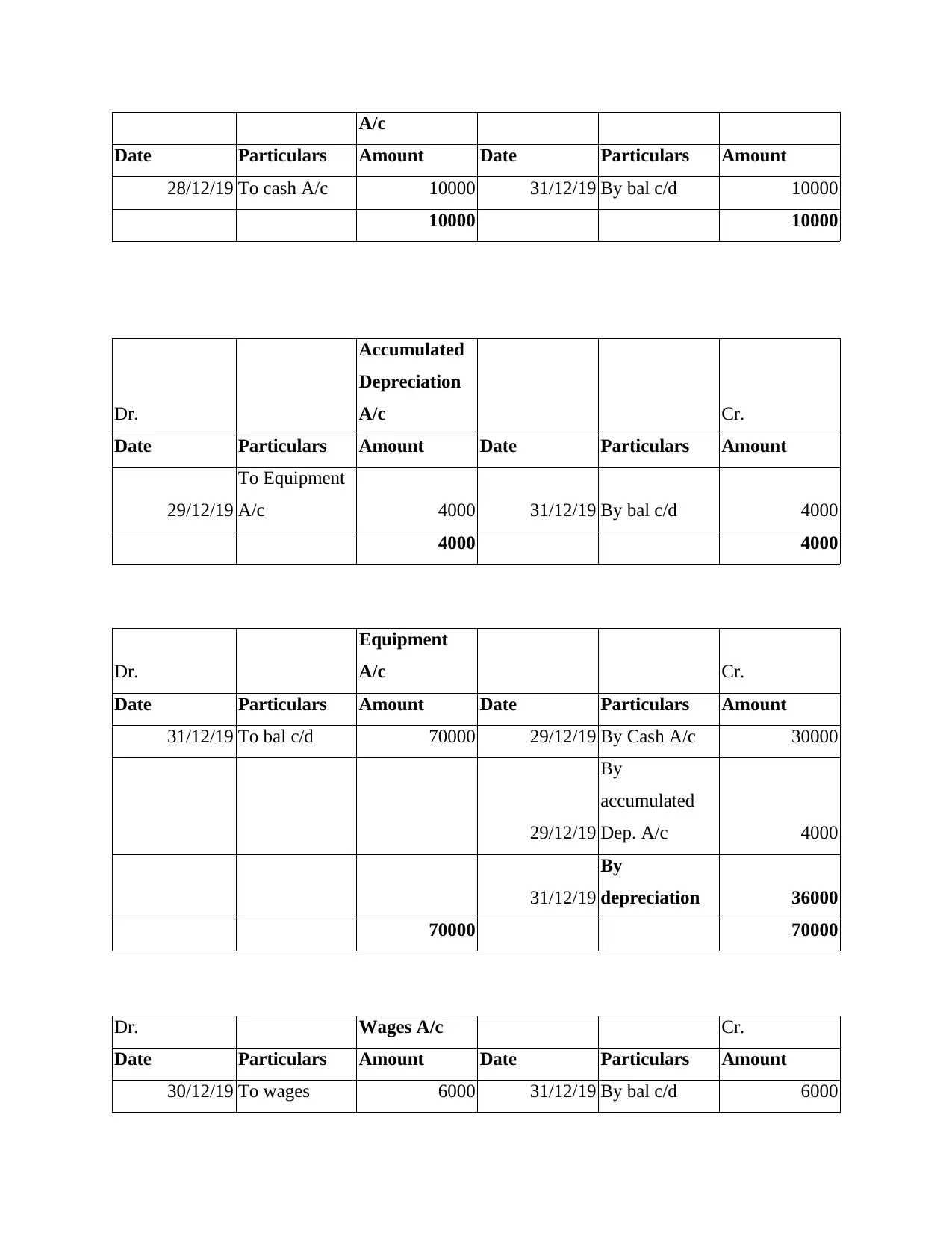

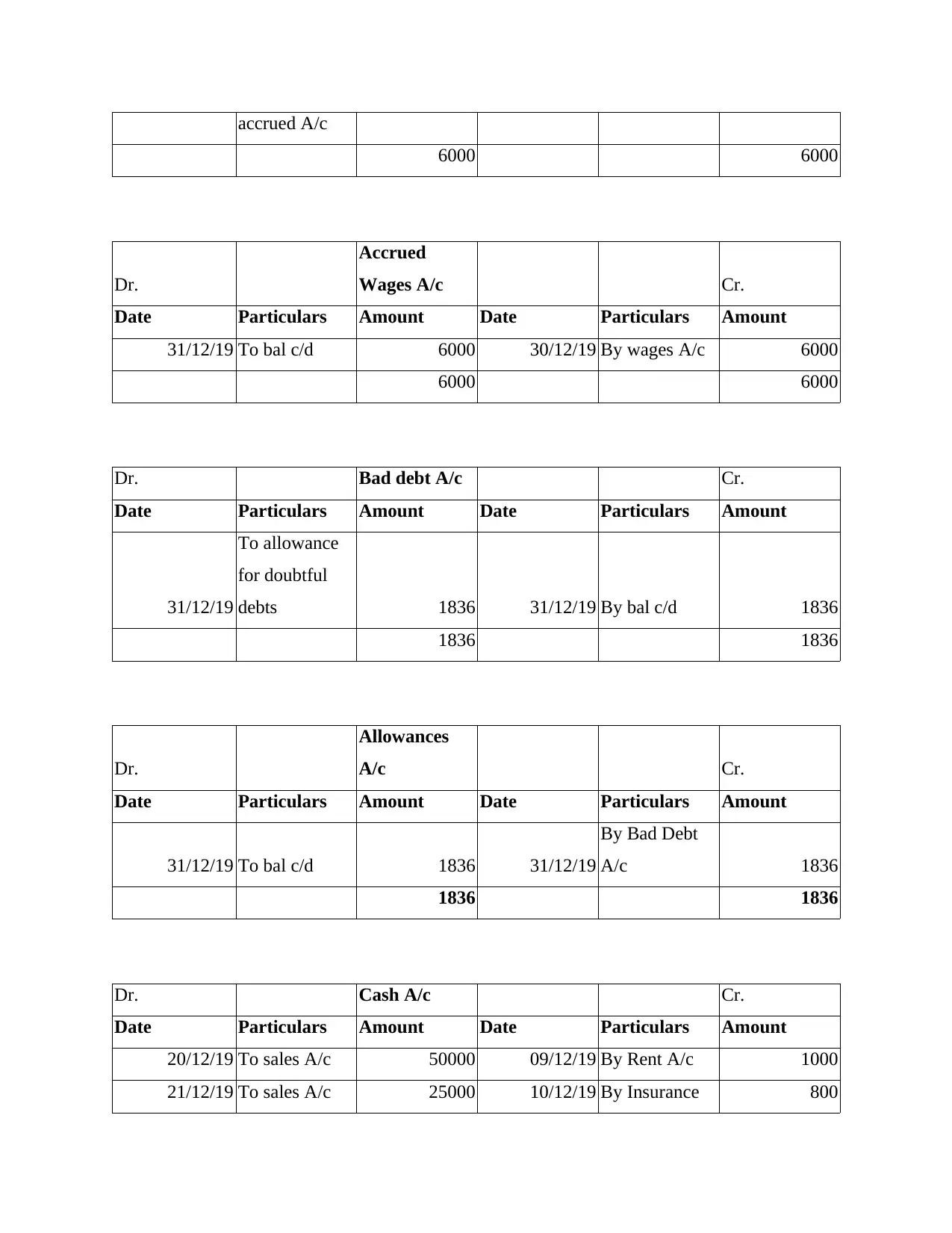

This document presents a comprehensive financial accounting assignment solution. It begins with the preparation of Wave's final accounts, including journal entries, ledgers, and a trial balance, providing a detailed view of its financial transactions. The assignment then delves into the analysis of revenue recognition, specifically focusing on ITV's revenue streams and how they are recognized based on the delivery of performance obligations. Furthermore, it explores the application of the consistency principle in accounting, examining how ITV applies this principle in its financial reporting, particularly concerning the valuation of assets and the presentation of financial statements. The assignment offers insights into financial statement analysis, accounting principles, and revenue recognition practices.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.