AV Roe PLC: Management Accounting Issues and Investment Appraisal

VerifiedAdded on 2023/01/12

|22

|3695

|29

Report

AI Summary

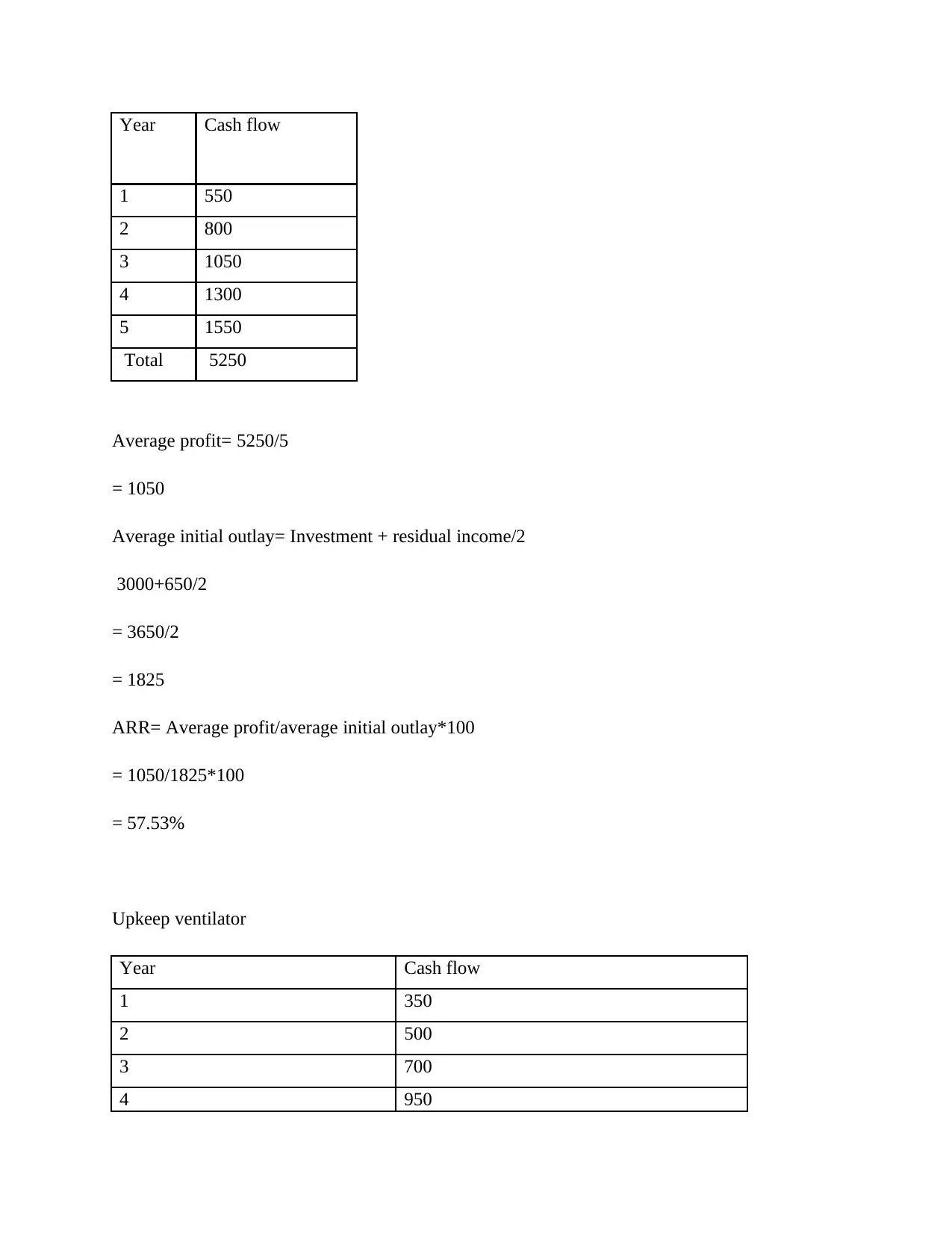

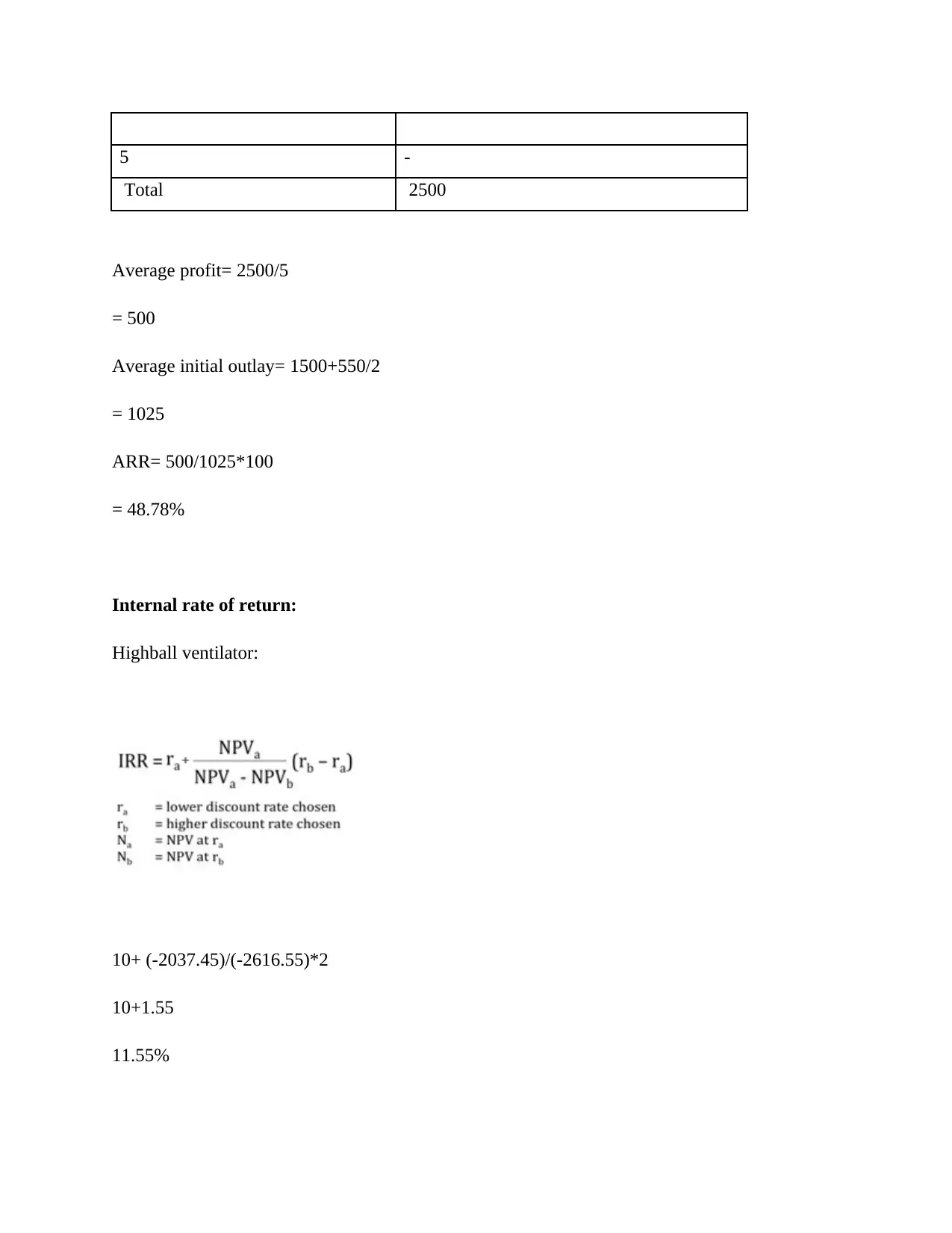

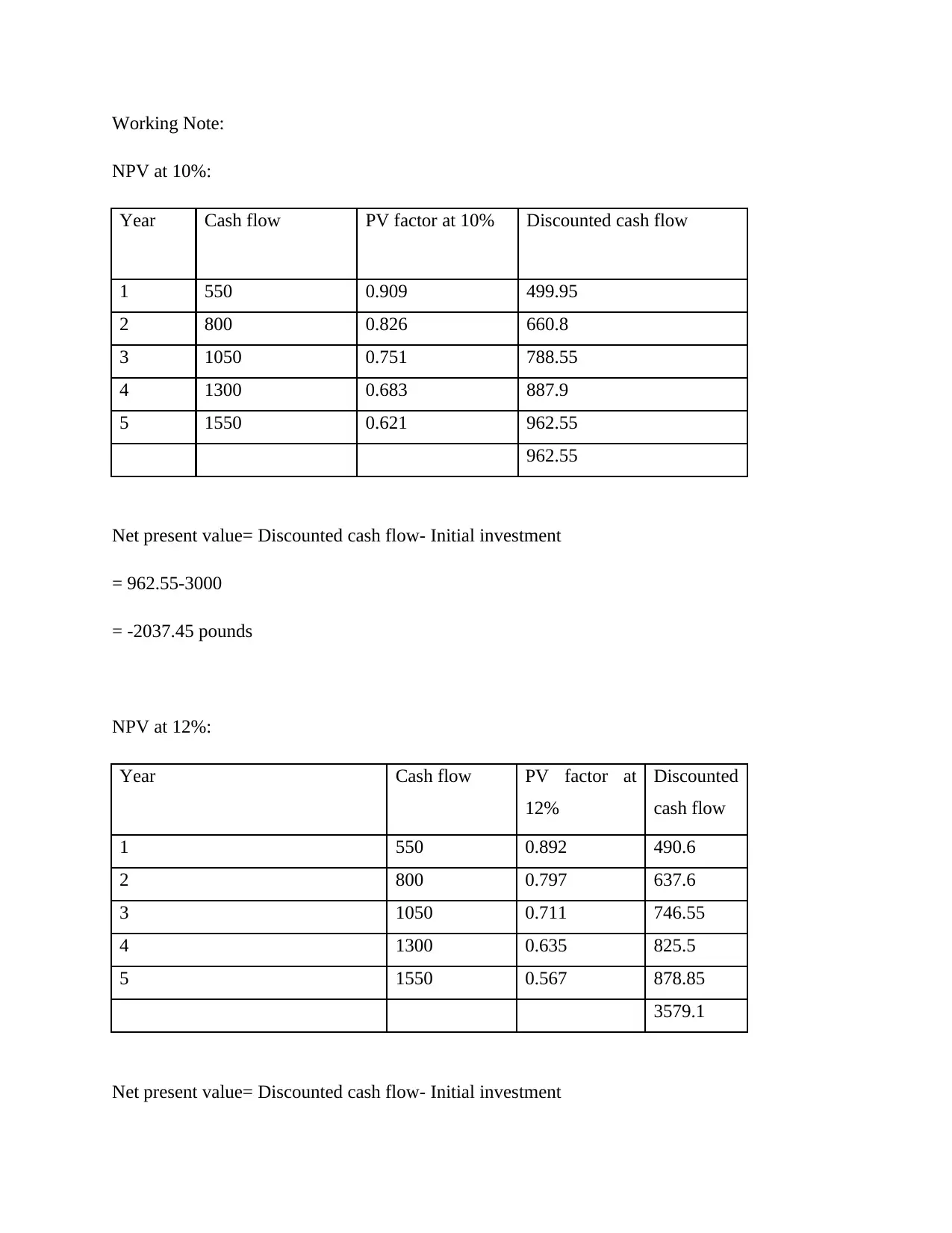

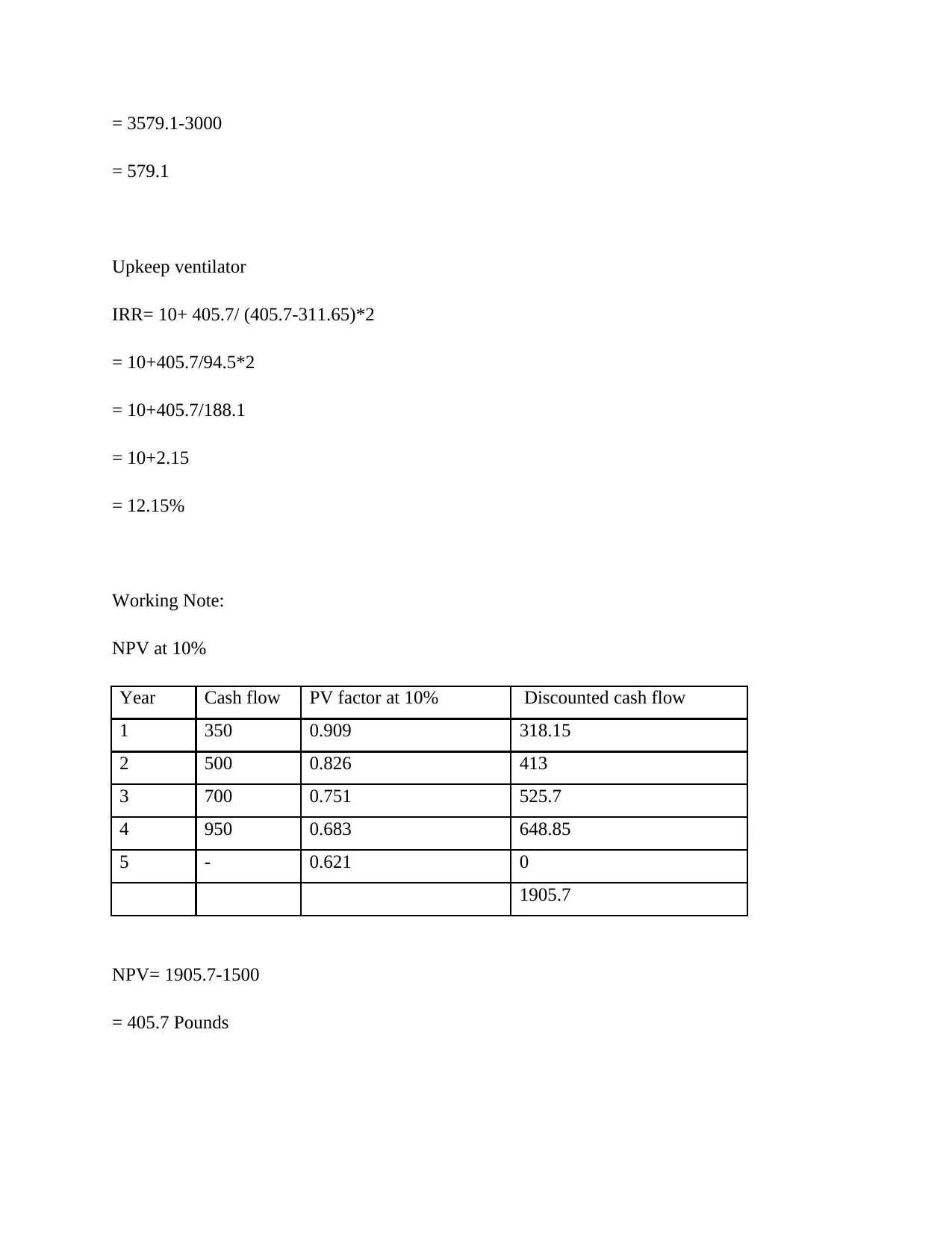

This report provides a detailed analysis of management accounting issues at AV Roe PLC, a company transitioning into medical equipment production. The report addresses three key issues: capital investment appraisal for ventilator options, surgical mask costing analysis, and a respiratory Davison budget. The analysis includes calculations for payback period, net present value, accounting rate of return, and internal rate of return to evaluate ventilator investment alternatives. Furthermore, it assesses surgical mask costing through break-even point and margin of safety calculations for different pricing options. The report concludes with recommendations for AV Roe's management based on the financial analysis, discussing the limitations of the methods used.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.