Accounting for Business BAP 12A Assignment 1, Trimester 1, 2020

VerifiedAdded on 2022/08/08

|11

|2600

|494

Homework Assignment

AI Summary

This document contains a detailed solution to an Accounting for Business assignment (BAP 12A) for Trimester 1, 2020. The assignment is divided into two parts. Part (a) requires the preparation of journal entries, posting them to general ledger accounts, and creating a trial balance for Orange Pty Ltd based on provided transactions. Part (b) provides the general ledger accounts with the balances. Part (c) requires the creation of a trial balance. Question 2 comprises of multiple-choice questions defining accounting, the accounting process, the conceptual framework, retained earnings, accounts, debits and credits, the recording process, journals, general ledgers, posting, trial balances, the accounting information system, and the elements of financial statements. The solution provides comprehensive answers to all questions and sub-parts, offering a complete guide for students studying accounting.

Accounting for Business

BAP 12A

Assessment 1 (5%): Individual hand-written assignment

Trimester 1, Year 2020

Student Id Number Student Name

Signature of Student: Date:

--------------------------------------------------- ------------------------------------------

I hereby confirm that this assignment submitted is my own original work and

handwritten by myself.

Instructions:

This is an Individual hand-written assignment.

o Photostats or typed submissions will not be allowed.

o Please ensure that your submission must be your own original

attempt. Student handwriting will be verified to other hand-written

assessments.

Student answers and submissions are required to be completed as follows:

o Questions 1 in the space provided in THIS answer booklet.

o Question 2 to be completed separately and your answer sheet to be

attached to THIS answer booklet.

Due date for this assignment is Week 4

o Your hand-written attempt must be handed to the lecturer by latest

end of lecture 4 class.

o Late submissions will be subject to a 25% reduction in marks

obtained.

Results for this assessment will be released at the end of week 10.

1 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

BAP 12A

Assessment 1 (5%): Individual hand-written assignment

Trimester 1, Year 2020

Student Id Number Student Name

Signature of Student: Date:

--------------------------------------------------- ------------------------------------------

I hereby confirm that this assignment submitted is my own original work and

handwritten by myself.

Instructions:

This is an Individual hand-written assignment.

o Photostats or typed submissions will not be allowed.

o Please ensure that your submission must be your own original

attempt. Student handwriting will be verified to other hand-written

assessments.

Student answers and submissions are required to be completed as follows:

o Questions 1 in the space provided in THIS answer booklet.

o Question 2 to be completed separately and your answer sheet to be

attached to THIS answer booklet.

Due date for this assignment is Week 4

o Your hand-written attempt must be handed to the lecturer by latest

end of lecture 4 class.

o Late submissions will be subject to a 25% reduction in marks

obtained.

Results for this assessment will be released at the end of week 10.

1 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

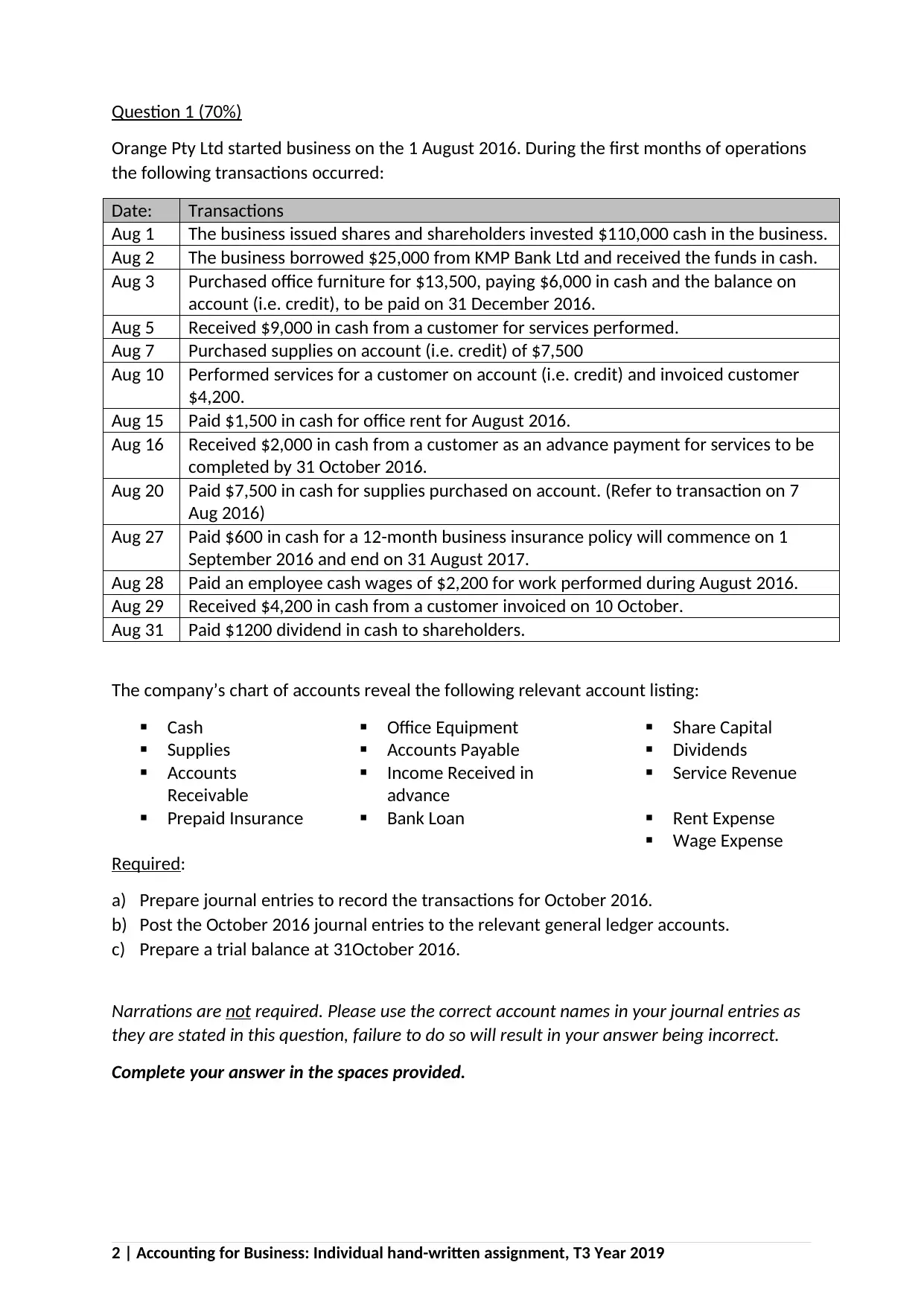

Question 1 (70%)

Orange Pty Ltd started business on the 1 August 2016. During the first months of operations

the following transactions occurred:

Date: Transactions

Aug 1 The business issued shares and shareholders invested $110,000 cash in the business.

Aug 2 The business borrowed $25,000 from KMP Bank Ltd and received the funds in cash.

Aug 3 Purchased office furniture for $13,500, paying $6,000 in cash and the balance on

account (i.e. credit), to be paid on 31 December 2016.

Aug 5 Received $9,000 in cash from a customer for services performed.

Aug 7 Purchased supplies on account (i.e. credit) of $7,500

Aug 10 Performed services for a customer on account (i.e. credit) and invoiced customer

$4,200.

Aug 15 Paid $1,500 in cash for office rent for August 2016.

Aug 16 Received $2,000 in cash from a customer as an advance payment for services to be

completed by 31 October 2016.

Aug 20 Paid $7,500 in cash for supplies purchased on account. (Refer to transaction on 7

Aug 2016)

Aug 27 Paid $600 in cash for a 12-month business insurance policy will commence on 1

September 2016 and end on 31 August 2017.

Aug 28 Paid an employee cash wages of $2,200 for work performed during August 2016.

Aug 29 Received $4,200 in cash from a customer invoiced on 10 October.

Aug 31 Paid $1200 dividend in cash to shareholders.

The company’s chart of accounts reveal the following relevant account listing:

Cash Office Equipment Share Capital

Supplies Accounts Payable Dividends

Accounts

Receivable

Income Received in

advance

Service Revenue

Prepaid Insurance Bank Loan Rent Expense

Wage Expense

Required:

a) Prepare journal entries to record the transactions for October 2016.

b) Post the October 2016 journal entries to the relevant general ledger accounts.

c) Prepare a trial balance at 31October 2016.

Narrations are not required. Please use the correct account names in your journal entries as

they are stated in this question, failure to do so will result in your answer being incorrect.

Complete your answer in the spaces provided.

2 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Orange Pty Ltd started business on the 1 August 2016. During the first months of operations

the following transactions occurred:

Date: Transactions

Aug 1 The business issued shares and shareholders invested $110,000 cash in the business.

Aug 2 The business borrowed $25,000 from KMP Bank Ltd and received the funds in cash.

Aug 3 Purchased office furniture for $13,500, paying $6,000 in cash and the balance on

account (i.e. credit), to be paid on 31 December 2016.

Aug 5 Received $9,000 in cash from a customer for services performed.

Aug 7 Purchased supplies on account (i.e. credit) of $7,500

Aug 10 Performed services for a customer on account (i.e. credit) and invoiced customer

$4,200.

Aug 15 Paid $1,500 in cash for office rent for August 2016.

Aug 16 Received $2,000 in cash from a customer as an advance payment for services to be

completed by 31 October 2016.

Aug 20 Paid $7,500 in cash for supplies purchased on account. (Refer to transaction on 7

Aug 2016)

Aug 27 Paid $600 in cash for a 12-month business insurance policy will commence on 1

September 2016 and end on 31 August 2017.

Aug 28 Paid an employee cash wages of $2,200 for work performed during August 2016.

Aug 29 Received $4,200 in cash from a customer invoiced on 10 October.

Aug 31 Paid $1200 dividend in cash to shareholders.

The company’s chart of accounts reveal the following relevant account listing:

Cash Office Equipment Share Capital

Supplies Accounts Payable Dividends

Accounts

Receivable

Income Received in

advance

Service Revenue

Prepaid Insurance Bank Loan Rent Expense

Wage Expense

Required:

a) Prepare journal entries to record the transactions for October 2016.

b) Post the October 2016 journal entries to the relevant general ledger accounts.

c) Prepare a trial balance at 31October 2016.

Narrations are not required. Please use the correct account names in your journal entries as

they are stated in this question, failure to do so will result in your answer being incorrect.

Complete your answer in the spaces provided.

2 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

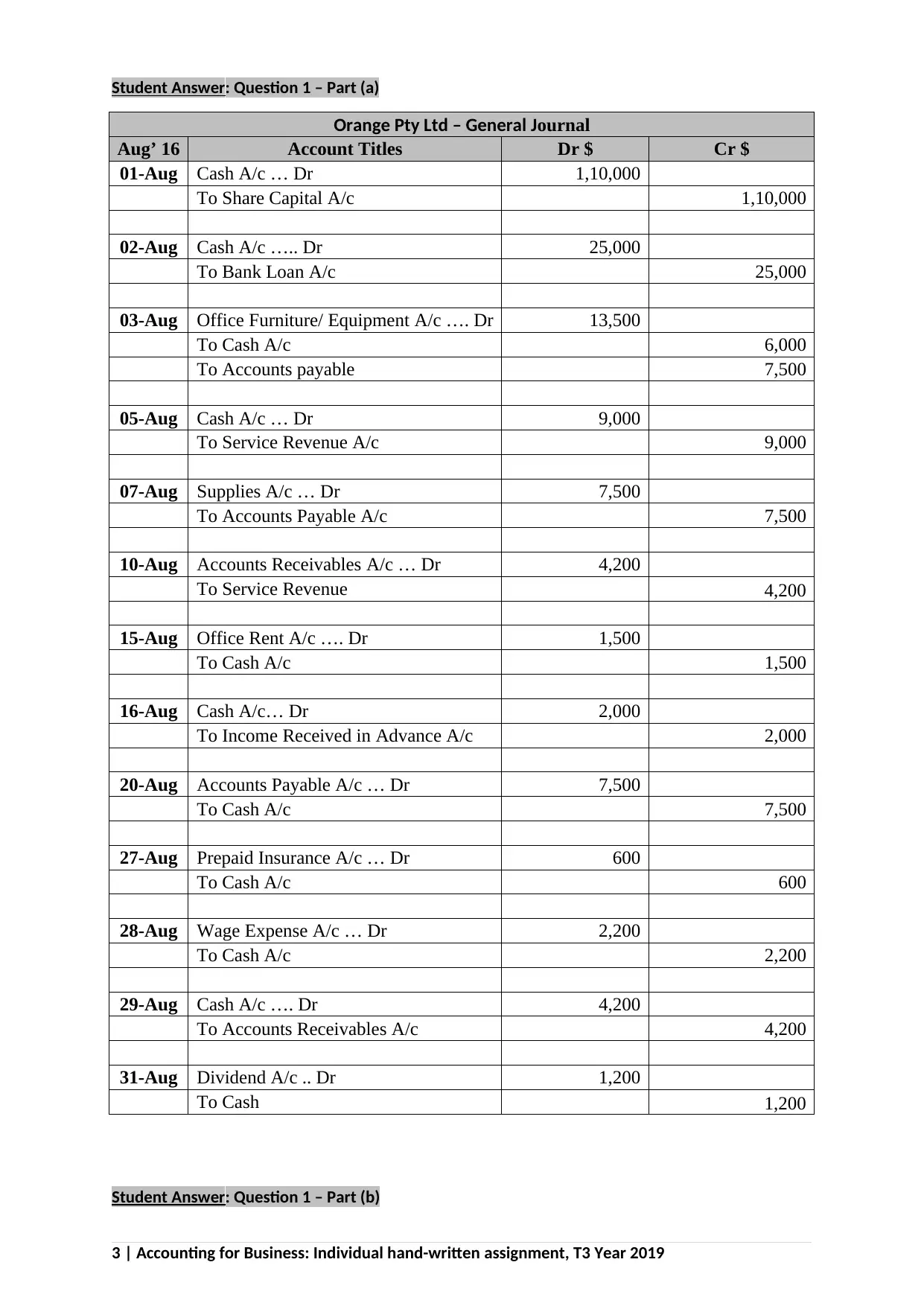

Student Answer: Question 1 – Part (a)

Orange Pty Ltd – General Journal

Aug’ 16 Account Titles Dr $ Cr $

01-Aug Cash A/c … Dr 1,10,000

To Share Capital A/c 1,10,000

02-Aug Cash A/c ….. Dr 25,000

To Bank Loan A/c 25,000

03-Aug Office Furniture/ Equipment A/c …. Dr 13,500

To Cash A/c 6,000

To Accounts payable 7,500

05-Aug Cash A/c … Dr 9,000

To Service Revenue A/c 9,000

07-Aug Supplies A/c … Dr 7,500

To Accounts Payable A/c 7,500

10-Aug Accounts Receivables A/c … Dr 4,200

To Service Revenue 4,200

15-Aug Office Rent A/c …. Dr 1,500

To Cash A/c 1,500

16-Aug Cash A/c… Dr 2,000

To Income Received in Advance A/c 2,000

20-Aug Accounts Payable A/c … Dr 7,500

To Cash A/c 7,500

27-Aug Prepaid Insurance A/c … Dr 600

To Cash A/c 600

28-Aug Wage Expense A/c … Dr 2,200

To Cash A/c 2,200

29-Aug Cash A/c …. Dr 4,200

To Accounts Receivables A/c 4,200

31-Aug Dividend A/c .. Dr 1,200

To Cash 1,200

Student Answer: Question 1 – Part (b)

3 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Orange Pty Ltd – General Journal

Aug’ 16 Account Titles Dr $ Cr $

01-Aug Cash A/c … Dr 1,10,000

To Share Capital A/c 1,10,000

02-Aug Cash A/c ….. Dr 25,000

To Bank Loan A/c 25,000

03-Aug Office Furniture/ Equipment A/c …. Dr 13,500

To Cash A/c 6,000

To Accounts payable 7,500

05-Aug Cash A/c … Dr 9,000

To Service Revenue A/c 9,000

07-Aug Supplies A/c … Dr 7,500

To Accounts Payable A/c 7,500

10-Aug Accounts Receivables A/c … Dr 4,200

To Service Revenue 4,200

15-Aug Office Rent A/c …. Dr 1,500

To Cash A/c 1,500

16-Aug Cash A/c… Dr 2,000

To Income Received in Advance A/c 2,000

20-Aug Accounts Payable A/c … Dr 7,500

To Cash A/c 7,500

27-Aug Prepaid Insurance A/c … Dr 600

To Cash A/c 600

28-Aug Wage Expense A/c … Dr 2,200

To Cash A/c 2,200

29-Aug Cash A/c …. Dr 4,200

To Accounts Receivables A/c 4,200

31-Aug Dividend A/c .. Dr 1,200

To Cash 1,200

Student Answer: Question 1 – Part (b)

3 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

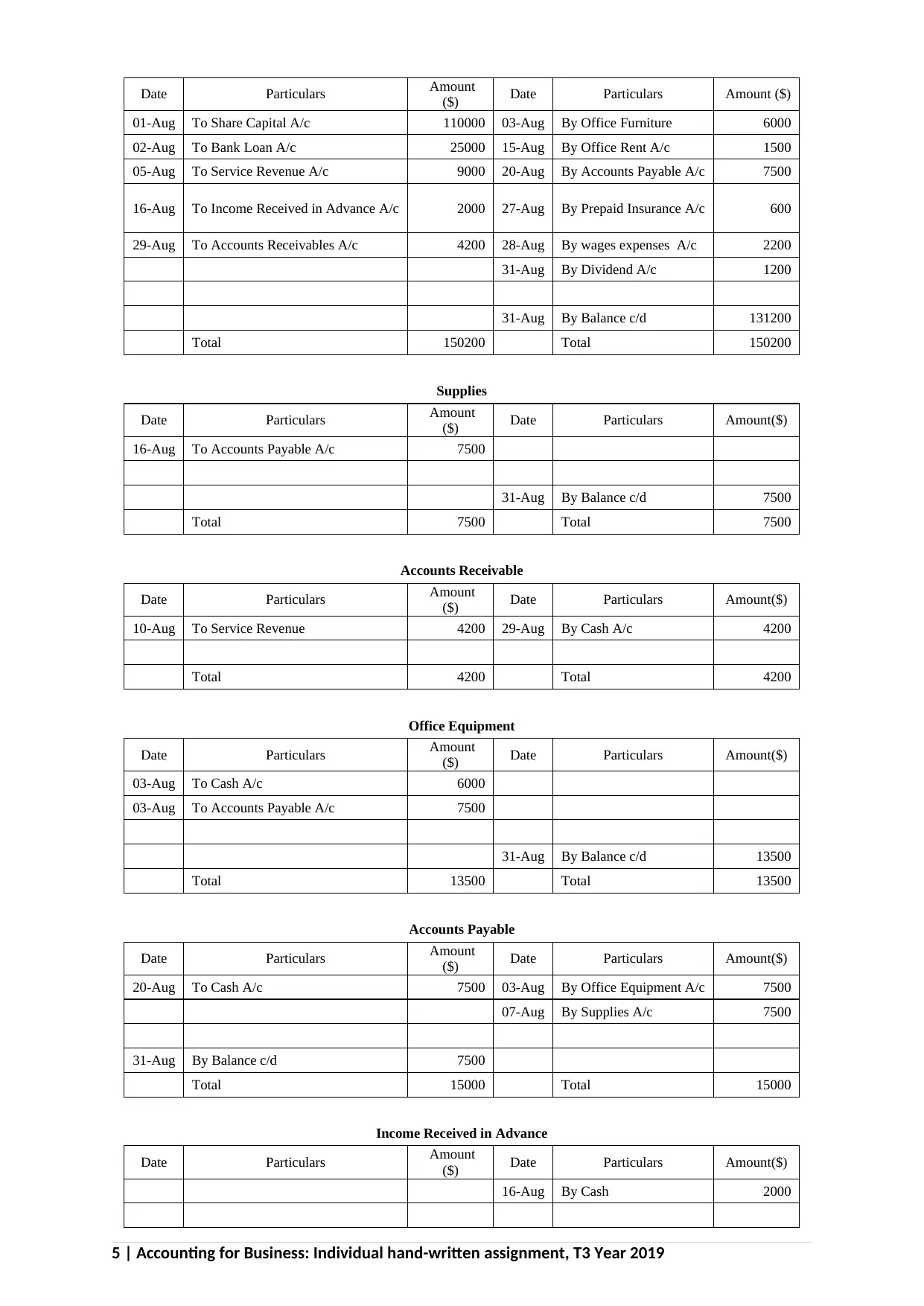

Cash

4 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

4 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Amount

($) Date Particulars Amount ($)

01-Aug To Share Capital A/c 110000 03-Aug By Office Furniture 6000

02-Aug To Bank Loan A/c 25000 15-Aug By Office Rent A/c 1500

05-Aug To Service Revenue A/c 9000 20-Aug By Accounts Payable A/c 7500

16-Aug To Income Received in Advance A/c 2000 27-Aug By Prepaid Insurance A/c 600

29-Aug To Accounts Receivables A/c 4200 28-Aug By wages expenses A/c 2200

31-Aug By Dividend A/c 1200

31-Aug By Balance c/d 131200

Total 150200 Total 150200

Supplies

Date Particulars Amount

($) Date Particulars Amount($)

16-Aug To Accounts Payable A/c 7500

31-Aug By Balance c/d 7500

Total 7500 Total 7500

Accounts Receivable

Date Particulars Amount

($) Date Particulars Amount($)

10-Aug To Service Revenue 4200 29-Aug By Cash A/c 4200

Total 4200 Total 4200

Office Equipment

Date Particulars Amount

($) Date Particulars Amount($)

03-Aug To Cash A/c 6000

03-Aug To Accounts Payable A/c 7500

31-Aug By Balance c/d 13500

Total 13500 Total 13500

Accounts Payable

Date Particulars Amount

($) Date Particulars Amount($)

20-Aug To Cash A/c 7500 03-Aug By Office Equipment A/c 7500

07-Aug By Supplies A/c 7500

31-Aug By Balance c/d 7500

Total 15000 Total 15000

Income Received in Advance

Date Particulars Amount

($) Date Particulars Amount($)

16-Aug By Cash 2000

5 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

($) Date Particulars Amount ($)

01-Aug To Share Capital A/c 110000 03-Aug By Office Furniture 6000

02-Aug To Bank Loan A/c 25000 15-Aug By Office Rent A/c 1500

05-Aug To Service Revenue A/c 9000 20-Aug By Accounts Payable A/c 7500

16-Aug To Income Received in Advance A/c 2000 27-Aug By Prepaid Insurance A/c 600

29-Aug To Accounts Receivables A/c 4200 28-Aug By wages expenses A/c 2200

31-Aug By Dividend A/c 1200

31-Aug By Balance c/d 131200

Total 150200 Total 150200

Supplies

Date Particulars Amount

($) Date Particulars Amount($)

16-Aug To Accounts Payable A/c 7500

31-Aug By Balance c/d 7500

Total 7500 Total 7500

Accounts Receivable

Date Particulars Amount

($) Date Particulars Amount($)

10-Aug To Service Revenue 4200 29-Aug By Cash A/c 4200

Total 4200 Total 4200

Office Equipment

Date Particulars Amount

($) Date Particulars Amount($)

03-Aug To Cash A/c 6000

03-Aug To Accounts Payable A/c 7500

31-Aug By Balance c/d 13500

Total 13500 Total 13500

Accounts Payable

Date Particulars Amount

($) Date Particulars Amount($)

20-Aug To Cash A/c 7500 03-Aug By Office Equipment A/c 7500

07-Aug By Supplies A/c 7500

31-Aug By Balance c/d 7500

Total 15000 Total 15000

Income Received in Advance

Date Particulars Amount

($) Date Particulars Amount($)

16-Aug By Cash 2000

5 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

31-Aug By Balance c/d 2000

Total 2000 Total 2000

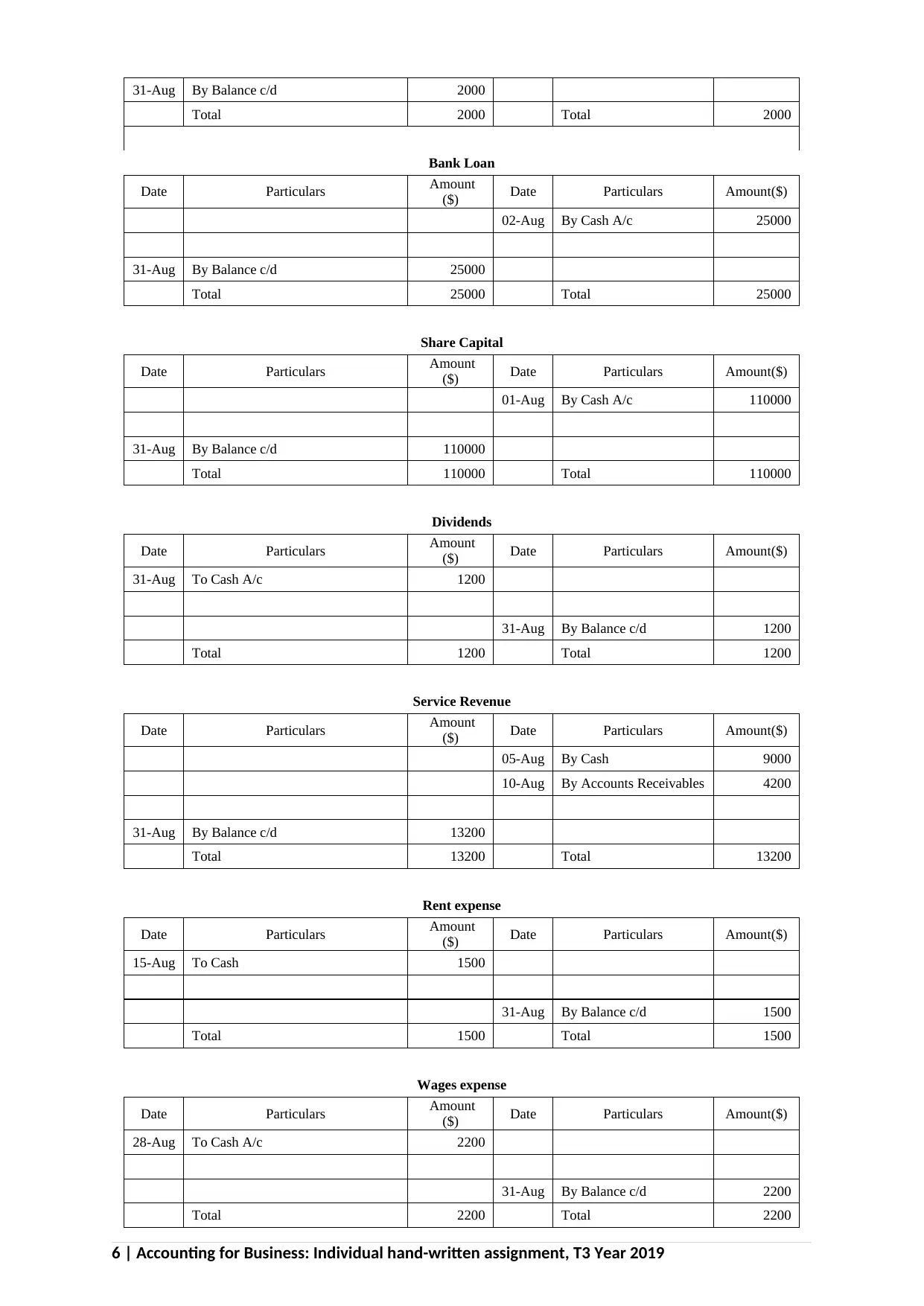

Bank Loan

Date Particulars Amount

($) Date Particulars Amount($)

02-Aug By Cash A/c 25000

31-Aug By Balance c/d 25000

Total 25000 Total 25000

Share Capital

Date Particulars Amount

($) Date Particulars Amount($)

01-Aug By Cash A/c 110000

31-Aug By Balance c/d 110000

Total 110000 Total 110000

Dividends

Date Particulars Amount

($) Date Particulars Amount($)

31-Aug To Cash A/c 1200

31-Aug By Balance c/d 1200

Total 1200 Total 1200

Service Revenue

Date Particulars Amount

($) Date Particulars Amount($)

05-Aug By Cash 9000

10-Aug By Accounts Receivables 4200

31-Aug By Balance c/d 13200

Total 13200 Total 13200

Rent expense

Date Particulars Amount

($) Date Particulars Amount($)

15-Aug To Cash 1500

31-Aug By Balance c/d 1500

Total 1500 Total 1500

Wages expense

Date Particulars Amount

($) Date Particulars Amount($)

28-Aug To Cash A/c 2200

31-Aug By Balance c/d 2200

Total 2200 Total 2200

6 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Total 2000 Total 2000

Bank Loan

Date Particulars Amount

($) Date Particulars Amount($)

02-Aug By Cash A/c 25000

31-Aug By Balance c/d 25000

Total 25000 Total 25000

Share Capital

Date Particulars Amount

($) Date Particulars Amount($)

01-Aug By Cash A/c 110000

31-Aug By Balance c/d 110000

Total 110000 Total 110000

Dividends

Date Particulars Amount

($) Date Particulars Amount($)

31-Aug To Cash A/c 1200

31-Aug By Balance c/d 1200

Total 1200 Total 1200

Service Revenue

Date Particulars Amount

($) Date Particulars Amount($)

05-Aug By Cash 9000

10-Aug By Accounts Receivables 4200

31-Aug By Balance c/d 13200

Total 13200 Total 13200

Rent expense

Date Particulars Amount

($) Date Particulars Amount($)

15-Aug To Cash 1500

31-Aug By Balance c/d 1500

Total 1500 Total 1500

Wages expense

Date Particulars Amount

($) Date Particulars Amount($)

28-Aug To Cash A/c 2200

31-Aug By Balance c/d 2200

Total 2200 Total 2200

6 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

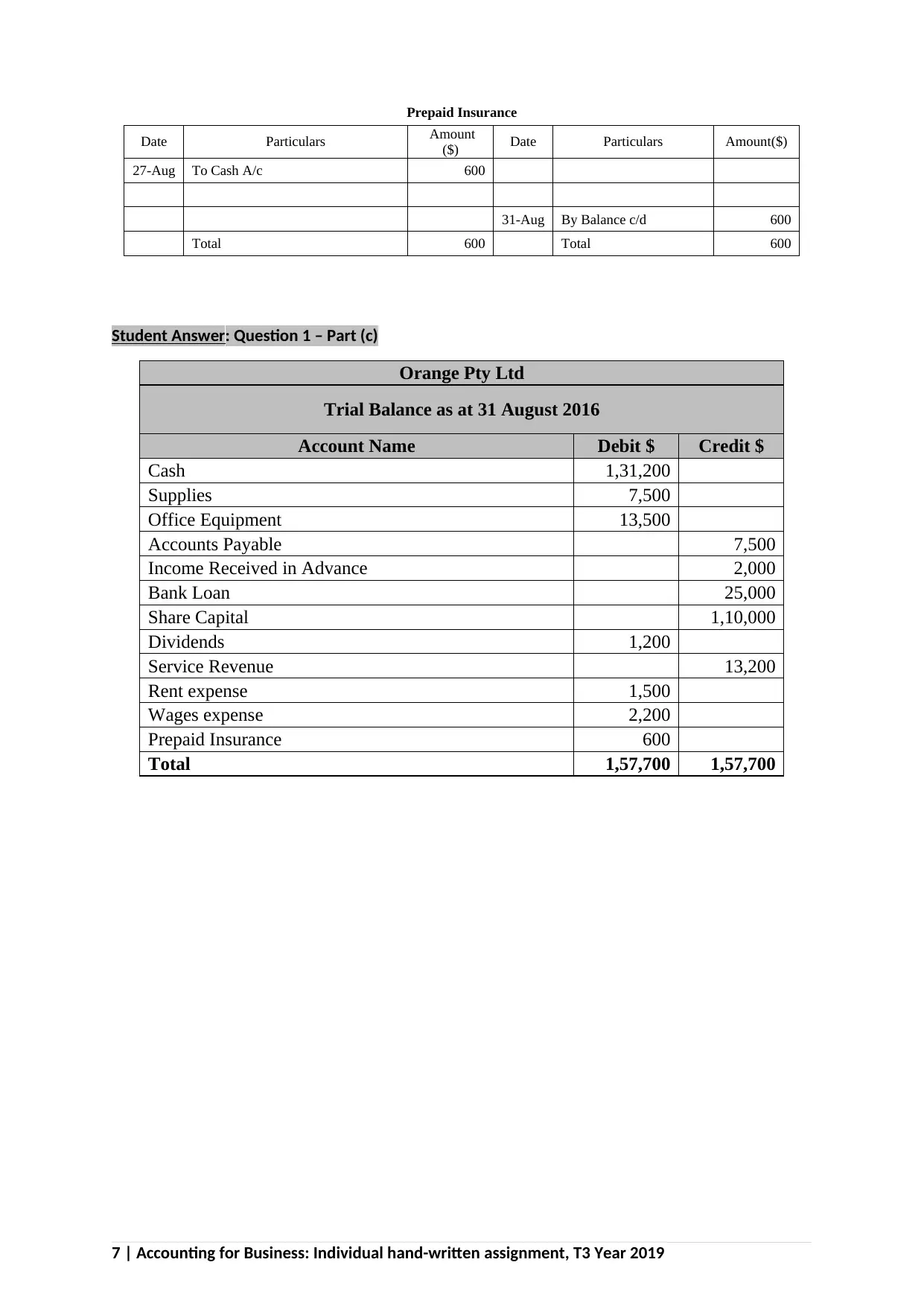

Prepaid Insurance

Date Particulars Amount

($) Date Particulars Amount($)

27-Aug To Cash A/c 600

31-Aug By Balance c/d 600

Total 600 Total 600

Student Answer: Question 1 – Part (c)

Orange Pty Ltd

Trial Balance as at 31 August 2016

Account Name Debit $ Credit $

Cash 1,31,200

Supplies 7,500

Office Equipment 13,500

Accounts Payable 7,500

Income Received in Advance 2,000

Bank Loan 25,000

Share Capital 1,10,000

Dividends 1,200

Service Revenue 13,200

Rent expense 1,500

Wages expense 2,200

Prepaid Insurance 600

Total 1,57,700 1,57,700

7 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Date Particulars Amount

($) Date Particulars Amount($)

27-Aug To Cash A/c 600

31-Aug By Balance c/d 600

Total 600 Total 600

Student Answer: Question 1 – Part (c)

Orange Pty Ltd

Trial Balance as at 31 August 2016

Account Name Debit $ Credit $

Cash 1,31,200

Supplies 7,500

Office Equipment 13,500

Accounts Payable 7,500

Income Received in Advance 2,000

Bank Loan 25,000

Share Capital 1,10,000

Dividends 1,200

Service Revenue 13,200

Rent expense 1,500

Wages expense 2,200

Prepaid Insurance 600

Total 1,57,700 1,57,700

7 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2 (30%)

Part A Define accounting and describe the accounting process.

Part B What is the conceptual framework and what purpose does it serve?

Part C What is retained earnings. What items increase or decrease the balance in retained

earnings?

Part D Explain what an account is and how it helps in the recording process.

Part E Define debits and credits and explain how they are used to record accounting

transactions

Part F Identify the basic steps in the recording process?

Part G Explain what a journal is and how it helps in the recording process.

Part H Explain what a general ledger is and how it helps in the recording process

Part I Explain what posting is and how it helps in the recording process

Part J Explain the purposes of a trial balance.

Part K Describe the accounting information system and the steps in the recording process.

Part L Identify the elements of each of the four main financial statements?

Student Answer: Question 2

Question

No. 2

Part A Define accounting and describe the accounting process.

Accounting is a systematic process of recording financial transaction of business. This

process involves identifying, summarizing, analyzing, classifying and interpreting the

financial transaction of business. It shows the income and expenses of a particular period

and the values of asset, liabilities and shareholder’s equity of any firm.

The accounting process is the financial transaction which occurred from the beginning to

the end of the accounting period. The three types of accounting process transactions are

The reversing entries for the previous year transaction.

Recording the steps in the individual business transaction in accounting.

It produces the financial statement of the end processing of period.

Part B What is the conceptual framework, and what purpose does it serve?

Conceptual framework of accounting is a set of rules, regulation and standard of

accounting which developed by the International accounting standard board (IASB) to

perform a balance among different accounting methods.

The purpose of the conceptual accounting framework that

8 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Part A Define accounting and describe the accounting process.

Part B What is the conceptual framework and what purpose does it serve?

Part C What is retained earnings. What items increase or decrease the balance in retained

earnings?

Part D Explain what an account is and how it helps in the recording process.

Part E Define debits and credits and explain how they are used to record accounting

transactions

Part F Identify the basic steps in the recording process?

Part G Explain what a journal is and how it helps in the recording process.

Part H Explain what a general ledger is and how it helps in the recording process

Part I Explain what posting is and how it helps in the recording process

Part J Explain the purposes of a trial balance.

Part K Describe the accounting information system and the steps in the recording process.

Part L Identify the elements of each of the four main financial statements?

Student Answer: Question 2

Question

No. 2

Part A Define accounting and describe the accounting process.

Accounting is a systematic process of recording financial transaction of business. This

process involves identifying, summarizing, analyzing, classifying and interpreting the

financial transaction of business. It shows the income and expenses of a particular period

and the values of asset, liabilities and shareholder’s equity of any firm.

The accounting process is the financial transaction which occurred from the beginning to

the end of the accounting period. The three types of accounting process transactions are

The reversing entries for the previous year transaction.

Recording the steps in the individual business transaction in accounting.

It produces the financial statement of the end processing of period.

Part B What is the conceptual framework, and what purpose does it serve?

Conceptual framework of accounting is a set of rules, regulation and standard of

accounting which developed by the International accounting standard board (IASB) to

perform a balance among different accounting methods.

The purpose of the conceptual accounting framework that

8 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

It assists the IASB to develop the future IFRS and check the existing IFRS.

It prepares the financial statement to develop the accounting policies to perform

transaction or events with the existing rules and standards.

Sometimes IASB may have any issues with the rules of the IFRS and can ask to

revise the rules and regulations of the accounting framework. This cause conflicts

and ask to end the framework for the IFRS.

Part C What is retained earnings? What items increase or decrease the balance in retained

earnings?

Retained earnings are the net income of a business which produce after payment of

dividend and taxes; however, even the non-payment to the shareholder will include in the

retained earning term. The profit which incurred after the payment can also re-invest back

to the business for its growth and development process.

The items which increased or decreased the retained earnings is dividend payment to the

shareholder and other small or large transaction. Net income can also increase or decrease

earnings.

Part D Explain what an account is and how it helps in the recording process.

In simple term, an account is a recording, classifying, summarizing and interpreting the

financial transaction of business. It shows the income and losses of the business

transaction.

It helps to record the financial information into journal entries, which helps to locate the

errors in transaction due to comparing debit and credit entry amount.

Part E Define debits and credits and explain how they are used to record accounting

transactions

The debit is an accounting entry which can increase expenses and asset and can decrease

the liability or equity account of a transaction. Credit is another accounting entry which

increases the income and liability and decreases the expenses and asset.

Debit and credit use to monitor the incoming and outgoing transaction of a business and

help the business to use the double-entry system.

Part F Identify the basic steps in the recording process?

The basic steps in the recording process of accounting are

Analysing the financial transaction

Prepare the journal entries based on the given information

Posting the entries in the ledger accounts formats

Based on the ledger, prepare the trial balance and then the financial statement.

Part G Explain what a journal is and how it helps in the recording process.

Journal is an accounts transaction which records all the financial data by allotting the

accounts names with debit and credit. It is a detailed financial transaction which used in

reconciling the future transaction.

Journal helps in the recording process as it completely discloses the effect of any

transaction; it records a systematic accounting transaction and locates the errors that

delivered while in debiting or crediting.

9 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

It prepares the financial statement to develop the accounting policies to perform

transaction or events with the existing rules and standards.

Sometimes IASB may have any issues with the rules of the IFRS and can ask to

revise the rules and regulations of the accounting framework. This cause conflicts

and ask to end the framework for the IFRS.

Part C What is retained earnings? What items increase or decrease the balance in retained

earnings?

Retained earnings are the net income of a business which produce after payment of

dividend and taxes; however, even the non-payment to the shareholder will include in the

retained earning term. The profit which incurred after the payment can also re-invest back

to the business for its growth and development process.

The items which increased or decreased the retained earnings is dividend payment to the

shareholder and other small or large transaction. Net income can also increase or decrease

earnings.

Part D Explain what an account is and how it helps in the recording process.

In simple term, an account is a recording, classifying, summarizing and interpreting the

financial transaction of business. It shows the income and losses of the business

transaction.

It helps to record the financial information into journal entries, which helps to locate the

errors in transaction due to comparing debit and credit entry amount.

Part E Define debits and credits and explain how they are used to record accounting

transactions

The debit is an accounting entry which can increase expenses and asset and can decrease

the liability or equity account of a transaction. Credit is another accounting entry which

increases the income and liability and decreases the expenses and asset.

Debit and credit use to monitor the incoming and outgoing transaction of a business and

help the business to use the double-entry system.

Part F Identify the basic steps in the recording process?

The basic steps in the recording process of accounting are

Analysing the financial transaction

Prepare the journal entries based on the given information

Posting the entries in the ledger accounts formats

Based on the ledger, prepare the trial balance and then the financial statement.

Part G Explain what a journal is and how it helps in the recording process.

Journal is an accounts transaction which records all the financial data by allotting the

accounts names with debit and credit. It is a detailed financial transaction which used in

reconciling the future transaction.

Journal helps in the recording process as it completely discloses the effect of any

transaction; it records a systematic accounting transaction and locates the errors that

delivered while in debiting or crediting.

9 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part H Explain what a general ledger is and how it helps in the recording process

The general ledger is simply recording of journal entries of a business transaction in a

financial format with the debit and credit accounting records and then posting in a trial

balance.

General ledger helps in recording each accounts financial transaction in single account

entry and their transaction. Each account is separated from one other, which can be an

asset, liability, revenue, Cash or anything account.

Part I Explain what posting is and how it helps in the recording process

Ledger posting is an accounting entry from journal to record single account transaction.

Ledger post the single account-related information.

It helps in the recording process of a single account entry to multiple accounts which

distinguish the different account information in their respective ledger account.

Part J Explain the purposes of a trial balance.

The purpose of the trial balance is to check whether the general ledger posting is properly

balanced or not. It checks the account balance of each account and the financial

transaction entry is recorded properly or not. It records the details manually to check and

understand.

Part K Describe the accounting information system and the steps in the recording process.

The accounting information system (AIS) is a structure that a business use to store, collect,

manage, retrieve and record the financial information to guide its accountant, auditor,

analyst, managers and chief officer of the business.

Steps in the recording process are

Analysing the transaction of the account

Preparing the journal by entering the information

Transfer the required entries and posting a journal ledger

Preparing the trial balance based on the ledger account balances.

Part L Identify the elements of each of the four main financial statements?

The four main financial statements are

Income statements, termed as Profit or Loss account, generate the profit or loss of

the business by listing income and expenses.

The balance sheet shows the financial position of a business that is asset, liability

and equity.

Cash flow statement shows the changes in the cash and cash equivalent over a

given period.

Statement of equity and its changes related to the statement of retained earnings

of the owner’s equity which obtained from net profit after tax, dividend payments,

10 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

The general ledger is simply recording of journal entries of a business transaction in a

financial format with the debit and credit accounting records and then posting in a trial

balance.

General ledger helps in recording each accounts financial transaction in single account

entry and their transaction. Each account is separated from one other, which can be an

asset, liability, revenue, Cash or anything account.

Part I Explain what posting is and how it helps in the recording process

Ledger posting is an accounting entry from journal to record single account transaction.

Ledger post the single account-related information.

It helps in the recording process of a single account entry to multiple accounts which

distinguish the different account information in their respective ledger account.

Part J Explain the purposes of a trial balance.

The purpose of the trial balance is to check whether the general ledger posting is properly

balanced or not. It checks the account balance of each account and the financial

transaction entry is recorded properly or not. It records the details manually to check and

understand.

Part K Describe the accounting information system and the steps in the recording process.

The accounting information system (AIS) is a structure that a business use to store, collect,

manage, retrieve and record the financial information to guide its accountant, auditor,

analyst, managers and chief officer of the business.

Steps in the recording process are

Analysing the transaction of the account

Preparing the journal by entering the information

Transfer the required entries and posting a journal ledger

Preparing the trial balance based on the ledger account balances.

Part L Identify the elements of each of the four main financial statements?

The four main financial statements are

Income statements, termed as Profit or Loss account, generate the profit or loss of

the business by listing income and expenses.

The balance sheet shows the financial position of a business that is asset, liability

and equity.

Cash flow statement shows the changes in the cash and cash equivalent over a

given period.

Statement of equity and its changes related to the statement of retained earnings

of the owner’s equity which obtained from net profit after tax, dividend payments,

10 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

share capital, gains and losses in equity.

11 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

11 | Accounting for Business: Individual hand-written assignment, T3 Year 2019

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.