Accounting and Finance: Breakeven Analysis and Investment Report

VerifiedAdded on 2023/01/05

|14

|3994

|67

Report

AI Summary

This report provides a comprehensive overview of key accounting and finance concepts. It begins with the formulation of an income statement and statement of financial position for Collins Colman Limited, demonstrating an understanding of financial statement analysis. The report then delves into breakeven analysis, calculating contribution, breakeven points, and margin of safety for a microwave product, along with an analysis of a potential business strategy. Furthermore, the report explores investment appraisal techniques, including payback period, accounting rate of return, and net present value, evaluating their merits and limitations. Finally, it discusses the benefits and limitations of using budgets for strategic planning, offering a well-rounded analysis of financial management principles. The report is a valuable resource for students seeking to understand and apply core financial concepts.

Introduction to

Accounting and

Finance

Accounting and

Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Formulation of income statement as well as statement of financial position for Collins Colman

Limited.........................................................................................................................................1

PART B...........................................................................................................................................2

a. Contribution of each microwave covering fixed cost..............................................................2

b. Break-even point and margin of safety in terms of both the units and revenues for each

microwave....................................................................................................................................3

c. Calculation of profit for Parksmead Limited if 60000 units will be produced by it................4

d. Analysis of the strategy of the organisation whether it is good or not....................................4

e. Identification and explanation of assumptions of breakeven model including that the model

could be utilised by different businesses or not...........................................................................5

PART C...........................................................................................................................................6

a. Calculation of Payback period, accounting rate of return and net present value for the

organisation..................................................................................................................................6

b. Analysis of merits and limitations of all the investment appraisal techniques........................7

c. Benefits and limitation of using budget as a tool for strategic planning...............................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

PART A...........................................................................................................................................1

Formulation of income statement as well as statement of financial position for Collins Colman

Limited.........................................................................................................................................1

PART B...........................................................................................................................................2

a. Contribution of each microwave covering fixed cost..............................................................2

b. Break-even point and margin of safety in terms of both the units and revenues for each

microwave....................................................................................................................................3

c. Calculation of profit for Parksmead Limited if 60000 units will be produced by it................4

d. Analysis of the strategy of the organisation whether it is good or not....................................4

e. Identification and explanation of assumptions of breakeven model including that the model

could be utilised by different businesses or not...........................................................................5

PART C...........................................................................................................................................6

a. Calculation of Payback period, accounting rate of return and net present value for the

organisation..................................................................................................................................6

b. Analysis of merits and limitations of all the investment appraisal techniques........................7

c. Benefits and limitation of using budget as a tool for strategic planning...............................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

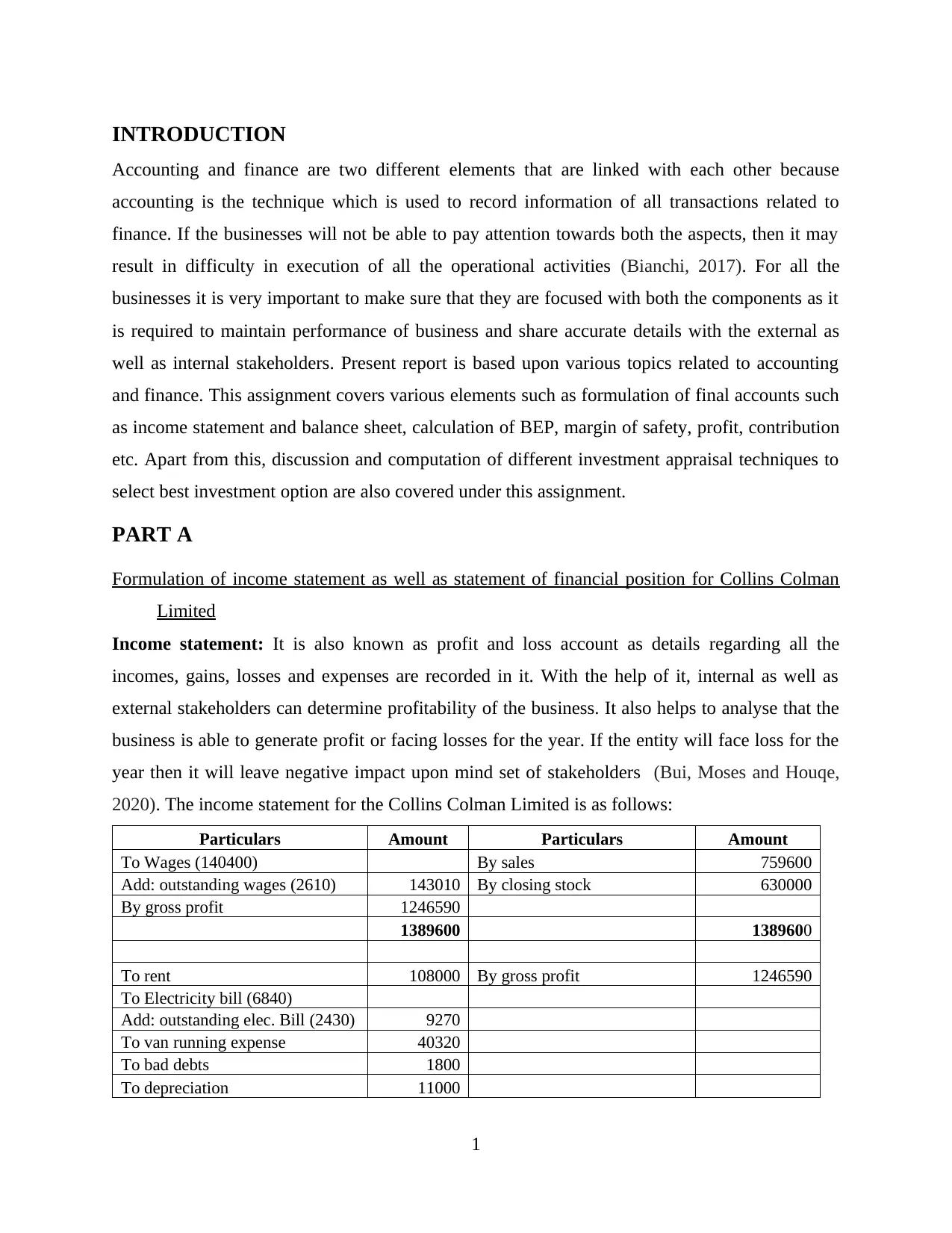

INTRODUCTION

Accounting and finance are two different elements that are linked with each other because

accounting is the technique which is used to record information of all transactions related to

finance. If the businesses will not be able to pay attention towards both the aspects, then it may

result in difficulty in execution of all the operational activities (Bianchi, 2017). For all the

businesses it is very important to make sure that they are focused with both the components as it

is required to maintain performance of business and share accurate details with the external as

well as internal stakeholders. Present report is based upon various topics related to accounting

and finance. This assignment covers various elements such as formulation of final accounts such

as income statement and balance sheet, calculation of BEP, margin of safety, profit, contribution

etc. Apart from this, discussion and computation of different investment appraisal techniques to

select best investment option are also covered under this assignment.

PART A

Formulation of income statement as well as statement of financial position for Collins Colman

Limited

Income statement: It is also known as profit and loss account as details regarding all the

incomes, gains, losses and expenses are recorded in it. With the help of it, internal as well as

external stakeholders can determine profitability of the business. It also helps to analyse that the

business is able to generate profit or facing losses for the year. If the entity will face loss for the

year then it will leave negative impact upon mind set of stakeholders (Bui, Moses and Houqe,

2020). The income statement for the Collins Colman Limited is as follows:

Particulars Amount Particulars Amount

To Wages (140400) By sales 759600

Add: outstanding wages (2610) 143010 By closing stock 630000

By gross profit 1246590

1389600 1389600

To rent 108000 By gross profit 1246590

To Electricity bill (6840)

Add: outstanding elec. Bill (2430) 9270

To van running expense 40320

To bad debts 1800

To depreciation 11000

1

Accounting and finance are two different elements that are linked with each other because

accounting is the technique which is used to record information of all transactions related to

finance. If the businesses will not be able to pay attention towards both the aspects, then it may

result in difficulty in execution of all the operational activities (Bianchi, 2017). For all the

businesses it is very important to make sure that they are focused with both the components as it

is required to maintain performance of business and share accurate details with the external as

well as internal stakeholders. Present report is based upon various topics related to accounting

and finance. This assignment covers various elements such as formulation of final accounts such

as income statement and balance sheet, calculation of BEP, margin of safety, profit, contribution

etc. Apart from this, discussion and computation of different investment appraisal techniques to

select best investment option are also covered under this assignment.

PART A

Formulation of income statement as well as statement of financial position for Collins Colman

Limited

Income statement: It is also known as profit and loss account as details regarding all the

incomes, gains, losses and expenses are recorded in it. With the help of it, internal as well as

external stakeholders can determine profitability of the business. It also helps to analyse that the

business is able to generate profit or facing losses for the year. If the entity will face loss for the

year then it will leave negative impact upon mind set of stakeholders (Bui, Moses and Houqe,

2020). The income statement for the Collins Colman Limited is as follows:

Particulars Amount Particulars Amount

To Wages (140400) By sales 759600

Add: outstanding wages (2610) 143010 By closing stock 630000

By gross profit 1246590

1389600 1389600

To rent 108000 By gross profit 1246590

To Electricity bill (6840)

Add: outstanding elec. Bill (2430) 9270

To van running expense 40320

To bad debts 1800

To depreciation 11000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

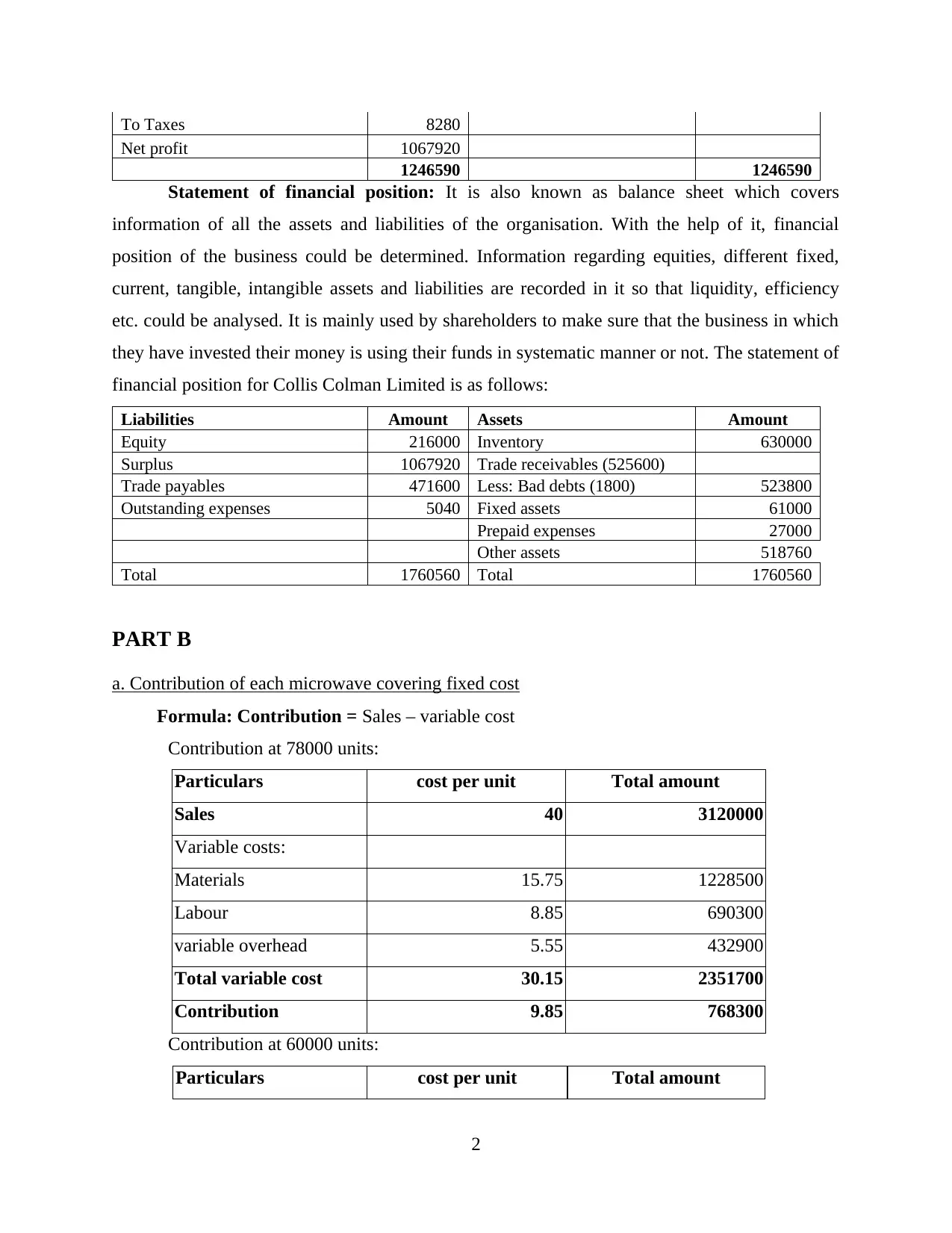

To Taxes 8280

Net profit 1067920

1246590 1246590

Statement of financial position: It is also known as balance sheet which covers

information of all the assets and liabilities of the organisation. With the help of it, financial

position of the business could be determined. Information regarding equities, different fixed,

current, tangible, intangible assets and liabilities are recorded in it so that liquidity, efficiency

etc. could be analysed. It is mainly used by shareholders to make sure that the business in which

they have invested their money is using their funds in systematic manner or not. The statement of

financial position for Collis Colman Limited is as follows:

Liabilities Amount Assets Amount

Equity 216000 Inventory 630000

Surplus 1067920 Trade receivables (525600)

Trade payables 471600 Less: Bad debts (1800) 523800

Outstanding expenses 5040 Fixed assets 61000

Prepaid expenses 27000

Other assets 518760

Total 1760560 Total 1760560

PART B

a. Contribution of each microwave covering fixed cost

Formula: Contribution = Sales – variable cost

Contribution at 78000 units:

Particulars cost per unit Total amount

Sales 40 3120000

Variable costs:

Materials 15.75 1228500

Labour 8.85 690300

variable overhead 5.55 432900

Total variable cost 30.15 2351700

Contribution 9.85 768300

Contribution at 60000 units:

Particulars cost per unit Total amount

2

Net profit 1067920

1246590 1246590

Statement of financial position: It is also known as balance sheet which covers

information of all the assets and liabilities of the organisation. With the help of it, financial

position of the business could be determined. Information regarding equities, different fixed,

current, tangible, intangible assets and liabilities are recorded in it so that liquidity, efficiency

etc. could be analysed. It is mainly used by shareholders to make sure that the business in which

they have invested their money is using their funds in systematic manner or not. The statement of

financial position for Collis Colman Limited is as follows:

Liabilities Amount Assets Amount

Equity 216000 Inventory 630000

Surplus 1067920 Trade receivables (525600)

Trade payables 471600 Less: Bad debts (1800) 523800

Outstanding expenses 5040 Fixed assets 61000

Prepaid expenses 27000

Other assets 518760

Total 1760560 Total 1760560

PART B

a. Contribution of each microwave covering fixed cost

Formula: Contribution = Sales – variable cost

Contribution at 78000 units:

Particulars cost per unit Total amount

Sales 40 3120000

Variable costs:

Materials 15.75 1228500

Labour 8.85 690300

variable overhead 5.55 432900

Total variable cost 30.15 2351700

Contribution 9.85 768300

Contribution at 60000 units:

Particulars cost per unit Total amount

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

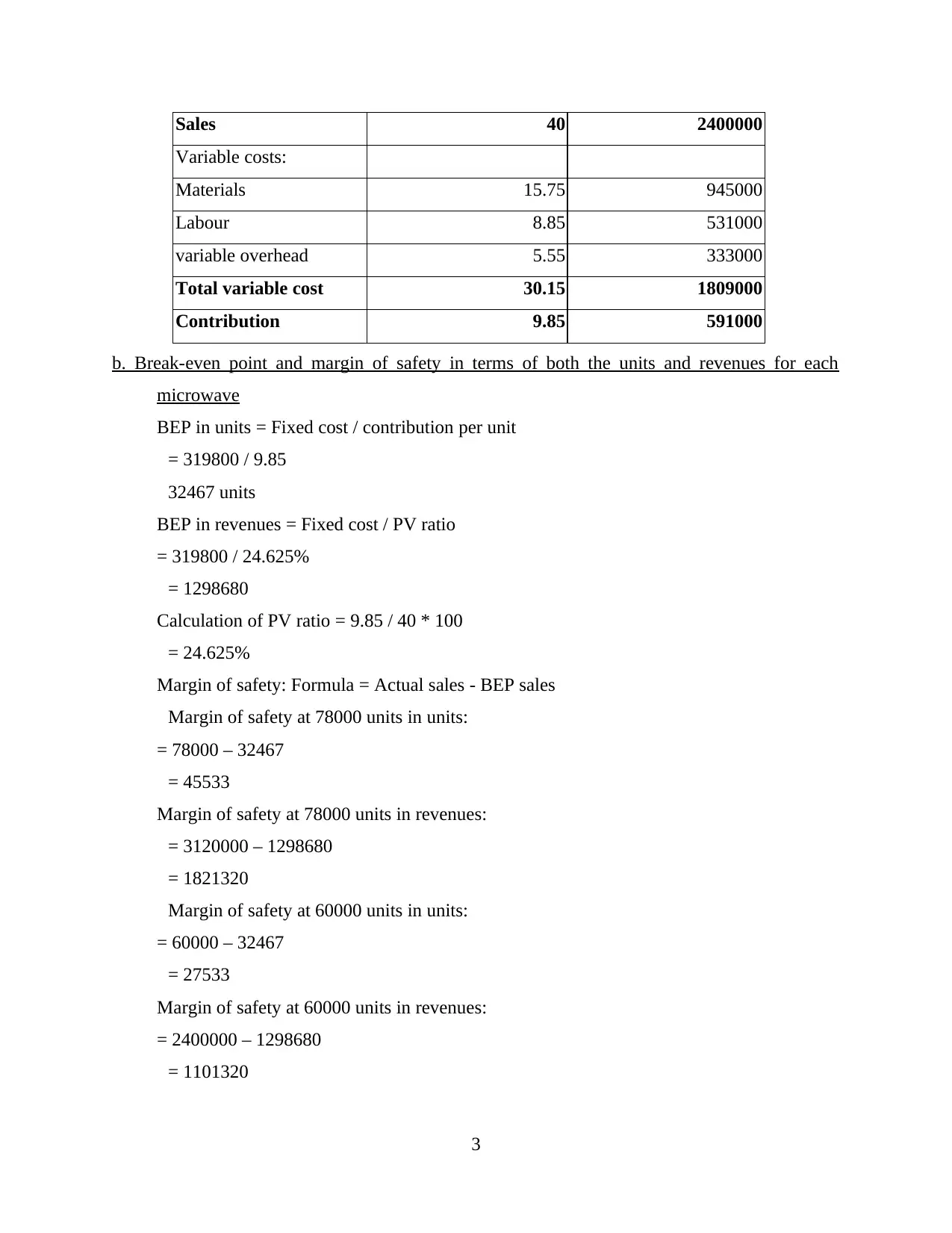

Sales 40 2400000

Variable costs:

Materials 15.75 945000

Labour 8.85 531000

variable overhead 5.55 333000

Total variable cost 30.15 1809000

Contribution 9.85 591000

b. Break-even point and margin of safety in terms of both the units and revenues for each

microwave

BEP in units = Fixed cost / contribution per unit

= 319800 / 9.85

32467 units

BEP in revenues = Fixed cost / PV ratio

= 319800 / 24.625%

= 1298680

Calculation of PV ratio = 9.85 / 40 * 100

= 24.625%

Margin of safety: Formula = Actual sales - BEP sales

Margin of safety at 78000 units in units:

= 78000 – 32467

= 45533

Margin of safety at 78000 units in revenues:

= 3120000 – 1298680

= 1821320

Margin of safety at 60000 units in units:

= 60000 – 32467

= 27533

Margin of safety at 60000 units in revenues:

= 2400000 – 1298680

= 1101320

3

Variable costs:

Materials 15.75 945000

Labour 8.85 531000

variable overhead 5.55 333000

Total variable cost 30.15 1809000

Contribution 9.85 591000

b. Break-even point and margin of safety in terms of both the units and revenues for each

microwave

BEP in units = Fixed cost / contribution per unit

= 319800 / 9.85

32467 units

BEP in revenues = Fixed cost / PV ratio

= 319800 / 24.625%

= 1298680

Calculation of PV ratio = 9.85 / 40 * 100

= 24.625%

Margin of safety: Formula = Actual sales - BEP sales

Margin of safety at 78000 units in units:

= 78000 – 32467

= 45533

Margin of safety at 78000 units in revenues:

= 3120000 – 1298680

= 1821320

Margin of safety at 60000 units in units:

= 60000 – 32467

= 27533

Margin of safety at 60000 units in revenues:

= 2400000 – 1298680

= 1101320

3

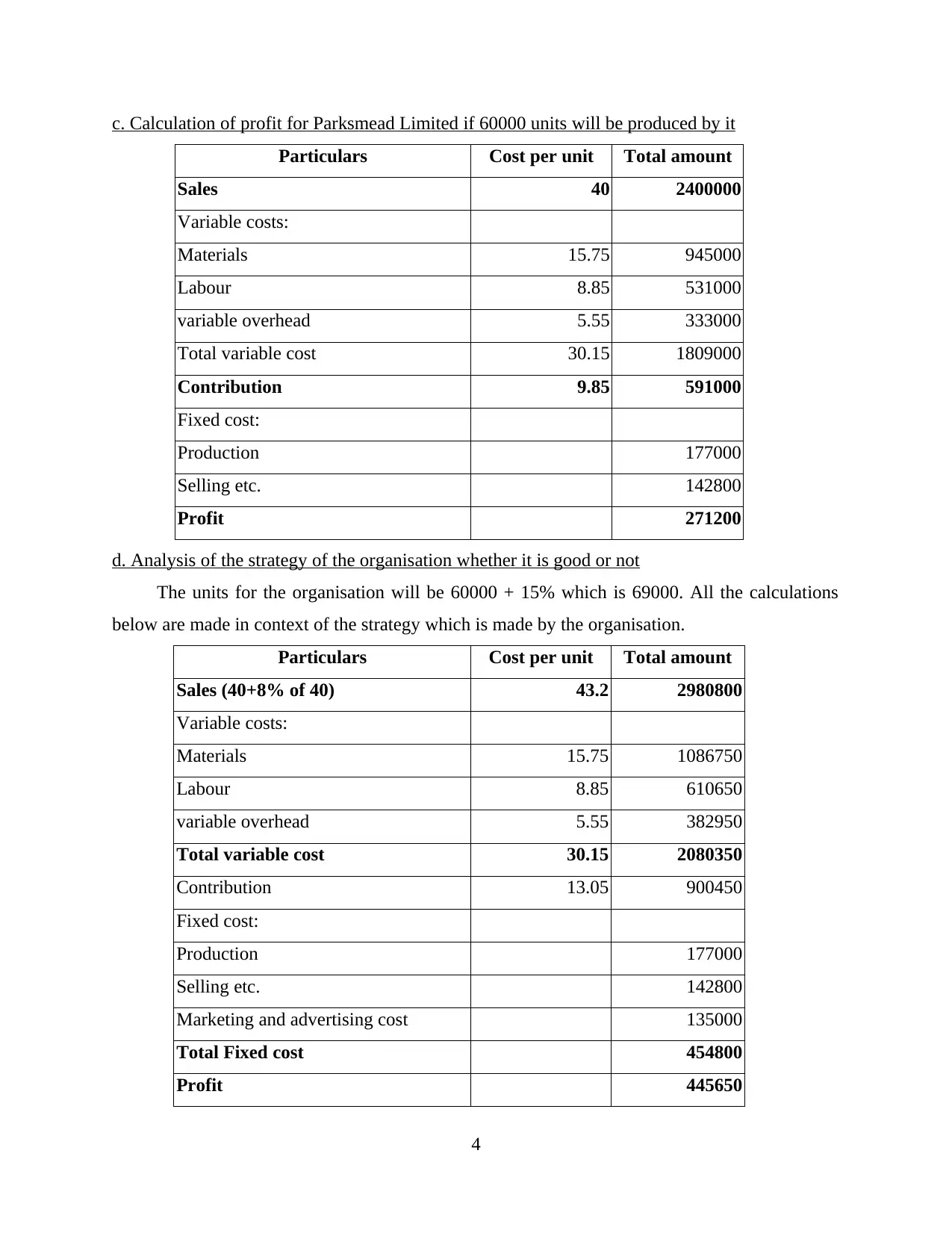

c. Calculation of profit for Parksmead Limited if 60000 units will be produced by it

Particulars Cost per unit Total amount

Sales 40 2400000

Variable costs:

Materials 15.75 945000

Labour 8.85 531000

variable overhead 5.55 333000

Total variable cost 30.15 1809000

Contribution 9.85 591000

Fixed cost:

Production 177000

Selling etc. 142800

Profit 271200

d. Analysis of the strategy of the organisation whether it is good or not

The units for the organisation will be 60000 + 15% which is 69000. All the calculations

below are made in context of the strategy which is made by the organisation.

Particulars Cost per unit Total amount

Sales (40+8% of 40) 43.2 2980800

Variable costs:

Materials 15.75 1086750

Labour 8.85 610650

variable overhead 5.55 382950

Total variable cost 30.15 2080350

Contribution 13.05 900450

Fixed cost:

Production 177000

Selling etc. 142800

Marketing and advertising cost 135000

Total Fixed cost 454800

Profit 445650

4

Particulars Cost per unit Total amount

Sales 40 2400000

Variable costs:

Materials 15.75 945000

Labour 8.85 531000

variable overhead 5.55 333000

Total variable cost 30.15 1809000

Contribution 9.85 591000

Fixed cost:

Production 177000

Selling etc. 142800

Profit 271200

d. Analysis of the strategy of the organisation whether it is good or not

The units for the organisation will be 60000 + 15% which is 69000. All the calculations

below are made in context of the strategy which is made by the organisation.

Particulars Cost per unit Total amount

Sales (40+8% of 40) 43.2 2980800

Variable costs:

Materials 15.75 1086750

Labour 8.85 610650

variable overhead 5.55 382950

Total variable cost 30.15 2080350

Contribution 13.05 900450

Fixed cost:

Production 177000

Selling etc. 142800

Marketing and advertising cost 135000

Total Fixed cost 454800

Profit 445650

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By analysing the results of the strategy which has been planned by Parksmead Ltd is very

effective as the profit by making all the changes is very high. If the organisation will increase

selling price by 8% and production by 15% then it will be very profitable for the entity therefore

it has been recommended to the organisation that it should adopt this strategy.

e. Identification and explanation of assumptions of breakeven model including that the model

could be utilised by different businesses or not

Break even model is used for the purpose of analysing the point where the company will be able

to Following are the assumptions of Break Even Point Model:

Foremost assumption of this model is that all costs can be classified or segregated as

variable or fixed costs. There are some costs which have elements of variable as well as

fixed costs, they are termed as semi variable costs, these costs are ignored while

calculating breakeven point (Chan and Docherty, 2016).

According to this model fixed cost remains constant irrespective of volume of output

produced which may be the case in real life. As when there is increases in level of output

produced, fixed of company also increases. For example, when production increases from

15000 units to 30000 units than equipment requirement of organization may also increase

which may lead to increase in fixed cost of company.

Another assumption states that variable cost of per unit will remain same even at different

levels of production while in reality when output level of firm increases it leads to

reduction in per unit variable cost as there is improvement in economies of scale and

hence company's efficiency increases because of which per unit cost of goods sold

reduces (Gödker and Mertins, 2018).

This model also assumes that selling cost per unit of company remains constant. But as it

is known that it is not the case always.

Scope of machinery breakdown, change in methods of production, change in efficiency

of employees working or change in technology, these factors affects the production of

output at huge level. Still they are ignored while evaluating breakeven point of business.

It is assumed that revenue generated by firm and cost incurred in business is affected by

only one factor, that is, 'Sales volume', while there are several other factors that affect

costs and revenue of company, such as rent, promotion expenses etc.

5

effective as the profit by making all the changes is very high. If the organisation will increase

selling price by 8% and production by 15% then it will be very profitable for the entity therefore

it has been recommended to the organisation that it should adopt this strategy.

e. Identification and explanation of assumptions of breakeven model including that the model

could be utilised by different businesses or not

Break even model is used for the purpose of analysing the point where the company will be able

to Following are the assumptions of Break Even Point Model:

Foremost assumption of this model is that all costs can be classified or segregated as

variable or fixed costs. There are some costs which have elements of variable as well as

fixed costs, they are termed as semi variable costs, these costs are ignored while

calculating breakeven point (Chan and Docherty, 2016).

According to this model fixed cost remains constant irrespective of volume of output

produced which may be the case in real life. As when there is increases in level of output

produced, fixed of company also increases. For example, when production increases from

15000 units to 30000 units than equipment requirement of organization may also increase

which may lead to increase in fixed cost of company.

Another assumption states that variable cost of per unit will remain same even at different

levels of production while in reality when output level of firm increases it leads to

reduction in per unit variable cost as there is improvement in economies of scale and

hence company's efficiency increases because of which per unit cost of goods sold

reduces (Gödker and Mertins, 2018).

This model also assumes that selling cost per unit of company remains constant. But as it

is known that it is not the case always.

Scope of machinery breakdown, change in methods of production, change in efficiency

of employees working or change in technology, these factors affects the production of

output at huge level. Still they are ignored while evaluating breakeven point of business.

It is assumed that revenue generated by firm and cost incurred in business is affected by

only one factor, that is, 'Sales volume', while there are several other factors that affect

costs and revenue of company, such as rent, promotion expenses etc.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This model also states that there will be no change in inventory level of company during

the accounting period.

According to this model, only one type of product is produced by firm, which is not the

case with every company as most of the organizations usually produces more than one

variety of goods (Hutchinson, Mack and Verhoeven, 2017).

All the businesses can use BEP because with the help of it, the entities will be able to

determine the units that are required to be sold by them for recovering all the costs. For example,

if a retail business is willing to generate higher revenues then it will be very important for it to

make sure that it is able to meet the BEP point. It will facilitate the attainment of all the goals

and objectives. On the other hand, if a manufacturing business having goal of profit

maximisation then it will be essential for that business to make sure that it is able to generate

revenues that will result in recovery of all the costs. By analysing the assumptions of BEP it has

been determined that the entities are required to pay attention towards use of BEP as it can help

to meet all the long as well as short term objectives (Hyun, Park and Tian, 2020).

PART C

a. Calculation of Payback period, accounting rate of return and net present value for the

organisation

Provided information:

Cost of machine= 8000000

Cash inflow = 3,400,000

Cash outflow= 1,280,000

Cash inflow= 2120000

Payback period:

Formula: Initial investment / cash inflow

= 8000000 / 2120000

= 3.78 years

Working notes: Calculation of net cash inflow = Cash inflow – cash outflow

= 3400000 – 1280000

= 2120000

Accounting rate of return:

6

the accounting period.

According to this model, only one type of product is produced by firm, which is not the

case with every company as most of the organizations usually produces more than one

variety of goods (Hutchinson, Mack and Verhoeven, 2017).

All the businesses can use BEP because with the help of it, the entities will be able to

determine the units that are required to be sold by them for recovering all the costs. For example,

if a retail business is willing to generate higher revenues then it will be very important for it to

make sure that it is able to meet the BEP point. It will facilitate the attainment of all the goals

and objectives. On the other hand, if a manufacturing business having goal of profit

maximisation then it will be essential for that business to make sure that it is able to generate

revenues that will result in recovery of all the costs. By analysing the assumptions of BEP it has

been determined that the entities are required to pay attention towards use of BEP as it can help

to meet all the long as well as short term objectives (Hyun, Park and Tian, 2020).

PART C

a. Calculation of Payback period, accounting rate of return and net present value for the

organisation

Provided information:

Cost of machine= 8000000

Cash inflow = 3,400,000

Cash outflow= 1,280,000

Cash inflow= 2120000

Payback period:

Formula: Initial investment / cash inflow

= 8000000 / 2120000

= 3.78 years

Working notes: Calculation of net cash inflow = Cash inflow – cash outflow

= 3400000 – 1280000

= 2120000

Accounting rate of return:

6

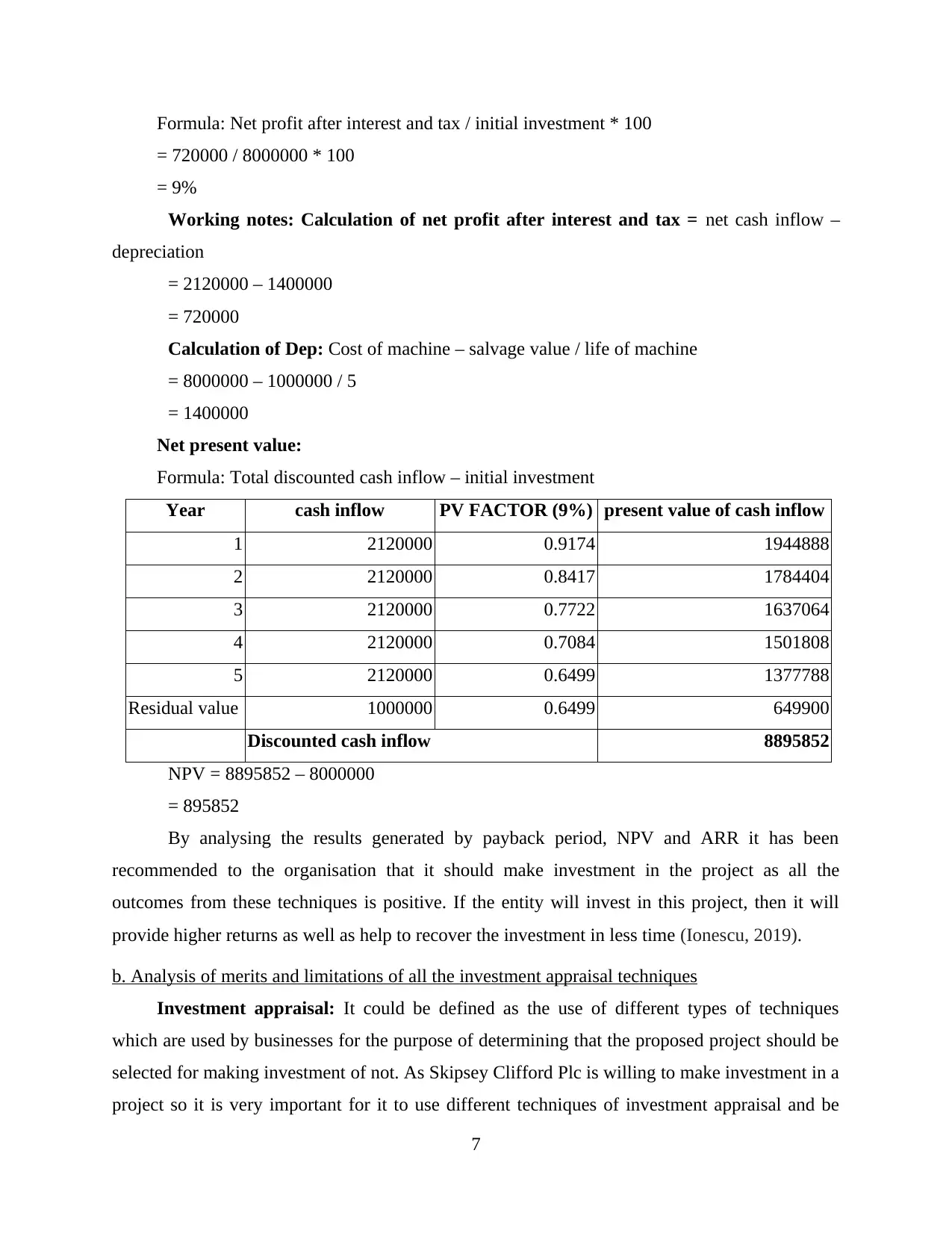

Formula: Net profit after interest and tax / initial investment * 100

= 720000 / 8000000 * 100

= 9%

Working notes: Calculation of net profit after interest and tax = net cash inflow –

depreciation

= 2120000 – 1400000

= 720000

Calculation of Dep: Cost of machine – salvage value / life of machine

= 8000000 – 1000000 / 5

= 1400000

Net present value:

Formula: Total discounted cash inflow – initial investment

Year cash inflow PV FACTOR (9%) present value of cash inflow

1 2120000 0.9174 1944888

2 2120000 0.8417 1784404

3 2120000 0.7722 1637064

4 2120000 0.7084 1501808

5 2120000 0.6499 1377788

Residual value 1000000 0.6499 649900

Discounted cash inflow 8895852

NPV = 8895852 – 8000000

= 895852

By analysing the results generated by payback period, NPV and ARR it has been

recommended to the organisation that it should make investment in the project as all the

outcomes from these techniques is positive. If the entity will invest in this project, then it will

provide higher returns as well as help to recover the investment in less time (Ionescu, 2019).

b. Analysis of merits and limitations of all the investment appraisal techniques

Investment appraisal: It could be defined as the use of different types of techniques

which are used by businesses for the purpose of determining that the proposed project should be

selected for making investment of not. As Skipsey Clifford Plc is willing to make investment in a

project so it is very important for it to use different techniques of investment appraisal and be

7

= 720000 / 8000000 * 100

= 9%

Working notes: Calculation of net profit after interest and tax = net cash inflow –

depreciation

= 2120000 – 1400000

= 720000

Calculation of Dep: Cost of machine – salvage value / life of machine

= 8000000 – 1000000 / 5

= 1400000

Net present value:

Formula: Total discounted cash inflow – initial investment

Year cash inflow PV FACTOR (9%) present value of cash inflow

1 2120000 0.9174 1944888

2 2120000 0.8417 1784404

3 2120000 0.7722 1637064

4 2120000 0.7084 1501808

5 2120000 0.6499 1377788

Residual value 1000000 0.6499 649900

Discounted cash inflow 8895852

NPV = 8895852 – 8000000

= 895852

By analysing the results generated by payback period, NPV and ARR it has been

recommended to the organisation that it should make investment in the project as all the

outcomes from these techniques is positive. If the entity will invest in this project, then it will

provide higher returns as well as help to recover the investment in less time (Ionescu, 2019).

b. Analysis of merits and limitations of all the investment appraisal techniques

Investment appraisal: It could be defined as the use of different types of techniques

which are used by businesses for the purpose of determining that the proposed project should be

selected for making investment of not. As Skipsey Clifford Plc is willing to make investment in a

project so it is very important for it to use different techniques of investment appraisal and be

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

aware of all the advantages and disadvantages of all of them. With the help of it, the managers

will be able to take effective decisions for betterment of business (Liu and O'Neill, 2018). The

discussion of all the techniques along with their advantages and disadvantages is as follows:

Payback period- It means the time taken by the cash flow of the particular project to

cover the initial investment. It is very important for the entities to select the project will short

period of payback period because it will demonstrate that very small period of time is required

for completing the project. If the project with high payback period will be selected, then it will

take longer time to recover the value of initial investment (O'Neill, Wang and Liu, 2016). All the

advantages and disadvantages of this method are as follows:

Advantages of payback period-

This method is easy to use by the organization, because in this only initial investment

and cash inflow is required which is easy to access information. Skipsey Clifford Plc

also use this method to check whether project is complete in short period or not (Oler

and et.al., 2016).

This method is useful for small businesses because it requires small information related

to project, it gives result in short period of time which have limited resources and by

which manager can take decision to reinvest in other projects.

This method provides quick result with the help of less information which is good for

manager to take fast decision related to project. Skipsey Clifford Plc also takes fast

decision related to the equipment in which investment will be made in future (Roberts

and Weikmans, 2017).

Disadvantages of payback period:

This method is does not considers Time value of money which is important criteria for

all businesses as it helps to determine the changes in income which may take place in

future.

It only considers the cash flow which is used for recovering the initial investment.

Accounting rate of return – It means the return which is generated from dividing the

expected average annual profit from initial investment which come from deduct expenses and

then it is check with management rate of return is it is equal then it is accepted (Rompotis, 2017).

Advantages of ARR-

8

will be able to take effective decisions for betterment of business (Liu and O'Neill, 2018). The

discussion of all the techniques along with their advantages and disadvantages is as follows:

Payback period- It means the time taken by the cash flow of the particular project to

cover the initial investment. It is very important for the entities to select the project will short

period of payback period because it will demonstrate that very small period of time is required

for completing the project. If the project with high payback period will be selected, then it will

take longer time to recover the value of initial investment (O'Neill, Wang and Liu, 2016). All the

advantages and disadvantages of this method are as follows:

Advantages of payback period-

This method is easy to use by the organization, because in this only initial investment

and cash inflow is required which is easy to access information. Skipsey Clifford Plc

also use this method to check whether project is complete in short period or not (Oler

and et.al., 2016).

This method is useful for small businesses because it requires small information related

to project, it gives result in short period of time which have limited resources and by

which manager can take decision to reinvest in other projects.

This method provides quick result with the help of less information which is good for

manager to take fast decision related to project. Skipsey Clifford Plc also takes fast

decision related to the equipment in which investment will be made in future (Roberts

and Weikmans, 2017).

Disadvantages of payback period:

This method is does not considers Time value of money which is important criteria for

all businesses as it helps to determine the changes in income which may take place in

future.

It only considers the cash flow which is used for recovering the initial investment.

Accounting rate of return – It means the return which is generated from dividing the

expected average annual profit from initial investment which come from deduct expenses and

then it is check with management rate of return is it is equal then it is accepted (Rompotis, 2017).

Advantages of ARR-

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This method provides clear picture of profitability analysis for the financial status of the

organization. In Skipsey Clifford Plc it shows that equipment is profitable for the

business or not by calculating the rate and then matching it with management rate.

This method used net income after deducting tax and depreciation, so the results that are

provided by it are more accurate from the methods which are using net cash inflow.

This method helps to determine ROI and return on capital employed on the given

project, ARR has similar concept with this. In Skipsey Clifford Plc it is used to calculate

ROI on machinery which will be purchased by the entity in future.

Disadvantage of ARR:

This method ignores time value of money because it includes only accounting reports. It

also avoids terminal value which is useful in capital budgeting techniques so the results

of it may get biased.

This method does not use external factor which mean it is does not use profit earning

capacity into action (Tran and et.al., 2017).

Net present value- It is a method which is used to analyse the actual present value of the

project which could be selected by the entity for the project of making investment. It begins with

cash flow then it is discounted with present factor to know that company should accept that

option or not if it is positive after deducting the cash outflow then it is acceptable. If the results

are negative, then it should not be selected by the businesses. The advantage and disadvantages

of it for Skipsey Clifford Plc are as follows:

Advantage of Net present value

This method uses time value of money for finding the rate of return because the value of

dollar today is more than tomorrow. In Skipsey Clifford Plc NPV is positive which mean

the project is acceptable in this net cash flow at discounting factor is used (Trigo, Belfo

and Estébanez, 2016 ).

This method is easy to use and it is best option to determine the project is acceptable or

not through calculation of discounted net cash inflow and then deducting it from cash

outflow.

Disadvantage of Net present value

9

organization. In Skipsey Clifford Plc it shows that equipment is profitable for the

business or not by calculating the rate and then matching it with management rate.

This method used net income after deducting tax and depreciation, so the results that are

provided by it are more accurate from the methods which are using net cash inflow.

This method helps to determine ROI and return on capital employed on the given

project, ARR has similar concept with this. In Skipsey Clifford Plc it is used to calculate

ROI on machinery which will be purchased by the entity in future.

Disadvantage of ARR:

This method ignores time value of money because it includes only accounting reports. It

also avoids terminal value which is useful in capital budgeting techniques so the results

of it may get biased.

This method does not use external factor which mean it is does not use profit earning

capacity into action (Tran and et.al., 2017).

Net present value- It is a method which is used to analyse the actual present value of the

project which could be selected by the entity for the project of making investment. It begins with

cash flow then it is discounted with present factor to know that company should accept that

option or not if it is positive after deducting the cash outflow then it is acceptable. If the results

are negative, then it should not be selected by the businesses. The advantage and disadvantages

of it for Skipsey Clifford Plc are as follows:

Advantage of Net present value

This method uses time value of money for finding the rate of return because the value of

dollar today is more than tomorrow. In Skipsey Clifford Plc NPV is positive which mean

the project is acceptable in this net cash flow at discounting factor is used (Trigo, Belfo

and Estébanez, 2016 ).

This method is easy to use and it is best option to determine the project is acceptable or

not through calculation of discounted net cash inflow and then deducting it from cash

outflow.

Disadvantage of Net present value

9

This method is not useful for comparing the project of different sizes, in net present

value cash flow is simply compared to capital outlay, it ignores future cost. It could only

be used to analyse that the project should be accepted or not.

This method sometimes finds difficulties in analysing the rate of return because

businesses doesn’t use the WACC as rate of return which is used as the hurdle rate.

c. Benefits and limitation of using budget as a tool for strategic planning

Budget is a type of financial plan which is used to by businesses for the purpose of making

sure that all the operational activities are executed in systematic manner. There are various types

of budgets that are used by different businesses. These are production, cash, sales, operating etc.

All of them have their own merits and demerits. The main purpose due to which these budgets

are used is strategic planning as with the help of budgets it will be very easy for businesses to

estimate future expenses and incomes. There are various benefits and limitations of using budget

as a tool for strategic planning (Vasilev, 2017). Discussion of all of them is as follows:

Benefits of using a budget: All the benefits of using a budget as strategic planning tool

are as follows:

With the help of budgets funds could be managed in systematic manner by the entities so

that the strategic plans could be executed properly in future.

Budgets help to monitor performance of the business that helps in strategic planning

because it can facilitate the formulation of effective strategies for future.

Limitations of using a budget: All the limitations of using a budget as strategic planning

tool are as follows:

The time which is taken for formulation of budget is very high therefore it may result in

ineffective planning of managers.

Another limitation of using budget as strategic planning tool is that it may affect the

attention of managers from their actual job which also affects their ability to take decision

for other activities.

CONCLUSION

From the above project report it has been concluded that finance and accounting are two

different aspects that are required to be focused by all the businesses as with the help of them

effective decisions for long term could be formulated. While planning to analyse financial

10

value cash flow is simply compared to capital outlay, it ignores future cost. It could only

be used to analyse that the project should be accepted or not.

This method sometimes finds difficulties in analysing the rate of return because

businesses doesn’t use the WACC as rate of return which is used as the hurdle rate.

c. Benefits and limitation of using budget as a tool for strategic planning

Budget is a type of financial plan which is used to by businesses for the purpose of making

sure that all the operational activities are executed in systematic manner. There are various types

of budgets that are used by different businesses. These are production, cash, sales, operating etc.

All of them have their own merits and demerits. The main purpose due to which these budgets

are used is strategic planning as with the help of budgets it will be very easy for businesses to

estimate future expenses and incomes. There are various benefits and limitations of using budget

as a tool for strategic planning (Vasilev, 2017). Discussion of all of them is as follows:

Benefits of using a budget: All the benefits of using a budget as strategic planning tool

are as follows:

With the help of budgets funds could be managed in systematic manner by the entities so

that the strategic plans could be executed properly in future.

Budgets help to monitor performance of the business that helps in strategic planning

because it can facilitate the formulation of effective strategies for future.

Limitations of using a budget: All the limitations of using a budget as strategic planning

tool are as follows:

The time which is taken for formulation of budget is very high therefore it may result in

ineffective planning of managers.

Another limitation of using budget as strategic planning tool is that it may affect the

attention of managers from their actual job which also affects their ability to take decision

for other activities.

CONCLUSION

From the above project report it has been concluded that finance and accounting are two

different aspects that are required to be focused by all the businesses as with the help of them

effective decisions for long term could be formulated. While planning to analyse financial

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.