Accounting Assignment: Bad Debts - Journal Entries and Analysis

VerifiedAdded on 2022/08/14

|7

|799

|17

Homework Assignment

AI Summary

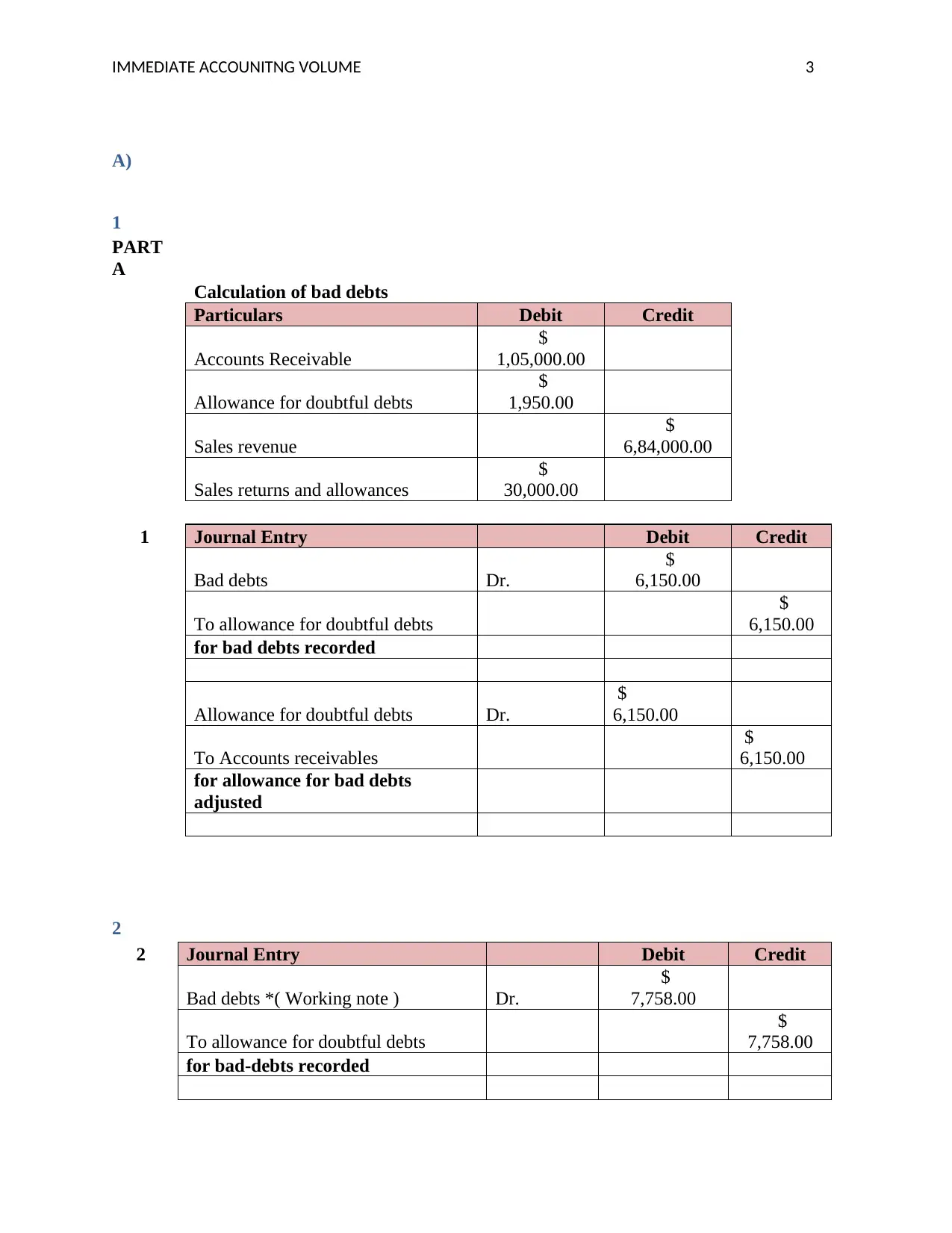

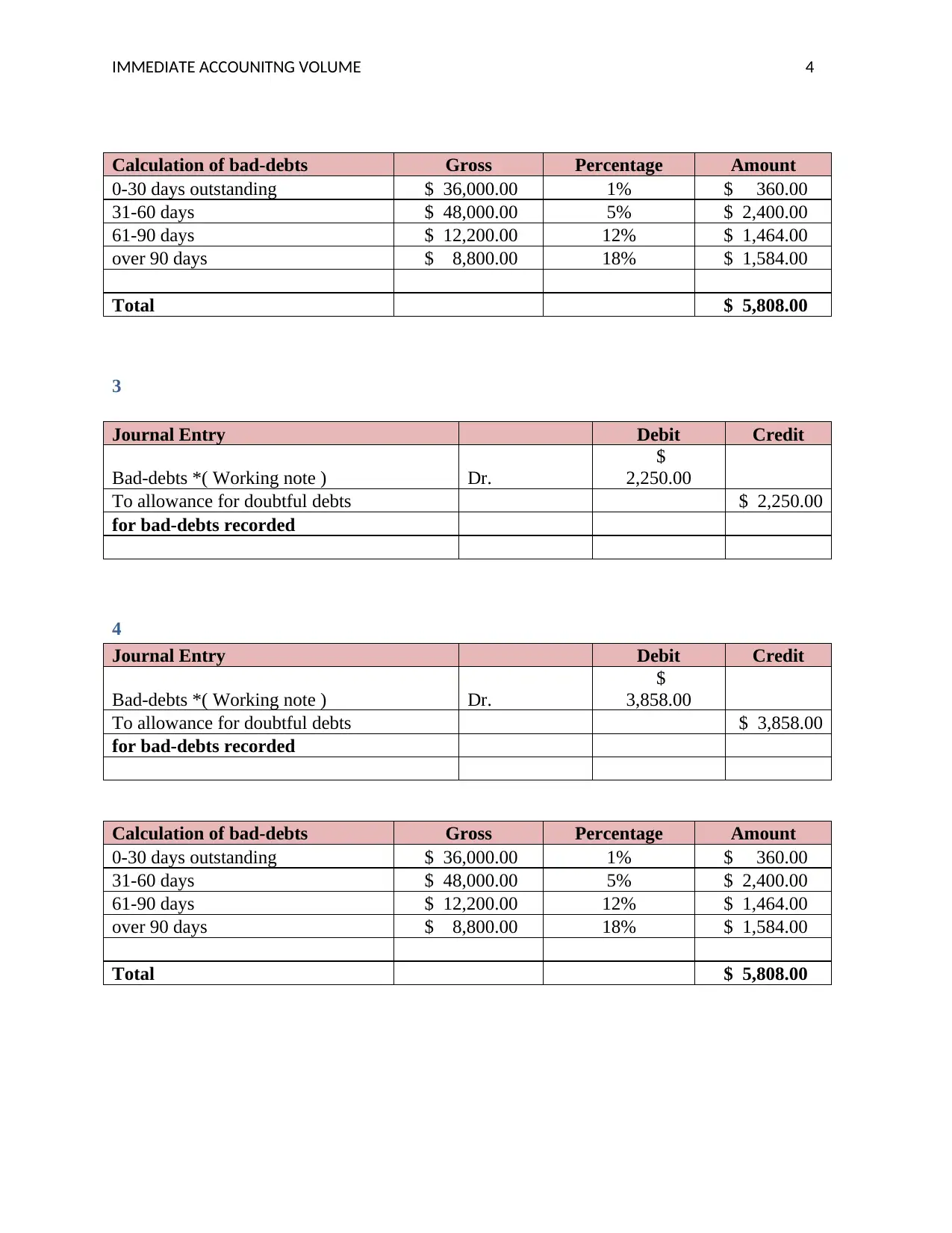

This accounting assignment focuses on the calculation and recording of bad debts. It includes journal entries for bad debt expense and the allowance for doubtful debts, using different methods such as a percentage of sales and aging of accounts receivable. The assignment provides detailed calculations of bad debts and discusses the perspective of an independent viewer of a trial balance, explaining how unadjusted debit balances relate to the provision for doubtful accounts. It further explores the evaluation of lifetime expected credit losses, the use of allowance methods, and the importance of considering current and future economic conditions, including industry and geographic factors. The assignment highlights the consistency of these approaches with IFRS 9, emphasizing the expected loss model.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.