LCBB4001 Accounting Fundamentals: Break-Even and Management Accounting

VerifiedAdded on 2022/12/29

|7

|1528

|88

Report

AI Summary

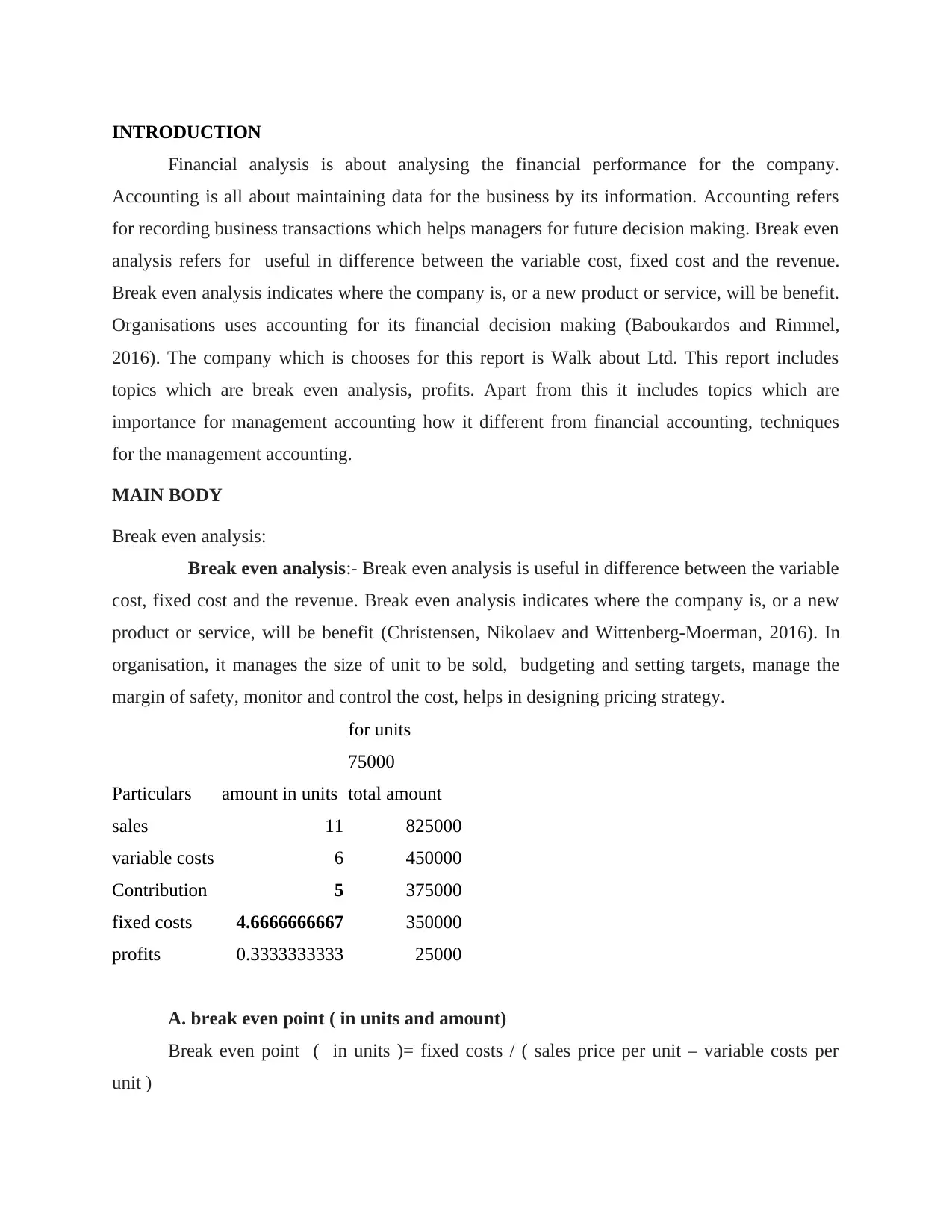

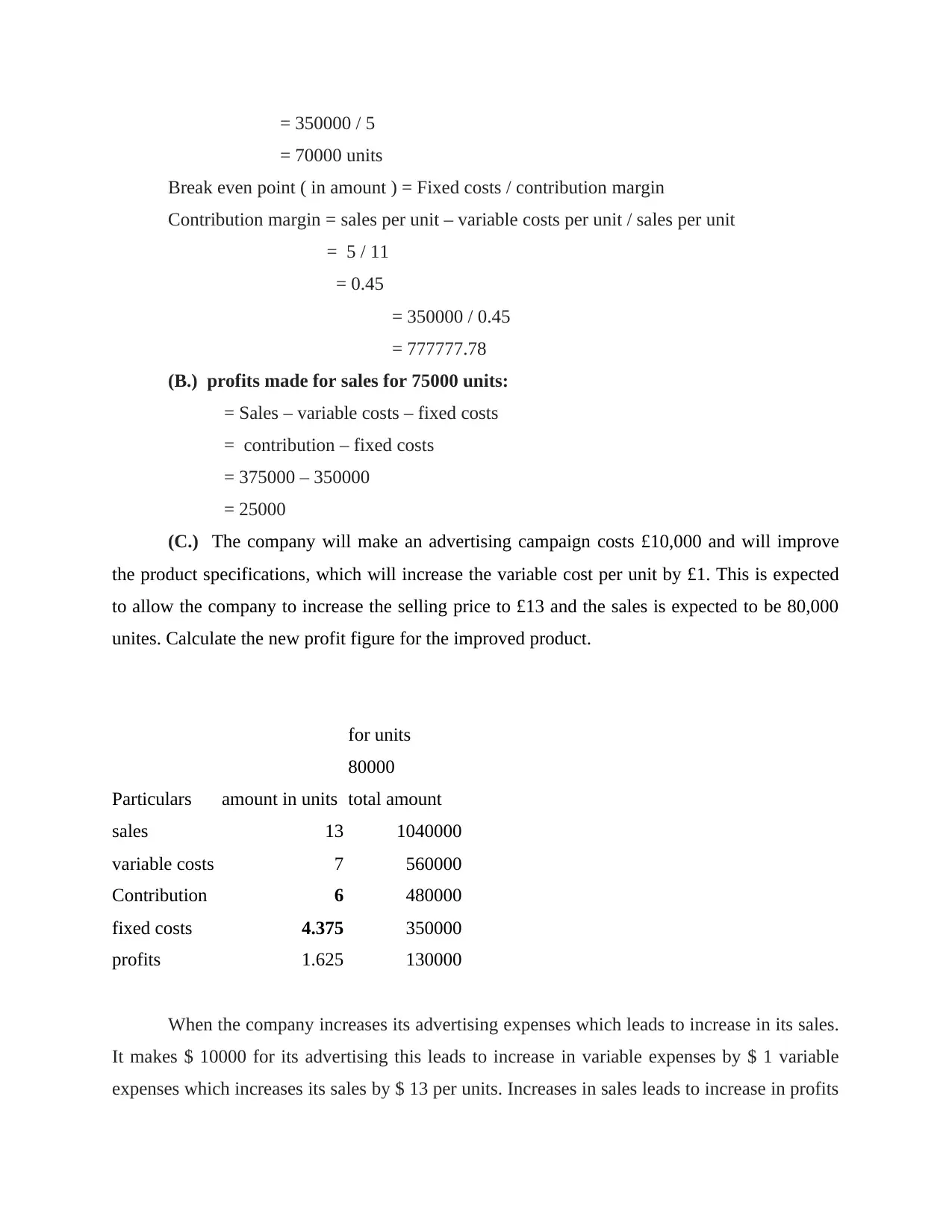

This report provides an in-depth analysis of accounting fundamentals, focusing on break-even analysis, its applications, and limitations within the context of a company, Walk about Ltd. The report delves into the calculation of break-even points, profit analysis under different scenarios, and the impact of advertising campaigns on profitability. Furthermore, it differentiates between management accounting and financial accounting, highlighting the importance of management accounting for internal decision-making, financial planning and financial statements analysis. The report also covers techniques for management accounting, such as financial planning, financial statement analysis, and historical cost accounting, providing a comprehensive overview of accounting principles and their practical implications for business decision-making. The report also includes references to books and journals related to the topics covered.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.