Accounting for Managers (ACC00724) - Assignment 2 Report

VerifiedAdded on 2023/04/23

|9

|1166

|495

Report

AI Summary

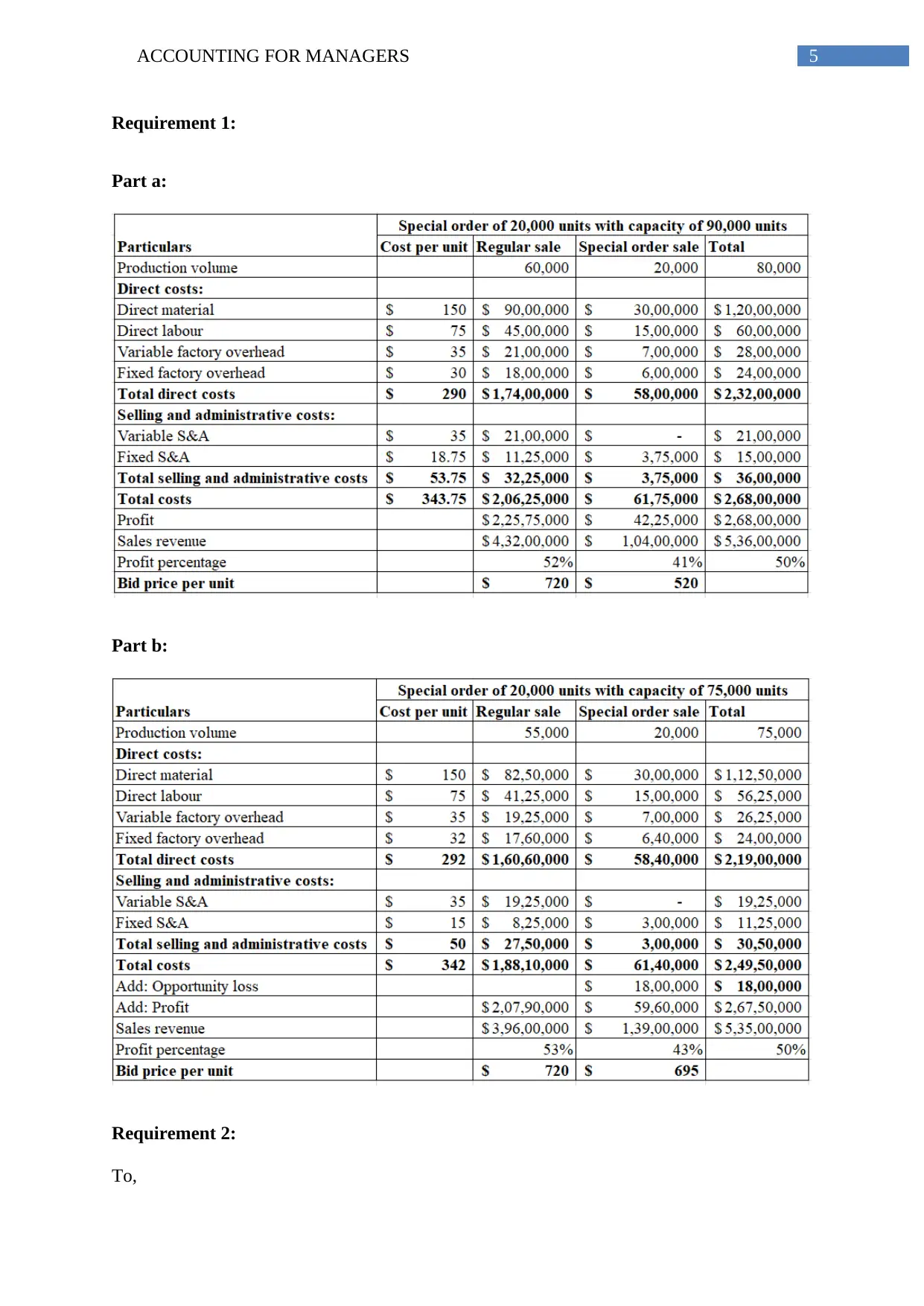

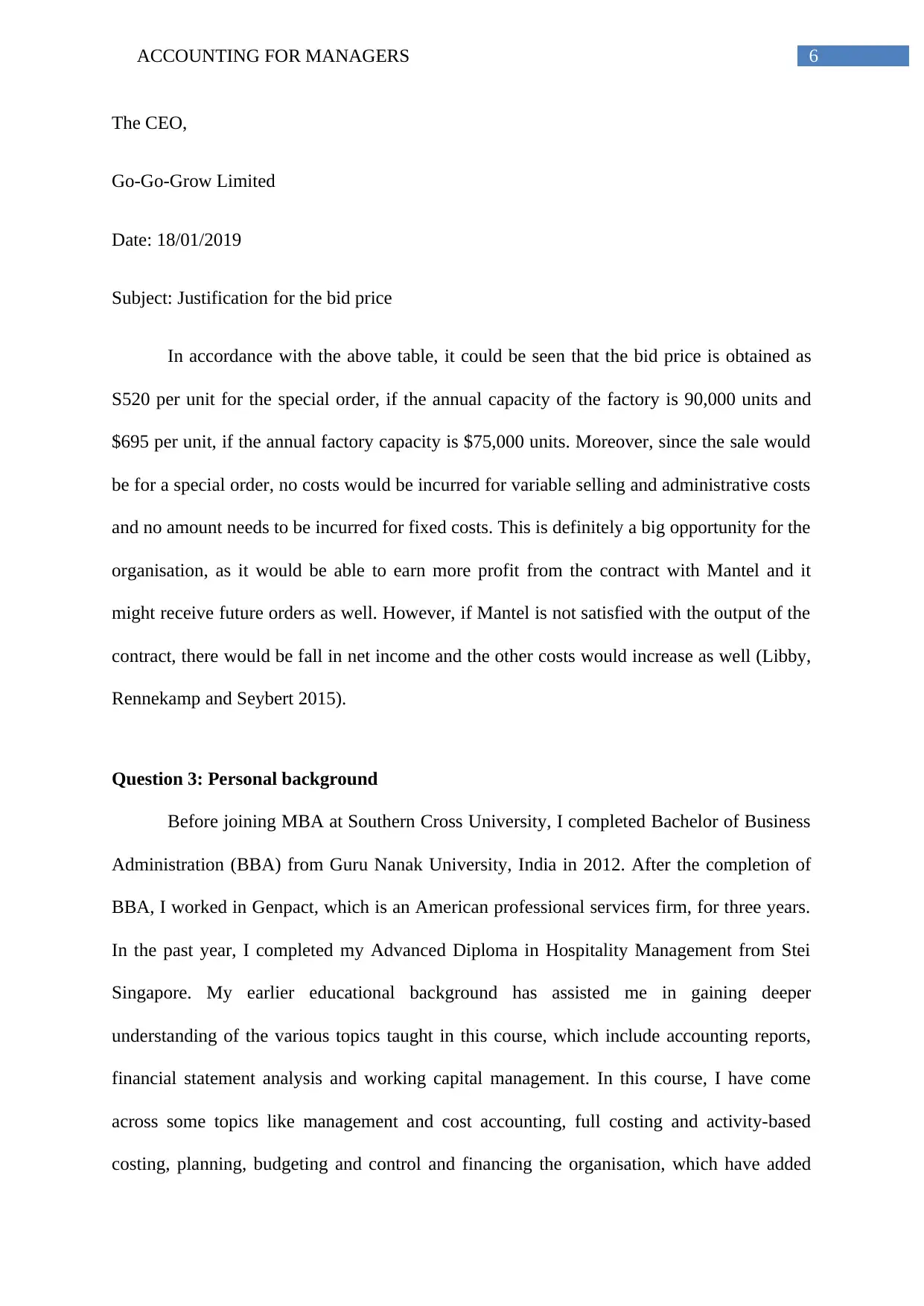

This report provides a comprehensive analysis of two financial scenarios presented in an Accounting for Managers assignment. The first part evaluates three proposals for Pacific Telemet Limited, examining their impact on sales, costs, and profitability, including calculations for contribution margin, break-even points, and margin of safety. The second part addresses a bid price justification for Go-Go-Grow Limited, considering different factory capacity levels and their effect on per-unit costs and potential profits from a special order. The report also includes a personal background section detailing the student's academic and professional experience relevant to the course, highlighting the application of accounting principles in real-world scenarios.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.