Accounting Report: Journal Entries, Financial Statements Analysis

VerifiedAdded on 2021/01/02

|12

|2678

|61

Homework Assignment

AI Summary

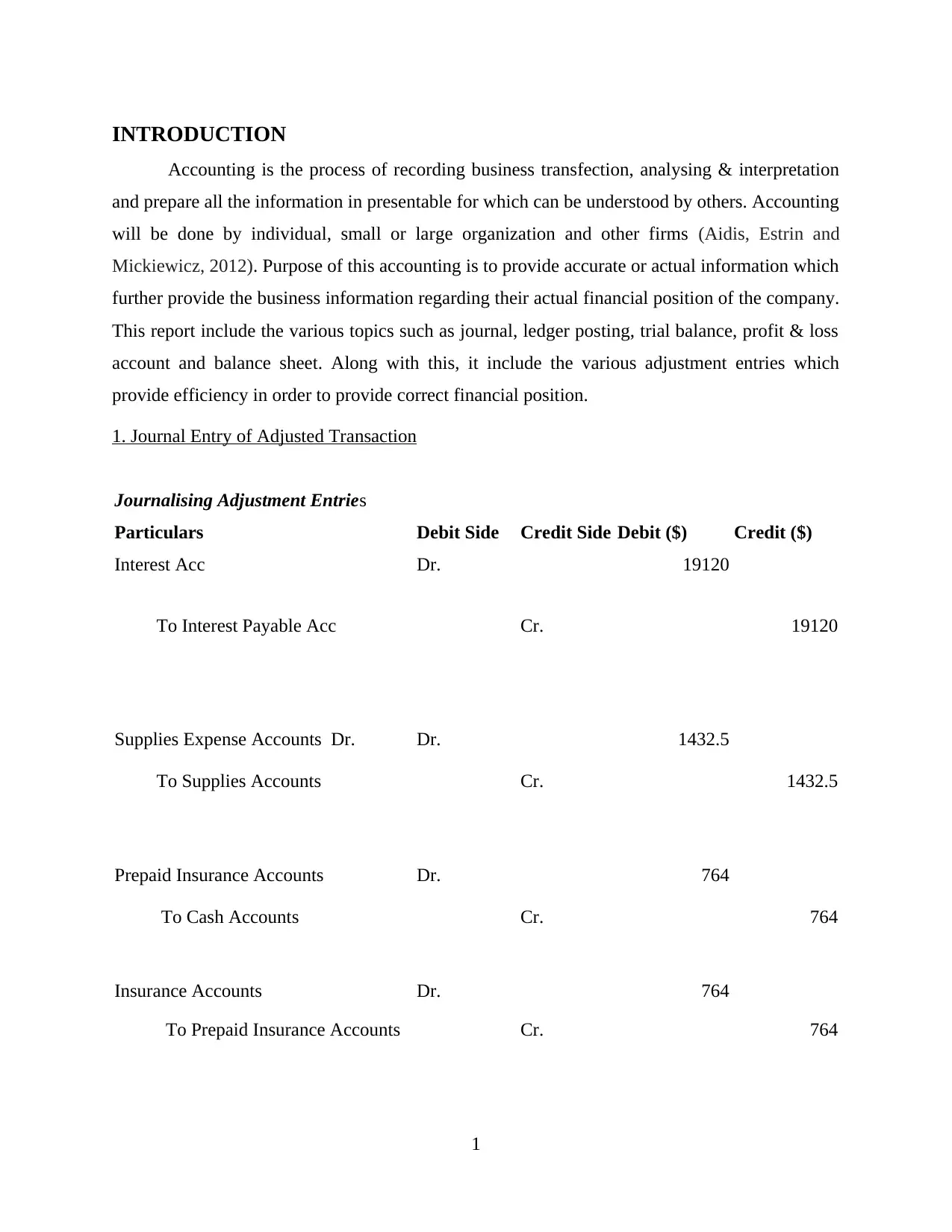

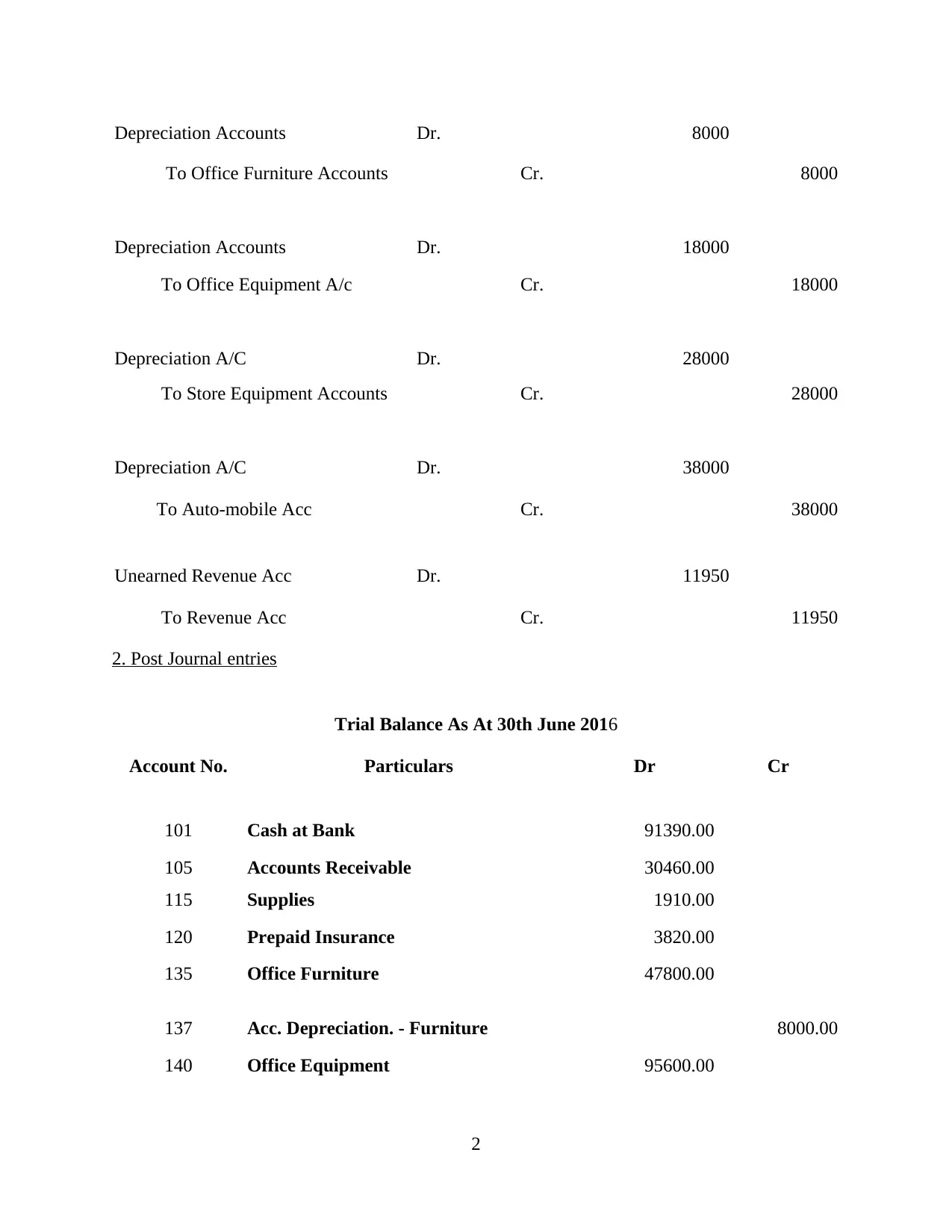

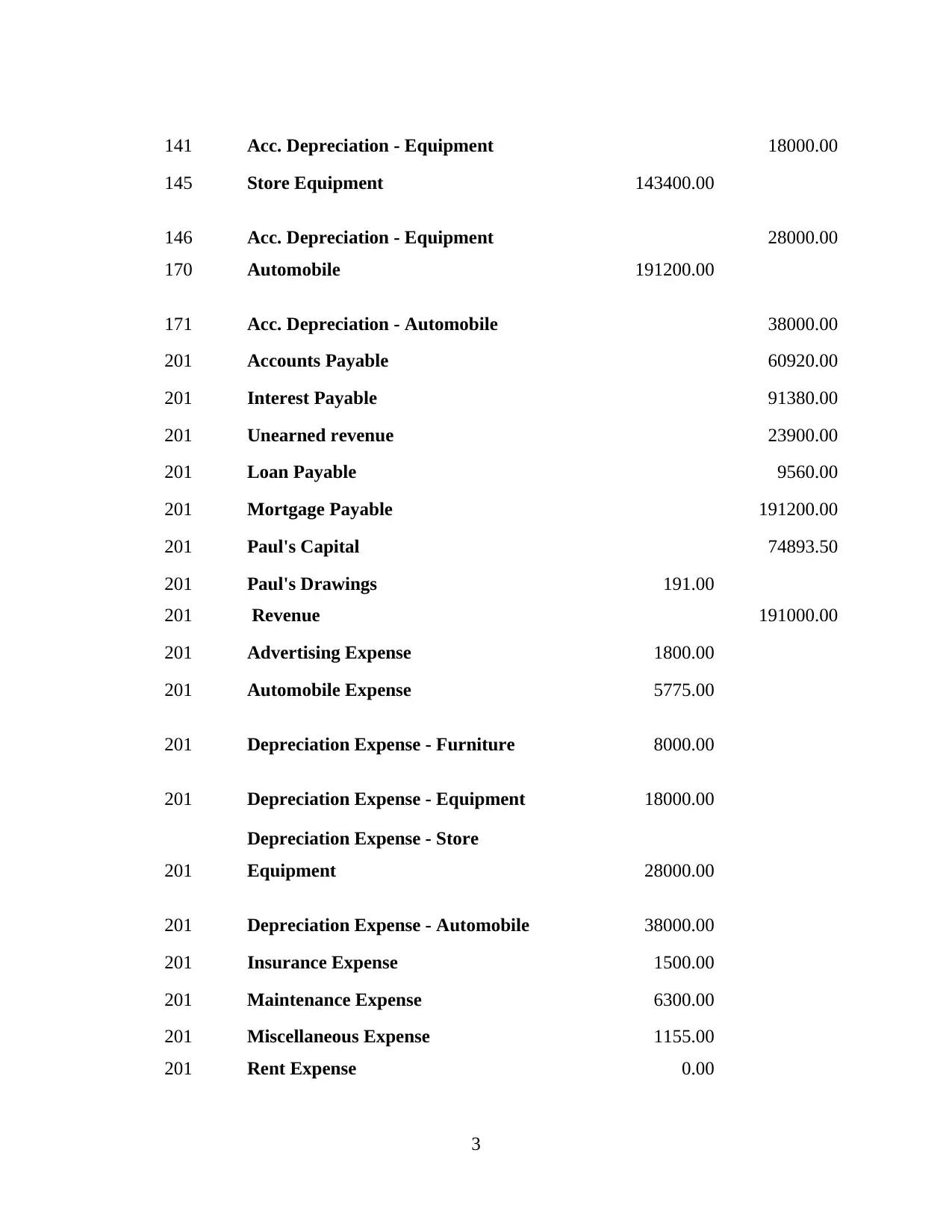

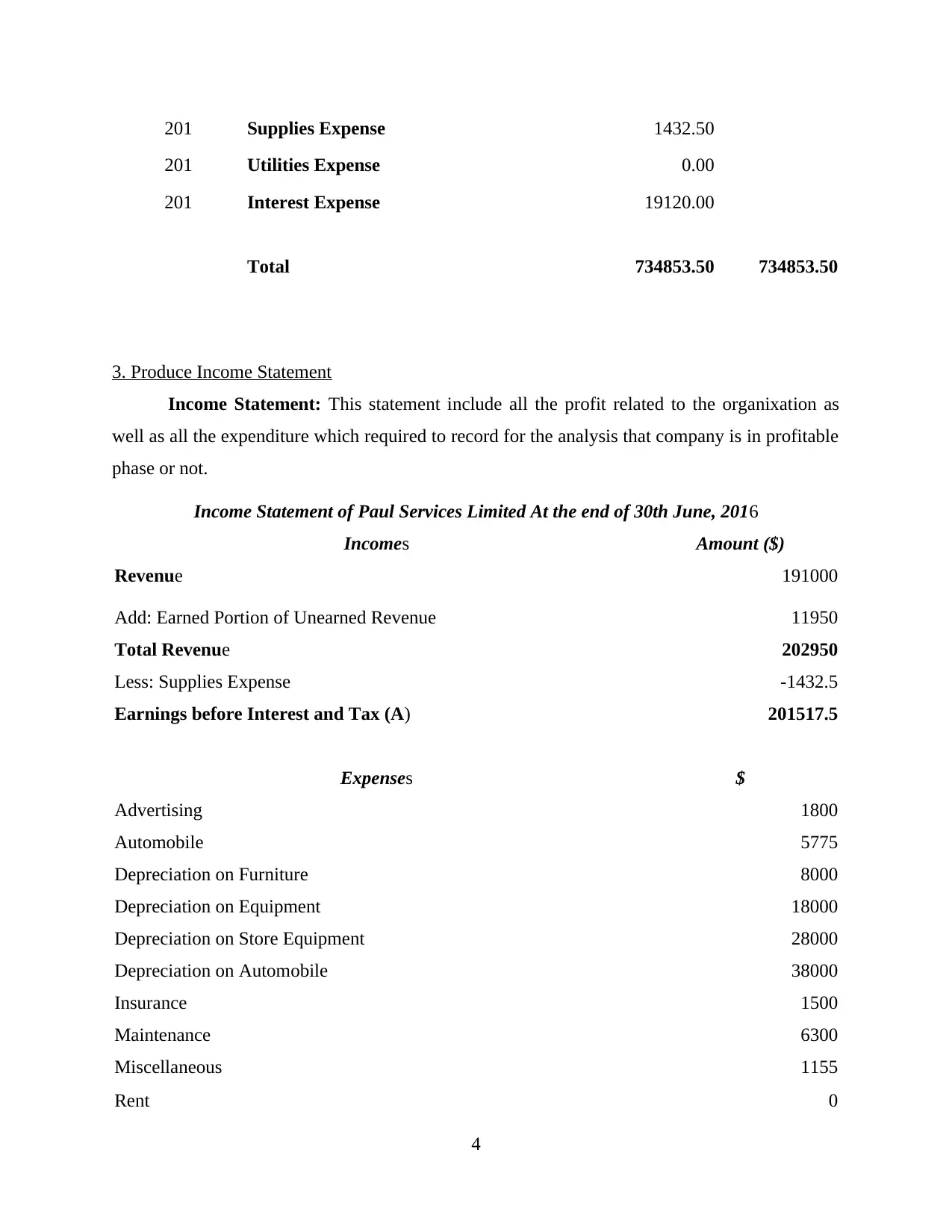

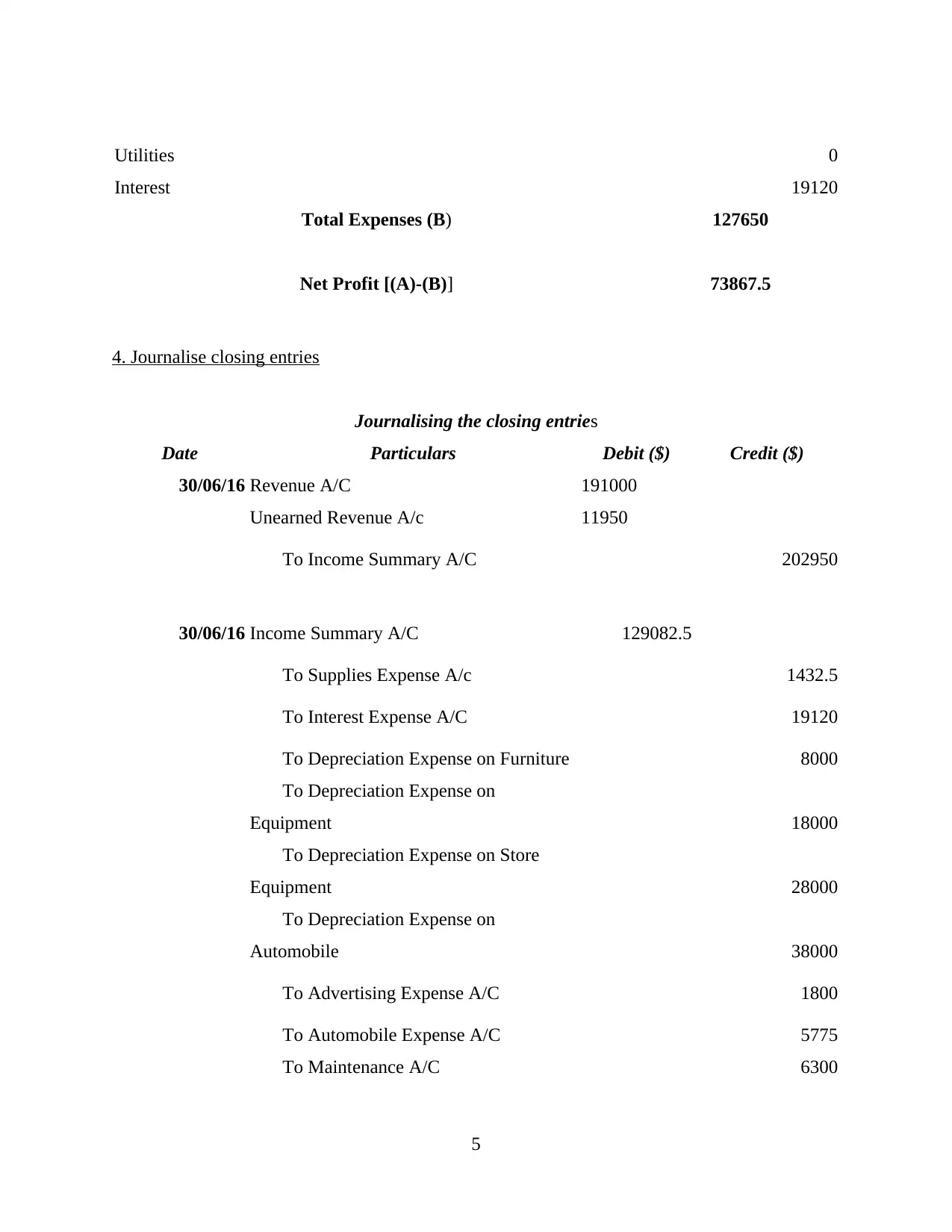

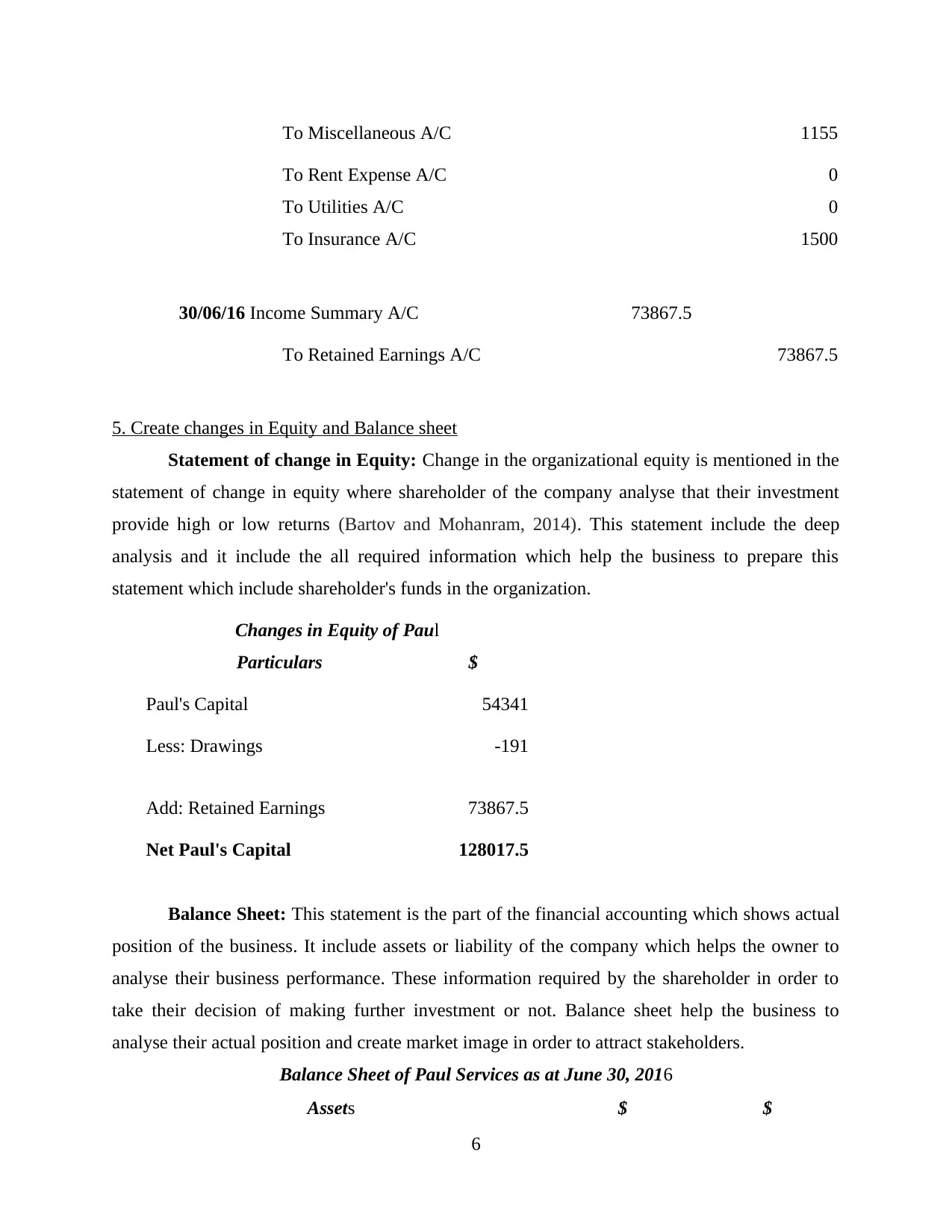

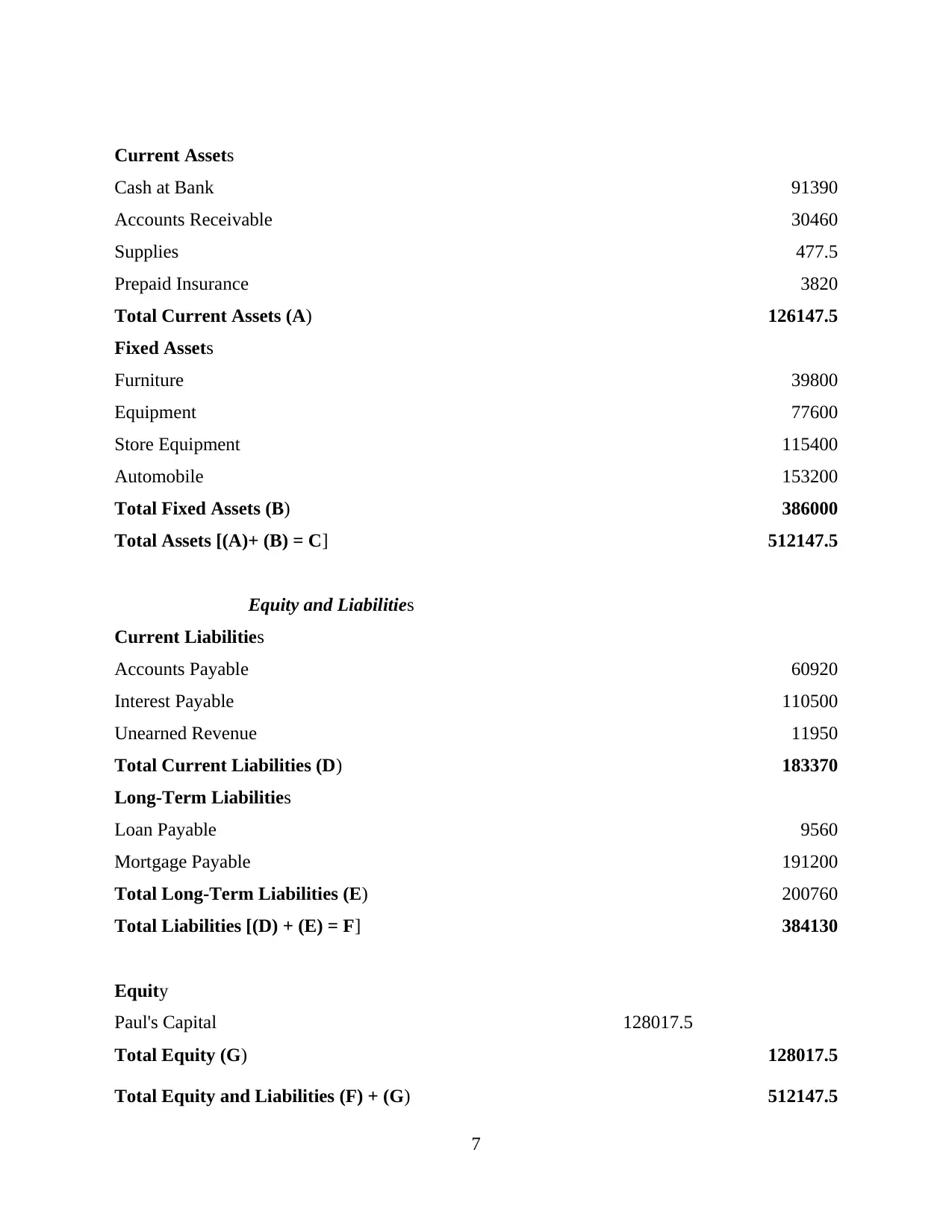

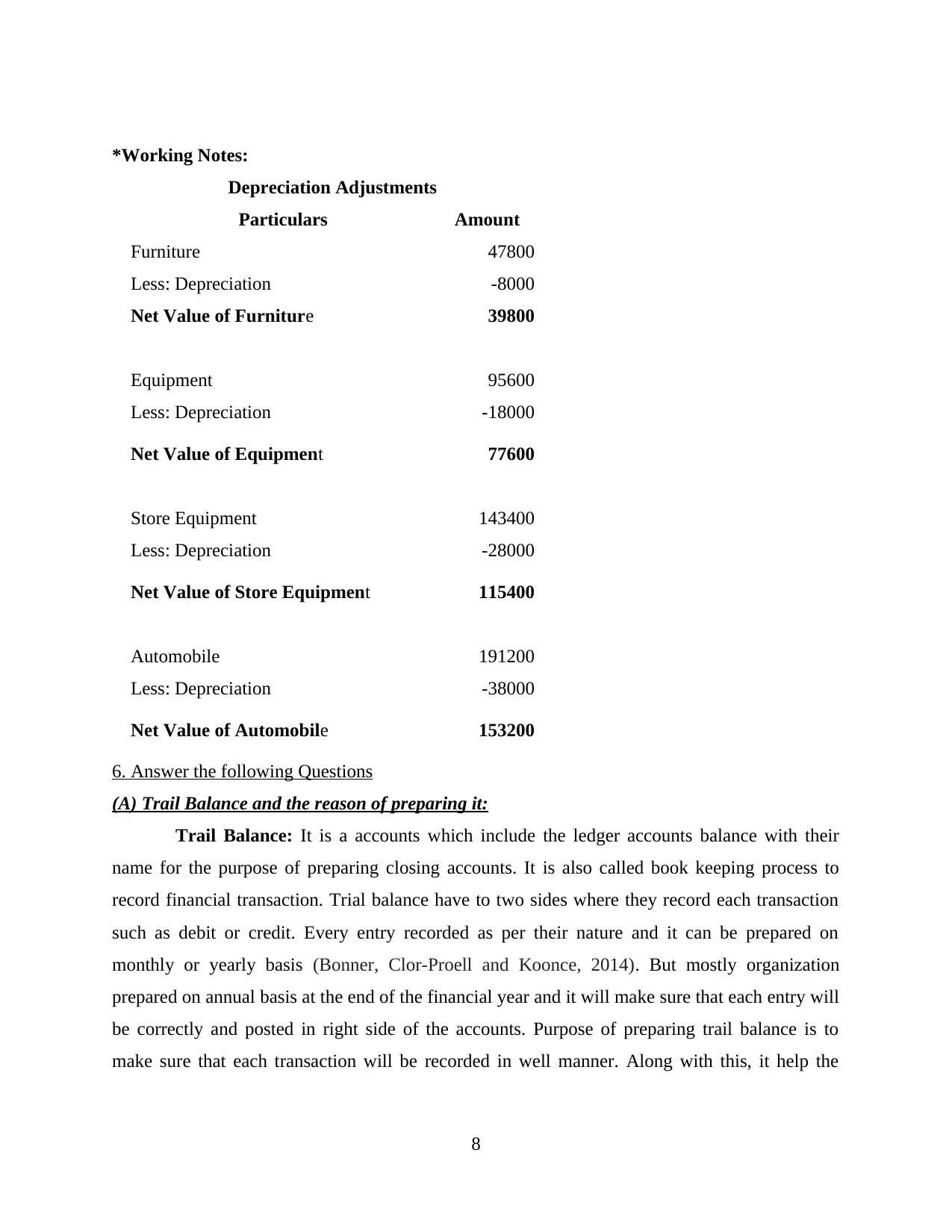

This accounting report provides a detailed analysis of financial transactions and the preparation of financial statements. It begins with journal entries for adjusted transactions, followed by the posting of these entries to a trial balance. The report then constructs an income statement to determine profitability and a statement of changes in equity. A balance sheet is also presented to show the company's assets, liabilities, and equity. Closing entries are journalized to prepare the accounts for the next period. The report also answers questions regarding the trial balance, adjustment entries, their purposes, and the differences between adjustment and closing journal entries. The report covers topics such as journal, ledger posting, trial balance, profit & loss account, balance sheet and adjustment entries.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.