Accounting for Business: Financial Statement Analysis Assignment

VerifiedAdded on 2023/01/11

|8

|1035

|57

Homework Assignment

AI Summary

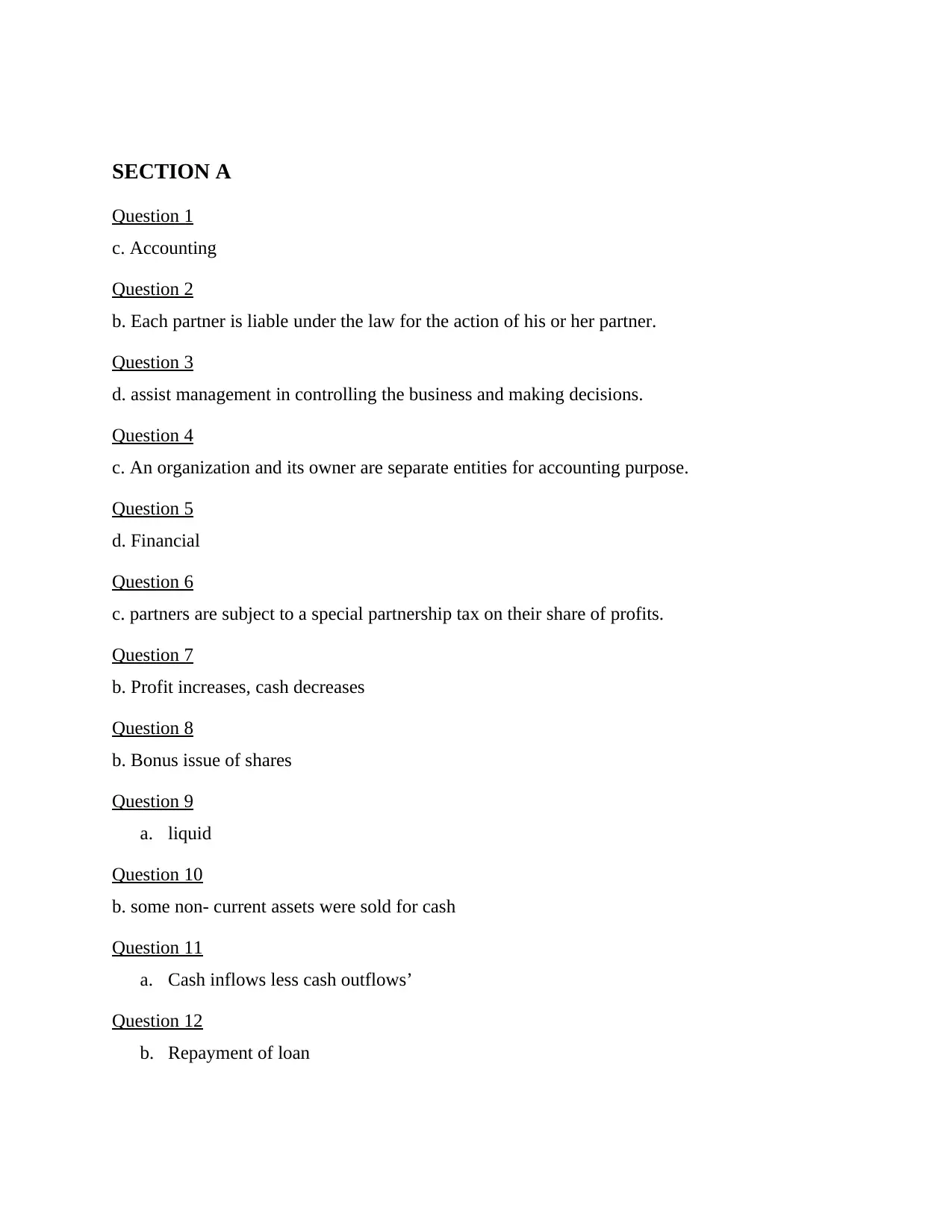

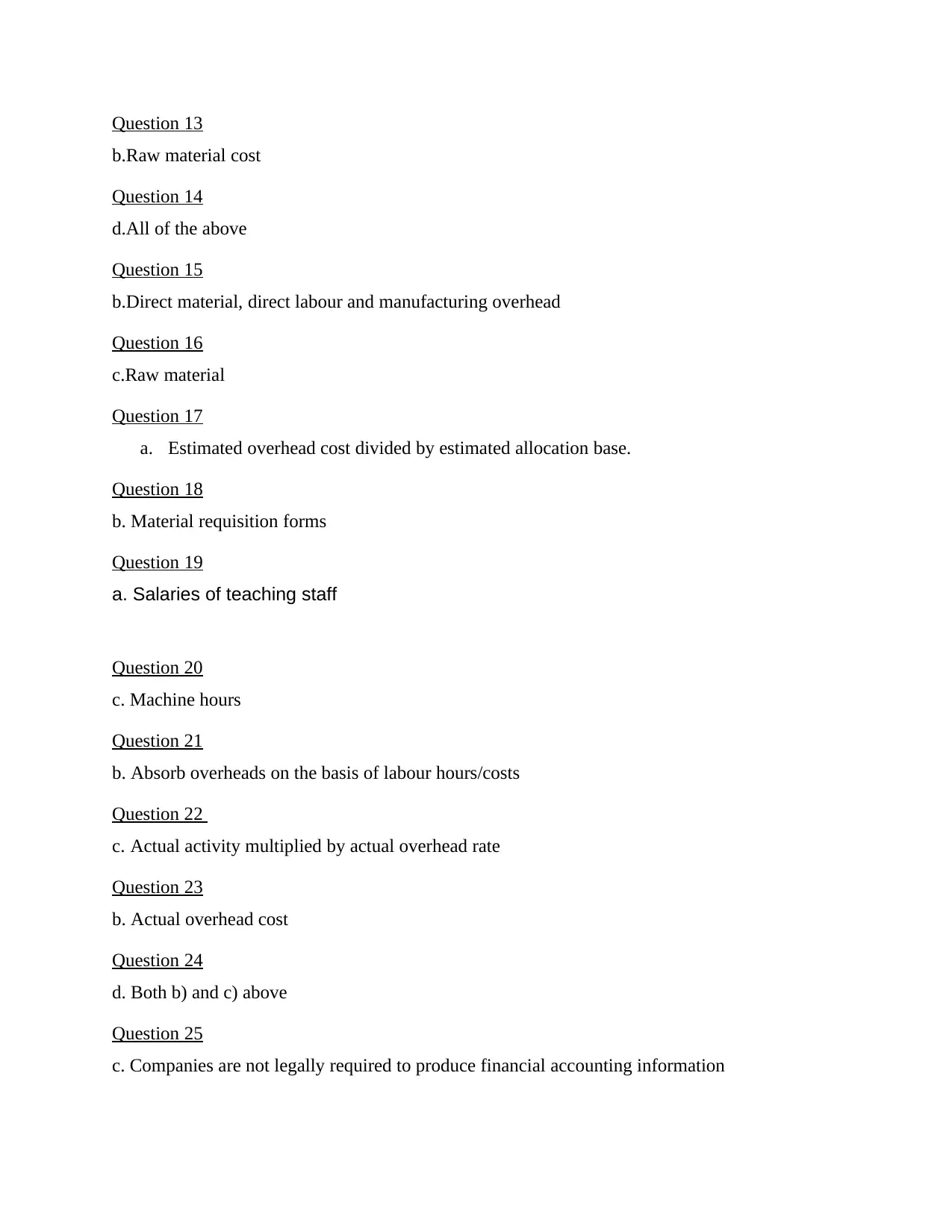

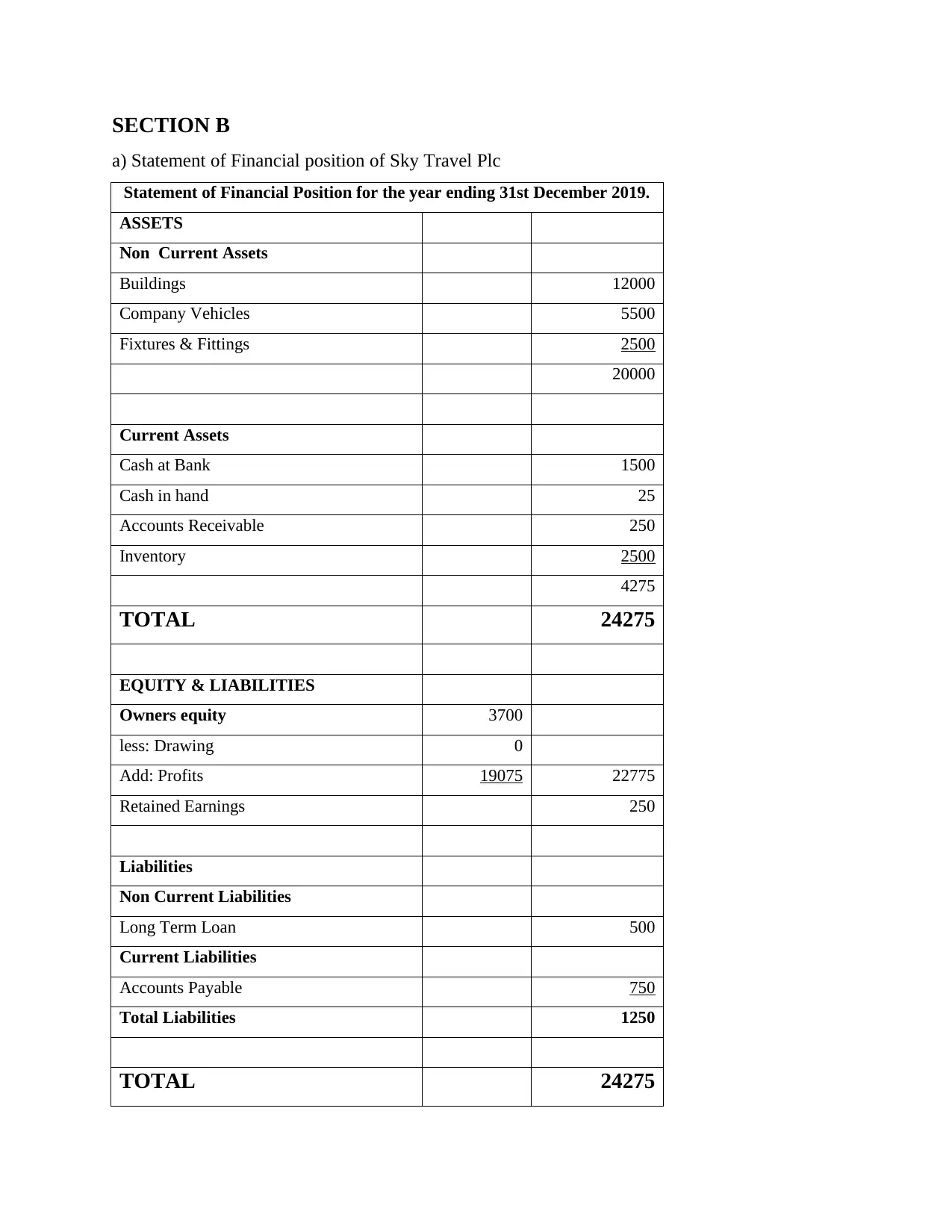

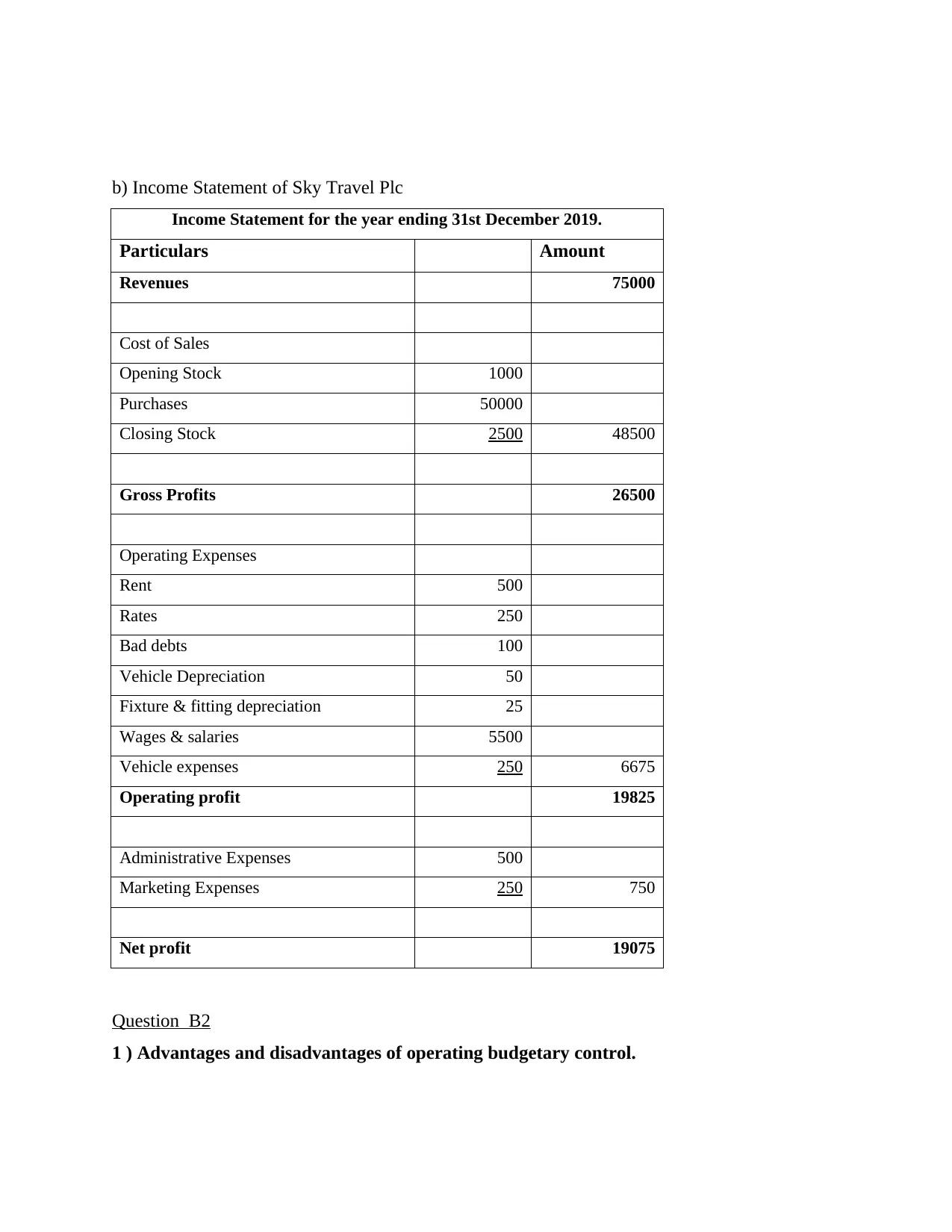

This accounting assignment solution covers various aspects of accounting for business, including multiple-choice questions in Section A and problem-solving in Section B. Section A tests understanding of fundamental accounting concepts such as partnerships, financial statements, cost accounting, and budgeting. Section B presents a statement of financial position and income statement for Sky Travel Plc, followed by questions on operating budgetary control, master budgets, annual budgets, rolling budgets, fixed budgets, and flexible budgets. The solution provides detailed answers and explanations for each question, making it a valuable resource for students studying accounting principles and financial statement analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.