Presentation on Accounting and Bookkeeping Principles and Practices

VerifiedAdded on 2023/02/02

|39

|2291

|71

Presentation

AI Summary

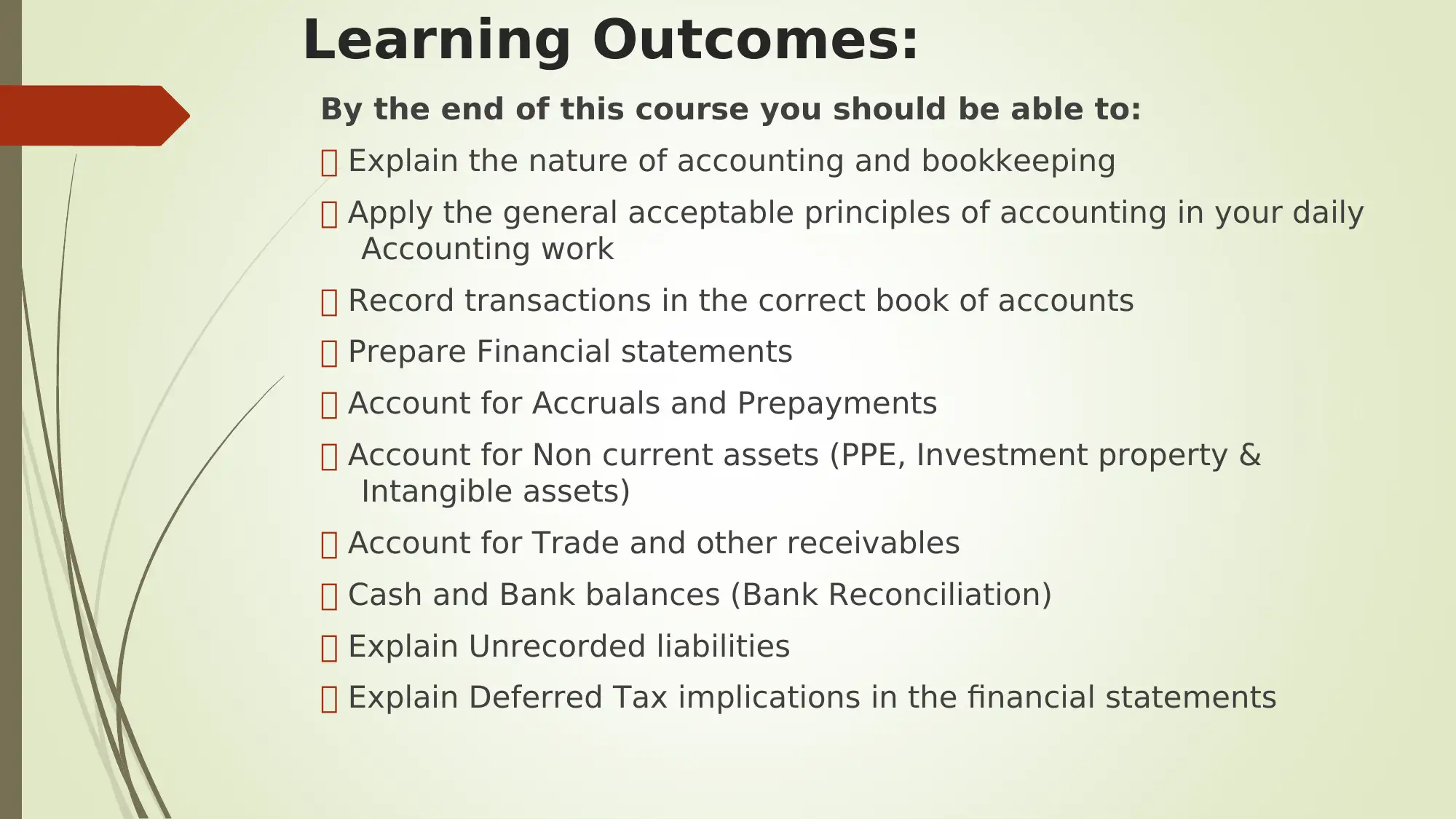

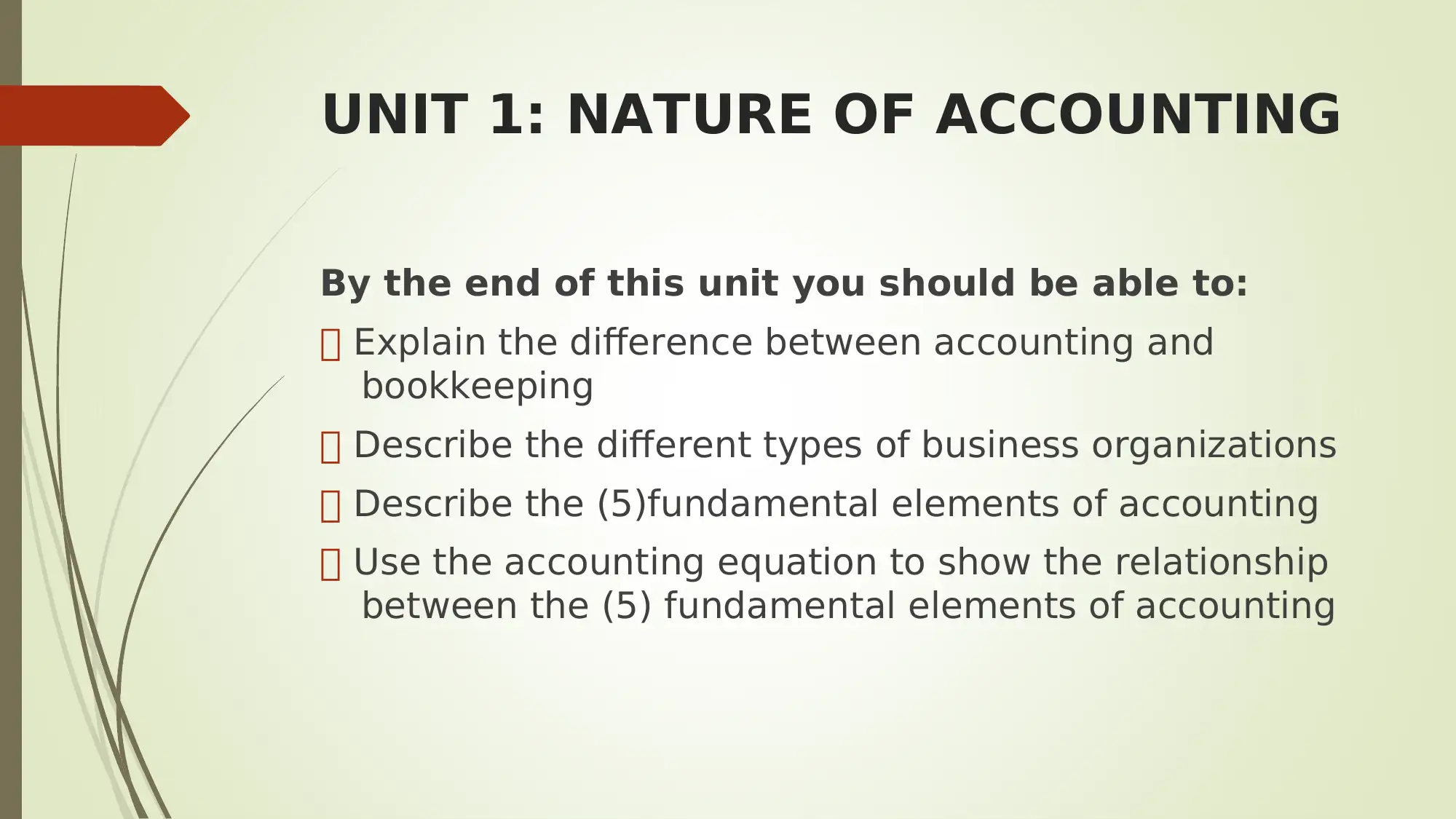

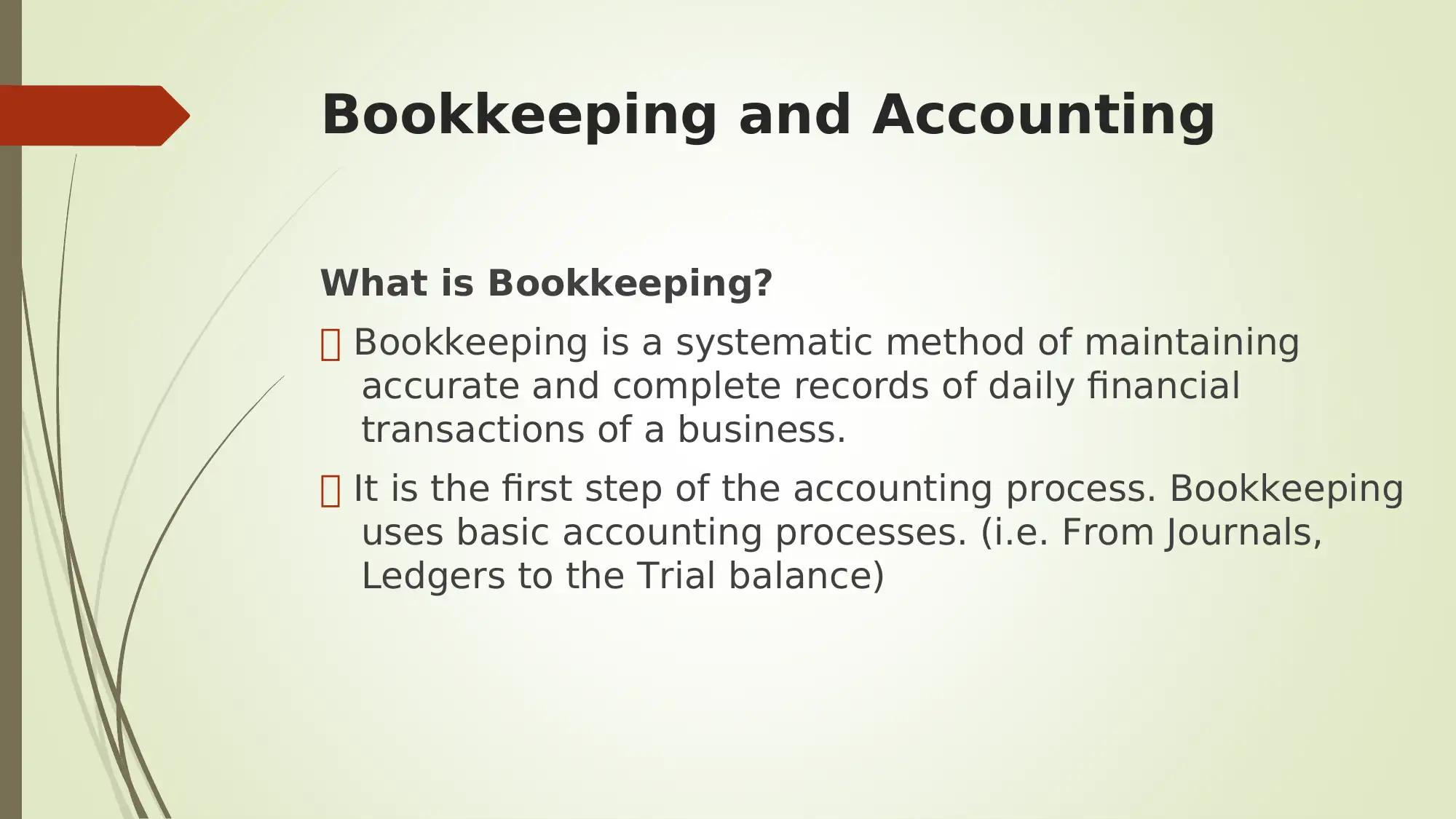

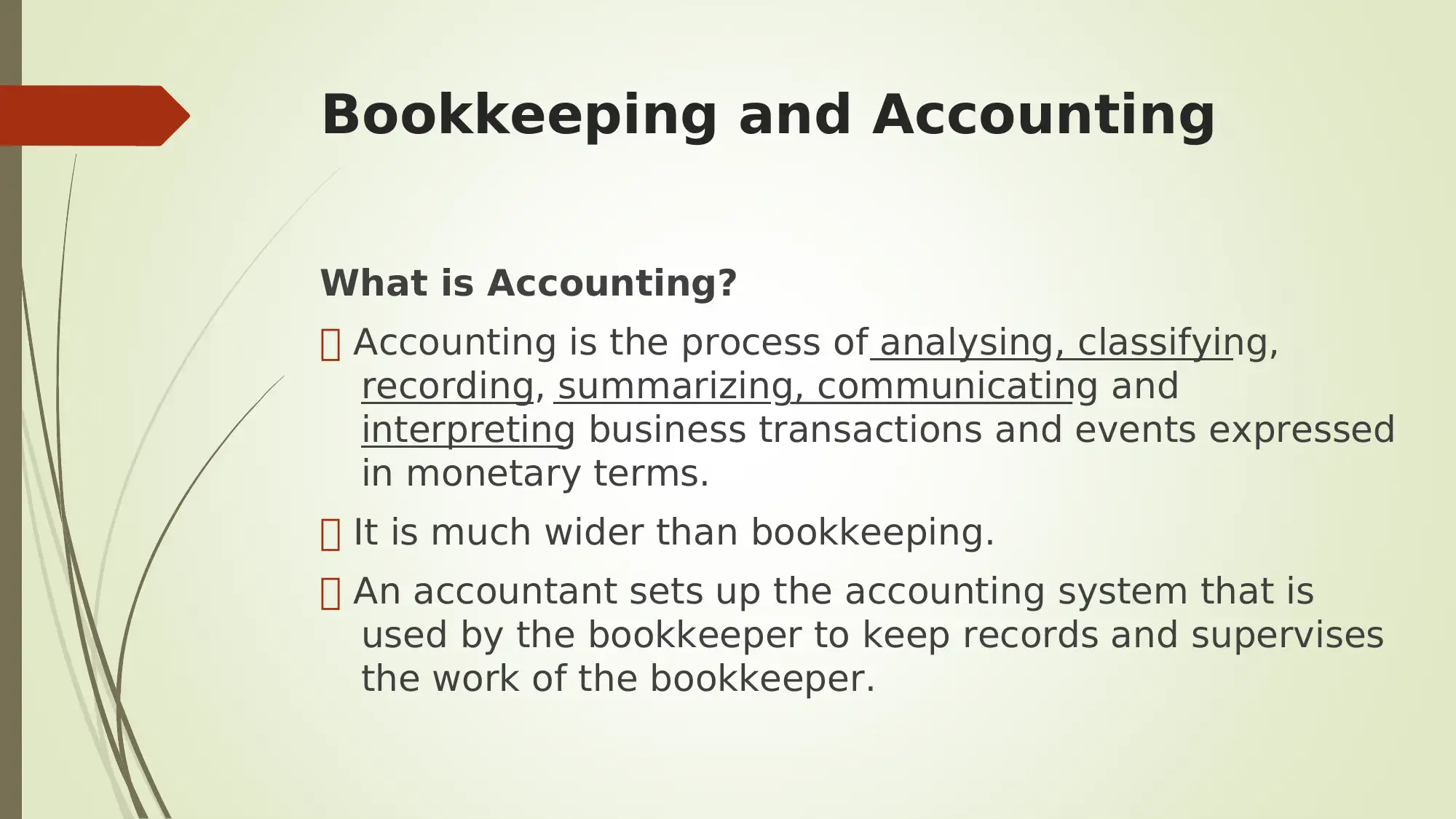

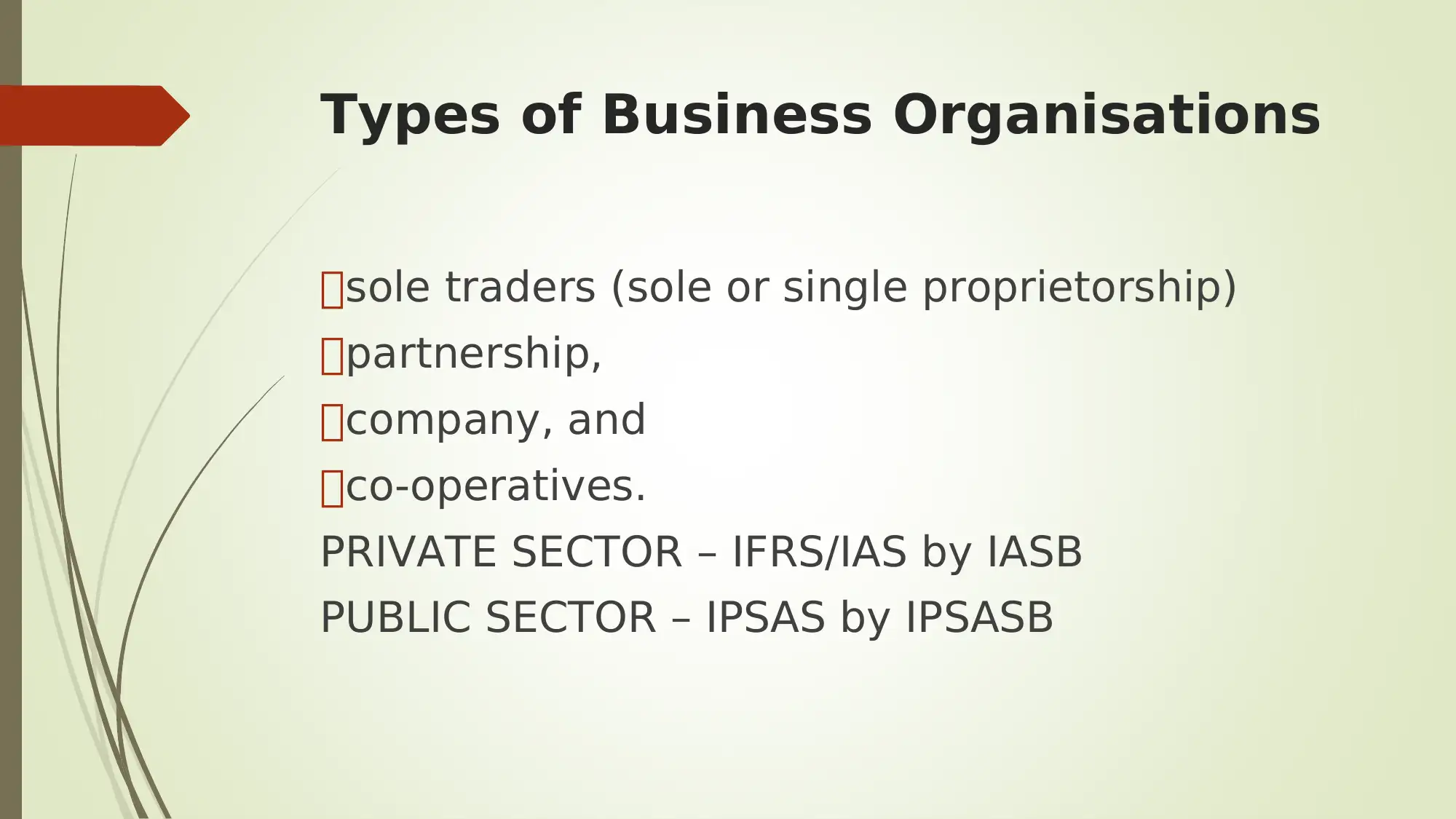

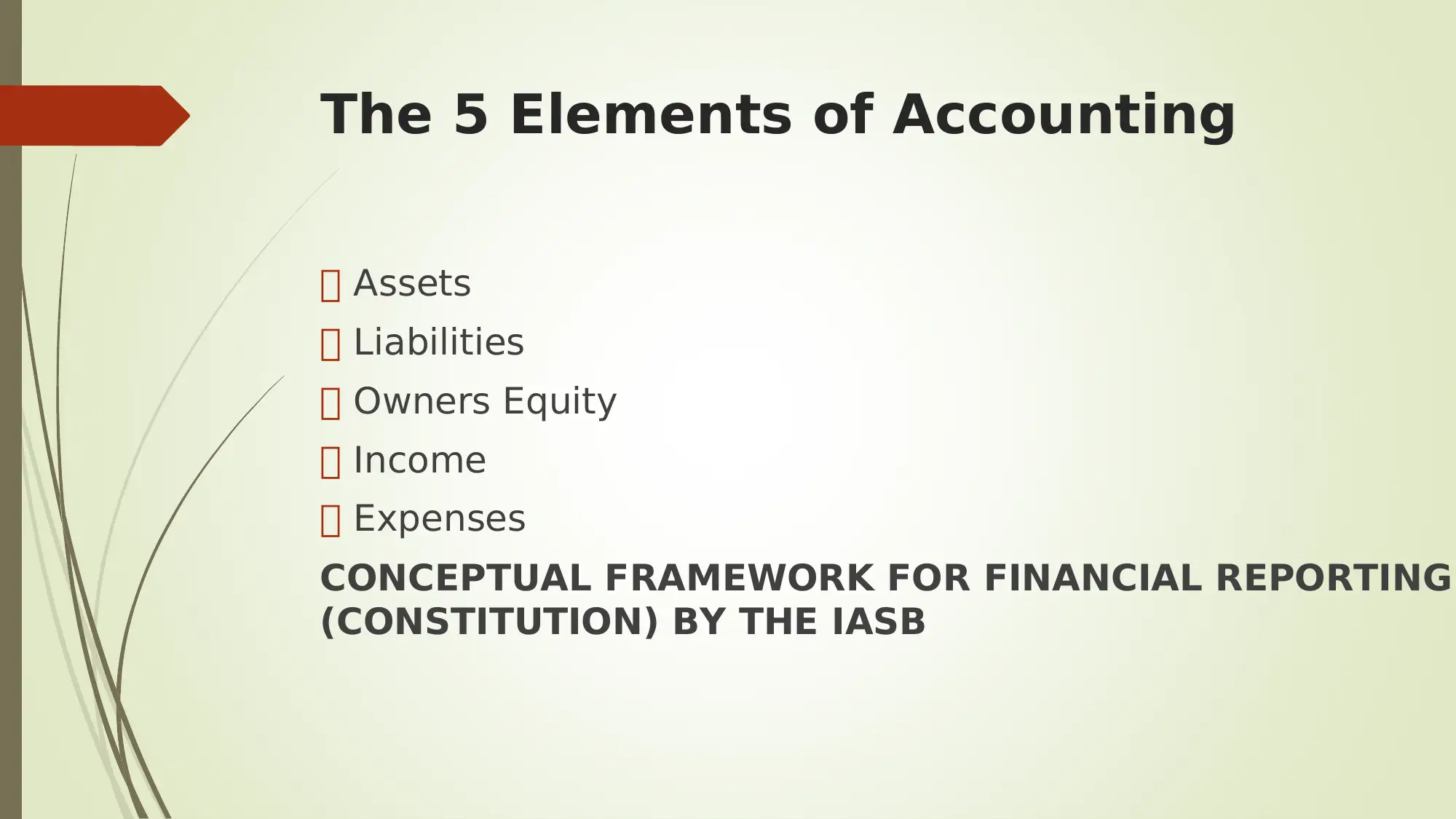

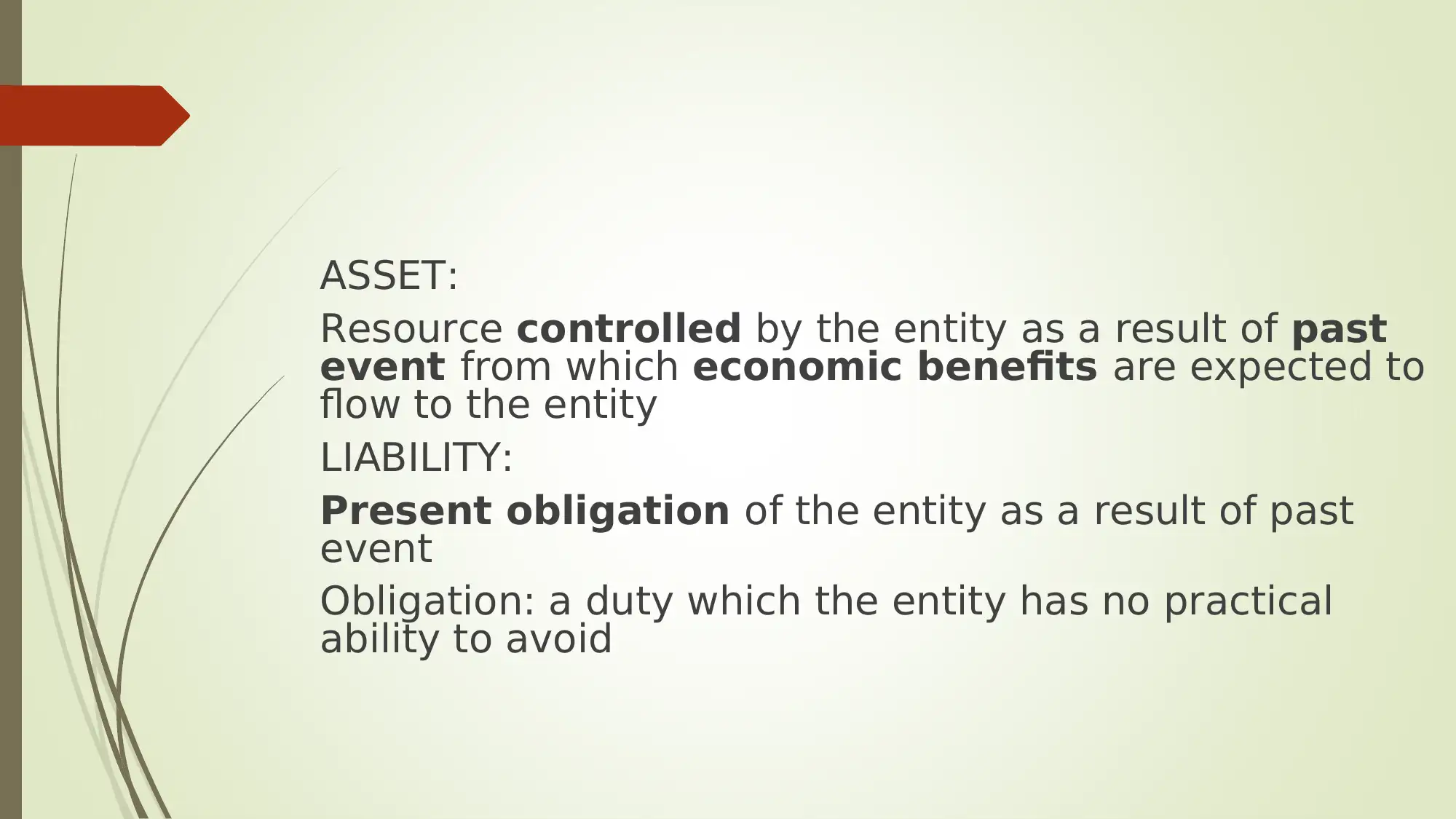

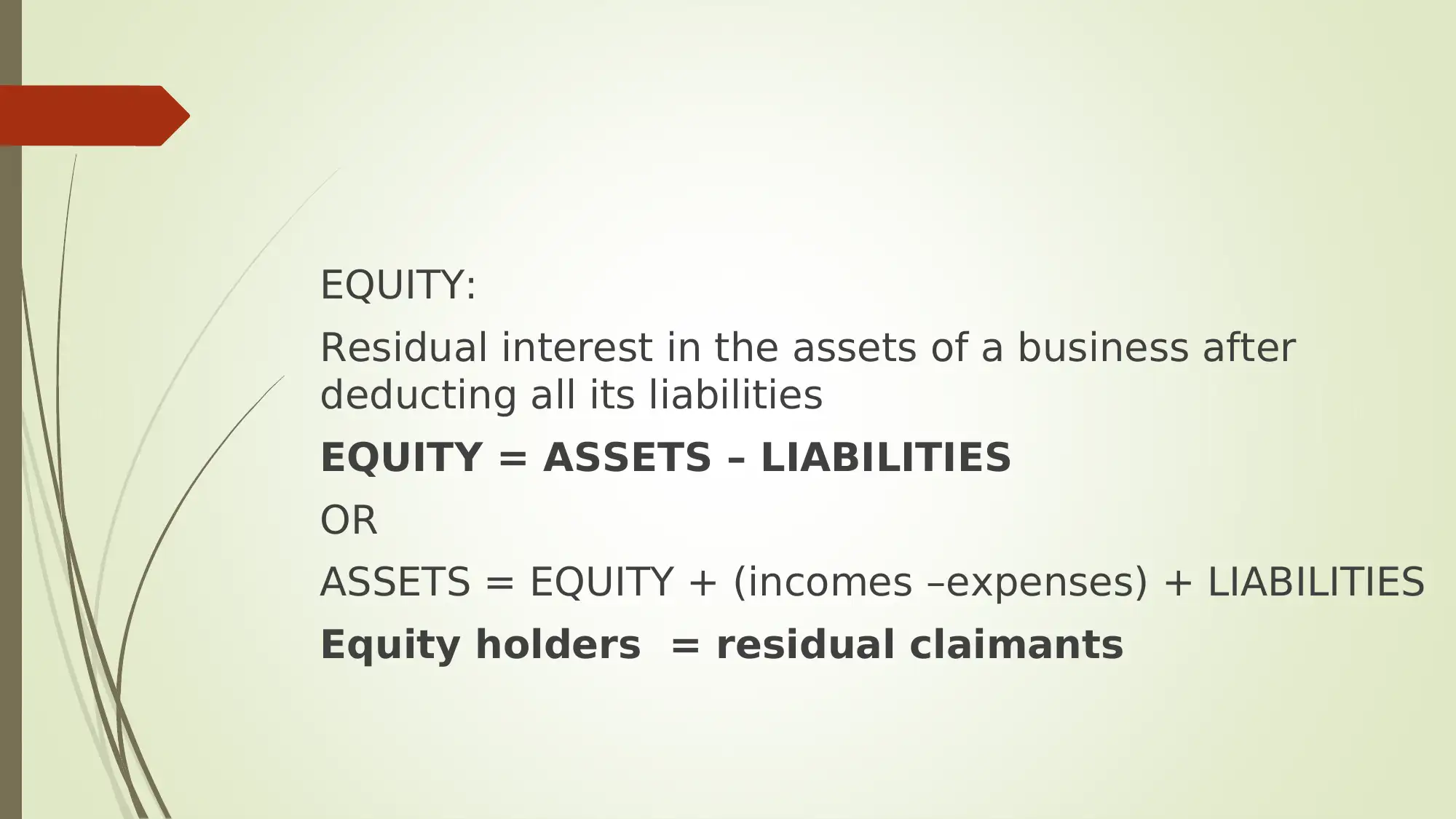

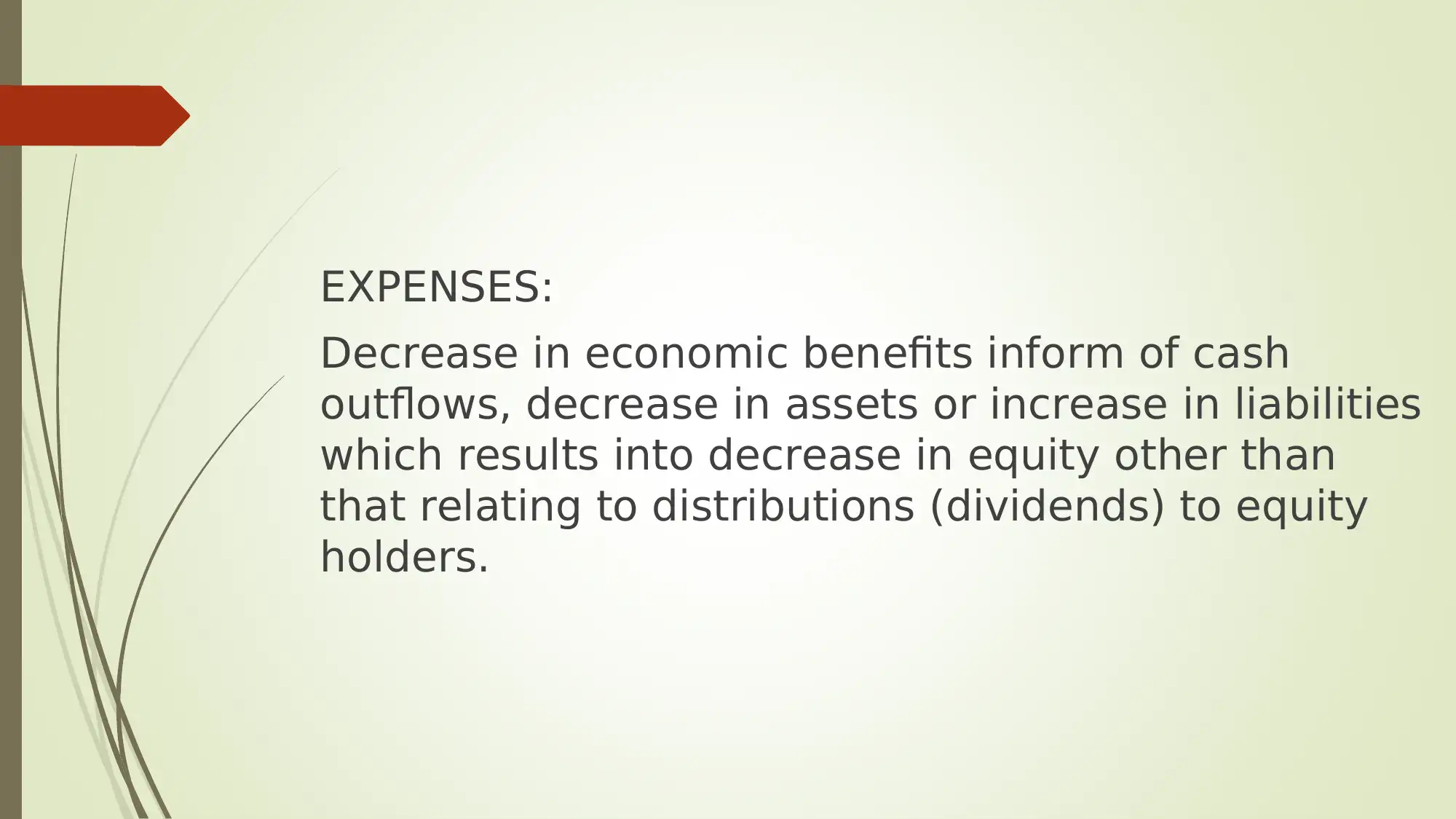

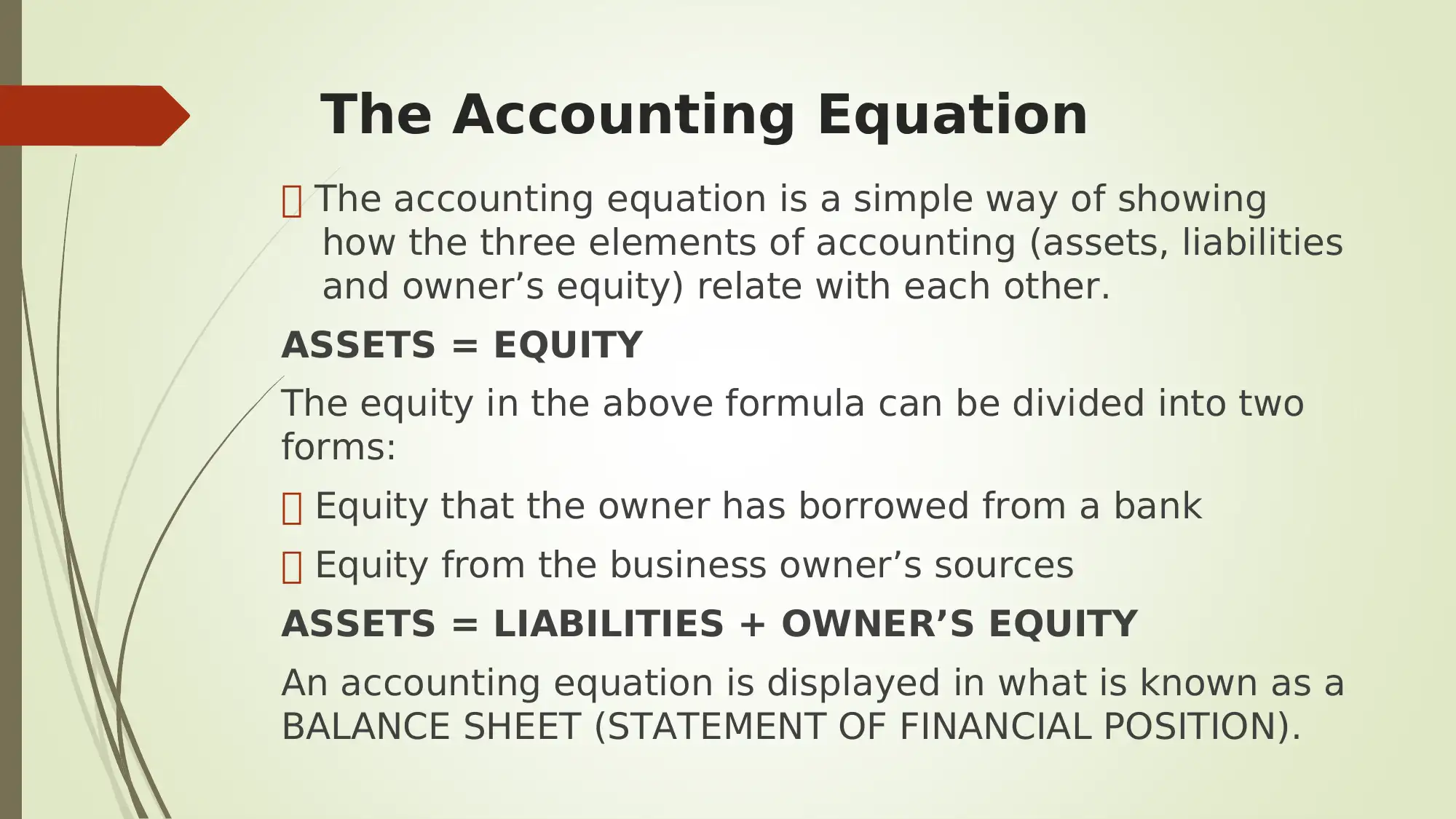

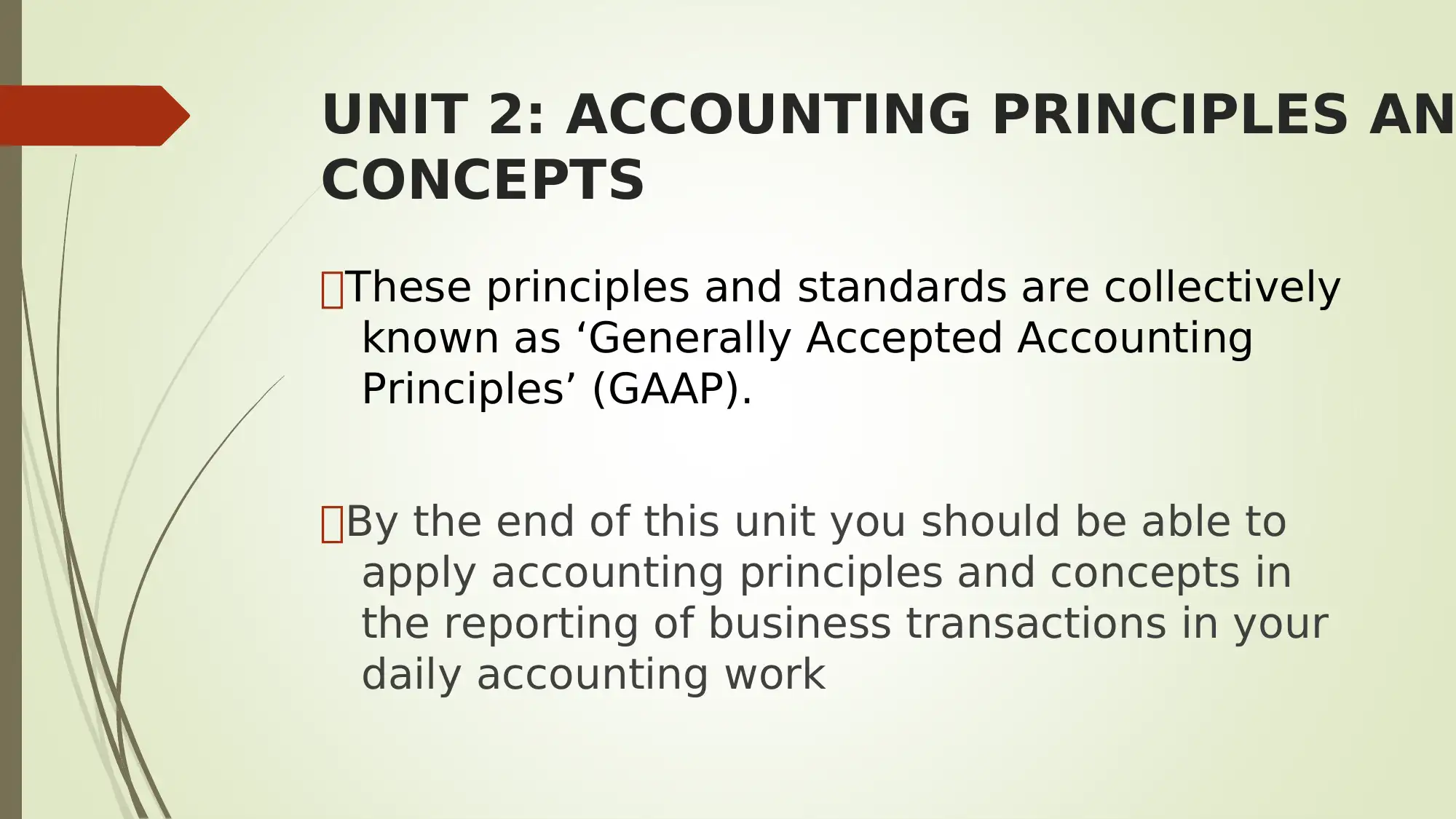

This presentation, delivered by CPA Vicent Laurian, provides a comprehensive overview of bookkeeping and accounting principles. It covers essential topics such as the nature of accounting, the difference between accounting and bookkeeping, and the different types of business organizations. The presentation delves into the five fundamental elements of accounting: assets, liabilities, owner's equity, income, and expenses, and explains the accounting equation. It further explores Generally Accepted Accounting Principles (GAAP), including the business entity, going concern, monetary unit, historical cost, accrual, matching, consistency, materiality, prudence, and substance over form principles. The presentation also covers accounting systems, including journal and ledger entries, and double-entry bookkeeping, with examples. It concludes with an overview of accounting for non-current assets like Property, Plant, and Equipment (PPE), Investment Property, and Intangible Assets, referencing relevant IAS standards. This presentation is a valuable resource for anyone looking to understand the core concepts and practices of accounting and bookkeeping. It's a great resource for students to understand the core concepts and practices of accounting and bookkeeping. Desklib provides past papers and solved assignments to help students excel.

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.