Applied Accounting and Budgeting Project for Graduate Diploma (DAM561)

VerifiedAdded on 2023/05/29

|11

|2034

|474

Project

AI Summary

This project provides a comprehensive analysis of accounting and budgeting principles, addressing various aspects of financial management. It begins with inventory valuation using FIFO and average methods, followed by a discussion on financial statement compliance with NZ GAAP. The project then delves into flexible budgeting, variance analysis, and the calculation of the cost of capital, including WACC. Furthermore, it includes net present value calculations and explores production and material budgeting. The project utilizes financial data to demonstrate the application of these concepts, offering insights into decision-making and financial planning. Overall, the project is a detailed exploration of key accounting and budgeting topics, providing practical examples and calculations to support the understanding of financial concepts.

Running head: ACCOUNTING AND BUDGETING

Accounting and budgeting

Name of the student

Name of the university

Student ID

Author note

Accounting and budgeting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING AND BUDGETING

Table of Contents

Question 1..................................................................................................................................2

a) FIFO method...................................................................................................................2

b) Average method..............................................................................................................2

Question 3..................................................................................................................................4

Question 4..................................................................................................................................5

a) Cost of each source of finnace........................................................................................5

b) Capital structure weights.................................................................................................6

Question 5..................................................................................................................................7

1. Net cash flow...................................................................................................................7

2. Net present value.............................................................................................................7

Question 6..................................................................................................................................8

a) Production budget...........................................................................................................8

b) Material budget...............................................................................................................8

Reference..................................................................................................................................10

Table of Contents

Question 1..................................................................................................................................2

a) FIFO method...................................................................................................................2

b) Average method..............................................................................................................2

Question 3..................................................................................................................................4

Question 4..................................................................................................................................5

a) Cost of each source of finnace........................................................................................5

b) Capital structure weights.................................................................................................6

Question 5..................................................................................................................................7

1. Net cash flow...................................................................................................................7

2. Net present value.............................................................................................................7

Question 6..................................................................................................................................8

a) Production budget...........................................................................................................8

b) Material budget...............................................................................................................8

Reference..................................................................................................................................10

2ACCOUNTING AND BUDGETING

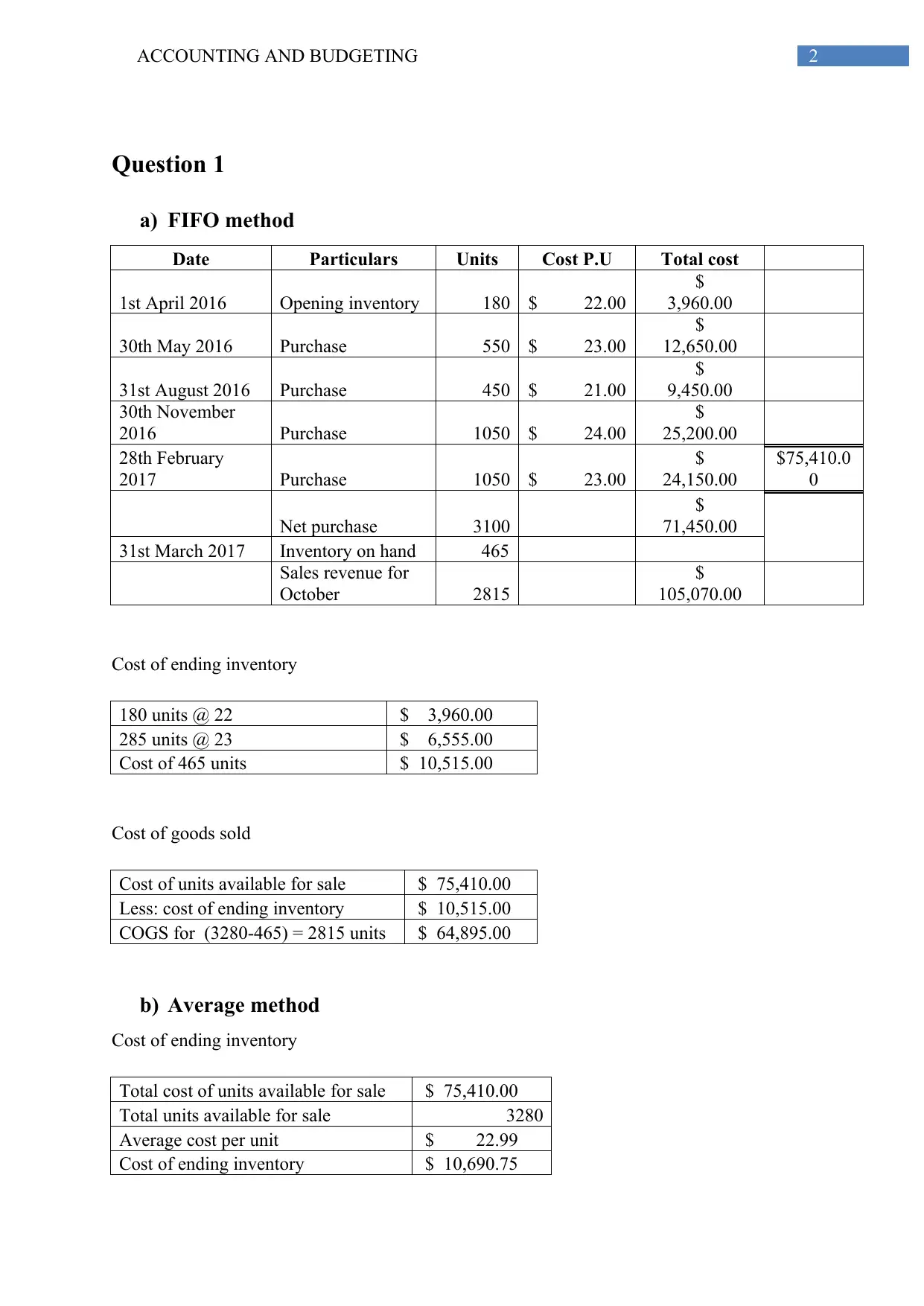

Question 1

a) FIFO method

Date Particulars Units Cost P.U Total cost

1st April 2016 Opening inventory 180 $ 22.00

$

3,960.00

30th May 2016 Purchase 550 $ 23.00

$

12,650.00

31st August 2016 Purchase 450 $ 21.00

$

9,450.00

30th November

2016 Purchase 1050 $ 24.00

$

25,200.00

28th February

2017 Purchase 1050 $ 23.00

$

24,150.00

$75,410.0

0

Net purchase 3100

$

71,450.00

31st March 2017 Inventory on hand 465

Sales revenue for

October 2815

$

105,070.00

Cost of ending inventory

180 units @ 22 $ 3,960.00

285 units @ 23 $ 6,555.00

Cost of 465 units $ 10,515.00

Cost of goods sold

Cost of units available for sale $ 75,410.00

Less: cost of ending inventory $ 10,515.00

COGS for (3280-465) = 2815 units $ 64,895.00

b) Average method

Cost of ending inventory

Total cost of units available for sale $ 75,410.00

Total units available for sale 3280

Average cost per unit $ 22.99

Cost of ending inventory $ 10,690.75

Question 1

a) FIFO method

Date Particulars Units Cost P.U Total cost

1st April 2016 Opening inventory 180 $ 22.00

$

3,960.00

30th May 2016 Purchase 550 $ 23.00

$

12,650.00

31st August 2016 Purchase 450 $ 21.00

$

9,450.00

30th November

2016 Purchase 1050 $ 24.00

$

25,200.00

28th February

2017 Purchase 1050 $ 23.00

$

24,150.00

$75,410.0

0

Net purchase 3100

$

71,450.00

31st March 2017 Inventory on hand 465

Sales revenue for

October 2815

$

105,070.00

Cost of ending inventory

180 units @ 22 $ 3,960.00

285 units @ 23 $ 6,555.00

Cost of 465 units $ 10,515.00

Cost of goods sold

Cost of units available for sale $ 75,410.00

Less: cost of ending inventory $ 10,515.00

COGS for (3280-465) = 2815 units $ 64,895.00

b) Average method

Cost of ending inventory

Total cost of units available for sale $ 75,410.00

Total units available for sale 3280

Average cost per unit $ 22.99

Cost of ending inventory $ 10,690.75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING AND BUDGETING

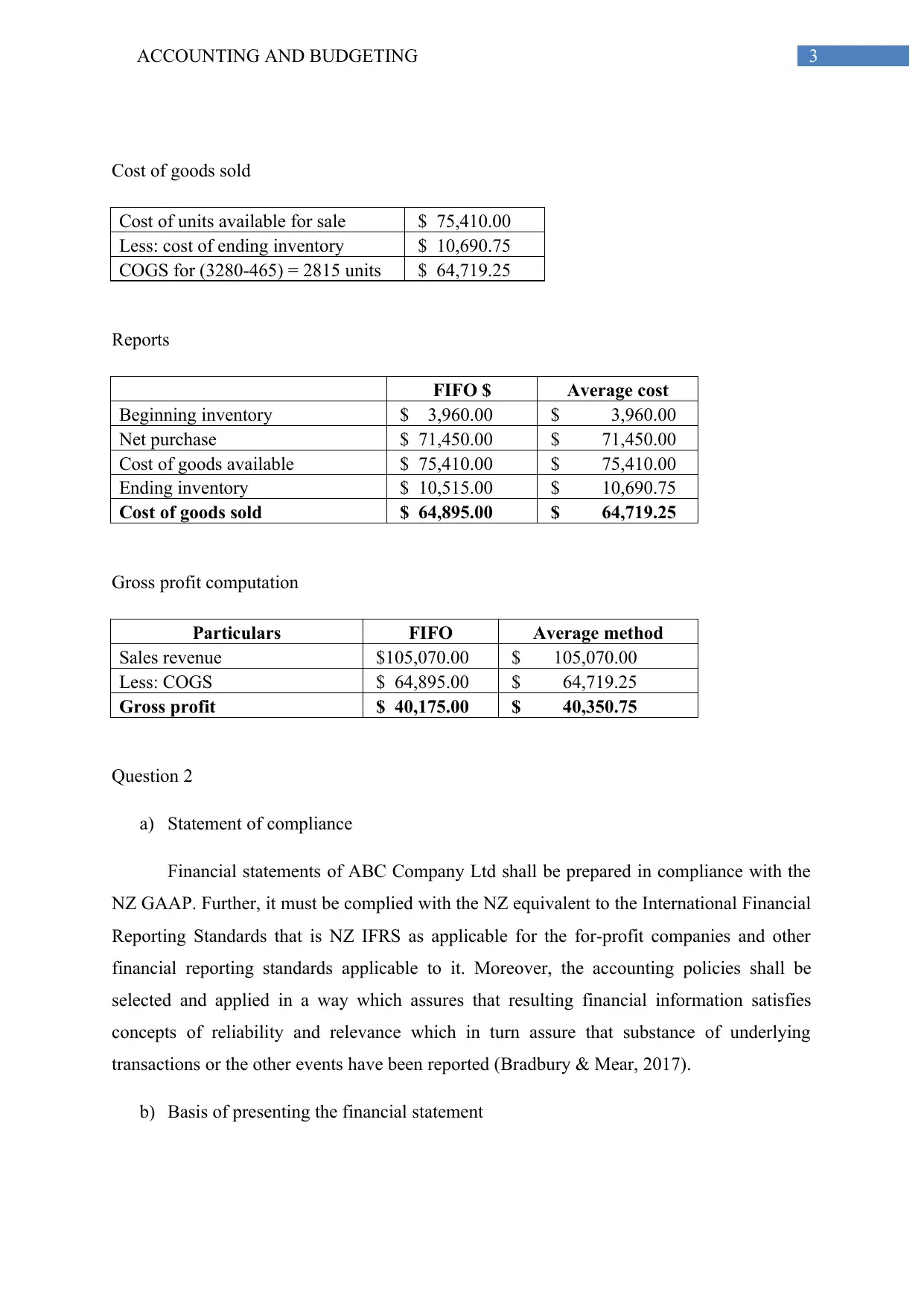

Cost of goods sold

Cost of units available for sale $ 75,410.00

Less: cost of ending inventory $ 10,690.75

COGS for (3280-465) = 2815 units $ 64,719.25

Reports

FIFO $ Average cost

Beginning inventory $ 3,960.00 $ 3,960.00

Net purchase $ 71,450.00 $ 71,450.00

Cost of goods available $ 75,410.00 $ 75,410.00

Ending inventory $ 10,515.00 $ 10,690.75

Cost of goods sold $ 64,895.00 $ 64,719.25

Gross profit computation

Particulars FIFO Average method

Sales revenue $105,070.00 $ 105,070.00

Less: COGS $ 64,895.00 $ 64,719.25

Gross profit $ 40,175.00 $ 40,350.75

Question 2

a) Statement of compliance

Financial statements of ABC Company Ltd shall be prepared in compliance with the

NZ GAAP. Further, it must be complied with the NZ equivalent to the International Financial

Reporting Standards that is NZ IFRS as applicable for the for-profit companies and other

financial reporting standards applicable to it. Moreover, the accounting policies shall be

selected and applied in a way which assures that resulting financial information satisfies

concepts of reliability and relevance which in turn assure that substance of underlying

transactions or the other events have been reported (Bradbury & Mear, 2017).

b) Basis of presenting the financial statement

Cost of goods sold

Cost of units available for sale $ 75,410.00

Less: cost of ending inventory $ 10,690.75

COGS for (3280-465) = 2815 units $ 64,719.25

Reports

FIFO $ Average cost

Beginning inventory $ 3,960.00 $ 3,960.00

Net purchase $ 71,450.00 $ 71,450.00

Cost of goods available $ 75,410.00 $ 75,410.00

Ending inventory $ 10,515.00 $ 10,690.75

Cost of goods sold $ 64,895.00 $ 64,719.25

Gross profit computation

Particulars FIFO Average method

Sales revenue $105,070.00 $ 105,070.00

Less: COGS $ 64,895.00 $ 64,719.25

Gross profit $ 40,175.00 $ 40,350.75

Question 2

a) Statement of compliance

Financial statements of ABC Company Ltd shall be prepared in compliance with the

NZ GAAP. Further, it must be complied with the NZ equivalent to the International Financial

Reporting Standards that is NZ IFRS as applicable for the for-profit companies and other

financial reporting standards applicable to it. Moreover, the accounting policies shall be

selected and applied in a way which assures that resulting financial information satisfies

concepts of reliability and relevance which in turn assure that substance of underlying

transactions or the other events have been reported (Bradbury & Mear, 2017).

b) Basis of presenting the financial statement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING AND BUDGETING

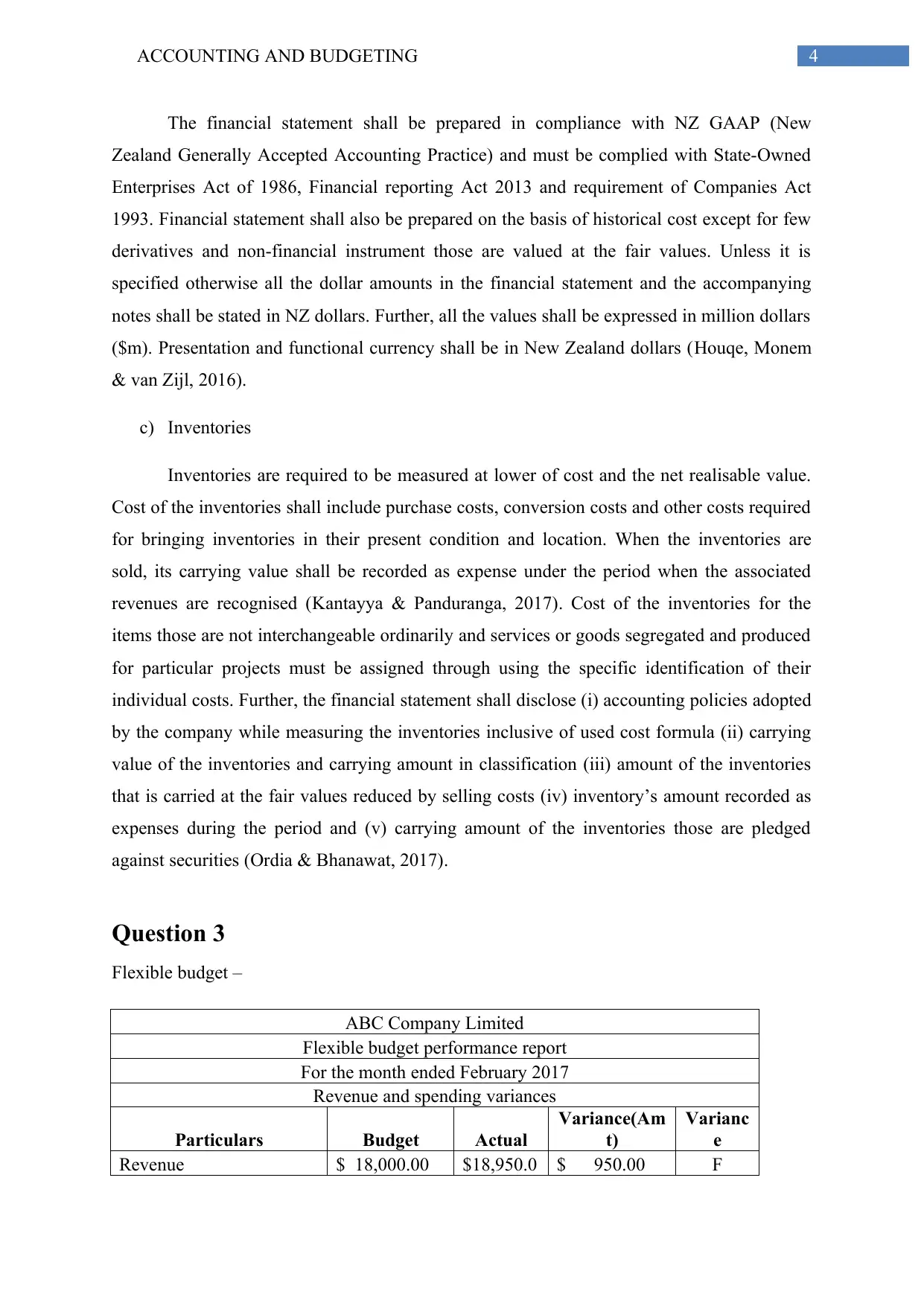

The financial statement shall be prepared in compliance with NZ GAAP (New

Zealand Generally Accepted Accounting Practice) and must be complied with State-Owned

Enterprises Act of 1986, Financial reporting Act 2013 and requirement of Companies Act

1993. Financial statement shall also be prepared on the basis of historical cost except for few

derivatives and non-financial instrument those are valued at the fair values. Unless it is

specified otherwise all the dollar amounts in the financial statement and the accompanying

notes shall be stated in NZ dollars. Further, all the values shall be expressed in million dollars

($m). Presentation and functional currency shall be in New Zealand dollars (Houqe, Monem

& van Zijl, 2016).

c) Inventories

Inventories are required to be measured at lower of cost and the net realisable value.

Cost of the inventories shall include purchase costs, conversion costs and other costs required

for bringing inventories in their present condition and location. When the inventories are

sold, its carrying value shall be recorded as expense under the period when the associated

revenues are recognised (Kantayya & Panduranga, 2017). Cost of the inventories for the

items those are not interchangeable ordinarily and services or goods segregated and produced

for particular projects must be assigned through using the specific identification of their

individual costs. Further, the financial statement shall disclose (i) accounting policies adopted

by the company while measuring the inventories inclusive of used cost formula (ii) carrying

value of the inventories and carrying amount in classification (iii) amount of the inventories

that is carried at the fair values reduced by selling costs (iv) inventory’s amount recorded as

expenses during the period and (v) carrying amount of the inventories those are pledged

against securities (Ordia & Bhanawat, 2017).

Question 3

Flexible budget –

ABC Company Limited

Flexible budget performance report

For the month ended February 2017

Revenue and spending variances

Particulars Budget Actual

Variance(Am

t)

Varianc

e

Revenue $ 18,000.00 $18,950.0 $ 950.00 F

The financial statement shall be prepared in compliance with NZ GAAP (New

Zealand Generally Accepted Accounting Practice) and must be complied with State-Owned

Enterprises Act of 1986, Financial reporting Act 2013 and requirement of Companies Act

1993. Financial statement shall also be prepared on the basis of historical cost except for few

derivatives and non-financial instrument those are valued at the fair values. Unless it is

specified otherwise all the dollar amounts in the financial statement and the accompanying

notes shall be stated in NZ dollars. Further, all the values shall be expressed in million dollars

($m). Presentation and functional currency shall be in New Zealand dollars (Houqe, Monem

& van Zijl, 2016).

c) Inventories

Inventories are required to be measured at lower of cost and the net realisable value.

Cost of the inventories shall include purchase costs, conversion costs and other costs required

for bringing inventories in their present condition and location. When the inventories are

sold, its carrying value shall be recorded as expense under the period when the associated

revenues are recognised (Kantayya & Panduranga, 2017). Cost of the inventories for the

items those are not interchangeable ordinarily and services or goods segregated and produced

for particular projects must be assigned through using the specific identification of their

individual costs. Further, the financial statement shall disclose (i) accounting policies adopted

by the company while measuring the inventories inclusive of used cost formula (ii) carrying

value of the inventories and carrying amount in classification (iii) amount of the inventories

that is carried at the fair values reduced by selling costs (iv) inventory’s amount recorded as

expenses during the period and (v) carrying amount of the inventories those are pledged

against securities (Ordia & Bhanawat, 2017).

Question 3

Flexible budget –

ABC Company Limited

Flexible budget performance report

For the month ended February 2017

Revenue and spending variances

Particulars Budget Actual

Variance(Am

t)

Varianc

e

Revenue $ 18,000.00 $18,950.0 $ 950.00 F

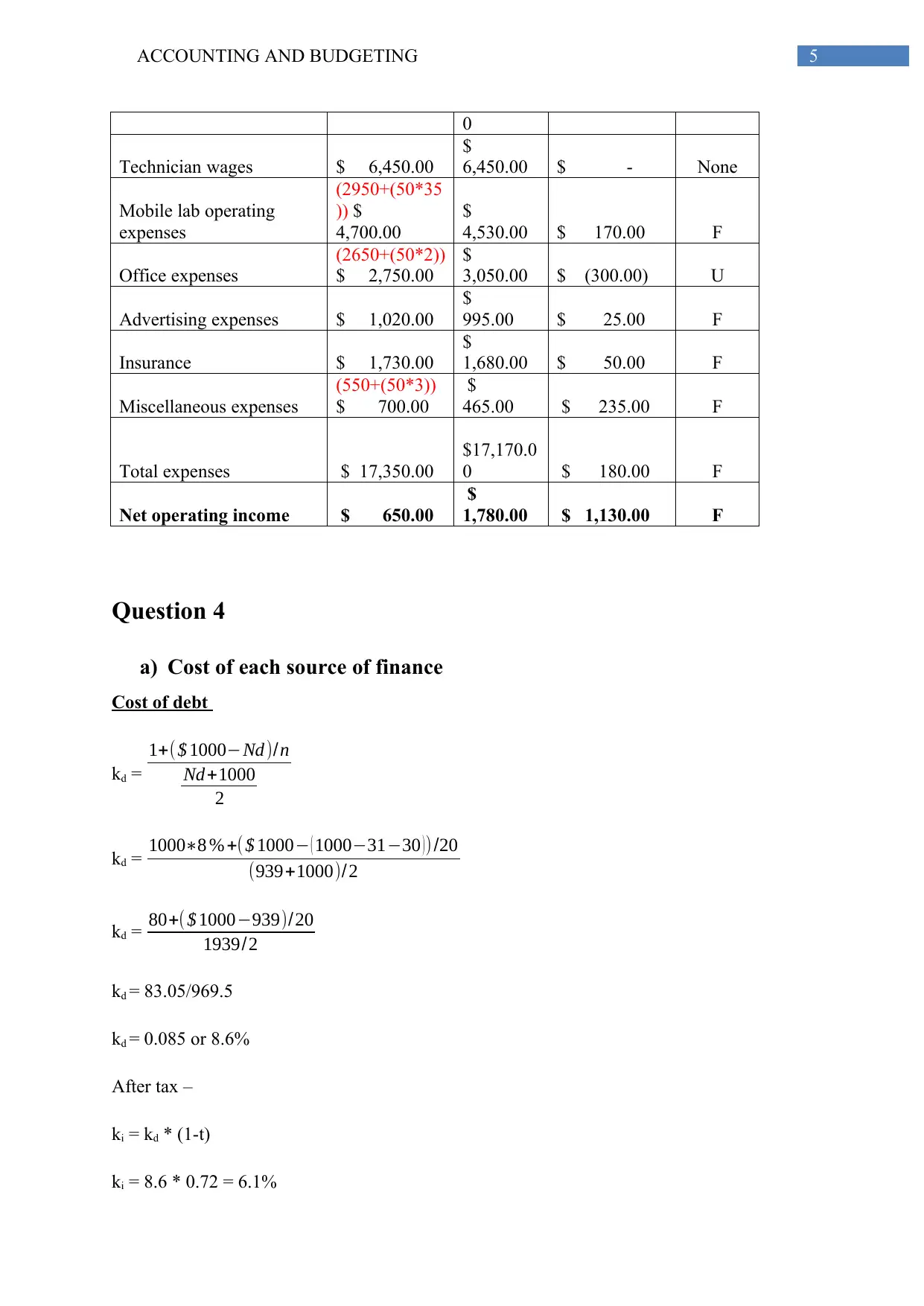

5ACCOUNTING AND BUDGETING

0

Technician wages $ 6,450.00

$

6,450.00 $ - None

Mobile lab operating

expenses

(2950+(50*35

)) $

4,700.00

$

4,530.00 $ 170.00 F

Office expenses

(2650+(50*2))

$ 2,750.00

$

3,050.00 $ (300.00) U

Advertising expenses $ 1,020.00

$

995.00 $ 25.00 F

Insurance $ 1,730.00

$

1,680.00 $ 50.00 F

Miscellaneous expenses

(550+(50*3))

$ 700.00

$

465.00 $ 235.00 F

Total expenses $ 17,350.00

$17,170.0

0 $ 180.00 F

Net operating income $ 650.00

$

1,780.00 $ 1,130.00 F

Question 4

a) Cost of each source of finance

Cost of debt

kd =

1+($ 1000−Nd)/n

Nd+1000

2

kd = 1000∗8 % +( $ 1000− ( 1000−31−30 )) /20

(939+1000)/2

kd = 80+( $ 1000−939)/20

1939/2

kd = 83.05/969.5

kd = 0.085 or 8.6%

After tax –

ki = kd * (1-t)

ki = 8.6 * 0.72 = 6.1%

0

Technician wages $ 6,450.00

$

6,450.00 $ - None

Mobile lab operating

expenses

(2950+(50*35

)) $

4,700.00

$

4,530.00 $ 170.00 F

Office expenses

(2650+(50*2))

$ 2,750.00

$

3,050.00 $ (300.00) U

Advertising expenses $ 1,020.00

$

995.00 $ 25.00 F

Insurance $ 1,730.00

$

1,680.00 $ 50.00 F

Miscellaneous expenses

(550+(50*3))

$ 700.00

$

465.00 $ 235.00 F

Total expenses $ 17,350.00

$17,170.0

0 $ 180.00 F

Net operating income $ 650.00

$

1,780.00 $ 1,130.00 F

Question 4

a) Cost of each source of finance

Cost of debt

kd =

1+($ 1000−Nd)/n

Nd+1000

2

kd = 1000∗8 % +( $ 1000− ( 1000−31−30 )) /20

(939+1000)/2

kd = 80+( $ 1000−939)/20

1939/2

kd = 83.05/969.5

kd = 0.085 or 8.6%

After tax –

ki = kd * (1-t)

ki = 8.6 * 0.72 = 6.1%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING AND BUDGETING

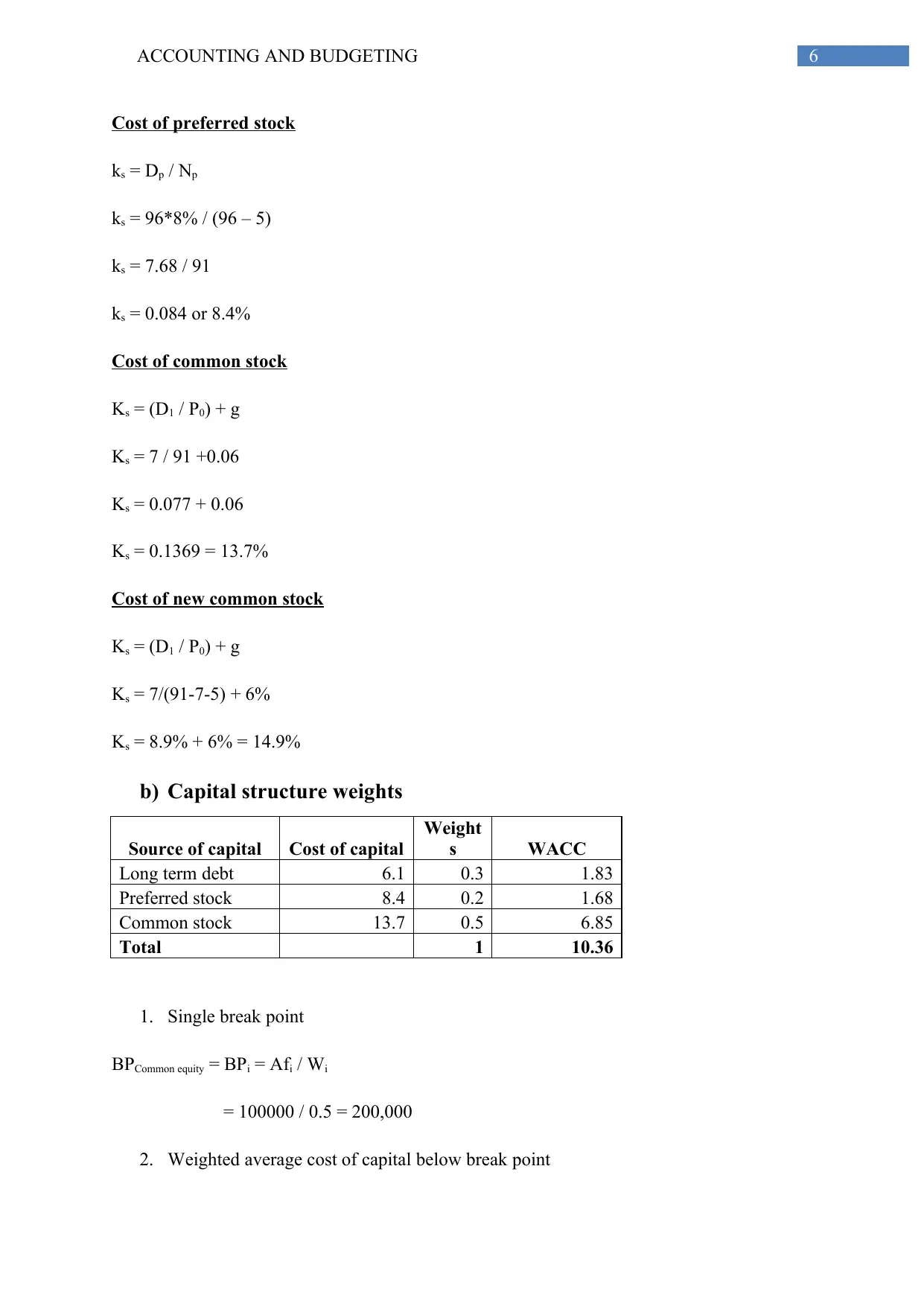

Cost of preferred stock

ks = Dp / Np

ks = 96*8% / (96 – 5)

ks = 7.68 / 91

ks = 0.084 or 8.4%

Cost of common stock

Ks = (D1 / P0) + g

Ks = 7 / 91 +0.06

Ks = 0.077 + 0.06

Ks = 0.1369 = 13.7%

Cost of new common stock

Ks = (D1 / P0) + g

Ks = 7/(91-7-5) + 6%

Ks = 8.9% + 6% = 14.9%

b) Capital structure weights

Source of capital Cost of capital

Weight

s WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 13.7 0.5 6.85

Total 1 10.36

1. Single break point

BPCommon equity = BPi = Afi / Wi

= 100000 / 0.5 = 200,000

2. Weighted average cost of capital below break point

Cost of preferred stock

ks = Dp / Np

ks = 96*8% / (96 – 5)

ks = 7.68 / 91

ks = 0.084 or 8.4%

Cost of common stock

Ks = (D1 / P0) + g

Ks = 7 / 91 +0.06

Ks = 0.077 + 0.06

Ks = 0.1369 = 13.7%

Cost of new common stock

Ks = (D1 / P0) + g

Ks = 7/(91-7-5) + 6%

Ks = 8.9% + 6% = 14.9%

b) Capital structure weights

Source of capital Cost of capital

Weight

s WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 13.7 0.5 6.85

Total 1 10.36

1. Single break point

BPCommon equity = BPi = Afi / Wi

= 100000 / 0.5 = 200,000

2. Weighted average cost of capital below break point

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING AND BUDGETING

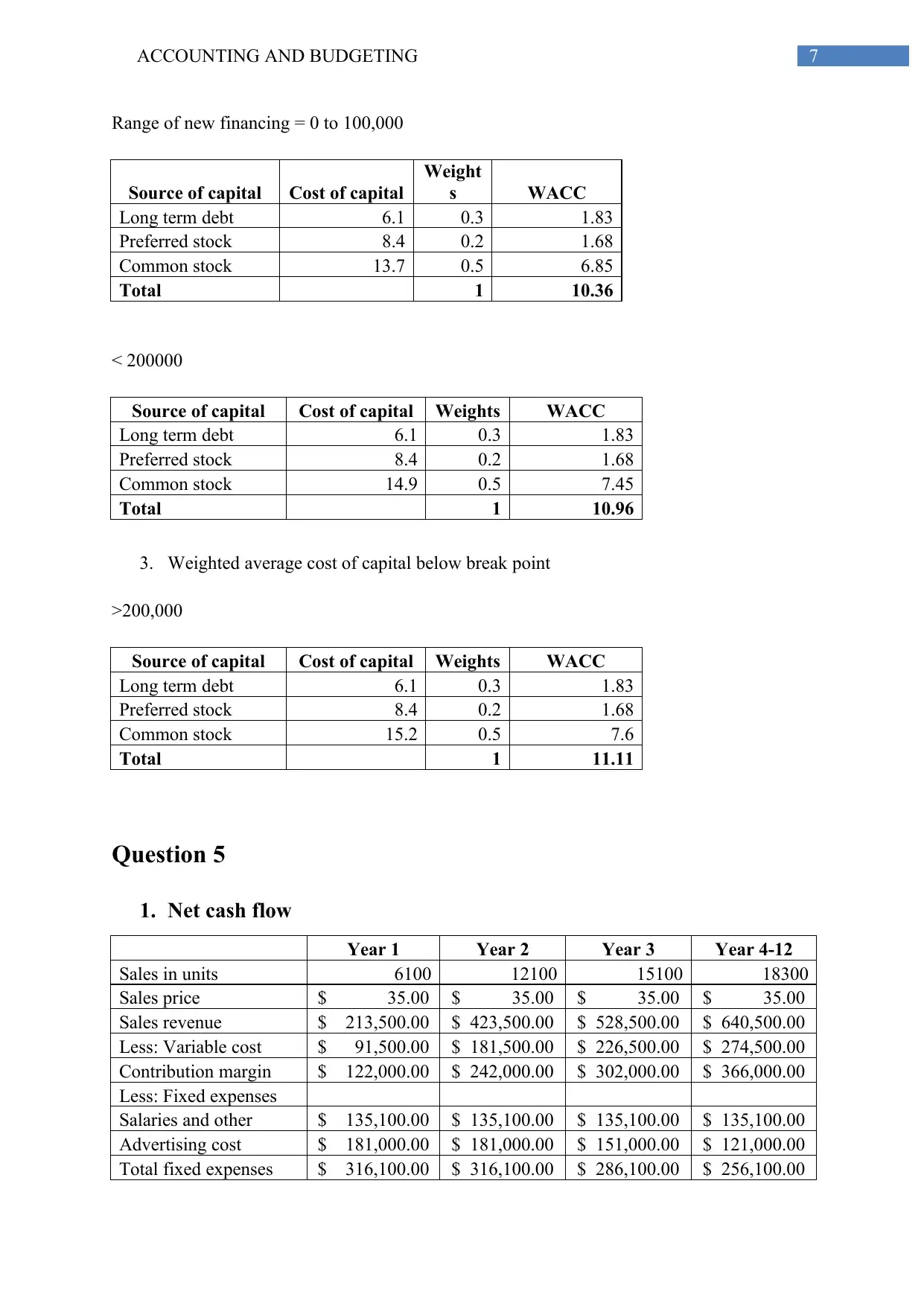

Range of new financing = 0 to 100,000

Source of capital Cost of capital

Weight

s WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 13.7 0.5 6.85

Total 1 10.36

< 200000

Source of capital Cost of capital Weights WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 14.9 0.5 7.45

Total 1 10.96

3. Weighted average cost of capital below break point

>200,000

Source of capital Cost of capital Weights WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 15.2 0.5 7.6

Total 1 11.11

Question 5

1. Net cash flow

Year 1 Year 2 Year 3 Year 4-12

Sales in units 6100 12100 15100 18300

Sales price $ 35.00 $ 35.00 $ 35.00 $ 35.00

Sales revenue $ 213,500.00 $ 423,500.00 $ 528,500.00 $ 640,500.00

Less: Variable cost $ 91,500.00 $ 181,500.00 $ 226,500.00 $ 274,500.00

Contribution margin $ 122,000.00 $ 242,000.00 $ 302,000.00 $ 366,000.00

Less: Fixed expenses

Salaries and other $ 135,100.00 $ 135,100.00 $ 135,100.00 $ 135,100.00

Advertising cost $ 181,000.00 $ 181,000.00 $ 151,000.00 $ 121,000.00

Total fixed expenses $ 316,100.00 $ 316,100.00 $ 286,100.00 $ 256,100.00

Range of new financing = 0 to 100,000

Source of capital Cost of capital

Weight

s WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 13.7 0.5 6.85

Total 1 10.36

< 200000

Source of capital Cost of capital Weights WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 14.9 0.5 7.45

Total 1 10.96

3. Weighted average cost of capital below break point

>200,000

Source of capital Cost of capital Weights WACC

Long term debt 6.1 0.3 1.83

Preferred stock 8.4 0.2 1.68

Common stock 15.2 0.5 7.6

Total 1 11.11

Question 5

1. Net cash flow

Year 1 Year 2 Year 3 Year 4-12

Sales in units 6100 12100 15100 18300

Sales price $ 35.00 $ 35.00 $ 35.00 $ 35.00

Sales revenue $ 213,500.00 $ 423,500.00 $ 528,500.00 $ 640,500.00

Less: Variable cost $ 91,500.00 $ 181,500.00 $ 226,500.00 $ 274,500.00

Contribution margin $ 122,000.00 $ 242,000.00 $ 302,000.00 $ 366,000.00

Less: Fixed expenses

Salaries and other $ 135,100.00 $ 135,100.00 $ 135,100.00 $ 135,100.00

Advertising cost $ 181,000.00 $ 181,000.00 $ 151,000.00 $ 121,000.00

Total fixed expenses $ 316,100.00 $ 316,100.00 $ 286,100.00 $ 256,100.00

8ACCOUNTING AND BUDGETING

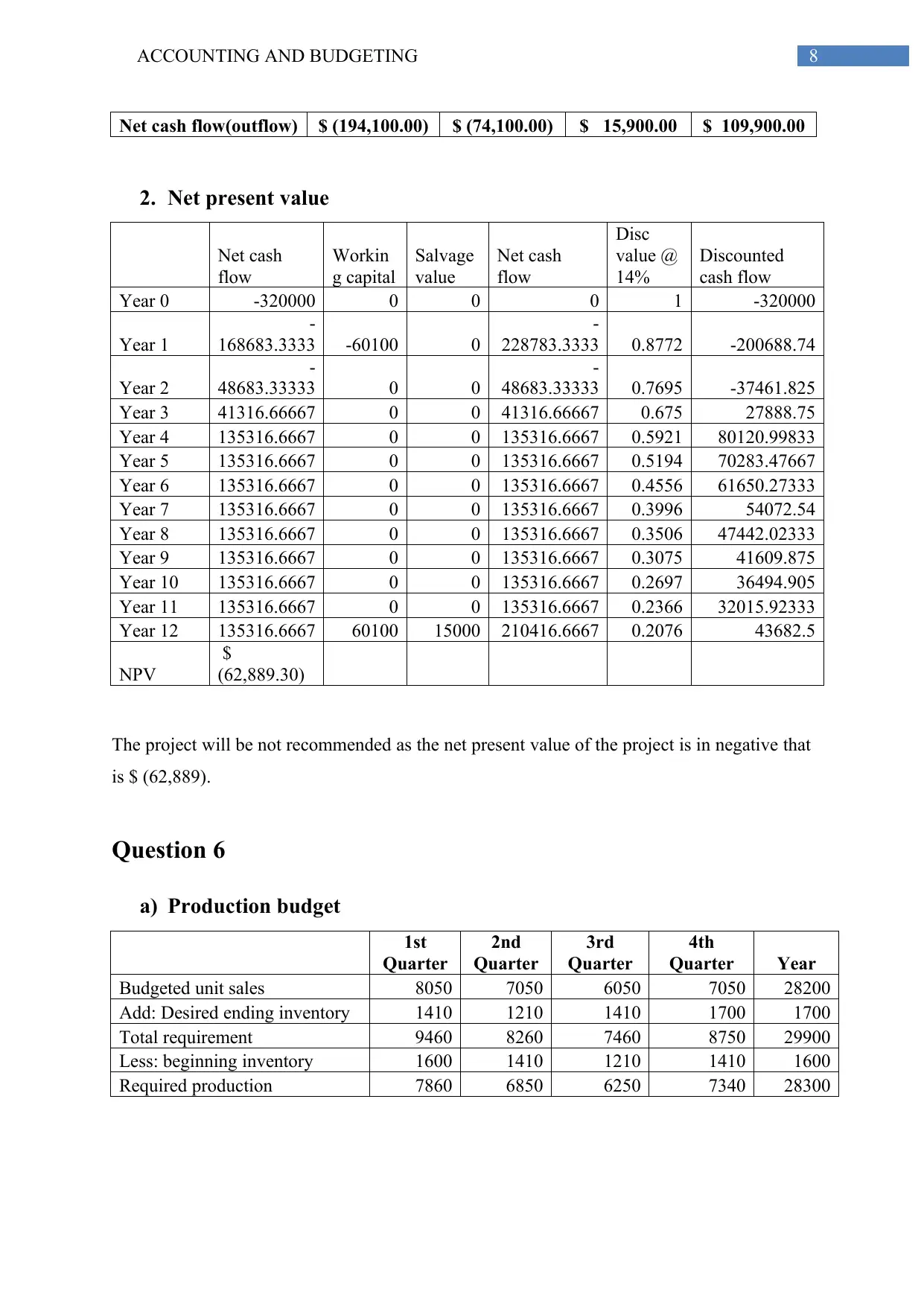

Net cash flow(outflow) $ (194,100.00) $ (74,100.00) $ 15,900.00 $ 109,900.00

2. Net present value

Net cash

flow

Workin

g capital

Salvage

value

Net cash

flow

Disc

value @

14%

Discounted

cash flow

Year 0 -320000 0 0 0 1 -320000

Year 1

-

168683.3333 -60100 0

-

228783.3333 0.8772 -200688.74

Year 2

-

48683.33333 0 0

-

48683.33333 0.7695 -37461.825

Year 3 41316.66667 0 0 41316.66667 0.675 27888.75

Year 4 135316.6667 0 0 135316.6667 0.5921 80120.99833

Year 5 135316.6667 0 0 135316.6667 0.5194 70283.47667

Year 6 135316.6667 0 0 135316.6667 0.4556 61650.27333

Year 7 135316.6667 0 0 135316.6667 0.3996 54072.54

Year 8 135316.6667 0 0 135316.6667 0.3506 47442.02333

Year 9 135316.6667 0 0 135316.6667 0.3075 41609.875

Year 10 135316.6667 0 0 135316.6667 0.2697 36494.905

Year 11 135316.6667 0 0 135316.6667 0.2366 32015.92333

Year 12 135316.6667 60100 15000 210416.6667 0.2076 43682.5

NPV

$

(62,889.30)

The project will be not recommended as the net present value of the project is in negative that

is $ (62,889).

Question 6

a) Production budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter Year

Budgeted unit sales 8050 7050 6050 7050 28200

Add: Desired ending inventory 1410 1210 1410 1700 1700

Total requirement 9460 8260 7460 8750 29900

Less: beginning inventory 1600 1410 1210 1410 1600

Required production 7860 6850 6250 7340 28300

Net cash flow(outflow) $ (194,100.00) $ (74,100.00) $ 15,900.00 $ 109,900.00

2. Net present value

Net cash

flow

Workin

g capital

Salvage

value

Net cash

flow

Disc

value @

14%

Discounted

cash flow

Year 0 -320000 0 0 0 1 -320000

Year 1

-

168683.3333 -60100 0

-

228783.3333 0.8772 -200688.74

Year 2

-

48683.33333 0 0

-

48683.33333 0.7695 -37461.825

Year 3 41316.66667 0 0 41316.66667 0.675 27888.75

Year 4 135316.6667 0 0 135316.6667 0.5921 80120.99833

Year 5 135316.6667 0 0 135316.6667 0.5194 70283.47667

Year 6 135316.6667 0 0 135316.6667 0.4556 61650.27333

Year 7 135316.6667 0 0 135316.6667 0.3996 54072.54

Year 8 135316.6667 0 0 135316.6667 0.3506 47442.02333

Year 9 135316.6667 0 0 135316.6667 0.3075 41609.875

Year 10 135316.6667 0 0 135316.6667 0.2697 36494.905

Year 11 135316.6667 0 0 135316.6667 0.2366 32015.92333

Year 12 135316.6667 60100 15000 210416.6667 0.2076 43682.5

NPV

$

(62,889.30)

The project will be not recommended as the net present value of the project is in negative that

is $ (62,889).

Question 6

a) Production budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter Year

Budgeted unit sales 8050 7050 6050 7050 28200

Add: Desired ending inventory 1410 1210 1410 1700 1700

Total requirement 9460 8260 7460 8750 29900

Less: beginning inventory 1600 1410 1210 1410 1600

Required production 7860 6850 6250 7340 28300

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING AND BUDGETING

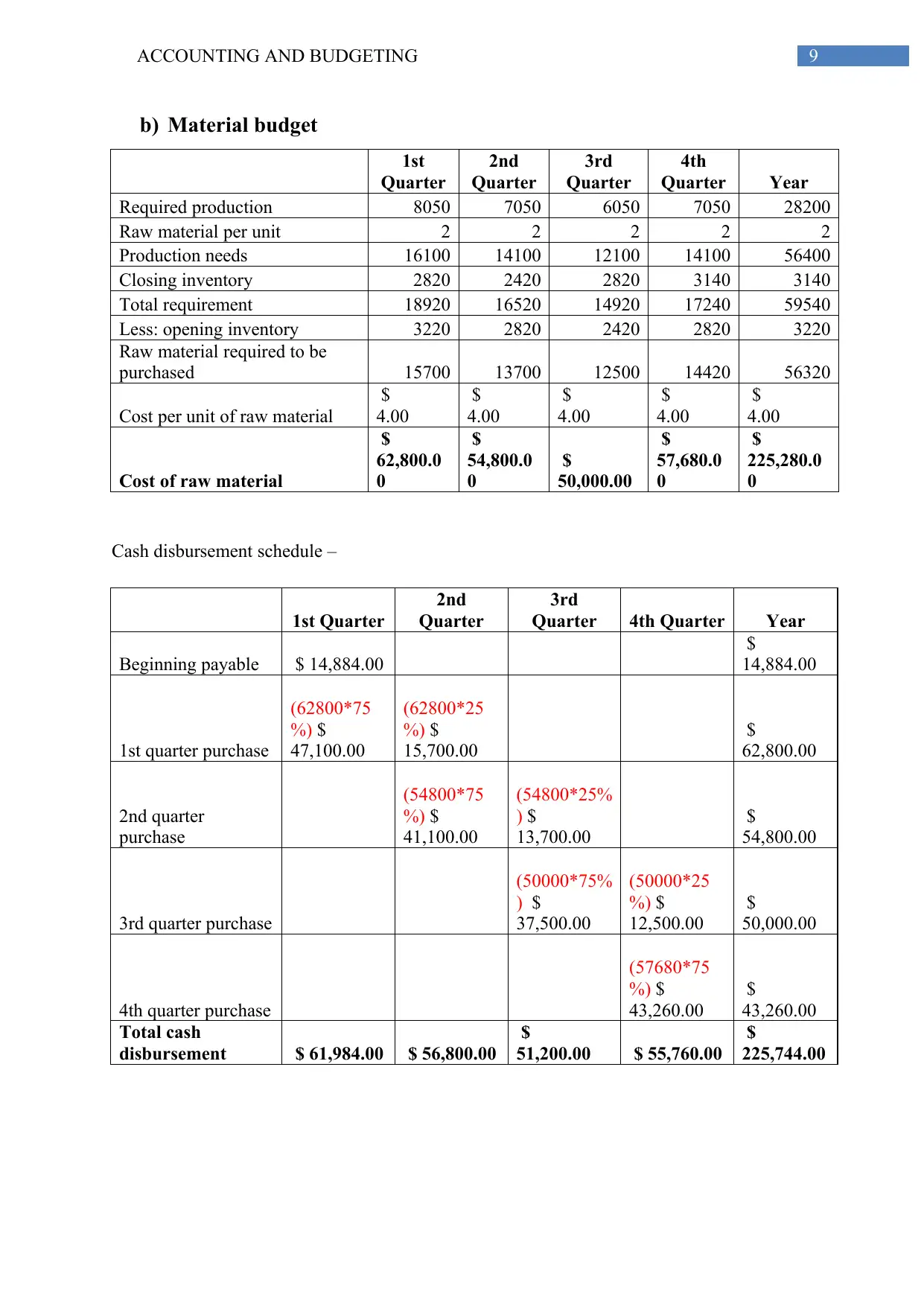

b) Material budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter Year

Required production 8050 7050 6050 7050 28200

Raw material per unit 2 2 2 2 2

Production needs 16100 14100 12100 14100 56400

Closing inventory 2820 2420 2820 3140 3140

Total requirement 18920 16520 14920 17240 59540

Less: opening inventory 3220 2820 2420 2820 3220

Raw material required to be

purchased 15700 13700 12500 14420 56320

Cost per unit of raw material

$

4.00

$

4.00

$

4.00

$

4.00

$

4.00

Cost of raw material

$

62,800.0

0

$

54,800.0

0

$

50,000.00

$

57,680.0

0

$

225,280.0

0

Cash disbursement schedule –

1st Quarter

2nd

Quarter

3rd

Quarter 4th Quarter Year

Beginning payable $ 14,884.00

$

14,884.00

1st quarter purchase

(62800*75

%) $

47,100.00

(62800*25

%) $

15,700.00

$

62,800.00

2nd quarter

purchase

(54800*75

%) $

41,100.00

(54800*25%

) $

13,700.00

$

54,800.00

3rd quarter purchase

(50000*75%

) $

37,500.00

(50000*25

%) $

12,500.00

$

50,000.00

4th quarter purchase

(57680*75

%) $

43,260.00

$

43,260.00

Total cash

disbursement $ 61,984.00 $ 56,800.00

$

51,200.00 $ 55,760.00

$

225,744.00

b) Material budget

1st

Quarter

2nd

Quarter

3rd

Quarter

4th

Quarter Year

Required production 8050 7050 6050 7050 28200

Raw material per unit 2 2 2 2 2

Production needs 16100 14100 12100 14100 56400

Closing inventory 2820 2420 2820 3140 3140

Total requirement 18920 16520 14920 17240 59540

Less: opening inventory 3220 2820 2420 2820 3220

Raw material required to be

purchased 15700 13700 12500 14420 56320

Cost per unit of raw material

$

4.00

$

4.00

$

4.00

$

4.00

$

4.00

Cost of raw material

$

62,800.0

0

$

54,800.0

0

$

50,000.00

$

57,680.0

0

$

225,280.0

0

Cash disbursement schedule –

1st Quarter

2nd

Quarter

3rd

Quarter 4th Quarter Year

Beginning payable $ 14,884.00

$

14,884.00

1st quarter purchase

(62800*75

%) $

47,100.00

(62800*25

%) $

15,700.00

$

62,800.00

2nd quarter

purchase

(54800*75

%) $

41,100.00

(54800*25%

) $

13,700.00

$

54,800.00

3rd quarter purchase

(50000*75%

) $

37,500.00

(50000*25

%) $

12,500.00

$

50,000.00

4th quarter purchase

(57680*75

%) $

43,260.00

$

43,260.00

Total cash

disbursement $ 61,984.00 $ 56,800.00

$

51,200.00 $ 55,760.00

$

225,744.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING AND BUDGETING

Reference

Bradbury, M. E., & Mear, K. M. (2017). Interpreting the Impact of IFRS

Adoption. Australian Accounting Review, 27(2), 214-219.

Houqe, M. N., Monem, R. M., & van Zijl, T. (2016). The economic consequences of IFRS

adoption: evidence from New Zealand. Journal of International Accounting, Auditing

and Taxation, 27, 40-48.

Kantayya, R., & Panduranga, V. (2017). A Comparative Study of Balance Sheets Prepared

under Indian GAAP and IFRS with Special Reference to Select IT

Companies. Europe, 44, 29.

Ordia, S., & Bhanawat, S. S. (2017). The Impact of Adoption of IFRS on Shareholders'

Wealth: A Study of Select Indian Companies. IUP Journal of Accounting Research &

Audit Practices, 16(2), 7.

Reference

Bradbury, M. E., & Mear, K. M. (2017). Interpreting the Impact of IFRS

Adoption. Australian Accounting Review, 27(2), 214-219.

Houqe, M. N., Monem, R. M., & van Zijl, T. (2016). The economic consequences of IFRS

adoption: evidence from New Zealand. Journal of International Accounting, Auditing

and Taxation, 27, 40-48.

Kantayya, R., & Panduranga, V. (2017). A Comparative Study of Balance Sheets Prepared

under Indian GAAP and IFRS with Special Reference to Select IT

Companies. Europe, 44, 29.

Ordia, S., & Bhanawat, S. S. (2017). The Impact of Adoption of IFRS on Shareholders'

Wealth: A Study of Select Indian Companies. IUP Journal of Accounting Research &

Audit Practices, 16(2), 7.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.