University Accounting Assignment Solution: ADM 2342

VerifiedAdded on 2022/08/23

|9

|1042

|31

Homework Assignment

AI Summary

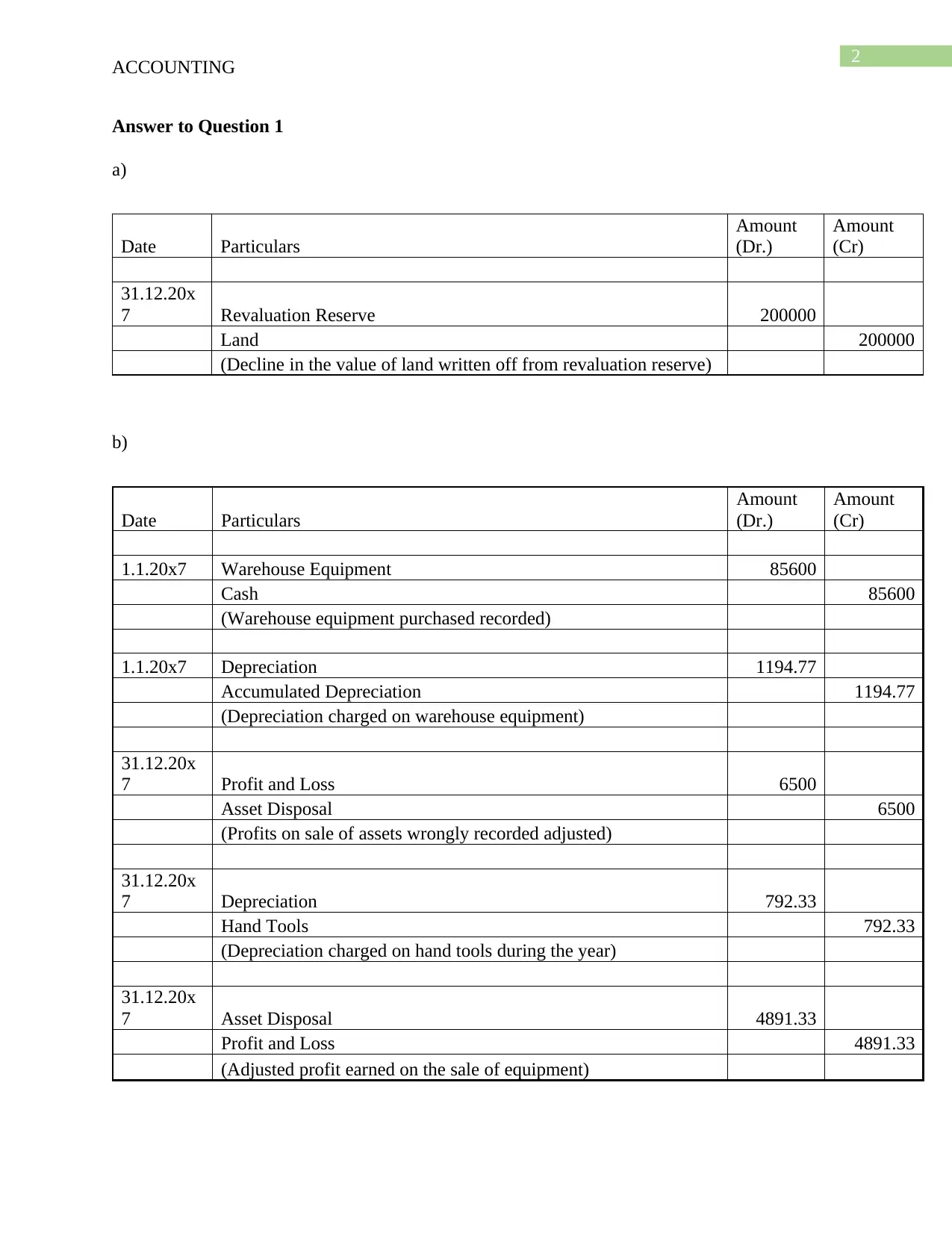

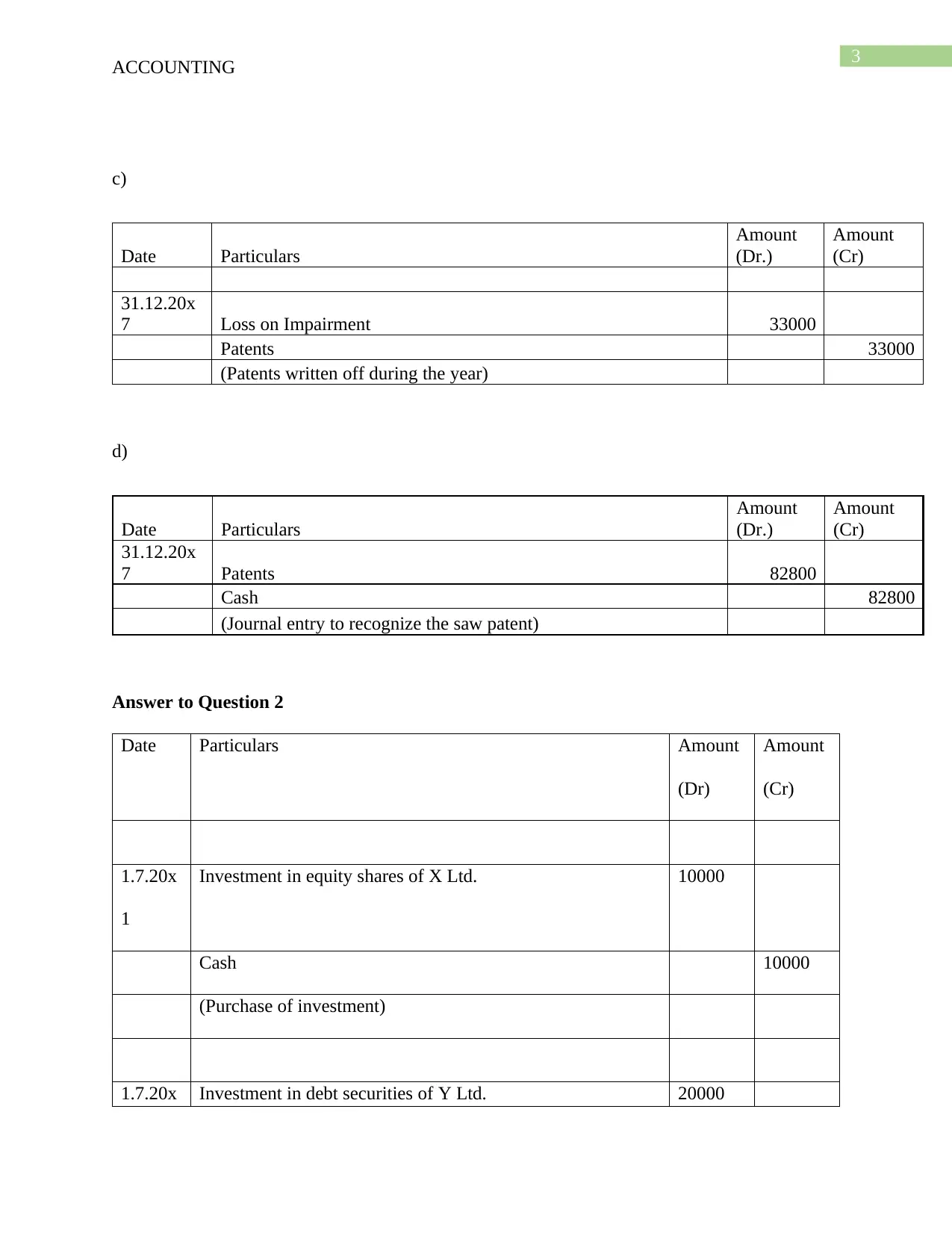

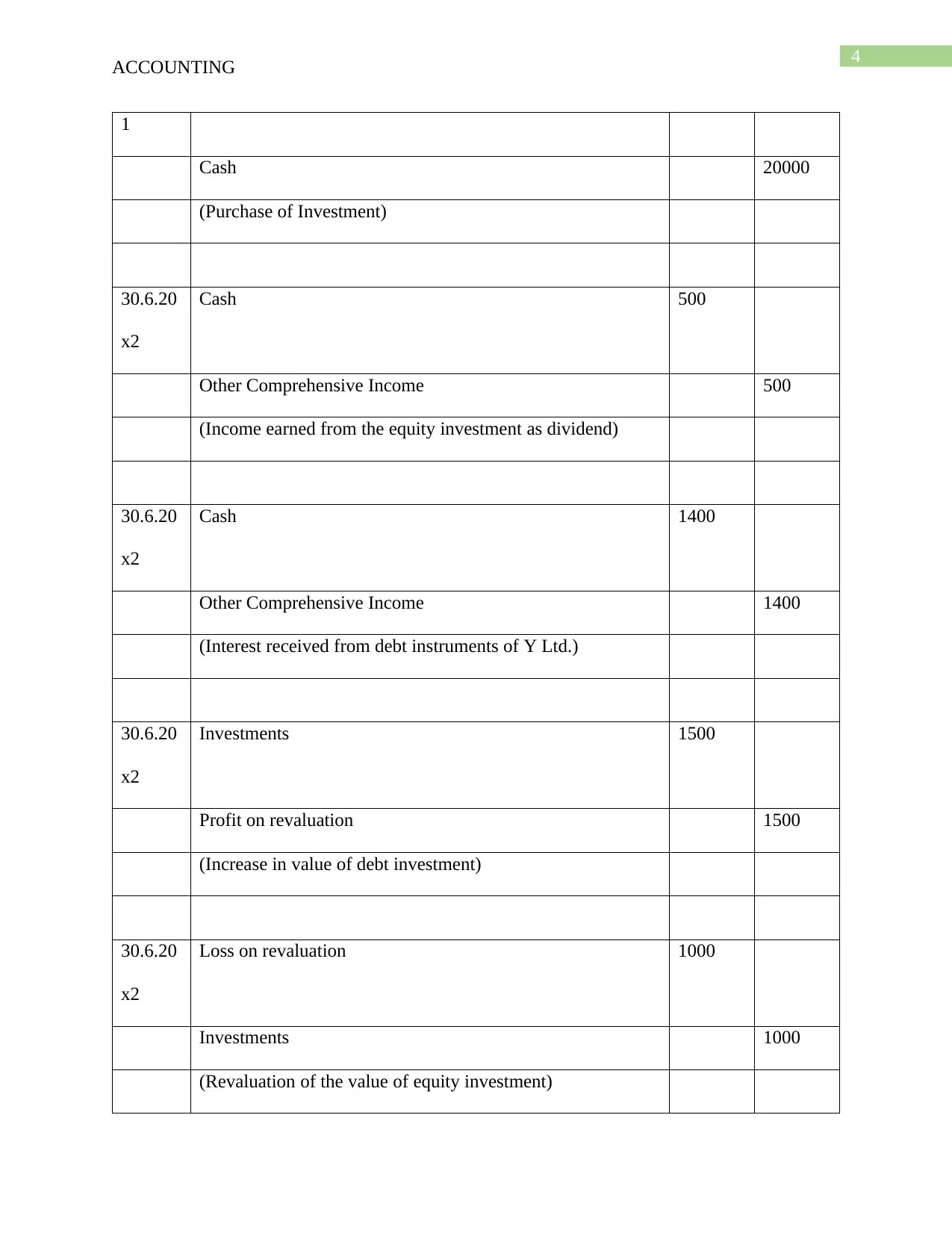

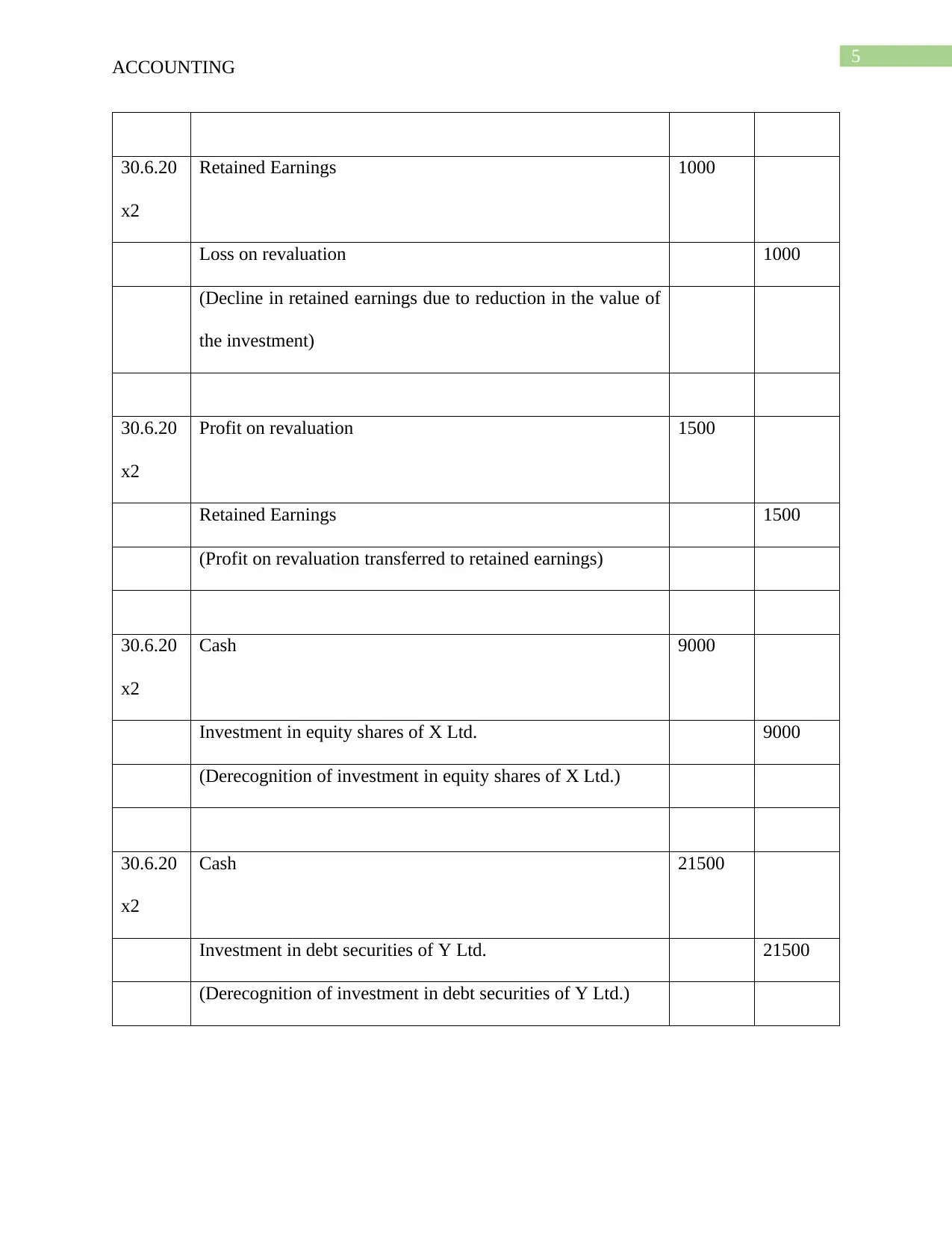

This accounting assignment solution covers a range of topics including journal entries for various transactions such as revaluation of land, purchase and depreciation of warehouse equipment, adjustments for asset disposal, and impairment losses on patents. It also includes journal entries related to investments in equity shares and debt securities, recording dividends, interest income, and revaluation gains and losses. Furthermore, the assignment features a memo explaining three depreciation methods: the straight-line method, the written-down value method, and the sum-of-the-years-digits method, along with their advantages and disadvantages. The memo provides recommendations on which method is most suitable for a specific scenario and concludes with a bibliography of relevant sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.