Accounting for Managers: Pacific Telemet Ltd Profitability Report

VerifiedAdded on 2023/04/23

|10

|998

|160

Report

AI Summary

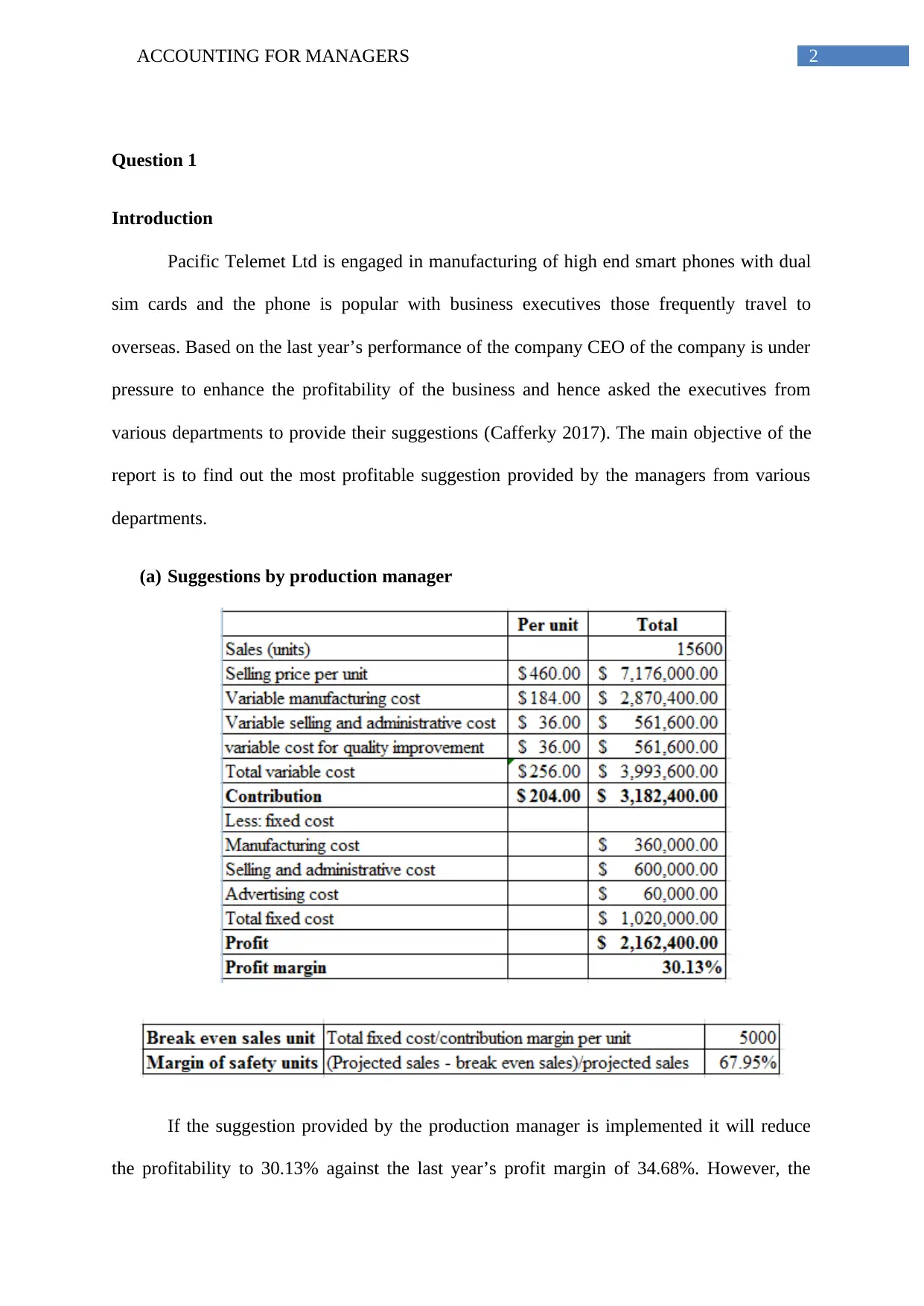

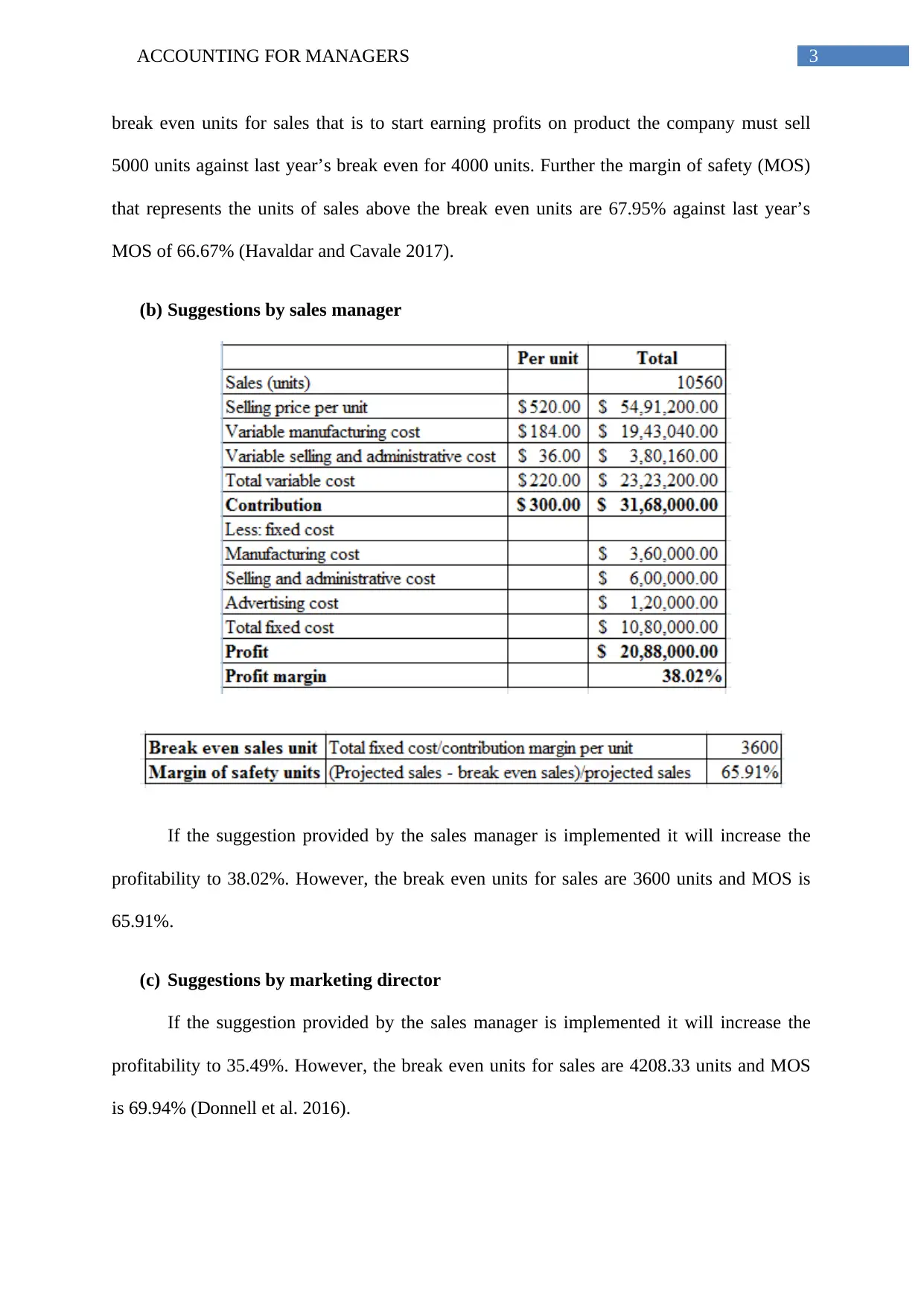

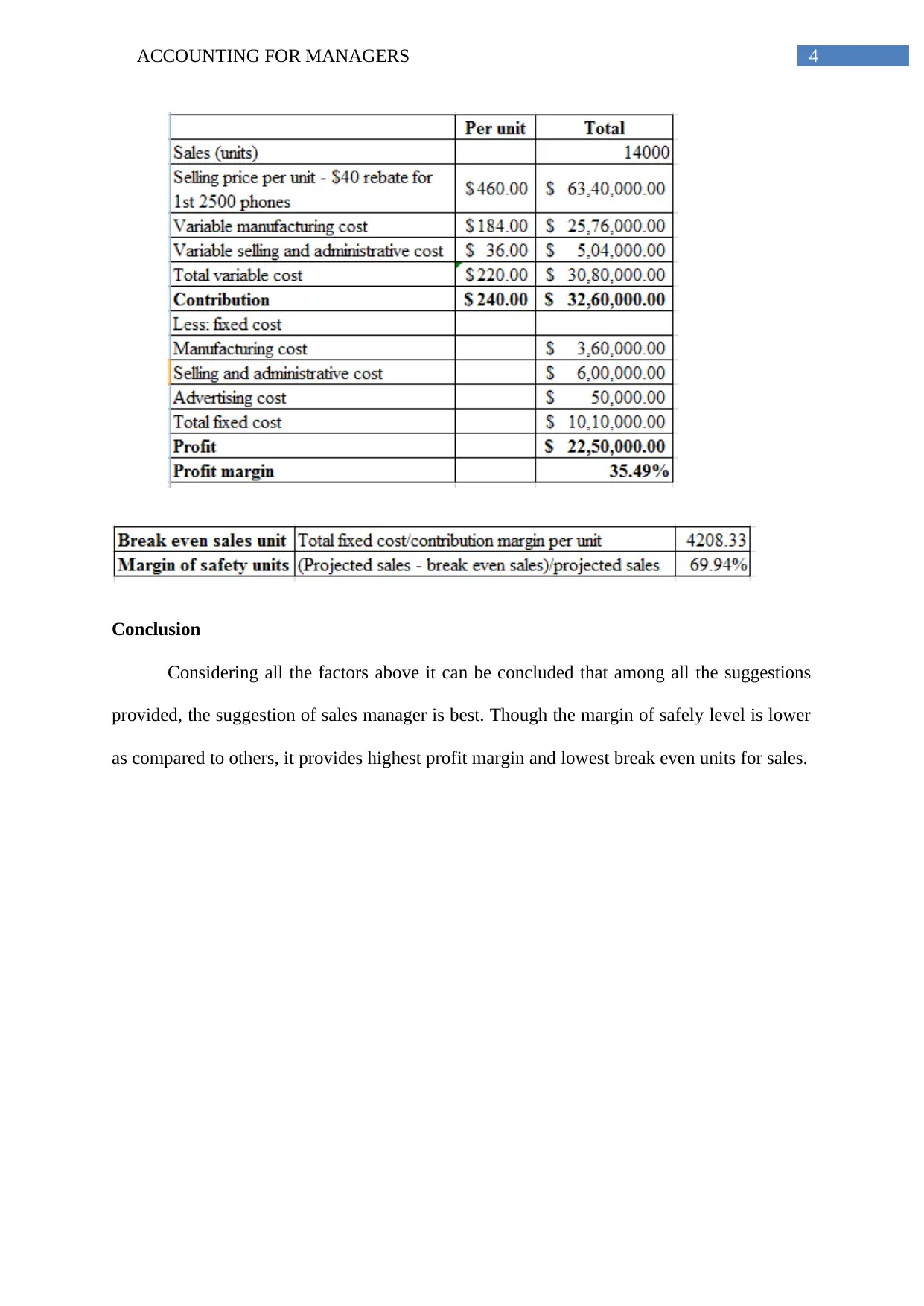

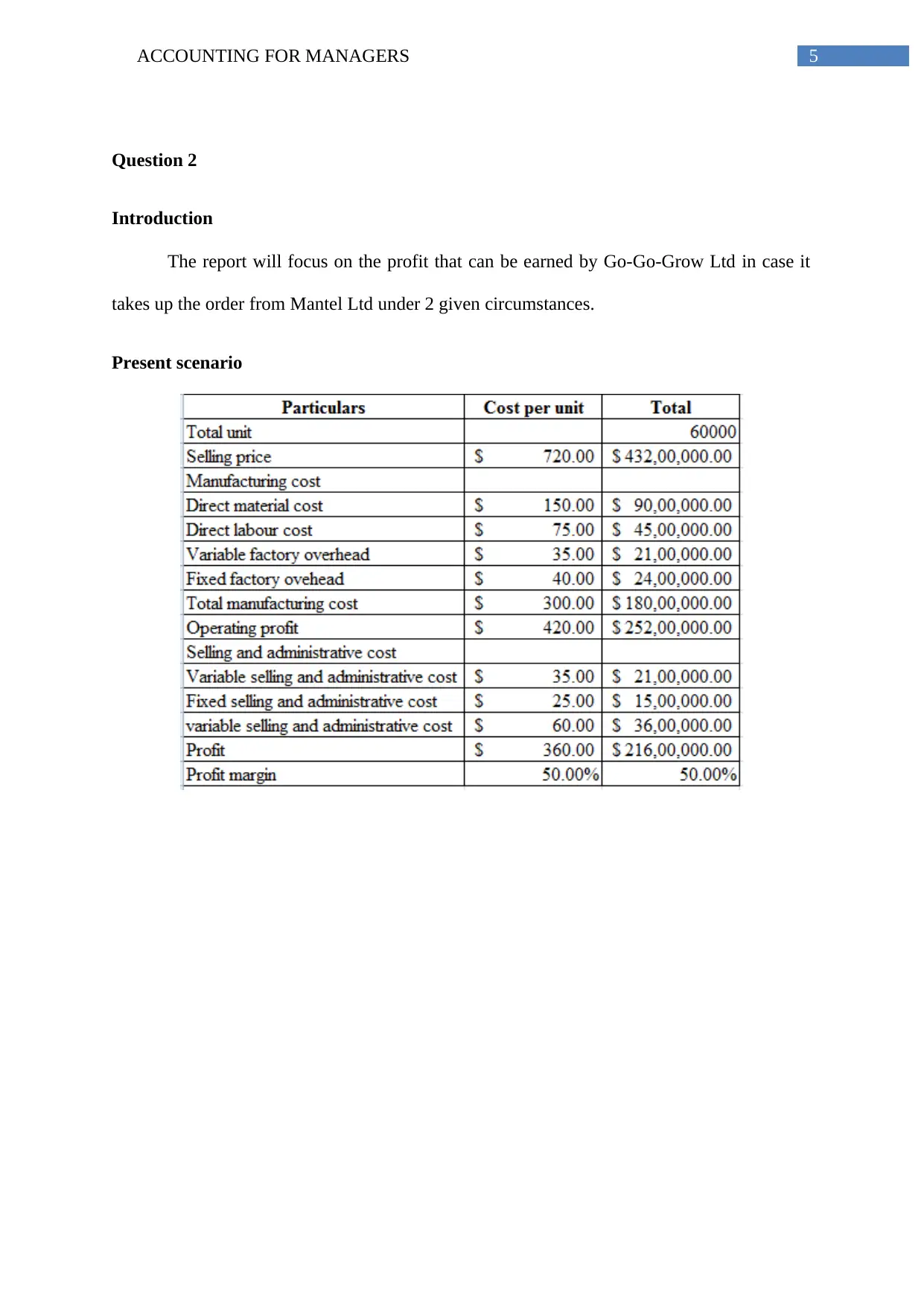

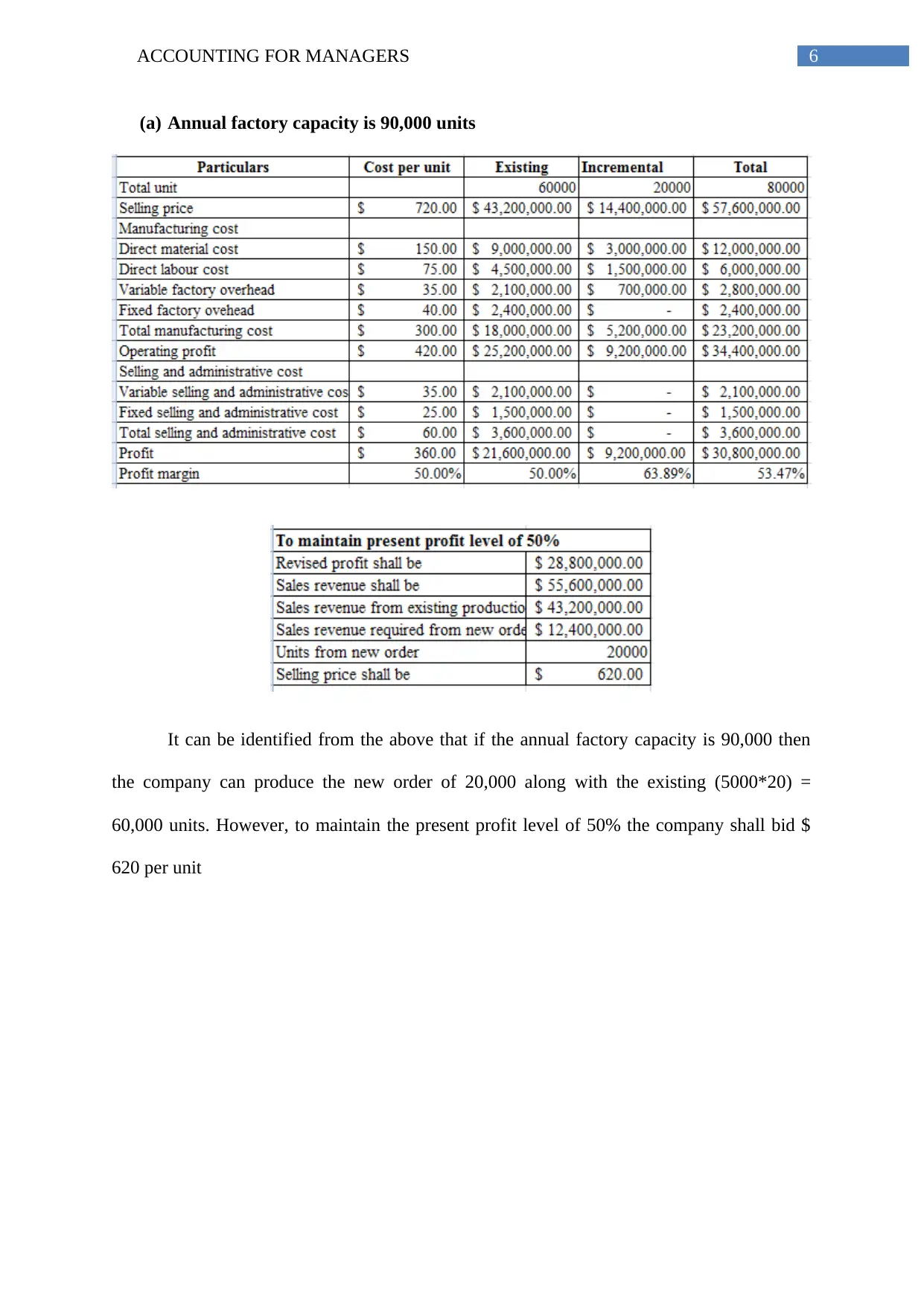

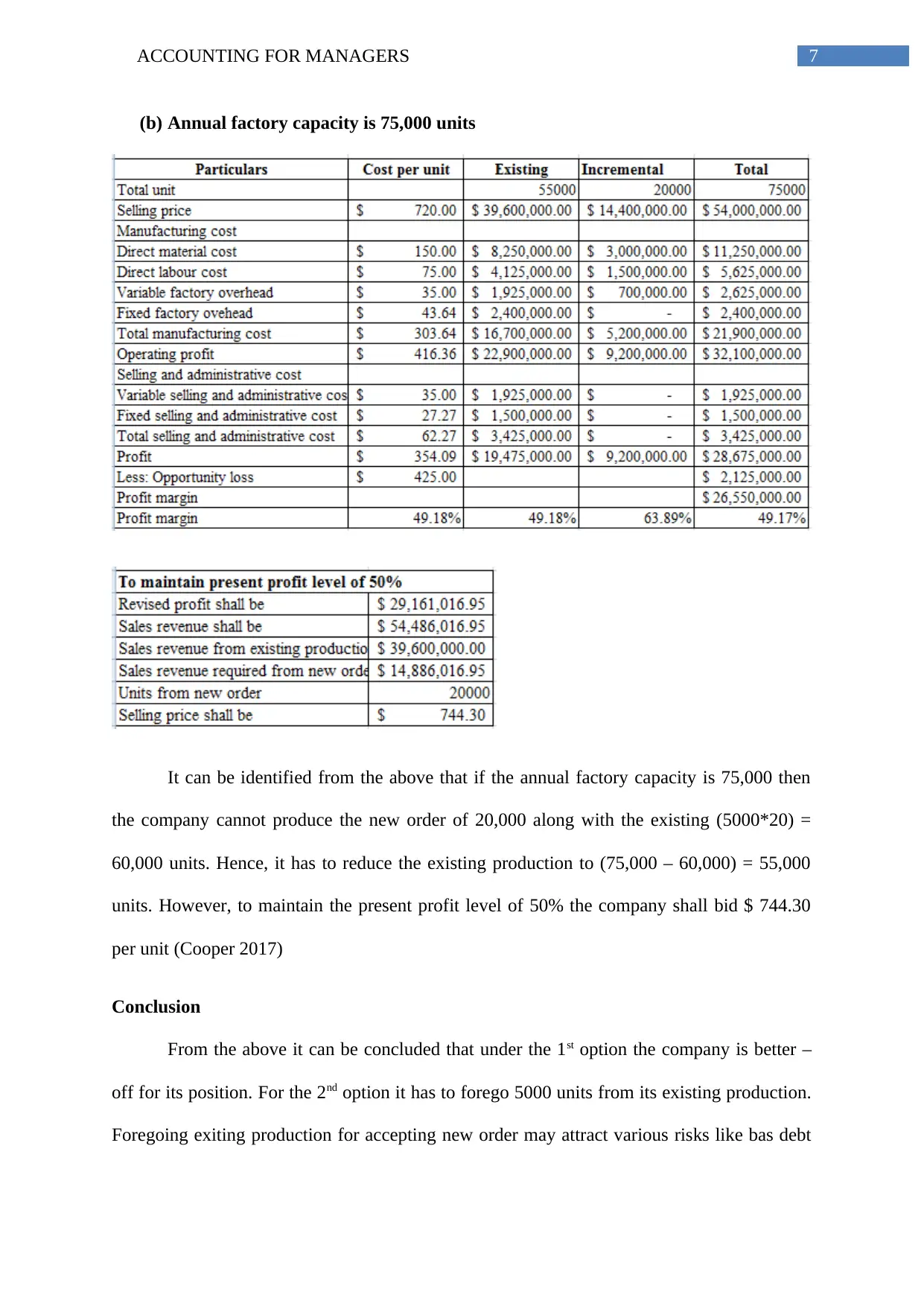

This report analyzes the profitability of Pacific Telemet Ltd, a manufacturer of high-end smartphones. The assignment, focused on ACC00724 (Accounting for Managers), evaluates suggestions from the production, sales, and marketing departments to improve profitability. The report calculates profit margins, break-even points, and margin of safety under different scenarios, comparing the financial impact of each suggestion. The analysis includes the impact of increased advertising, quality improvements, and production capacity on the company's financial performance. Furthermore, the report assesses the profitability of a potential order from Mantel Ltd, considering different factory capacity levels and their effects on pricing and production decisions. Finally, the report includes a reflection on the student's learning experience and the usefulness of Excel spreadsheets in financial accounting. The report concludes that the sales manager's suggestion is the best among all the suggestions provided.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.